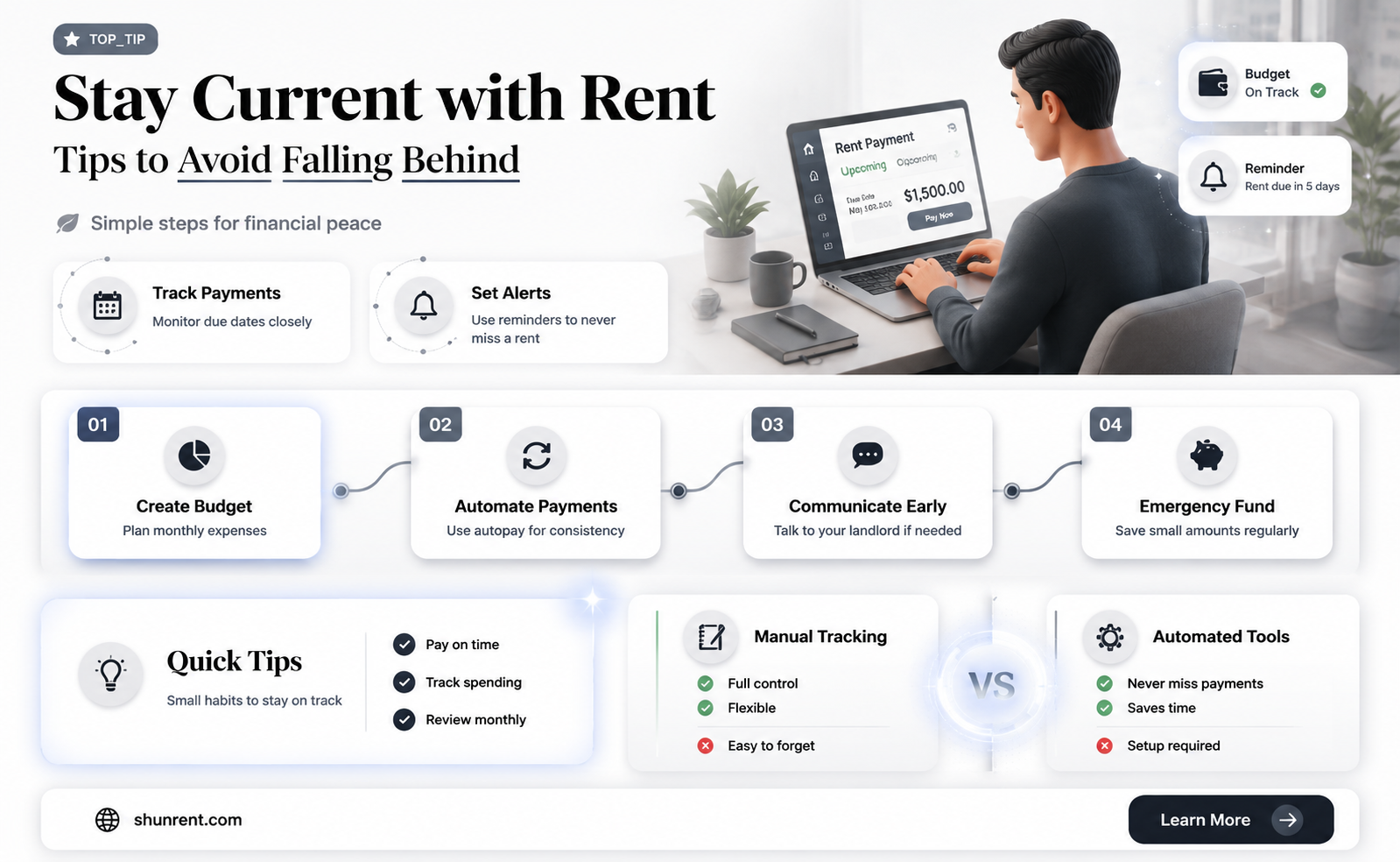

The question of whether you are presently current with your rent is a critical aspect of financial responsibility and tenant-landlord relationships. Staying up-to-date with rent payments ensures compliance with lease agreements, avoids late fees, and maintains a positive standing with your landlord. It also reflects your ability to manage personal finances effectively. Falling behind on rent can lead to eviction notices, legal complications, and damage to your credit score. Regularly reviewing your payment schedule and addressing any discrepancies promptly can help you stay current and avoid unnecessary stress. If you’re unsure about your payment status, it’s advisable to check your records or contact your landlord for clarification.

Explore related products

$9.99

What You'll Learn

![]()

Understanding Rent Due Dates

Rent due dates are not arbitrary; they are typically structured around the landlord’s mortgage payments, property management cycles, or local housing regulations. For tenants, understanding these dates is critical to maintaining financial stability and avoiding late fees, which can range from 5% to 10% of the monthly rent in many jurisdictions. For example, if your rent is $1,200, a 5% late fee adds $60 to your burden—a cost easily avoided with proper planning. Always review your lease agreement to confirm the exact due date, as it may differ from the common practice of rent being due on the first of the month.

A common misconception is that the "grace period" extends the due date. In reality, a grace period (usually 3–5 days) is a buffer before late fees are applied, not an extension of the payment deadline. For instance, if rent is due on the 1st and there’s a 5-day grace period, paying on the 6th incurs penalties. Tenants should treat the due date as non-negotiable and use the grace period as a safety net for unexpected delays, not a habit. Proactive communication with your landlord can sometimes prevent fees if you’re a day or two late, but this should be the exception, not the rule.

Comparing rent due dates across different housing markets reveals regional variations. In New York City, rent is often due on the 1st with a 5-day grace period, while in California, leases may allow payment up to the 5th without penalty. These differences underscore the importance of local research. For international tenants, currency exchange rates and transfer times can complicate timely payments; using automated payment systems or setting reminders 3–5 days in advance can mitigate these risks. Understanding these nuances ensures compliance and avoids unnecessary stress.

To stay current, adopt a system that aligns with your financial habits. If you’re paid biweekly, set aside half the rent from each paycheck into a dedicated account. Apps like Mint or Excel templates can track savings progress. For those prone to forgetting, enable auto-pay through your bank or rental platform, but ensure your account has sufficient funds to avoid overdraft fees, which average $35 per transaction. Lastly, keep a digital or physical calendar marked with due dates and grace period deadlines—a simple yet effective visual reminder.

In conclusion, mastering rent due dates requires clarity, discipline, and adaptability. By understanding the structure behind these dates, dispelling myths about grace periods, and tailoring strategies to your circumstances, you can avoid financial pitfalls. Staying current isn’t just about meeting deadlines—it’s about building a reliable tenant profile that fosters trust with landlords and safeguards your housing stability. Treat rent payments as a non-negotiable priority, and the rewards will extend beyond avoiding late fees.

Average PSF Rent for Big Box Tenants: A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Late Payment Penalties Explained

Late payment penalties are a landlord's tool to encourage timely rent payments, but they can quickly escalate a minor oversight into a financial burden for tenants. Understanding how these penalties work is crucial for anyone renting a property. Typically, late fees are a fixed amount or a percentage of the rent, charged after a grace period, usually 3 to 5 days post the due date. For instance, a common structure might be a $50 flat fee or 5% of the monthly rent, whichever is greater. These fees are not arbitrary; they are often outlined in the lease agreement, making it essential to read and understand your contract thoroughly.

The impact of late payment penalties extends beyond the immediate financial hit. Repeated late payments can lead to a strained landlord-tenant relationship, potentially resulting in eviction notices or legal actions. Moreover, some landlords report late payments to credit bureaus, which can negatively affect your credit score. A single late payment can remain on your credit report for up to seven years, influencing your ability to secure loans, credit cards, or even future rentals. This underscores the importance of prioritizing rent payments to avoid long-term financial consequences.

To mitigate the risk of late payment penalties, consider setting up automatic payments through your bank or using rent payment apps that offer reminders and scheduling features. If you anticipate difficulty in paying on time, communicate with your landlord proactively. Many landlords are willing to work out a payment plan or extend the due date if informed in advance. Additionally, keeping a small emergency fund can provide a buffer for unexpected financial shortfalls, ensuring you remain current with your rent.

Comparatively, late payment penalties in renting differ from those in other financial obligations, such as credit card bills or loans. While credit card late fees are often capped by law (e.g., $28 for the first offense, $39 for subsequent ones), rent late fees can vary widely and are primarily governed by state laws and individual lease agreements. This lack of uniformity makes it even more critical for tenants to be aware of their specific lease terms and local regulations.

In conclusion, late payment penalties are more than just an additional charge; they are a mechanism with far-reaching implications. By understanding the structure, potential consequences, and preventive measures, tenants can navigate their rental agreements more effectively. Staying informed and proactive not only helps in avoiding unnecessary fees but also fosters a positive and stable living situation. Always remember, being current with your rent is not just a financial responsibility—it’s a key to maintaining your financial health and peace of mind.

Insurance Coverage for Rented Lights: Do You Need More?

You may want to see also

Explore related products

![]()

Rent Payment Methods Overview

Rent payment methods have evolved significantly, offering tenants and landlords a variety of options to ensure timely and secure transactions. From traditional checks to digital platforms, the choice of method can impact convenience, security, and even financial planning. Understanding these options is crucial for maintaining a positive landlord-tenant relationship and staying current with rent obligations.

Analytical Perspective:

The most common rent payment methods include checks, online banking transfers, mobile payment apps, and direct deposit systems. Each method carries distinct advantages and drawbacks. For instance, checks are straightforward but prone to delays and loss, while mobile apps like Venmo or Zelle offer instant transfers but may lack formal payment records. Landlords often prefer methods that provide verifiable receipts and reduce administrative burden, such as automated clearing house (ACH) transfers, which are both secure and cost-effective. Tenants, on the other hand, may prioritize convenience and low fees, making platforms like PayPal or CashApp appealing despite potential transaction limits.

Instructive Approach:

To choose the best rent payment method, consider these steps: First, review your lease agreement to confirm accepted payment types. Second, assess your financial habits—do you prefer manual payments or automated systems? Third, evaluate fees associated with each method; for example, credit card payments often incur 2-3% processing charges, which can add up over time. Finally, prioritize security by using methods that encrypt data and provide transaction confirmations. For instance, setting up recurring ACH payments through your bank ensures rent is paid on time without requiring monthly reminders.

Comparative Analysis:

Digital payment methods are increasingly popular due to their speed and convenience, but they aren’t without risks. For example, while Venmo allows for quick transfers, it lacks built-in protections for disputes, unlike traditional bank transfers. Similarly, paying rent with a credit card can help build credit history but may tempt overspending if balances aren’t managed carefully. In contrast, prepaid rent cards—a newer option—offer a middle ground by allowing tenants to load funds in advance, ensuring landlords receive payment while tenants maintain control over their spending.

Descriptive Insight:

Imagine a tenant who uses a combination of methods to stay current: they set up an ACH transfer for the bulk of their rent but supplement it with a small credit card payment to earn rewards. This hybrid approach maximizes benefits while minimizing risks. Meanwhile, a landlord might offer incentives for tenants who use automated payments, such as waiving late fees or providing a small discount, fostering mutual convenience and reliability. Such strategies highlight how understanding payment methods can lead to innovative solutions for both parties.

Practical Tips:

To ensure you’re always current with your rent, establish a routine that aligns with your chosen payment method. For automated payments, mark your calendar to verify transactions each month. If using checks, mail them at least five business days before the due date to account for postal delays. Keep digital receipts in a dedicated folder for easy access during disputes or audits. Lastly, communicate openly with your landlord about any changes in your payment method or financial situation—proactive transparency can prevent misunderstandings and strengthen trust.

Renting Fifty Shades Darker on DirecTV: A Quick Guide

You may want to see also

Explore related products

![Adams Notice to Pay Rent or Vacate, Forms and Instructions [Print and Downloadable] (LF280), White](https://m.media-amazon.com/images/I/71+VR98L6sL._AC_UL320_.jpg)

$11.99

![]()

Rent Increase Notifications Guide

Rent increase notifications are a critical touchpoint in the landlord-tenant relationship, requiring clarity, compliance, and empathy. Landlords must adhere to local laws dictating notice periods, which typically range from 30 to 90 days, depending on the jurisdiction and lease type. For instance, in California, a 60-day notice is required for increases over 10%, while New York mandates 30 days for month-to-month tenants. Always verify your local ordinances to avoid legal pitfalls.

Crafting the notification itself demands precision and professionalism. Begin with a clear subject line, such as "Important Notice Regarding Rent Adjustment," to ensure tenants recognize its urgency. Include the current rent amount, the new rent, and the effective date of the change. Provide a concise reason for the increase, whether it’s rising property taxes, maintenance costs, or market adjustments. Transparency builds trust and reduces disputes. For example, "Due to increased property taxes and utility costs, your monthly rent will adjust from $1,200 to $1,300, effective October 1, 2023."

Tenants often respond emotionally to rent increases, so anticipate their concerns and address them proactively. Offer resources, such as local rent assistance programs or budgeting tips, to demonstrate goodwill. If feasible, consider phased increases or incentives, like a waived late fee for on-time payments, to ease the transition. Remember, retaining a good tenant is often more cost-effective than finding a new one.

Finally, document everything meticulously. Send the notice via certified mail or email with read receipts to prove delivery. Keep copies of all communications and lease agreements in case of disputes. While no landlord enjoys delivering bad news, a well-executed rent increase notification can preserve the relationship and ensure compliance with legal standards.

How to Properly Calculate Your Rent Certificate

You may want to see also

Explore related products

![]()

Lease Renewal Process Details

Being current with your rent is the first step in a smooth lease renewal process, but it’s only the beginning. Landlords typically review payment history, property condition, and tenant behavior before offering a renewal. Late payments, even if eventually settled, can flag your account as high-risk, potentially leading to non-renewal or increased scrutiny. Pro tip: If you’ve had a slip-up, address it proactively with your landlord—a written explanation and commitment to timely payments can salvage your standing.

The lease renewal process varies by jurisdiction, but most follow a structured timeline. In many states, landlords must notify tenants 30–60 days before the lease ends, specifying terms or rent increases. Tenants usually have 14–30 days to respond. Miss these deadlines, and you could face automatic month-to-month conversion or lease termination. Mark your calendar 90 days before your lease ends to allow time for negotiation or alternative planning.

Rent increases are a common point of contention during renewals. Landlords can raise rent by up to 10% annually in unregulated areas, but some cities cap increases at 3–5%. Research local rent control laws to understand your rights. If faced with a steep hike, negotiate by offering a longer lease term (e.g., 2 years) in exchange for a lower increase. Document all communication—verbal agreements hold no weight in disputes.

Inspecting the property before renewal benefits both parties. Landlords assess wear and tear, while tenants can request repairs or upgrades as part of the renewal agreement. Minor issues like chipped paint or loose fixtures are typically the tenant’s responsibility, but structural problems (e.g., leaky roofs) fall on the landlord. Take photos during the inspection to avoid disputes later. A well-maintained property strengthens your case for renewal on favorable terms.

Finally, review the renewal contract carefully. Some landlords slip in new clauses, like pet restrictions or increased late fees. Compare it to your original lease and question any discrepancies. If you’re unsure, consult a tenant advocacy group or attorney. Signing blindly could bind you to unfavorable terms for another year. Remember: Renewal is an opportunity to renegotiate, not just a formality.

Renting Your Orange County Condo: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Yes, I am currently up to date with all rent payments as per the lease agreement.

Being current with rent means all payments have been made on time and in full, with no outstanding balances due.

You can check your payment records, bank statements, or contact your landlord or property manager for confirmation.

If you are not current, you may face late fees, eviction notices, or legal action, depending on the terms of your lease and local laws.

Yes, you can become current by paying any missed amounts, including late fees, as soon as possible. Communicate with your landlord to resolve the issue promptly.