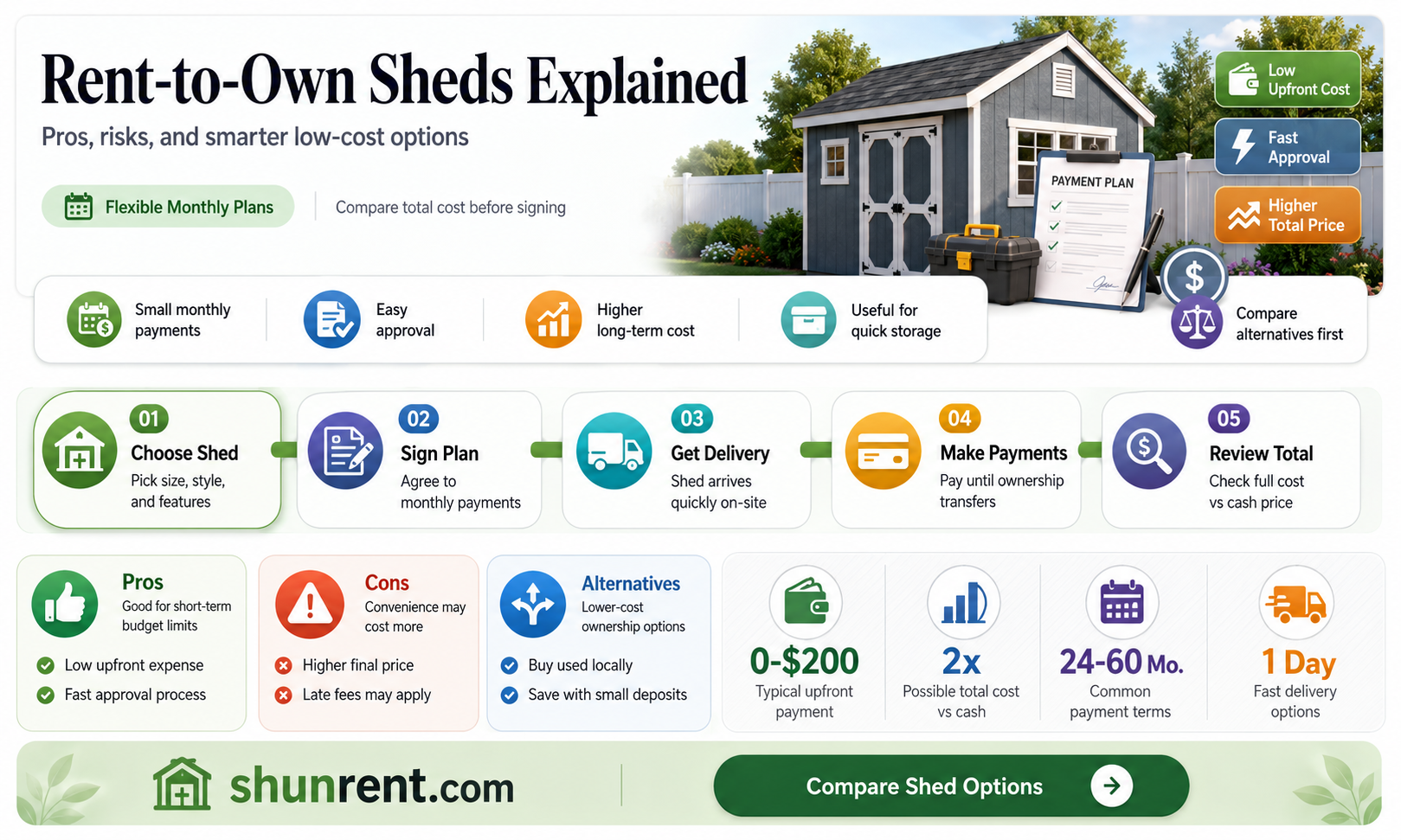

Rent-to-own sheds have emerged as a popular alternative for those seeking additional storage space without the immediate financial burden of purchasing outright. This arrangement allows individuals to rent a shed with the option to own it over time by making regular payments, often without a credit check or large down payment. While this can be appealing for those with limited cash flow or poor credit, it’s essential to weigh the long-term costs, as rent-to-own agreements typically result in paying significantly more than the shed’s retail price. Additionally, terms and conditions can vary widely, so understanding contract details, such as ownership timelines and early buyout options, is crucial. Ultimately, whether rent-to-own sheds are worth it depends on individual financial situations, storage needs, and the willingness to pay a premium for flexibility.

Explore related products

$1394.95 $1999

What You'll Learn

![]()

Initial Costs vs. Long-Term Savings

The upfront cost of a rent-to-own shed can be deceptively low, often just a small down payment followed by monthly installments. This makes it an attractive option for those with limited cash flow or poor credit. However, these monthly payments, typically spanning 24 to 60 months, add up quickly. A $5,000 shed with a 36-month term at 10% interest, for example, could cost you over $6,000 in total. Compare this to purchasing a similar shed outright, where you avoid interest charges altogether.

Understanding Assignment of Leases and Rents in Real Estate Transactions

You may want to see also

Explore related products

![]()

Ownership Terms and Conditions Explained

Rent-to-own sheds often present ownership terms that blend rental flexibility with a path to eventual ownership, but deciphering these agreements requires careful scrutiny. Typically, the contract outlines a monthly payment structure, part of which applies toward the shed’s purchase price if you decide to buy. However, the devil is in the details: some agreements include a buyout clause that requires a lump-sum payment to claim ownership, while others allow you to own the shed after a set number of payments. Understanding these terms is critical, as failing to meet the conditions can result in forfeiture of all payments made, leaving you with nothing but a rented structure.

Analyzing the financial implications reveals a stark contrast between renting and outright purchasing. For instance, a $2,000 shed might cost $100 monthly over 36 months, totaling $3,600—an 80% markup. This premium price often includes delivery and setup, but it’s essential to compare this to traditional financing options. If you have access to a low-interest loan, you could potentially save hundreds or even thousands of dollars. The trade-off? Rent-to-own offers no credit checks, making it accessible to those with poor credit but at a higher long-term cost.

One often-overlooked aspect of these agreements is the maintenance responsibility. Unlike traditional rentals, where the landlord handles repairs, rent-to-own sheds typically place the burden of upkeep on you from day one. This means you’re responsible for weatherproofing, pest control, and structural repairs, even if you haven’t yet taken full ownership. Before signing, assess whether you’re prepared to shoulder these costs, as neglecting maintenance can void the agreement or reduce the shed’s value if you decide to buy.

Persuasively, the flexibility of rent-to-own sheds can be their most appealing feature, especially for those in transitional living situations. If you’re renting a home or planning to move within a few years, the option to return the shed without penalty (in some contracts) can be a lifesaver. However, this convenience comes with strings attached: early termination fees or the loss of all rental payments made. To maximize this flexibility, negotiate terms that allow for early buyout or return without excessive penalties, ensuring you’re not locked into a costly commitment.

Finally, a comparative look at ownership timelines highlights the importance of long-term planning. While traditional purchases offer immediate ownership, rent-to-own sheds require patience—often 24 to 36 months of consistent payments. If your goal is quick ownership, this option may not align with your needs. Conversely, if you prioritize low upfront costs and the ability to walk away, it could be a viable choice. The key is aligning the terms with your financial goals and lifestyle, ensuring the shed serves as an asset, not a liability.

Understanding the Average Rent at Oakwood Village: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Maintenance Responsibilities During Rental Period

One of the critical aspects of rent-to-own shed agreements is understanding who bears the responsibility for maintenance during the rental period. Unlike traditional rentals, where the landlord typically handles upkeep, rent-to-own contracts often shift this burden to the renter. This means you’ll likely be responsible for tasks like cleaning gutters, repairing minor damage, and ensuring the shed remains structurally sound. Before signing, carefully review the contract to identify which maintenance tasks are your responsibility and which, if any, the provider covers. Overlooking this detail could lead to unexpected costs or disputes down the line.

Consider the long-term implications of maintenance responsibilities when evaluating whether a rent-to-own shed is worth it. For instance, if the shed is made of wood, you’ll need to budget for periodic staining or sealing to prevent rot and pest infestations. Metal sheds may require rust treatment, while plastic sheds might need cleaning to avoid discoloration. Factor in the cost of tools, materials, and time required for these tasks. If you’re not handy or lack the time, the maintenance demands could outweigh the benefits of owning a shed eventually.

A comparative analysis reveals that maintenance responsibilities in rent-to-own agreements often mirror those of outright ownership but with added risks. As a renter, you’re investing in a structure you don’t yet own, meaning any neglect could jeopardize your equity. For example, failing to address a leaky roof promptly could lead to water damage, reducing the shed’s value and potentially voiding your contract. In contrast, owning a shed outright gives you full control over maintenance decisions without the risk of losing your investment due to contractual violations.

To navigate maintenance responsibilities effectively, adopt a proactive approach. Create a maintenance schedule based on the shed’s material and local climate. For example, inspect the roof and foundation seasonally, especially after severe weather. Keep a log of all repairs and maintenance activities, as this documentation can be useful if disputes arise. Additionally, consider setting aside a small monthly fund for maintenance expenses, ensuring you’re financially prepared for unexpected repairs. By treating maintenance as an ongoing commitment rather than a reactive chore, you’ll maximize the shed’s lifespan and protect your investment.

Renting Your Shop in New Jersey: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Early Purchase Options and Benefits

One of the most compelling aspects of rent-to-own shed programs is the flexibility they offer through early purchase options. Unlike traditional financing, which locks you into a fixed payment schedule, rent-to-own agreements often allow you to buy the shed outright before the contract ends. This feature can save you significant money by eliminating remaining rental payments and associated fees. For instance, if you’re 12 months into a 36-month agreement and decide to purchase, you could bypass the higher total cost of continuing to rent. This option is particularly advantageous if your financial situation improves sooner than expected or if you realize the shed’s value exceeds the cost of ownership.

Analyzing the benefits, early purchase options provide a clear financial incentive. Rent-to-own programs typically include a buyout clause that calculates the remaining balance based on the original price minus payments already made, often with no additional interest or penalties. For example, if a $3,000 shed has a 36-month rental agreement with monthly payments of $100, purchasing after 18 months would cost approximately $1,800 (remaining balance) instead of continuing to pay $2,400 over the next 18 months. This structure rewards proactive decision-making and can make ownership more attainable for those who initially opted to rent due to budget constraints.

From a practical standpoint, exercising an early purchase option requires careful planning. Start by reviewing your contract to understand the buyout terms, including any specific conditions or formulas used to calculate the remaining balance. Keep track of your payments and monitor your financial situation to identify the optimal time to buy. For instance, if you receive a tax refund or bonus, consider using it to settle the balance early. Additionally, ensure the shed meets your long-term needs before committing to ownership, as modifications or upgrades may be easier to justify once you own the structure outright.

Comparatively, early purchase options in rent-to-own shed programs stand out when contrasted with other financing methods. Traditional loans often come with strict prepayment penalties or fixed interest rates that diminish the benefit of paying off the balance early. In contrast, rent-to-own agreements are designed to encourage ownership, making them a more flexible and cost-effective solution for those who value adaptability. For individuals who prioritize both affordability and the freedom to adjust their financial commitments, this feature can be a deciding factor in choosing rent-to-own over other options.

In conclusion, early purchase options within rent-to-own shed programs offer a unique blend of financial savings and flexibility. By understanding the terms, planning strategically, and acting decisively, you can maximize the benefits of this feature. Whether you’re looking to save money, gain ownership sooner, or simply retain control over your financial commitments, this option makes rent-to-own sheds a worthwhile consideration for those in need of storage solutions.

Millennials' Housing Dilemma: Buying vs. Renting Trends Unveiled

You may want to see also

Explore related products

![]()

Comparing Rent-to-Own to Traditional Shed Buying

Rent-to-own sheds offer a flexible alternative to traditional purchasing, but the devil is in the details. Unlike buying outright, where you own the shed immediately, rent-to-own agreements allow you to pay in installments over time, often with the option to return the shed if your needs change. This model appeals to those who want a shed without a large upfront cost or long-term commitment. However, it’s crucial to compare the total cost, including interest and fees, to determine if this option is truly worth it.

Consider the financial implications of both approaches. Traditional shed buying requires a lump sum payment, which can be a barrier for some. In contrast, rent-to-own sheds typically involve weekly or monthly payments, making them more accessible for those on tighter budgets. However, these payments often include interest, and the total amount paid over time can exceed the shed’s retail price. For example, a $2,000 shed might cost $3,500 or more by the end of a rent-to-own contract. Calculate the total cost of both options to see which aligns better with your financial goals.

Flexibility is another key factor in this comparison. Rent-to-own agreements often allow you to return the shed without penalty if you no longer need it, which can be advantageous for temporary storage needs. Traditional buying, on the other hand, locks you into ownership, which may not suit those who move frequently or have uncertain long-term plans. However, owning a shed outright gives you the freedom to modify or sell it, whereas rent-to-own sheds typically come with restrictions on customization and ownership transfer.

Finally, consider the long-term value. If you plan to use a shed for many years, buying outright may be more cost-effective despite the initial expense. Rent-to-own sheds can be a good fit for short-term needs or those testing the waters, but they rarely offer the same return on investment. Evaluate your timeline and intended use to decide which option provides the best value for your situation.

Boat Rentals: Do Local Laws Require a License?

You may want to see also

Frequently asked questions

Rent-to-own sheds can be a good option if you need immediate storage but lack the funds to purchase outright. However, they often come with higher total costs due to interest and fees, so they may not be the most financially efficient choice in the long run.

Rent-to-own sheds offer flexibility with no credit checks, low monthly payments, and the option to return the shed if it’s no longer needed. They also allow you to own the shed after completing all payments, making them a viable alternative to traditional financing.

Yes, rent-to-own sheds typically cost more over time due to added interest and fees. You may also face penalties for late payments or early termination. Additionally, the shed’s quality and customization options might be limited compared to purchasing outright.