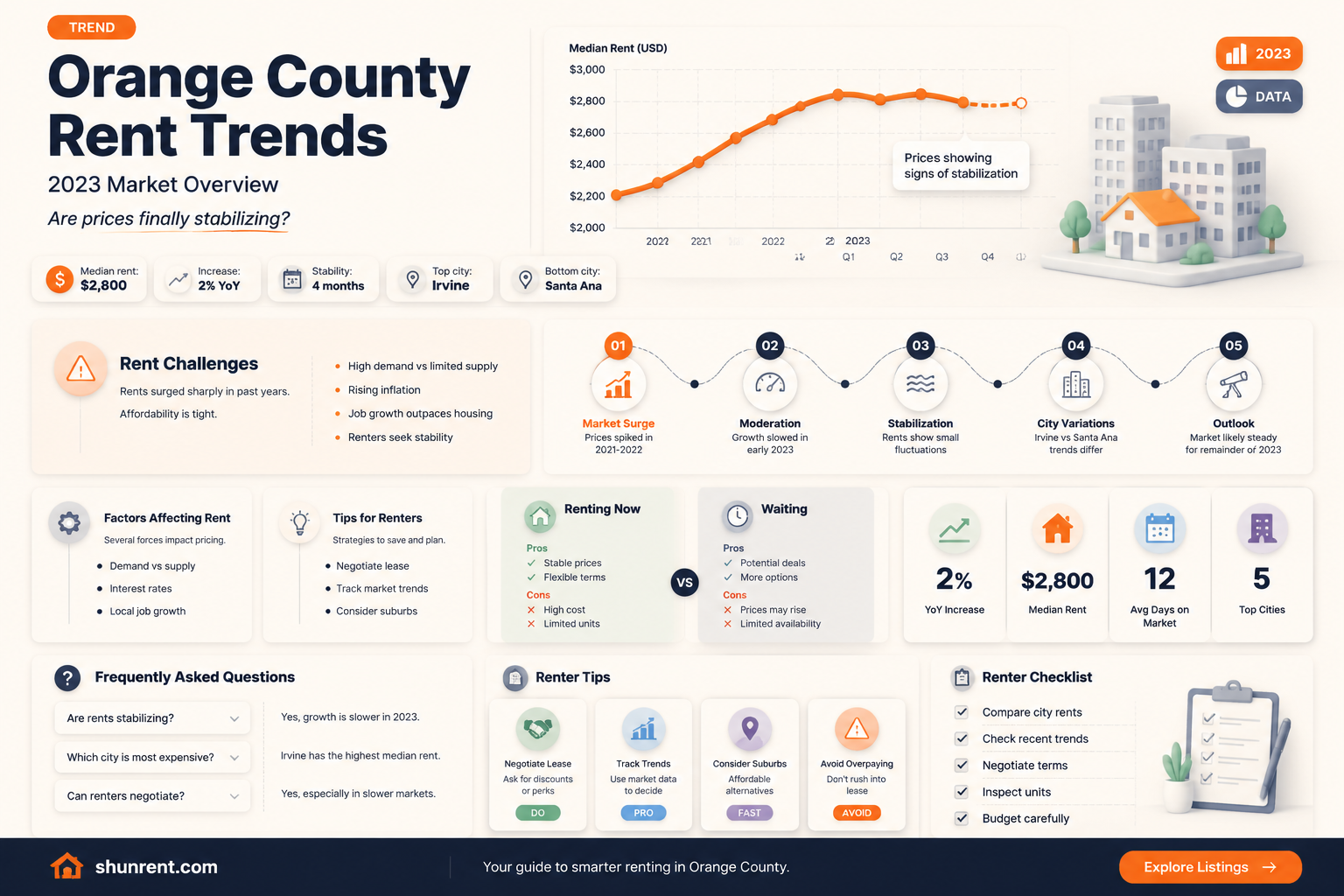

Orange County's rental market has been a focal point for residents and investors alike, with soaring rents over the past few years leaving many to wonder if the trend is sustainable. Recent data suggests that rent growth in the region may finally be leveling off, providing a glimmer of hope for tenants who have faced significant financial strain. Factors such as increased housing supply, shifting migration patterns, and economic uncertainties are contributing to this potential stabilization. While rents remain historically high, the slowdown in price increases indicates a possible shift in the market dynamics, prompting both renters and landlords to reassess their strategies in this evolving landscape.

| Characteristics | Values |

|---|---|

| Rent Trend (2023) | Mixed signals; some sources indicate a slowdown in rent growth, while others show continued increases. |

| Year-over-Year Rent Change (2023) | Varies by source: some report a 0-2% increase, others show a slight decline. |

| Median Rent (2023) | Approximately $3,000 - $3,500 for a 2-bedroom apartment (varies by city within Orange County). |

| Vacancy Rate (2023) | Low, around 2-4%, indicating a tight rental market. |

| New Construction Impact | Increased supply from new apartment complexes may be contributing to slower rent growth in some areas. |

| Economic Factors | Strong local economy and job market continue to drive demand for housing, though inflation and interest rates may be tempering growth. |

| Seasonal Fluctuations | Typical seasonal patterns may show slight decreases in winter months, but overall trend remains elevated. |

| Affordability Concerns | Persistent issue, with many residents spending a high percentage of income on rent. |

| Comparison to National Trends | Orange County rent growth is generally outpacing national averages, though the gap is narrowing. |

| Forecast (2024) | Predictions vary; some expect stabilization or modest increases, while others anticipate continued growth, albeit at a slower pace. |

Explore related products

![Orange County [Blu-ray]](https://m.media-amazon.com/images/I/81Xxkz8QbgL._AC_UY218_.jpg)

What You'll Learn

![]()

Current rental price trends in Orange County

Orange County's rental market has been a rollercoaster in recent years, with prices climbing steadily since the pandemic. However, recent data suggests a potential shift. According to a Q3 2023 report by CoStar, rent growth in Orange County has slowed significantly, dropping to 0.8% year-over-year, the lowest rate since 2020. This marks a stark contrast to the double-digit increases seen in 2021 and early 2022.

Several factors contribute to this cooling trend. Firstly, new apartment construction is finally catching up with demand. Over 5,000 new units are expected to hit the market in 2024, providing much-needed relief to renters. Secondly, rising interest rates have made homeownership less attainable, leading some potential buyers to remain in the rental market, but also discouraging investors from purchasing rental properties, thus reducing competition.

Additionally, economic uncertainties and inflationary pressures may be causing renters to be more price-sensitive, pushing landlords to moderate rent increases.

This slowdown doesn't necessarily mean rents are plummeting. While growth has decelerated, average rents in Orange County remain significantly higher than pre-pandemic levels. A one-bedroom apartment in Irvine, for example, still averages around $2,500 per month, a 20% increase compared to 2019. However, the rate of increase is slowing, offering a glimmer of hope for renters who have been struggling with affordability.

It's important to note that trends can vary across neighborhoods. Coastal cities like Newport Beach and Laguna Beach still command premium rents, while inland areas may see more pronounced price stabilization.

For renters, this shift presents an opportunity to negotiate lease renewals or explore new options. With more inventory coming online and slower rent growth, tenants have more leverage than they've had in years. However, it's crucial to remain realistic about expectations. Orange County remains a desirable location with a strong job market, so significant rent decreases are unlikely in the near future.

Discover Cozy Cabins for Rent Near Greenville, Ohio

You may want to see also

Explore related products

![Orange County [DVD]](https://m.media-amazon.com/images/I/612WI4EYiIL._AC_UY218_.jpg)

![Orange County [VHS]](https://m.media-amazon.com/images/I/91bSQwD50uL._AC_UY218_.jpg)

![Orange County [Region 2]](https://m.media-amazon.com/images/I/8121lrLfoWL._AC_UY218_.jpg)

![]()

Factors influencing rent stabilization in the region

Orange County's rental market has been a rollercoaster in recent years, with rents soaring to unprecedented heights. However, recent data suggests a potential shift, with some areas experiencing a slowdown in rent growth. This begs the question: what factors are contributing to this stabilization?

Supply and Demand Dynamics: A key driver of rent stabilization is the balance between housing supply and population demand. Orange County has seen a surge in multi-family housing construction, particularly in urban centers like Irvine and Anaheim. This increased supply helps alleviate the pressure on rents, as more units become available for occupancy. For instance, the city of Irvine has approved over 20,000 new housing units since 2018, with a significant portion dedicated to affordable and workforce housing. As these units come online, they absorb some of the pent-up demand, moderating rent increases.

Economic Factors and Affordability: The region's economic landscape plays a crucial role in rent stabilization. As of 2023, Orange County's median household income is approximately $95,000, while the average rent for a two-bedroom apartment hovers around $2,800. This disparity highlights the affordability challenge faced by many residents. When rents outpace income growth, it creates a natural ceiling, as tenants reach their maximum budget capacity. Landlords, in response, may opt to maintain current rates or offer incentives to retain tenants, effectively stabilizing rents. A comparative analysis of neighboring counties reveals that areas with similar economic profiles but more aggressive rent control policies have experienced slower rent growth, underscoring the importance of affordability measures.

Policy Interventions and Their Impact: Local and state policies can significantly influence rent stabilization. California's Tenant Protection Act of 2019, which caps annual rent increases at 5% plus inflation, has had a moderating effect on Orange County's rental market. Additionally, the county's inclusionary housing policies, which require developers to allocate a percentage of units for low- and moderate-income households, contribute to a more balanced housing stock. However, it's essential to approach policy interventions cautiously. Overly restrictive measures may discourage new development, exacerbating the housing shortage. A nuanced approach, combining incentives for affordable housing production with tenant protections, is more likely to foster long-term rent stabilization.

Demographic Shifts and Lifestyle Changes: Evolving demographics and lifestyle preferences also play a role in shaping rent trends. Orange County is experiencing a growing population of remote workers, who prioritize flexibility and affordability over proximity to traditional employment hubs. This shift has led to increased demand for rental properties in suburban and exurban areas, where rents are generally lower. Furthermore, the rise of co-living spaces and accessory dwelling units (ADUs) provides alternative housing options, particularly for younger renters and those seeking more affordable arrangements. These trends contribute to a more diversified rental market, reducing pressure on traditional apartment rentals and supporting overall rent stabilization.

To promote sustained rent stabilization, stakeholders should focus on a multi-pronged strategy. This includes: (1) incentivizing the development of affordable housing units, (2) implementing targeted rent control measures that balance tenant protections with landlord incentives, (3) fostering economic growth that outpaces rent increases, and (4) adapting to shifting demographic and lifestyle trends. By addressing these factors in a coordinated manner, Orange County can work towards a more stable and equitable rental market.

Contract for Deed vs. Rent-to-Own: Understanding Key Differences

You may want to see also

Explore related products

![]()

Impact of housing supply on rental rates

The relationship between housing supply and rental rates is a delicate balance, and in Orange County, this equilibrium has been a key factor in the recent rental market trends. As of the latest data, the county's rental landscape is showing signs of a shift, with a potential leveling off of rents after a period of rapid growth. This phenomenon can be largely attributed to the gradual increase in housing supply, which has started to meet the high demand that has characterized the region for years.

Analyzing the Supply-Demand Dynamics:

In economics, the law of supply and demand is fundamental, and the housing market is no exception. Orange County's rental market has been a prime example of this principle. Historically, the county has experienced a housing supply shortage, driving rental rates upwards as demand consistently outpaced available units. However, recent developments indicate a change in this trajectory. The completion of several large-scale residential projects has introduced a significant number of new rental units to the market. This increased supply has the potential to alleviate the pressure on rental prices, providing a much-needed respite for tenants.

The Role of New Developments:

A closer look at the data reveals that the impact of new housing developments on rental rates is not immediate but rather a gradual process. For instance, in the past year, Orange County saw the addition of over 2,000 new apartment units, primarily in urban centers like Irvine and Anaheim. This influx of supply has started to show effects, with average rental prices in these areas increasing at a slower rate compared to previous years. The trend suggests that as more projects reach completion, the county could witness a more pronounced stabilization or even a slight decline in rents, especially in neighborhoods with a higher concentration of new developments.

A Comparative Perspective:

To understand the potential future of Orange County's rental market, it's instructive to compare it with other regions that have experienced similar supply-driven shifts. For instance, Seattle's rental market underwent a comparable transformation a few years ago. After a period of rapid rent growth, a surge in new apartment constructions led to a leveling off of prices, providing relief to renters. This example illustrates that while increased supply may not lead to immediate rent decreases, it can effectively curb the rate of growth, offering a more sustainable rental environment.

Practical Implications for Renters and Investors:

For renters in Orange County, the current trend is a positive sign, indicating that the rapid rent increases might be becoming a thing of the past. This could mean more negotiating power and better long-term rental stability. However, it's essential to note that the impact of increased supply varies across neighborhoods. Renters should research areas with upcoming or recently completed developments, as these are more likely to offer competitive rates. For investors and developers, the message is clear: while the market is adjusting, there is still a demand for housing, particularly in well-planned, amenity-rich communities. Balancing supply with the unique needs of Orange County's diverse population will be crucial in maintaining a healthy rental market.

In summary, the impact of housing supply on rental rates in Orange County is a critical aspect of understanding the current market dynamics. The recent trends suggest that a strategic increase in supply can effectively moderate rent growth, providing a more stable environment for renters and investors alike. As the county continues to navigate its housing challenges, a nuanced approach to development, considering both quantity and quality, will be essential for long-term success.

Late Rent Penalties: Daily Charges and Their Implications

You may want to see also

Explore related products

![]()

Economic conditions affecting tenant affordability

Orange County's rental market has been a rollercoaster in recent years, with rents soaring to unprecedented heights. However, recent data suggests a potential shift, as some areas are experiencing a slowdown in rent growth. This begs the question: what economic conditions are influencing tenant affordability in the region?

The Supply-Demand Imbalance: A Key Factor

Consider the fundamental economic principle of supply and demand. In Orange County, a surge in new apartment constructions has increased the housing supply, particularly in cities like Irvine and Anaheim. This influx of new units has helped alleviate the extreme demand pressures that drove rents upward. For instance, a 2023 report by Yardi Matrix reveals that over 5,000 new apartment units were completed in Orange County, with an additional 10,000 units under construction. As a result, vacancy rates have risen slightly, giving tenants more negotiating power and slowing rent growth.

Interest Rates and Housing Affordability: A Complex Relationship

The Federal Reserve's interest rate hikes have had a ripple effect on the housing market. Higher mortgage rates have priced some buyers out of the market, increasing demand for rental properties. However, this effect is mitigated by the fact that higher interest rates also discourage new construction, as developers face increased borrowing costs. In Orange County, this has led to a nuanced situation where rents are leveling off, but not necessarily decreasing. Tenants aged 25-40, who are most likely to be first-time homebuyers, are particularly affected by these conditions. To navigate this landscape, consider negotiating lease terms, such as longer-term contracts with capped rent increases, to secure more stable housing costs.

Local Economic Conditions: A Double-Edged Sword

Orange County's robust job market, driven by industries like healthcare, technology, and tourism, has historically supported high rents. However, recent layoffs in the tech sector and a slowdown in tourism growth have reduced demand for housing in certain areas. For example, cities like Santa Ana and Garden Grove have seen rent growth slow to around 2-3% annually, compared to the double-digit increases of previous years. To take advantage of these localized trends, tenants should research neighborhood-specific data and consider areas with a diverse economic base, which are more resilient to industry-specific downturns.

Practical Tips for Tenants: Navigating the Affordability Landscape

To improve affordability, tenants can take proactive steps such as:

- Timing the rental search: Aim to sign leases during winter months (December-February), when demand is typically lower.

- Considering alternative housing options: Explore co-living spaces or accessory dwelling units (ADUs), which can offer more affordable rents.

- Negotiating rent and lease terms: Request a lower rent or additional amenities, such as a parking space or storage unit, in exchange for a longer lease commitment.

- Monitoring local economic indicators: Stay informed about job growth, construction activity, and tourism trends in your target neighborhoods to anticipate rent fluctuations.

By understanding the economic conditions affecting tenant affordability in Orange County, renters can make informed decisions and secure more stable housing costs. As the market continues to evolve, staying ahead of these trends will be crucial for navigating the region's complex rental landscape.

Easy Guide to Renting a Scooter in Washington, DC

You may want to see also

Explore related products

![]()

Comparison of Orange County rents to neighboring areas

Orange County’s rental market has long been a benchmark for Southern California’s housing trends, but its prices don’t exist in a vacuum. To understand whether rents are leveling off, it’s critical to compare them to neighboring areas like Los Angeles County, Riverside County, and San Bernardino County. These regions share similar economic drivers—employment hubs, lifestyle attractions, and proximity to major cities—yet their rental markets diverge in notable ways. For instance, while Orange County’s median rent hovers around $2,800 for a one-bedroom apartment, Riverside County’s median is roughly $1,800, reflecting a stark affordability gap. This comparison isn’t just about numbers; it’s about understanding why renters might opt for a longer commute in exchange for lower costs.

Analyzing the data reveals a pattern: Orange County’s rents, though historically higher, have begun to plateau in recent months, while neighboring areas continue to see modest increases. Los Angeles County, for example, saw a 3% rent hike in the past year, driven by demand in tech and entertainment sectors. In contrast, Orange County’s growth has stalled at 1%, suggesting a potential saturation point. This divergence could be attributed to Orange County’s limited housing supply and stricter zoning laws, which have historically kept inventory low and prices high. Meanwhile, Riverside and San Bernardino Counties are experiencing a construction boom, adding thousands of new units and keeping rent growth in check.

For renters weighing their options, the comparison highlights a trade-off between convenience and cost. Orange County’s proximity to major employers like Disneyland, Irvine Spectrum, and John Wayne Airport makes it an attractive but expensive choice. Neighboring areas, however, offer more bang for the buck, particularly for remote workers or those willing to commute. For example, a two-bedroom apartment in Anaheim (Orange County) averages $3,200, while a similar unit in Corona (Riverside County) costs around $2,400. This $800 difference translates to significant savings over time, though it comes with added commute time and potentially fewer amenities.

Persuasively, the data suggests that Orange County’s rental market is reaching a tipping point where neighboring areas become increasingly competitive. For investors, this signals an opportunity to diversify into more affordable markets with higher growth potential. For policymakers, it underscores the need to address Orange County’s housing supply constraints to prevent further displacement of middle-income renters. Meanwhile, renters themselves should consider expanding their search radius, using tools like rent-to-income calculators to determine the financial feasibility of living in adjacent counties.

In conclusion, while Orange County’s rents may be leveling off, the broader regional context tells a more nuanced story. Neighboring areas offer viable alternatives, but their appeal depends on individual priorities—whether it’s affordability, proximity to work, or quality of life. By comparing these markets, renters, investors, and policymakers can make informed decisions that align with their goals, ensuring a more balanced and sustainable housing landscape across Southern California.

When Should Landlords Stop Charging Rent: Key Considerations for Tenants

You may want to see also

Frequently asked questions

Yes, recent data indicates that rent growth in Orange County is slowing down, with some areas experiencing minimal increases or even slight decreases compared to the rapid rises seen in previous years.

Factors include increased housing supply, rising interest rates reducing demand for rentals, and economic uncertainties that are making renters more cautious about affordability.

While predictions vary, many experts believe rents may stabilize or grow at a slower pace in the near future, though long-term trends will depend on economic conditions, housing policies, and population growth.