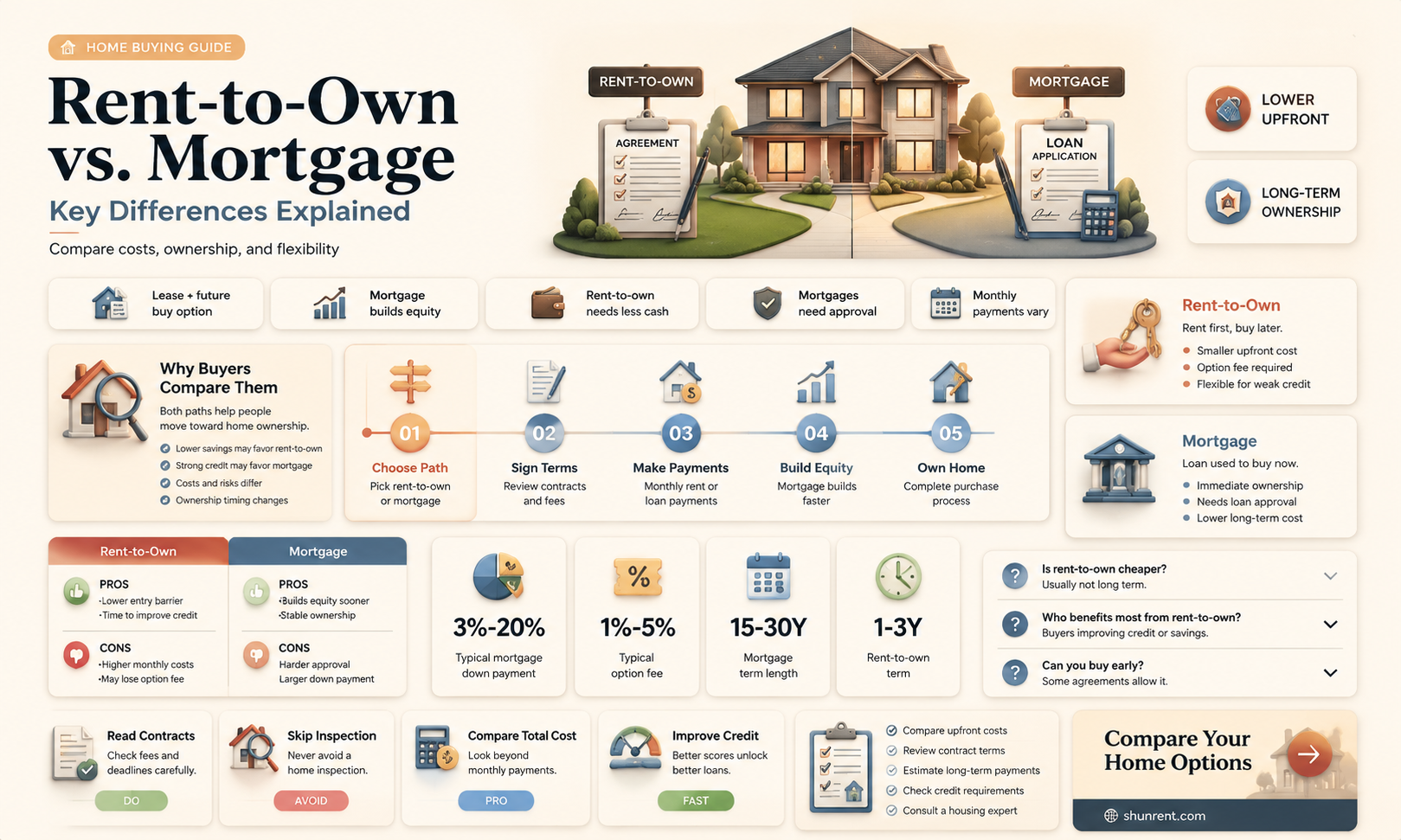

Rent-to-own and traditional mortgages are two different paths to homeownership. Rent-to-own agreements are an option for people who may not be able to secure a mortgage initially or make an upfront down payment. They offer an alternative route to homeownership for those unable to secure traditional mortgages. Rent-to-own agreements can give you time to improve your credit or save for a down payment while living in the home you hope to purchase. On the other hand, a traditional mortgage means you borrow money from a lender to purchase a home, which you then repay over several years. This gives you full control and rights over the property.

| Characteristics | Values |

|---|---|

| Definition | Rent-to-own is an agreement with a landlord to rent a property with the option to purchase it at a later date. A mortgage is a loan from a lender to purchase a property, which is then repaid with interest over several years. |

| Ownership | Rent-to-own agreements do not confer ownership of the property until the end of the lease period when the tenant may choose to buy the property. With a mortgage, the property is owned by the buyer, although the lender has an interest in it until the loan is repaid. |

| Credit Score | Rent-to-own agreements may be an option for those with poor credit scores as they offer time to improve creditworthiness. Traditional mortgages require a good credit score for approval, although there are mortgages designed for those with poor credit. |

| Down Payment | Rent-to-own agreements allow tenants to save for a down payment by putting part of their monthly rent towards it. Mortgages typically require a down payment upfront, although there are low-down-payment mortgage options. |

| Monthly Costs | Rent-to-own agreements usually involve higher monthly costs than a simple lease or mortgage. |

| Flexibility | Rent-to-own agreements offer flexibility, allowing tenants to walk away from the purchase if their circumstances change. Mortgages are less flexible, requiring buyers to commit to the purchase. |

| Risk | Rent-to-own agreements carry the risk of losing money if tenants decide not to purchase the property, as they may lose their deposit and face legal consequences. Traditional mortgages carry less financial risk. |

| Control | With a rent-to-own agreement, tenants do not have financial control over the property and are still subject to a landlord-tenant relationship. With a mortgage, the buyer has full control and rights over the property. |

Explore related products

What You'll Learn

- Rent-to-own agreements can be more expensive than traditional mortgages

- Rent-to-own agreements offer a simplified home-buying process by including closing costs, taxes and insurance in the agreement

- Rent-to-own agreements are more flexible than traditional mortgages

- Rent-to-own agreements can be a good option for those with poor credit scores as they offer a chance to improve credit scores

- Rent-to-own agreements may be a scam

![]()

Rent-to-own agreements can be more expensive than traditional mortgages

The complexity of the rent-to-own process contributes to its potential expense. Unlike traditional homeownership, where you become the homeowner immediately after closing, rent-to-own agreements involve a lease-option or lease-purchase contract. During the lease period, you are still considered a tenant and are not financially responsible for the home. This means that you may need to pay for renters insurance instead of homeowners insurance until you complete the purchase. Additionally, there may be uncertainties and risks associated with the purchase price. While some rent-to-own agreements allow you to lock in a sales price early, there is a possibility that you could end up paying more for the home than its current value if its value declines during the lease period.

The financial implications of rent-to-own agreements can be significant. In some cases, you may be responsible for maintenance and repairs during the lease period, which can add to your overall costs. Additionally, there is a risk of encountering scams or predatory practices in the rent-to-own market. It is crucial to thoroughly research and understand the terms of any rent-to-own agreement before signing, as the complexities and potential costs can vary.

While rent-to-own agreements offer an alternative path to homeownership for those who may not qualify for traditional mortgages, they often come with higher costs and financial risks. It is important for individuals to carefully consider their financial situation, seek professional advice, and explore all available options before entering into any homeownership agreement.

Rent vs Lease: What's the Difference?

You may want to see also

Explore related products

![]()

Rent-to-own agreements offer a simplified home-buying process by including closing costs, taxes and insurance in the agreement

Rent-to-own agreements are a good option for people who cannot secure a mortgage or make an upfront down payment. They offer a simplified home-buying process by including closing costs, taxes, and insurance in the agreement. Here's how:

Simplified financing

Rent-to-own agreements allow you to build equity by putting part of your monthly rent towards a down payment on the property. This helps you save for a down payment while living in the home you plan to buy. During this time, you can also work on improving your credit score to eventually secure a mortgage. This simplifies the financing process by giving you a head start on both down payment savings and credit score requirements, which are typically major hurdles in traditional home-buying.

Reduced closing costs

Closing costs are typically lower in rent-to-own agreements as compared to traditional mortgages. When you rent a home and then buy the same residence, you save on moving costs since you don't have to relocate. Additionally, some rent-to-own programs may offer lender credits towards closing costs, equivalent to a percentage of your total rental payment.

Included taxes and insurance

Most rent-to-own companies include property taxes and insurance in the agreement, which simplifies the process and reduces the financial burden on homebuyers. This means you don't have to worry about additional taxes or the cost of obtaining homeowners insurance separately. However, it's important to note that during the lease period, you will likely need renters insurance instead of homeowners insurance to cover your belongings.

While rent-to-own agreements offer a simplified process, it's crucial to carefully review the contract terms. Understand your responsibilities, potential risks, and how your funds will be held for the eventual down payment. Additionally, be aware of potential scams and work with a real estate attorney or agent to ensure a smooth and secure transaction.

Renting: Financial Disadvantages and Lack of Equity

You may want to see also

Explore related products

$15.75

$9.99 $39.99

![]()

Rent-to-own agreements are more flexible than traditional mortgages

Secondly, rent-to-own agreements provide more flexibility in terms of interest rates. As these agreements typically span several years, if interest rates are high when the contract is signed, they may become more favourable by the time of purchase. This allows buyers to lock in the home without being locked into a high-interest rate. Additionally, rent-to-own contracts often include closing costs, taxes, and insurance, simplifying the financial process and lessening the initial financial burden on homebuyers.

Furthermore, rent-to-own agreements offer a "trial period" in a specific home and area, providing a level of flexibility that traditional mortgages lack. Buyers can experience living in the home and neighbourhood before committing to ownership, reducing the risk of buyer's remorse. This flexibility also extends to the financial aspects of the agreement, as buyers can choose to walk away from the contract if their circumstances change, although they may lose some of the extra rent paid towards the down payment.

While rent-to-own agreements offer advantages in terms of flexibility, it is important to carefully consider the potential risks and downsides. These agreements can be more expensive due to additional fees, and buyers may lose money if they decide not to purchase the home after the lease ends. Unpredictable housing trends and market fluctuations can also impact the final purchase price, potentially leading to overspending. Therefore, while rent-to-own agreements provide flexibility, they require careful consideration and financial planning.

San Francisco Rent: How Much Does it Cost?

You may want to see also

Explore related products

![]()

Rent-to-own agreements can be a good option for those with poor credit scores as they offer a chance to improve credit scores

Rent-to-own agreements are a good option for those with poor credit scores as they offer a chance to improve credit scores and build a positive credit history. While renting the home, individuals can take steps to improve their credit score, such as making monthly payments on time, reducing debt, and keeping credit utilization low. This positive payment history can then be reported to credit bureaus, which can positively impact an individual's credit score.

Rent-to-own agreements are often more lenient than traditional mortgages when it comes to credit score requirements, making them more accessible to individuals with poor credit. These agreements provide a window of time for individuals to build or repair their credit before applying for a mortgage. During this period, individuals can work on improving their credit score by making timely payments, reducing debt, and keeping credit utilization low. This can increase their chances of securing a mortgage when the lease period ends.

Additionally, rent-to-own agreements offer other benefits, such as the ability to lock in a sales price at the beginning of the lease, avoiding bidding wars in a competitive housing market, and saving on moving costs. However, it is important to note that rent-to-own agreements also come with financial risks, and individuals should carefully consider their options before entering into any agreement.

While rent-to-own agreements can provide an opportunity to improve credit scores, it is not automatic. Individuals must be diligent in making timely payments and managing their finances responsibly. It is also important to understand the terms and conditions of the agreement, as well as the potential risks, to ensure a successful outcome.

Overall, rent-to-own agreements can be a good option for those with poor credit scores, offering a chance to improve their creditworthiness and eventually secure a mortgage to purchase their dream home.

Informing Tenants of Rent Increase with a Letter

You may want to see also

Explore related products

![]()

Rent-to-own agreements may be a scam

Rent-to-own agreements are a popular alternative for people who cannot secure a mortgage or make upfront down payments. They are also attractive to people who want to improve their credit scores. However, the Federal Trade Commission (FTC) warns that these agreements can be shady deals and scams. Here are some reasons why:

Firstly, the landlord might not be the actual owner of the property. The FTC warns that scammers may list a home online that they don't own to collect upfront fees. Therefore, it is crucial to verify the property's ownership by researching tax records. Additionally, be cautious if a landlord requests a non-refundable deposit before signing a contract or moving in, as legitimate landlords should not ask for money without a formal agreement.

Secondly, the property might have hidden issues, such as structural problems, unpaid taxes, or legal disputes. Scammers may underprice a home to lure buyers in, making the deal seem too good to be true. To avoid this, it is essential to know the market and compare how similar properties in the area are priced. Request a detailed property history and a current market analysis to understand its true value.

Thirdly, rent-to-own agreements may include additional fees that do not count towards rent or the down payment. Furthermore, you may be responsible for maintenance and repairs from the beginning of your lease, which is not typically the case in standard rental agreements.

Lastly, these agreements often heavily favour the landlord, as they usually write the contracts. Some terms may even be unlawful, such as allowing the landlord to evict you and keep your money if you miss payments or violate the contract.

To protect yourself, it is highly recommended to have a realtor or attorney review the agreement. They can help identify potential risks and ensure the terms are fair and in your best interests.

Renting vs Buying: What's the Better Deal?

You may want to see also

Frequently asked questions

Rent-to-own agreements are an option for people who may not be able to secure a mortgage initially or make an upfront down payment. Instead, they enter into an agreement with a property owner to purchase the home at the end of a lease term.

In a rent-to-own agreement, you lease a home for a set amount of time before buying it. The process can be a way for people with limited savings to buy homes because the agreement builds in opportunities to save for a down payment.

Rent-to-own agreements can give you time to improve your credit or save for a down payment while living in the home you hope to purchase. It can also be a good way to get started if you need time to repair your credit before applying for a mortgage.

Rent-to-own agreements can be more expensive because there are usually fees associated with this option. You’ll have to pay those as well as the regular closing costs and fees when it’s time to buy the house. Monthly costs are usually higher than in a simple lease.

No, they are not the same. Rent-to-own agreements are an alternative path to homeownership for those unable to secure traditional mortgages.