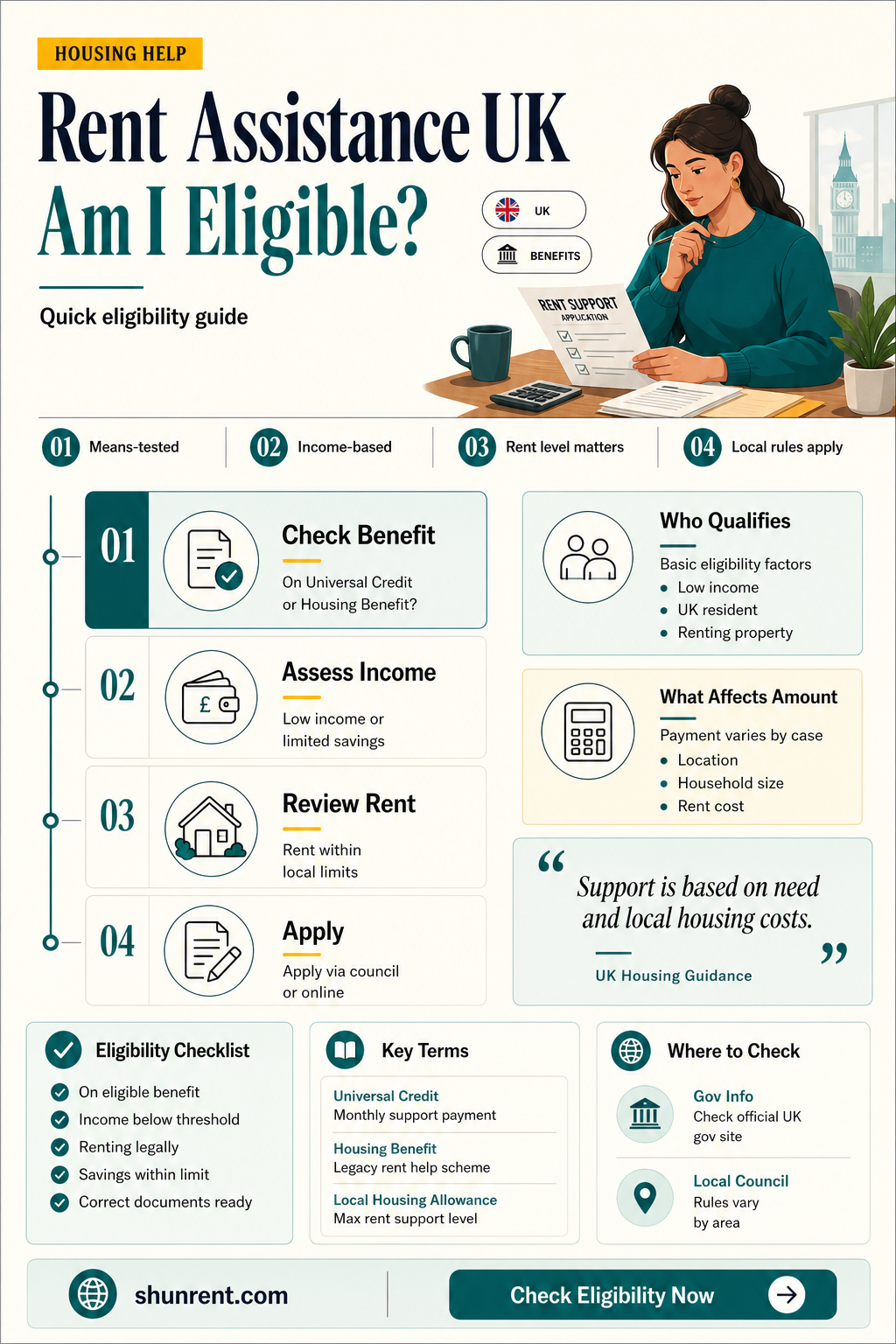

In the UK, many individuals and families may find themselves struggling to meet the rising costs of rent, prompting the question: Am I entitled to rent assistance? The UK government offers several schemes to help eligible residents with housing costs, including Housing Benefit for those on a low income or claiming other benefits, and Universal Credit, which includes a housing element for renters. Eligibility for these programs depends on factors such as income, savings, the size of your household, and the type of tenancy you have. Additionally, local councils may provide Discretionary Housing Payments (DHPs) to cover shortfalls in rent not met by benefits. Understanding the criteria and application processes for these forms of assistance is crucial for anyone facing financial difficulties with their housing expenses.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Must be on a low income, receiving benefits, or have housing costs. |

| Applicable Benefits | Universal Credit, Housing Benefit, Income Support, Pension Credit, etc. |

| Age Requirement | No specific age limit; applies to working-age and pension-age individuals. |

| Residency Status | Must be a UK resident with a right to reside in the UK. |

| Housing Type | Applies to private rented, social housing, and some types of supported housing. |

| Income Threshold | Varies based on location, household size, and circumstances. |

| Savings Limit | £16,000 or more in savings may affect eligibility. |

| Rent Assistance Types | Housing Benefit (for those on legacy benefits) and Housing Element of Universal Credit. |

| Local Housing Allowance (LHA) | Caps rent assistance based on local rent rates and household size. |

| Application Process | Apply through Universal Credit or Housing Benefit, depending on circumstances. |

| Frequency of Payments | Usually paid monthly, directly to the tenant or landlord. |

| Additional Support | Discretionary Housing Payments (DHP) available in some cases for extra help. |

| Changes in Circumstances | Must report changes (e.g., income, household size) to avoid overpayments. |

| Taxable Benefit | Rent assistance is not taxable. |

| Impact on Other Benefits | May affect eligibility for other means-tested benefits. |

| Regional Variations | Rates and eligibility may vary slightly in Scotland, Wales, and Northern Ireland. |

| Latest Updates (as of 2023) | No significant changes; rates adjusted annually based on inflation. |

Explore related products

$42.55 $55.99

$150 $46.99

What You'll Learn

- Eligibility Criteria: Income limits, benefits status, and residency requirements for rent assistance in the UK

- Housing Benefit: Financial aid for private or social housing tenants based on income

- Universal Credit: Rent support through Universal Credit for eligible low-income households

- Discretionary Housing Payments: Extra help for rent shortfalls in specific circumstances

- Local Council Schemes: Regional rent assistance programs and application processes in the UK

![]()

Eligibility Criteria: Income limits, benefits status, and residency requirements for rent assistance in the UK

Understanding whether you qualify for rent assistance in the UK hinges on three critical eligibility criteria: income limits, benefits status, and residency requirements. Each of these factors is meticulously assessed to ensure that support reaches those most in need. For instance, Housing Benefit and Universal Credit, the two primary forms of rent assistance, have income thresholds that vary depending on your circumstances, such as whether you’re single, part of a couple, or have children. Exceeding these limits, even by a small margin, can disqualify you from receiving aid, making it essential to understand where your income stands in relation to these caps.

Income limits are not the only determinant; your benefits status plays a pivotal role. If you’re already receiving benefits like Income Support, Jobseeker’s Allowance, or Pension Credit, you’re more likely to qualify for rent assistance. However, the type of benefit you receive can influence the amount of rent assistance you’re entitled to. For example, Universal Credit claimants may receive housing costs as part of their monthly payment, but this is subject to the Local Housing Allowance (LHA) rate for their area, which caps the maximum eligible rent based on property size and location.

Residency requirements further refine eligibility, ensuring that rent assistance is allocated to those with a legitimate right to reside in the UK. You must typically be a British citizen, have settled status, or hold a valid visa that permits access to public funds. EU citizens, for instance, may need to demonstrate settled or pre-settled status under the EU Settlement Scheme. Temporary visitors or those with "no recourse to public funds" conditions on their visas are generally excluded, highlighting the importance of checking your immigration status before applying.

Practical tips can streamline the process. First, use online benefits calculators to estimate your eligibility based on your income and circumstances. Second, gather proof of income, residency, and benefits status before applying to avoid delays. Finally, stay informed about changes to eligibility criteria, as government policies and LHA rates are subject to periodic updates. By carefully navigating these requirements, you can determine whether you’re entitled to rent assistance and take the necessary steps to secure it.

Is Renting an ATV in Mykonos Safe? Tips and Insights

You may want to see also

Explore related products

![]()

Housing Benefit: Financial aid for private or social housing tenants based on income

In the UK, Housing Benefit serves as a vital financial lifeline for tenants struggling to meet their rent obligations. This income-based support is designed to bridge the gap between what tenants can afford and the actual cost of their housing, whether in private or social housing. Eligibility hinges on factors such as income, savings, household composition, and the local housing market. For instance, a single person under 35 is typically restricted to the shared accommodation rate, while families or older individuals may qualify for higher amounts. Understanding these nuances is crucial for maximising the benefit’s potential.

To apply for Housing Benefit, tenants must navigate a process that varies slightly depending on their housing type. Private tenants, for example, can only claim if they were born before 1 April 1983 or fall into specific exempt categories, such as having a child or receiving disability benefits. Social housing tenants, on the other hand, can apply regardless of age. The application involves providing detailed financial information, including income, savings, and rent costs. A key tip is to gather all necessary documents—such as tenancy agreements, bank statements, and proof of income—before starting the application to streamline the process.

One critical aspect of Housing Benefit is its calculation, which is far from one-size-fits-all. The amount awarded is determined by the Local Housing Allowance (LHA) rate for private tenants, which caps the benefit based on the area and property size. For social housing tenants, the benefit covers eligible rent, which excludes service charges or heating costs. A practical takeaway is to use the government’s online benefit calculator to estimate eligibility and potential payments. This tool provides a realistic expectation and helps tenants plan their finances accordingly.

Despite its benefits, Housing Benefit is not without limitations. For private tenants, the LHA rates often fall short of actual rents, particularly in high-cost areas like London. This discrepancy can leave tenants facing a shortfall, necessitating additional financial planning. Social housing tenants, while generally better covered, may still face reductions if deemed to have “spare rooms” under the bedroom tax. To mitigate these challenges, tenants should explore supplementary support, such as Discretionary Housing Payments, which offer temporary relief in cases of hardship.

In conclusion, Housing Benefit is a cornerstone of rent assistance in the UK, offering tailored support to those in need. By understanding its eligibility criteria, application process, and calculation methods, tenants can navigate the system more effectively. While challenges exist, particularly in private rentals, proactive steps—such as using benefit calculators and seeking additional aid—can help maximise this essential financial support. For anyone asking, “Am I entitled to rent assistance in the UK?” Housing Benefit is a critical starting point worth exploring.

Renting Out Your Barn: Essential Permits and Legal Requirements

You may want to see also

Explore related products

![]()

Universal Credit: Rent support through Universal Credit for eligible low-income households

In the UK, Universal Credit has become a cornerstone for supporting low-income households with housing costs, replacing older benefits like Housing Benefit. If you’re struggling to meet rent payments, understanding how Universal Credit’s housing element works is crucial. This support is not automatic; it’s calculated based on your circumstances, including income, family size, and where you live. For instance, the maximum housing allowance for a single person under 35 is capped at the shared accommodation rate, even if they live alone, unless they qualify for exceptions like having a disability or caring responsibilities.

To determine eligibility, start by assessing your household’s financial situation. Universal Credit’s housing element covers rent for both private and social housing tenants, but the amount varies. Private renters receive support based on local housing allowance (LHA) rates, which are set by postcode and property size. Social housing tenants get help with eligible rent, which excludes service charges or heating costs. For example, a family of four in London might receive a higher LHA rate compared to a similar family in a rural area due to regional rent disparities.

Applying for this support requires careful attention to detail. First, check if you’re eligible by using the government’s online benefits calculator. If you qualify, apply for Universal Credit through the official Gov.uk portal, ensuring you provide accurate information about your rent, income, and living situation. Be aware that payments may take up to five weeks to start, so plan ahead. If you’re already on legacy benefits, you’ll need to transition to Universal Credit, which could affect your housing support temporarily.

One common pitfall is misunderstanding how changes in circumstances impact your entitlement. For instance, moving to a more expensive property without updating your claim could leave you underpaid. Conversely, earning more through work might reduce your housing element due to Universal Credit’s taper rate, where 55p of every £1 earned above your work allowance is deducted from your benefit. Regularly reviewing and updating your claim ensures you receive the correct amount.

Finally, if your rent exceeds the LHA rate or eligible rent, you’ll need to cover the shortfall yourself. Practical tips include negotiating a lower rent with your landlord, seeking discretionary housing payments (DHPs) from your local council, or exploring shared living arrangements to reduce costs. While Universal Credit provides vital rent support, it’s often just one part of a broader strategy to manage housing affordability in the UK.

Rent Umbrellas at Indian Rock Beach: Top Spots for Shade

You may want to see also

Explore related products

![]()

Discretionary Housing Payments: Extra help for rent shortfalls in specific circumstances

Discretionary Housing Payments (DHPs) serve as a vital safety net for UK residents facing rent shortfalls that cannot be covered by Housing Benefit or Universal Credit. Unlike standard housing support, DHPs are not an automatic entitlement; they are awarded at the discretion of local councils based on individual circumstances. This means eligibility hinges on demonstrating a genuine need, such as a sudden drop in income, unexpected expenses, or a gap between rent and benefit payments. For instance, a single parent with two children living in a high-rent area might qualify if their Universal Credit housing element falls short of their actual rent, leaving them at risk of eviction.

To apply for a DHP, start by contacting your local council’s housing department. The process typically involves completing an application form and providing evidence of your financial situation, such as bank statements, rent agreements, and proof of income. Be prepared to explain why your current benefits are insufficient and how the additional payment would prevent homelessness or financial hardship. It’s crucial to act promptly, as DHPs are often time-limited and subject to funding availability. Councils may prioritize cases involving vulnerable groups, such as disabled individuals, families with young children, or those fleeing domestic violence.

One key aspect of DHPs is their flexibility. Payments can be awarded as a one-off lump sum, a series of installments, or an ongoing supplement, depending on the council’s assessment. For example, a tenant facing a temporary rent increase due to a landlord’s repairs might receive a short-term DHP to bridge the gap until their benefits are recalculated. Conversely, someone with long-term financial difficulties may be granted recurring payments to stabilize their housing situation. However, DHPs are not a permanent solution; they are designed to provide temporary relief while individuals address the root causes of their rent shortfall.

While DHPs offer critical support, they are not without limitations. Councils have finite budgets for these payments, and applications may be rejected if funds are exhausted. Additionally, DHPs do not cover all housing costs—they are specifically for rent shortfalls, not utilities or other living expenses. Applicants should also be aware that receiving a DHP does not affect their eligibility for other benefits, but it may influence future financial planning. For instance, if a DHP helps avoid eviction, tenants can focus on increasing their income or finding more affordable accommodation.

In conclusion, Discretionary Housing Payments are a targeted resource for those in specific, urgent need of rent assistance. By understanding the application process, providing thorough documentation, and recognizing the temporary nature of this support, individuals can maximize their chances of securing this vital aid. While not a long-term solution, DHPs can provide the breathing space needed to resolve financial challenges and maintain stable housing.

Unrentable Property: What's the Reason Behind It?

You may want to see also

Explore related products

![]()

Local Council Schemes: Regional rent assistance programs and application processes in the UK

Local councils across the UK offer a variety of rent assistance schemes tailored to regional needs, often filling gaps left by national programs like Housing Benefit or Universal Credit. These schemes, known as Discretionary Housing Payments (DHPs) or local welfare assistance, are designed to support residents facing financial hardship with their housing costs. Eligibility criteria vary by council, but common factors include income, savings, and specific circumstances such as disability or homelessness risk. For instance, some councils prioritize applicants who are transitioning from temporary accommodation or those affected by the benefit cap. Understanding your local council’s scheme is the first step to accessing this vital support.

To apply for a local council rent assistance scheme, start by identifying your council’s specific program. Most councils provide detailed information on their websites, including eligibility criteria and application forms. Typically, you’ll need to provide proof of income, tenancy details, and evidence of your financial situation. Some councils accept online applications, while others require phone or in-person submissions. For example, Birmingham City Council’s DHP scheme allows online applications and considers factors like medical conditions or large families. In contrast, Manchester City Council offers both DHP and a local welfare provision fund, each with distinct application processes. Always check for deadlines, as some schemes operate on a first-come, first-served basis.

One critical aspect of local council schemes is their discretionary nature, meaning awards are not guaranteed and depend on available funding. This makes it essential to provide a clear, detailed explanation of your circumstances when applying. Include any supporting documents, such as medical letters or eviction notices, to strengthen your case. For instance, if you’re a single parent with a disabled child, highlight how your additional expenses impact your ability to pay rent. Councils often assess applications on a case-by-case basis, so personalizing your application can significantly improve your chances of approval.

While local council schemes offer valuable support, they are not a long-term solution to housing affordability. They are typically short-term measures to prevent homelessness or alleviate immediate financial pressure. If you’re awarded assistance, use this time to explore other options, such as negotiating a rent reduction with your landlord or seeking advice from housing charities like Shelter or Citizens Advice. Additionally, stay informed about changes to local schemes, as funding and eligibility criteria can shift annually. By combining local council support with proactive financial planning, you can better navigate the challenges of renting in the UK.

A Decade Ago: Average Rent Prices and Housing Trends

You may want to see also

Frequently asked questions

Eligibility for rent assistance in the UK depends on factors such as income, savings, housing situation, and whether you’re claiming other benefits. Common schemes include Housing Benefit (for those on legacy benefits) and Universal Credit (for housing costs). You may qualify if you’re on a low income, unemployed, or have high housing costs relative to your income.

To apply for rent assistance, you typically need to claim either Housing Benefit or the housing element of Universal Credit. For Housing Benefit, apply through your local council. For Universal Credit, apply online via the gov.uk website. You’ll need to provide details about your income, savings, and housing situation during the application process.

The amount of rent assistance you can receive depends on your circumstances, such as your income, the size of your household, and the local housing allowance (LHA) rates in your area. Rent assistance may cover some or all of your rent, but it’s capped based on LHA rates, which vary by region and property size. Additional factors, like non-dependent deductions, may also affect the amount.