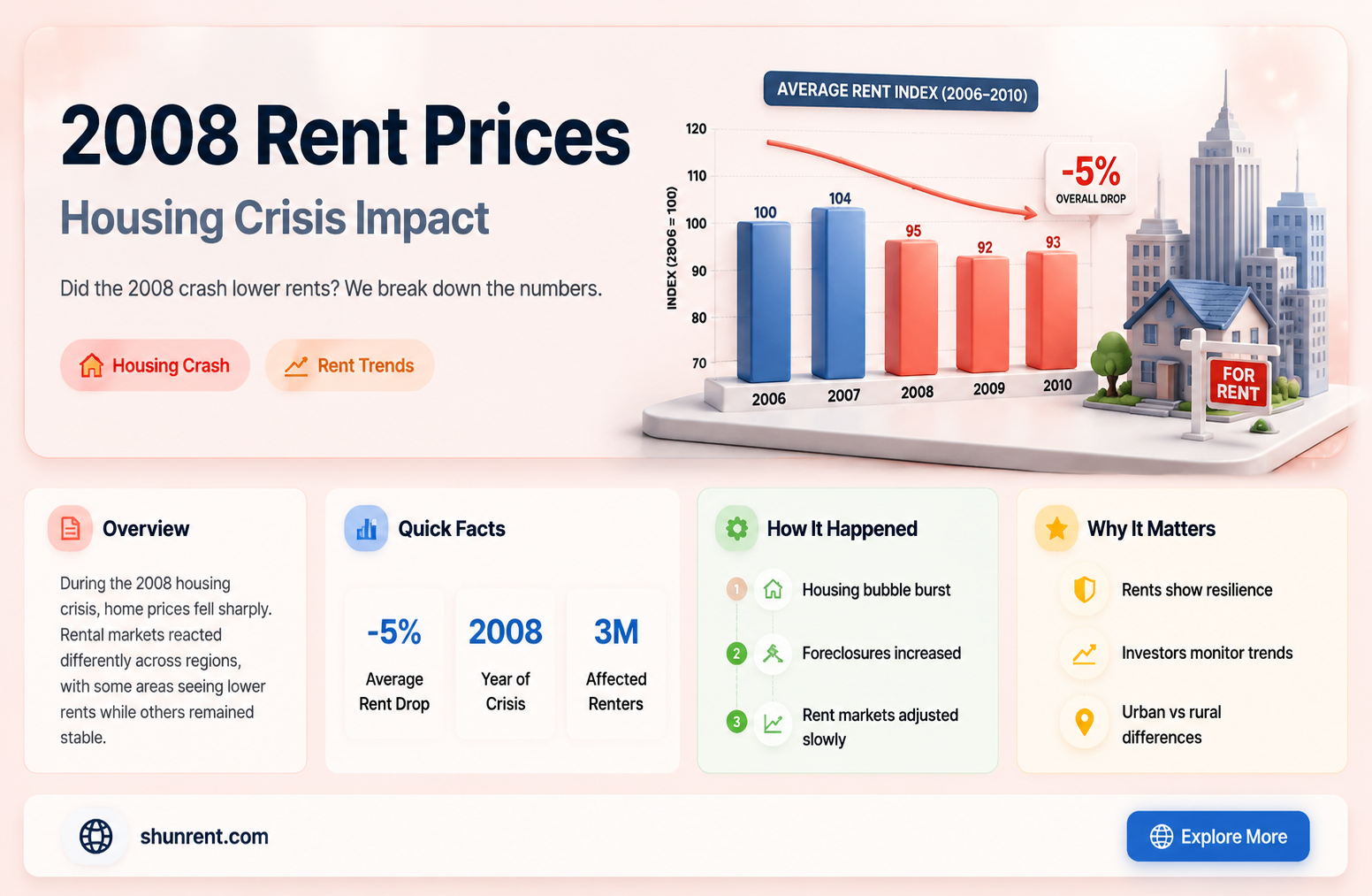

The year 2008 was marked by significant economic turmoil, primarily due to the global financial crisis triggered by the collapse of the U.S. housing market and the subsequent recession. This period had a profound impact on various sectors, including the rental market. As homeowners faced foreclosures and the housing market plummeted, many turned to renting, increasing demand for rental properties. However, the overall economic downturn also led to job losses and reduced consumer spending, which could have potentially offset this demand. Consequently, the question of whether rent prices went down in 2008 is complex, varying by region and influenced by the interplay of these economic forces.

| Characteristics | Values |

|---|---|

| Year | 2008 |

| Rent Price Trend | Generally decreased in many U.S. cities, especially in areas heavily affected by the housing market crash. |

| National Average Rent Change | Declined by approximately 2-4% in 2008, depending on the source. |

| Hardest-Hit Cities | Cities like Phoenix, Las Vegas, and Miami saw significant rent decreases due to high foreclosure rates and oversupply of housing. |

| Stable or Increasing Markets | Some cities, such as New York and San Francisco, saw minimal changes or slight increases in rent prices due to stronger local economies. |

| Economic Context | The 2008 financial crisis and housing market collapse led to reduced demand for rental properties in many areas. |

| Vacancy Rates | Increased in many markets, contributing to downward pressure on rent prices. |

| Long-Term Impact | Rent prices began to recover in subsequent years as the economy stabilized and demand for rentals increased. |

| Data Sources | U.S. Census Bureau, Zillow, and other real estate market reports. |

Explore related products

What You'll Learn

- Economic Recession Impact: How the 2008 recession directly influenced rent prices nationwide

- Housing Market Crash: Effects of the housing crash on rental demand and pricing

- Urban vs. Rural Trends: Comparison of rent changes in cities versus rural areas in 2008

- Foreclosure Rates: Role of increased foreclosures in shifting rental market dynamics

- Government Interventions: Impact of 2008 policies on stabilizing or reducing rent prices

![]()

Economic Recession Impact: How the 2008 recession directly influenced rent prices nationwide

The 2008 economic recession, triggered by the collapse of the housing market and financial crisis, had a profound and multifaceted impact on rent prices across the United States. As homeowners faced foreclosures and tightened credit conditions, many were forced to transition from owning to renting, increasing demand in the rental market. This surge in demand, particularly in urban areas, initially put upward pressure on rents. However, the broader economic downturn, characterized by job losses and reduced consumer spending, soon counterbalanced this trend. By mid-2008, rent prices began to stabilize and, in some regions, decline as landlords struggled to fill vacancies in an oversaturated market.

Analyzing the data reveals a nuanced picture of regional disparities. In hard-hit areas like Florida, Arizona, and California, where the housing bubble burst most dramatically, rent prices dropped significantly as former homeowners flooded the rental market. For instance, in Miami, rents fell by as much as 10% in 2008, while Phoenix saw a 7% decline. Conversely, cities with stronger job markets and lower foreclosure rates, such as Washington, D.C., and Boston, experienced more modest changes or even slight increases in rents. This variation underscores the importance of local economic conditions in shaping rental trends during a national recession.

From a practical standpoint, renters in 2008 found themselves in a unique position of negotiating power. With vacancy rates rising, landlords became more willing to offer concessions, such as reduced rents, waived fees, or month-to-month leases. Prospective tenants could leverage this environment by researching local market conditions, comparing prices, and negotiating terms. For example, in markets with high vacancy rates, renters could request rent reductions of 5–10% or ask for upgrades like new appliances or utilities included in the rent. This period also highlighted the value of flexibility; short-term leases allowed renters to adapt to changing economic circumstances without long-term commitments.

Comparatively, the 2008 recession’s impact on rent prices differed from previous downturns due to the housing crisis’s central role. Unlike recessions driven solely by job losses or reduced consumer spending, the 2008 recession created a dual dynamic: increased rental demand from displaced homeowners and decreased consumer confidence. This duality led to a temporary stabilization of rents in some areas, even as economic conditions worsened. In contrast, recessions like the early 1990s downturn saw more uniform rent declines due to straightforward reductions in demand. Understanding this distinction is crucial for predicting how future economic shocks might affect rental markets.

In conclusion, the 2008 recession directly influenced rent prices nationwide through a complex interplay of increased rental demand, economic hardship, and regional disparities. While some areas experienced significant rent declines, others saw stabilization or modest increases, reflecting local economic conditions. For renters, this period offered opportunities to negotiate better terms and adapt to changing circumstances. The recession’s unique dynamics also provide valuable insights for understanding how housing crises and economic downturns intersect to shape rental markets, offering lessons for both tenants and policymakers in future economic challenges.

Is Renting from Enterprise for a Week Cost-Effective? A Breakdown

You may want to see also

Explore related products

![]()

Housing Market Crash: Effects of the housing crash on rental demand and pricing

The 2008 housing market crash sent shockwaves through the economy, but its impact on rent prices wasn't as straightforward as a universal decline. While some areas saw dips, others experienced surprising stability or even increases. This paradox highlights the complex relationship between homeownership, rental demand, and local market dynamics.

Let's dissect this phenomenon.

A Surge in Demand, A Temporary Dip in Prices: The crash triggered a wave of foreclosures, forcing many homeowners into the rental market. This sudden influx of renters initially put downward pressure on prices in some regions, particularly those hit hardest by the crisis. Cities like Phoenix and Las Vegas, where speculative buying fueled a housing bubble, saw rent prices soften as supply temporarily outpaced demand.

However, this trend was often short-lived.

The Long-Term Shift: A Renters' Market Emerges: As the dust settled, a new reality emerged. The crash eroded confidence in homeownership, leading to a cultural shift towards renting. Millennials, entering their prime renting years, further fueled this trend, prioritizing flexibility and affordability over the traditional American dream of owning a home. This sustained increase in rental demand ultimately pushed prices upwards in many markets, even surpassing pre-crash levels.

Think of it as a pendulum swing: the initial shock caused a temporary dip, but the long-term consequences tilted the market decisively in favor of landlords.

Local Nuances Matter: It's crucial to remember that national trends mask significant local variations. Factors like job growth, population density, and the pre-crash housing market health played a pivotal role in determining how rent prices responded. For instance, cities with strong job markets and limited housing stock, like San Francisco and New York, saw rent prices remain relatively stable or even rise during the crisis, as demand remained high despite the economic downturn.

Lessons Learned: A Cautionary Tale: The 2008 crash offers valuable insights for both renters and policymakers. For renters, it underscores the importance of understanding local market dynamics and being prepared for potential fluctuations. For policymakers, it highlights the need for robust tenant protections and affordable housing initiatives to mitigate the impact of future economic shocks on vulnerable populations. The crash may have initially seemed like a boon for renters, but its long-term legacy was a more complex and challenging rental landscape.

Best Boat Rental Spots on Kentucky Lake: Your Ultimate Guide

You may want to see also

Explore related products

![]()

Urban vs. Rural Trends: Comparison of rent changes in cities versus rural areas in 2008

The 2008 financial crisis sent shockwaves through the housing market, but its impact on rent prices wasn't uniform. While urban areas, particularly those heavily reliant on finance and real estate, saw dramatic rent declines, rural regions often experienced a different trajectory. This disparity highlights the complex interplay between economic forces and local market dynamics.

Urban centers, like New York City and Las Vegas, witnessed a sharp drop in rents as job losses and foreclosures pushed residents towards more affordable options. Data from Zillow shows that in 2008, rents in Manhattan fell by 5.4%, while Las Vegas saw a staggering 12.7% decline. This urban downturn was fueled by a combination of factors: a glut of vacant apartments due to halted construction projects, a surge in foreclosures forcing homeowners into the rental market, and a general economic pessimism that discouraged new leases.

Conversely, many rural areas experienced rent stability or even modest increases during this period. Smaller towns and suburban areas, often less exposed to the financial sector, saw less severe job losses. Additionally, the flight from expensive cities led some renters to seek refuge in more affordable rural locations, driving up demand and, in some cases, rents. This trend was particularly evident in areas near major cities, where commuters sought a balance between affordability and proximity to urban centers.

This urban-rural rent divergence illustrates the importance of local context in understanding housing market fluctuations. While national trends provide a broad picture, they often mask significant regional variations. For instance, while overall U.S. rents fell by 2.4% in 2008 according to the Bureau of Labor Statistics, this figure obscures the stark differences between booming rural areas and struggling urban centers.

Understanding these regional disparities is crucial for both renters and policymakers. Renters seeking affordability during economic downturns may find better options in rural areas, while urban dwellers might need to negotiate rent reductions or explore shared housing arrangements. Policymakers, on the other hand, need to tailor housing policies to address the specific needs of different regions, ensuring that both urban and rural residents have access to stable and affordable housing, regardless of economic conditions.

Richmond VA Rent Trends: Average Costs and What to Expect

You may want to see also

Explore related products

![]()

Foreclosure Rates: Role of increased foreclosures in shifting rental market dynamics

The 2008 housing crisis unleashed a wave of foreclosures, pushing millions of homeowners into the rental market. This sudden influx of new renters, coupled with a shrinking supply of available homes due to foreclosures being tied up in legal proceedings, created a perfect storm for rent prices.

Imagine a city where 10% of homeowners lose their properties to foreclosure in a single year. That's 10% more households seeking rental housing, while the number of available units remains stagnant or even decreases as foreclosed homes sit vacant. Basic economics dictates that increased demand and limited supply lead to higher prices. This is precisely what happened in many areas during the 2008 crisis.

Rents didn't universally skyrocket, however. The impact was felt most acutely in regions with high foreclosure rates and already tight rental markets. Cities like Las Vegas, Phoenix, and Miami, which experienced some of the highest foreclosure rates in the nation, saw significant rent increases despite the overall economic downturn.

This dynamic highlights a crucial point: while the 2008 crisis was primarily a homeowner crisis, its ripple effects were deeply felt in the rental market. Increased foreclosures didn't directly cause rent prices to fall; instead, they contributed to upward pressure on rents in certain areas, demonstrating the complex interplay between homeownership and rental market dynamics.

Save Money on College Books: Rent Textbooks from Barnes & Noble

You may want to see also

Explore related products

![]()

Government Interventions: Impact of 2008 policies on stabilizing or reducing rent prices

The 2008 financial crisis triggered a cascade of government interventions aimed at stabilizing the housing market, but their impact on rent prices was nuanced and often indirect. One key policy was the Troubled Asset Relief Program (TARP), which injected capital into struggling banks to prevent systemic collapse. While TARP’s primary goal was to stabilize the financial sector, it indirectly influenced rental markets by preventing a sharper decline in homeownership rates. By shoring up banks, the program helped maintain mortgage availability, reducing the number of foreclosures that might have pushed former homeowners into the rental market. This, in turn, likely mitigated upward pressure on rents in some areas.

Another critical intervention was the expansion of foreclosure prevention programs, such as the Home Affordable Modification Program (HAMP). These initiatives aimed to keep homeowners in their homes by modifying loan terms, thereby reducing the supply of rental-seeking individuals. In regions with high foreclosure rates, such as Florida and California, these programs may have contributed to rent stabilization or even modest declines. However, their effectiveness varied widely depending on local market conditions and the pace of implementation. For instance, areas with slower foreclosure processing times saw less immediate relief, limiting the program’s impact on rent prices.

The American Recovery and Reinvestment Act (ARRA) of 2009 also played a role, though its effects on rent were more indirect. By investing in infrastructure and providing tax credits, ARRA aimed to stimulate economic recovery and reduce unemployment. A stronger job market could have increased demand for rentals, but the program’s broader economic stabilization likely prevented rent spikes in areas where unemployment remained high. For example, cities like Detroit and Cleveland, which were already struggling pre-2008, saw rents remain relatively flat as ARRA-funded projects created jobs but did not significantly alter housing demand dynamics.

A comparative analysis of regions with and without robust government intervention reveals mixed outcomes. In cities like Phoenix, where foreclosure prevention programs were aggressively implemented, rent increases were tempered compared to pre-crisis trends. Conversely, in areas with less intervention, such as parts of the Midwest, rents remained stagnant due to weak economic fundamentals rather than policy impact. This suggests that while government policies could stabilize rents in distressed markets, their effectiveness was highly context-dependent.

In conclusion, government interventions in 2008 and beyond had a stabilizing effect on rent prices, particularly in hard-hit markets, but their success was uneven. Policies like TARP and HAMP indirectly reduced rental demand by addressing foreclosure crises, while ARRA’s economic stimulus prevented sharper rent declines in struggling regions. For policymakers today, the takeaway is clear: targeted interventions that address both housing supply and economic stability are essential for managing rent prices during economic downturns. Practical tips for future crises include prioritizing rapid implementation of foreclosure prevention programs and coordinating housing policies with broader economic recovery efforts.

Understanding Rent-to-Own: A Comprehensive Guide to This Housing Option

You may want to see also

Frequently asked questions

Yes, rent prices generally declined in 2008, particularly in areas heavily affected by the housing market crash and economic recession.

The decline in rent prices in 2008 was primarily driven by the global financial crisis, high unemployment rates, and a surplus of housing inventory due to foreclosures and reduced demand.

No, rent price declines varied by region. Areas with high foreclosure rates and oversupply of housing, such as Florida, California, and Nevada, saw more significant drops compared to more stable markets.