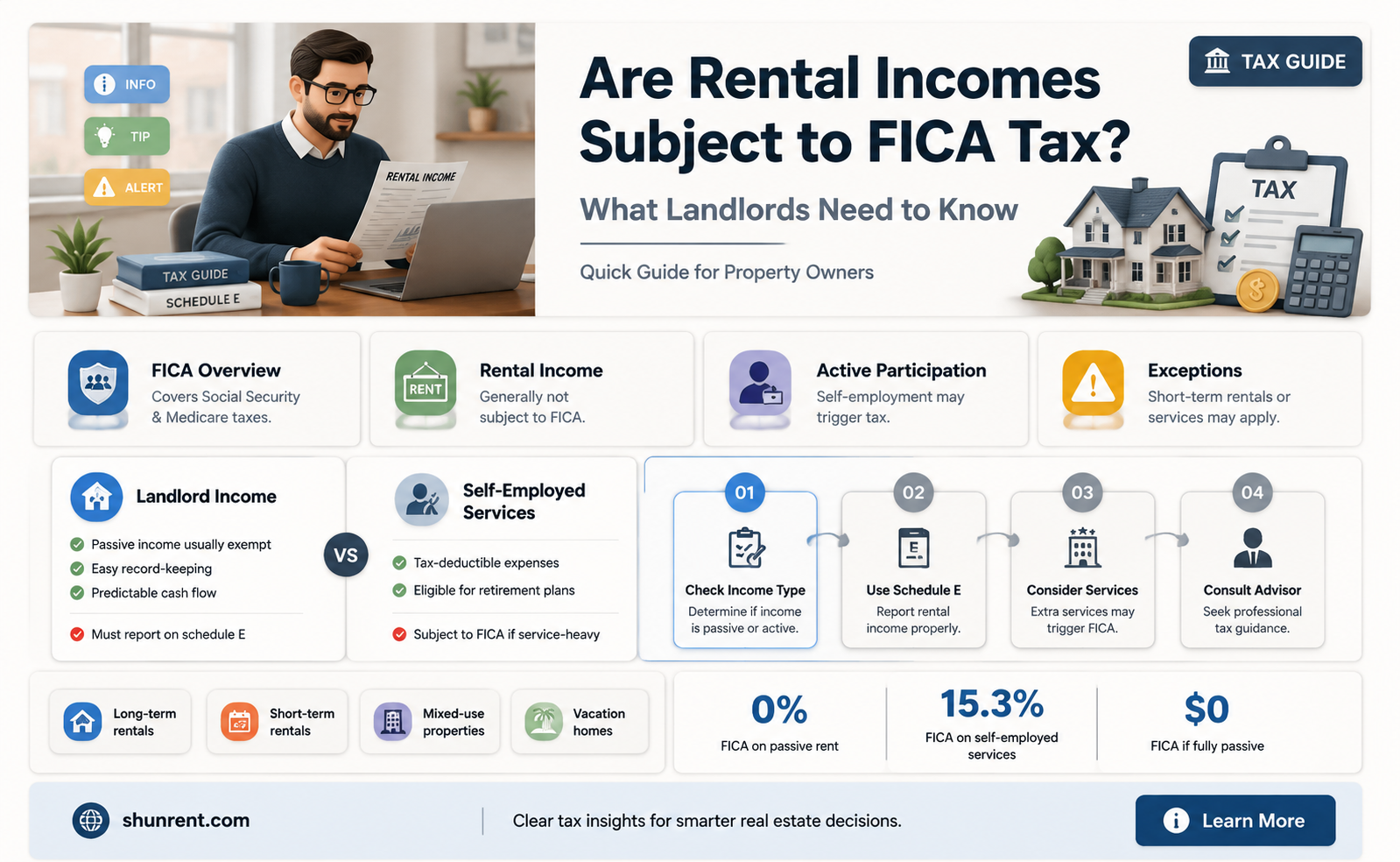

Rent income is generally not subject to Federal Insurance Contributions Act (FICA) tax, which includes Social Security and Medicare taxes. FICA taxes are typically levied on wages, salaries, and self-employment income, rather than passive income like rent. However, if rental activities rise to the level of a trade or business and are considered self-employment, the net earnings from those activities may be subject to self-employment tax, which is similar to FICA tax. Landlords should consult tax professionals to determine their specific obligations based on their level of involvement in rental property management.

| Characteristics | Values |

|---|---|

| Subject to FICA Tax | No, rental income is generally not subject to FICA (Social Security and Medicare) taxes. |

| Tax Classification | Rental income is considered passive income, not earned income. |

| Self-Employment Tax | Not applicable unless the rental activity rises to the level of a trade or business and the taxpayer is considered a real estate professional. |

| Income Tax Treatment | Rental income is taxed as ordinary income on federal tax returns. |

| Net Investment Income Tax (NIIT) | May be subject to the 3.8% NIIT if the taxpayer’s modified adjusted gross income exceeds certain thresholds. |

| State Tax Treatment | Varies by state; some states may impose additional taxes or follow federal guidelines. |

| Reporting Requirements | Reported on Schedule E (Form 1040) for federal tax purposes. |

| Exceptions | If rental income is derived from a business activity (e.g., real estate professional), it may be subject to self-employment tax. |

| FICA Tax Applicability | FICA taxes apply to wages, salaries, and self-employment income, not passive rental income. |

| IRS Guidance | IRS Publication 527 and Publication 334 provide detailed guidance on rental income taxation. |

Explore related products

What You'll Learn

- Wages vs. Rental Income: FICA taxes apply to wages, not passive rental income from properties

- Self-Employment Tax: Landlords with active involvement may owe self-employment taxes on net earnings

- Passive Activity Rules: Rental income is generally considered passive, exempt from FICA taxes

- Material Participation: Active landlords might face FICA if they materially participate in management

- Tax Reporting Requirements: Rental income reported on Schedule E, not subject to FICA withholding

![]()

Wages vs. Rental Income: FICA taxes apply to wages, not passive rental income from properties

FICA taxes, which fund Social Security and Medicare, are a significant payroll deduction for employees and employers alike. However, not all income types are subject to these taxes. A critical distinction exists between wages and rental income, with FICA taxes applying exclusively to the former. This differentiation is rooted in the nature of the income: wages are earned through active work, while rental income is typically passive, derived from property ownership rather than labor.

Consider the mechanics of FICA taxation. For wages, employers withhold 7.65% of an employee’s earnings (6.2% for Social Security and 1.65% for Medicare), and the employer matches this amount. Self-employed individuals pay the full 15.3% through self-employment taxes. In contrast, rental income—whether from a single property or a portfolio—is classified as passive and is not subject to FICA taxes. Instead, it is taxed as ordinary income on federal returns, with potential deductions for expenses like maintenance, property taxes, and mortgage interest.

A practical example illustrates this difference. Suppose an individual earns $60,000 annually as a salaried employee and receives $15,000 in rental income from a property. The $60,000 in wages is subject to FICA taxes, with $4,590 withheld by the employer and matched. The $15,000 in rental income, however, is exempt from FICA taxes, though it must be reported on Schedule E of Form 1040. This distinction is crucial for tax planning, as it allows property owners to retain more of their passive income without additional payroll tax liabilities.

For those managing both wage-based and rental income, understanding this divide is essential. While rental income may require quarterly estimated tax payments to cover federal and state income taxes, it avoids the 15.3% FICA burden faced by self-employed individuals on their earnings. This makes real estate investment an attractive strategy for diversifying income streams and minimizing certain tax obligations. However, careful record-keeping and consultation with a tax professional are advised to ensure compliance with IRS regulations and maximize deductions.

In summary, the FICA tax system draws a clear line between wages and rental income, exempting the latter from payroll taxes. This distinction offers property owners a financial advantage, as passive rental income is not subject to the 15.3% FICA rate applied to earned wages. By leveraging this difference, individuals can optimize their tax strategies and enhance their overall financial health.

Is Rent the Runway a Two-Sided Network? Exploring Its Business Model

You may want to see also

Explore related products

$10.9

![]()

Self-Employment Tax: Landlords with active involvement may owe self-employment taxes on net earnings

Landlords often assume rental income is taxed solely as passive income, but active involvement in property management can trigger self-employment taxes. The IRS considers landlords who provide substantial services—such as regular maintenance, tenant screening, or lease negotiations—as operating a trade or business. When this occurs, net earnings from rental activities may be subject to self-employment (SE) tax, which funds Social Security and Medicare. This distinction hinges on the level of participation, not just the income generated.

To determine if SE tax applies, evaluate the nature of your landlord activities. Passive landlords, who rely on a property manager and have minimal involvement, typically avoid this tax. However, those who actively manage properties—handling repairs, collecting rent, or advertising vacancies—cross into active business territory. For example, a landlord who spends 20 hours per week on property management tasks is more likely to owe SE tax than one who delegates these duties. The IRS scrutinizes the time, effort, and services provided to differentiate between passive and active income.

Calculating SE tax requires careful record-keeping. Start by determining net rental income (gross rent minus deductible expenses like repairs, mortgage interest, and property taxes). If your involvement qualifies as a business, this net income is subject to SE tax at a rate of 15.3% (as of 2023). For instance, a landlord with $50,000 in net rental income would owe $7,650 in SE tax. However, deductions such as half of the SE tax can be claimed on your federal income tax return, reducing the overall tax burden.

Avoiding SE tax inadvertently can lead to penalties and interest. Landlords should file Schedule SE (Form 1040) if net earnings from self-employment exceed $400. Proactive steps include maintaining clear records of time spent on rental activities and consulting a tax professional to assess your involvement level. For those nearing retirement, understanding SE tax implications is crucial, as it affects Social Security benefits. Conversely, overpaying SE tax due to misclassification of passive income can unnecessarily reduce cash flow.

In summary, landlords with active involvement in property management must navigate the complexities of self-employment tax. By distinguishing between passive and active income, accurately calculating net earnings, and staying compliant with IRS rules, landlords can avoid unexpected tax liabilities. This proactive approach ensures financial stability and minimizes the risk of audits, making it an essential consideration for anyone deriving income from rental properties.

Rent-a-Girlfriend Season 2: Will Kazuya's Fake Romance Continue?

You may want to see also

Explore related products

![]()

Passive Activity Rules: Rental income is generally considered passive, exempt from FICA taxes

Rental income, a staple of passive investment strategies, often escapes the clutches of FICA taxes due to its classification under the Passive Activity Rules. These rules, established by the IRS, differentiate between active and passive income, with the latter typically exempt from self-employment taxes, including FICA. For landlords and real estate investors, this distinction is crucial, as it can significantly impact their tax liabilities. Understanding the nuances of these rules allows taxpayers to optimize their financial planning and ensure compliance with tax regulations.

Consider the scenario of a property owner who collects $2,000 monthly in rent. This income, classified as passive, is not subject to the 15.3% FICA tax (combining Social Security and Medicare taxes). In contrast, active income, such as earnings from a job or self-employment, would incur this tax. The IRS defines passive activities as those in which the taxpayer does not materially participate, such as rental real estate ventures. Material participation involves regular, continuous, and substantial involvement in the activity, which is rare for rental property owners unless they are also acting as property managers.

However, exceptions exist. If a taxpayer is a real estate professional who materially participates in the rental activity, the income may be reclassified as non-passive, making it subject to FICA taxes. To qualify as a real estate professional, one must spend more than 50% of their working hours and at least 750 hours annually on real estate trades or businesses. This classification requires meticulous record-keeping and documentation to substantiate the level of involvement.

For most rental property owners, the passive classification offers a significant tax advantage. To maintain this status, it’s essential to avoid activities that could be construed as material participation, such as approving new tenants, directing daily operations, or providing regular maintenance. Instead, delegating these tasks to a property manager or management company helps preserve the passive nature of the income. Additionally, keeping detailed records of involvement and income sources ensures compliance and simplifies tax reporting.

In conclusion, the Passive Activity Rules provide a clear framework for distinguishing between active and passive rental income, with the latter generally exempt from FICA taxes. By understanding and adhering to these rules, rental property owners can maximize their tax efficiency while remaining compliant. Whether you’re a seasoned investor or a first-time landlord, recognizing the passive nature of rental income is a key step in effective tax planning.

Renting a Condo: What to Expect and Key Considerations

You may want to see also

Explore related products

![]()

Material Participation: Active landlords might face FICA if they materially participate in management

Active landlords who materially participate in the management of their rental properties may find themselves subject to FICA taxes, a detail often overlooked in the realm of real estate income. The IRS defines material participation as involvement in the operations of a trade or business that is regular, continuous, and substantial. For landlords, this could mean handling tenant screening, property maintenance, rent collection, or even advertising vacancies. If these activities rise to the level of material participation, the income generated from these properties is reclassified as earned income, making it subject to self-employment taxes, including FICA.

Consider a landlord who owns three rental units and spends an average of 20 hours per week managing them. This individual screens tenants, coordinates repairs, and handles lease agreements personally. Under IRS guidelines, such involvement would likely qualify as material participation. As a result, the net rental income from these properties would be treated as self-employment income, requiring the landlord to pay 15.3% in FICA taxes (12.4% for Social Security and 2.9% for Medicare). This contrasts sharply with passive landlords, whose rental income is generally taxed as unearned income and exempt from FICA.

To determine whether your activities constitute material participation, the IRS provides seven tests, including the 500-hour test (participating more than 500 hours in the tax year) and the significant participation test (participating for more than 100 hours and no other individual participating more). Landlords should meticulously track their time spent on rental activities to assess their risk of FICA liability. For instance, maintaining a log of hours spent on tenant communications, property inspections, and financial management can provide critical evidence in case of an audit.

Avoiding unintended FICA liability requires strategic planning. One approach is to delegate management tasks to a property manager, thereby reducing personal involvement below the material participation threshold. Alternatively, landlords can structure their rental activities as a formal business, hiring themselves as employees and paying FICA taxes through payroll deductions. This not only ensures compliance but also provides access to Social Security and Medicare benefits. However, this strategy should be weighed against the administrative burden and costs of formalizing the arrangement.

Ultimately, the line between passive and active landlord participation is thin but critical. Landlords who enjoy hands-on management should consult a tax professional to evaluate their exposure to FICA taxes. By understanding the rules of material participation and proactively structuring their activities, they can optimize their tax position while maintaining control over their rental properties. Ignoring this distinction could lead to unexpected tax liabilities, penalties, and interest, undermining the financial benefits of real estate investment.

Renting Hockey vs. Figure Skates: Which Option Fits Your Needs?

You may want to see also

Explore related products

![]()

Tax Reporting Requirements: Rental income reported on Schedule E, not subject to FICA withholding

Rental income, a common source of earnings for many property owners, is reported on Schedule E of Form 1040 when filing federal taxes in the United States. One critical aspect that distinguishes rental income from wages or salaries is its treatment under the Federal Insurance Contributions Act (FICA). Unlike earned income, rental income is not subject to FICA withholding, which includes Social Security and Medicare taxes. This distinction is rooted in the classification of rental income as passive income rather than active earnings from employment.

Understanding this exemption is crucial for landlords and property owners to ensure accurate tax reporting. When completing Schedule E, taxpayers report rental income and associated expenses, such as property maintenance, insurance, and depreciation. The net income from these activities is then transferred to Form 1040, where it contributes to the taxpayer’s overall taxable income. However, this net income is not included in the calculation for FICA taxes, which are levied on wages, salaries, and self-employment income but explicitly exclude passive income streams like rent.

A practical example illustrates this point: If a taxpayer earns $30,000 in rental income annually and incurs $10,000 in deductible expenses, the net rental income of $20,000 is reported on Schedule E. This $20,000 is subject to federal income tax but not to the 15.3% FICA tax rate (12.4% for Social Security and 2.9% for Medicare). This exemption can result in significant tax savings, particularly for individuals with substantial rental income. However, it’s essential to distinguish between rental income and self-employment income, as the latter—such as income from property management services—may still be subject to FICA taxes.

Taxpayers should exercise caution to avoid misclassification. For instance, if a landlord provides additional services beyond basic property rental (e.g., regular maintenance or concierge services), the income from these activities might be reclassified as self-employment income, making it subject to FICA taxes. To navigate these complexities, consulting IRS Publication 527, *Residential Rental Property*, or seeking professional tax advice is recommended. Proper classification ensures compliance and maximizes tax efficiency.

In summary, rental income reported on Schedule E is not subject to FICA withholding, offering a tax advantage for property owners. However, this benefit hinges on accurate reporting and clear distinctions between passive rental income and active self-employment income. By understanding these nuances, taxpayers can fulfill their tax obligations while optimizing their financial outcomes.

Rent's Shelter Metaphor: Exploring Themes of Home and Belonging

You may want to see also

Frequently asked questions

No, rent incomes are not subject to FICA tax because they are considered passive income, not earned income from employment or self-employment.

No, receiving rental income does not affect FICA tax obligations, as FICA taxes only apply to wages, salaries, and self-employment income, not passive rental income.

If you actively manage your rental property and are considered a real estate professional, the income may be treated as self-employment income and subject to self-employment taxes (including FICA). Otherwise, it remains passive and not subject to FICA tax.