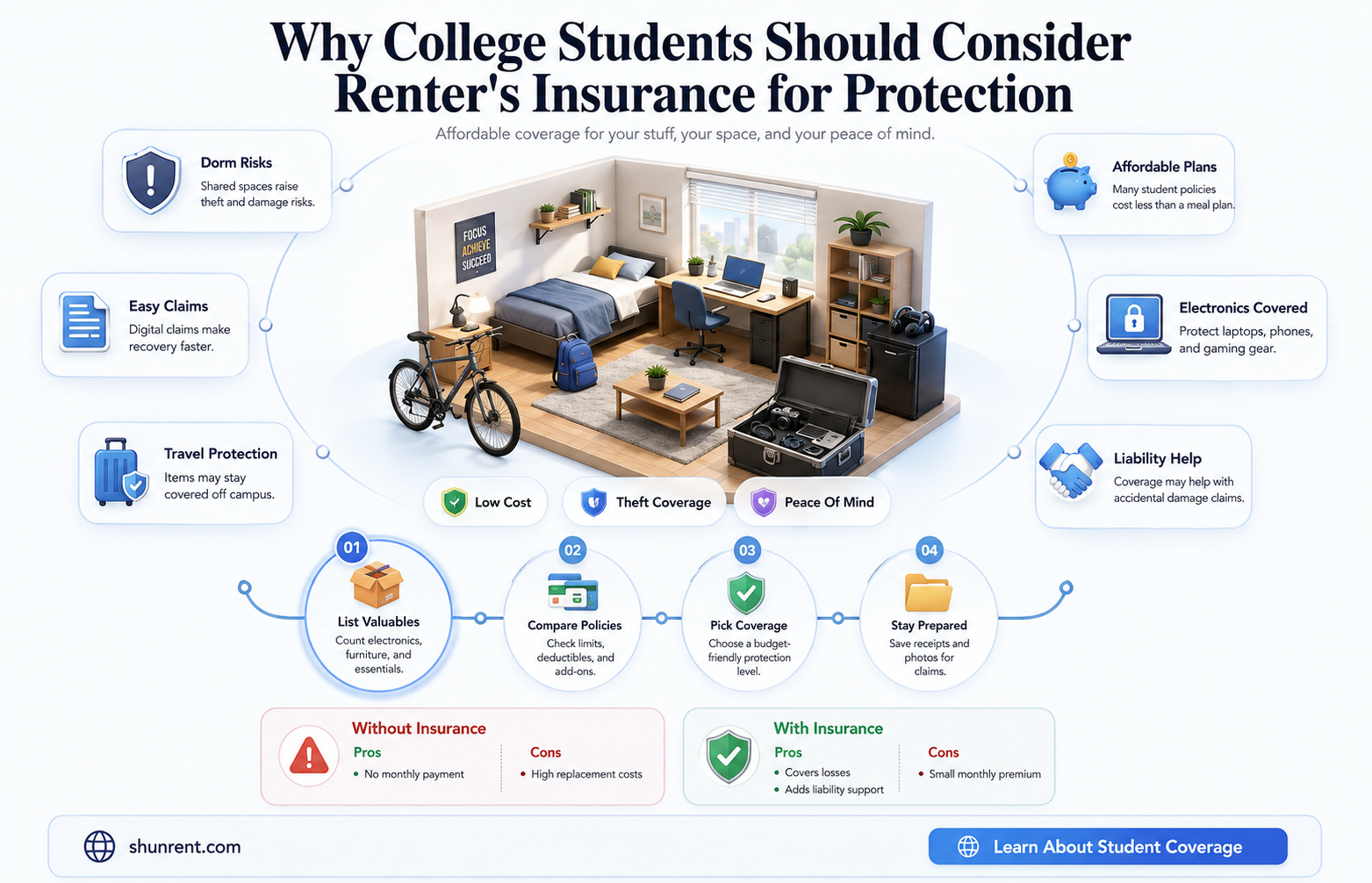

College students often overlook the importance of renter's insurance, assuming their belongings are already protected or that they don’t own enough valuable items to justify the cost. However, whether living in a dorm, apartment, or shared house, their possessions—such as laptops, textbooks, clothing, and furniture—are vulnerable to theft, damage, or loss from events like fires, floods, or break-ins. Renter's insurance not only covers personal property but also provides liability protection in case someone is injured in their rented space, which can be crucial for students on tight budgets. Given the relatively low cost of policies, typically less than $20 per month, renter's insurance offers college students peace of mind and financial protection during a time when unexpected expenses can be particularly burdensome.

| Characteristics | Values |

|---|---|

| Coverage for Personal Belongings | Protects against theft, fire, vandalism, and water damage. |

| Liability Protection | Covers legal expenses if someone is injured in the rented space. |

| Affordability | Typically costs $15-$30 per month, often with student discounts. |

| Roommate Coverage | Policies usually do not extend to roommates; each needs their own. |

| Off-Campus Housing | Highly recommended for students living off-campus. |

| Dormitory Coverage | Some parents’ homeowners’ insurance may cover dorm belongings, but limits often apply. |

| Temporary Housing | Covers belongings during breaks or study abroad periods. |

| High-Value Items | Additional coverage may be needed for expensive items like laptops or jewelry. |

| Ease of Purchase | Can be purchased online or through insurance providers. |

| Peace of Mind | Provides financial security and reduces stress during emergencies. |

| Landlord’s Insurance Limitations | Landlords’ insurance typically covers the building, not tenants’ belongings. |

| Flexibility | Policies can be tailored to fit specific student needs. |

| Claim Process | Generally straightforward, requiring documentation of losses. |

| Preventive Measures | Some insurers offer discounts for safety features like smoke detectors. |

| Legal Requirements | Not legally required but strongly recommended. |

Explore related products

What You'll Learn

- Cost vs. Value: Affordable premiums compared to potential loss coverage for college students

- Roommate Risks: Shared liability and protection against roommate-related damages or theft

- Dorm vs. Off-Campus: Coverage differences for on-campus housing versus private rentals

- Personal Property: Protection for laptops, textbooks, and other student essentials

- Liability Coverage: Financial safeguard against accidental damage or injury claims

![]()

Cost vs. Value: Affordable premiums compared to potential loss coverage for college students

College students often overlook renter's insurance, assuming it’s an unnecessary expense. However, the average cost of a renter’s insurance policy is just $15 to $30 per month—less than the price of a weekly coffee habit. For this modest premium, students gain coverage for personal belongings, liability protection, and even temporary living expenses if their rental becomes uninhabitable. When weighed against the potential loss of a laptop, textbooks, or other essentials, the value becomes clear: a small monthly investment can prevent financial strain in the event of theft, fire, or other disasters.

Consider the scenario of a dorm room fire, a not-uncommon occurrence on college campuses. Without renter’s insurance, a student could be left to replace thousands of dollars’ worth of items out of pocket. A standard policy typically covers up to $15,000 to $30,000 in personal property, depending on the plan. For students living off-campus, liability coverage is equally critical. If a guest is injured in their rental, the policy can cover medical bills and legal fees, potentially saving tens of thousands of dollars. This dual protection—for belongings and liability—makes the cost of premiums a practical safeguard rather than an indulgence.

To maximize value, students should assess their belongings and choose a policy with adequate coverage limits. For instance, those with high-value items like musical instruments or photography equipment may need additional riders to ensure full replacement cost. Additionally, bundling renter’s insurance with an existing auto policy can often reduce premiums by 5% to 15%. Some insurers also offer discounts for students with good grades or those living in secure buildings with fire alarms or sprinkler systems. These strategies make the already affordable premiums even more cost-effective.

A common misconception is that a parent’s homeowner’s insurance will cover a student’s belongings. While some policies extend limited coverage to off-campus students, it’s often insufficient and may require a high deductible. Renter’s insurance, on the other hand, provides comprehensive coverage tailored to a student’s lifestyle. For example, many policies include off-premises coverage, protecting belongings even when they’re not in the rental—ideal for students who frequently move items between home, school, and internships. This portability adds significant value to an already affordable product.

Ultimately, the decision to purchase renter’s insurance comes down to risk tolerance and financial planning. For the cost of a few meals out, students can protect themselves from unexpected losses that could derail their academic and financial stability. By comparing premiums to potential losses, it’s evident that the value of renter’s insurance far outweighs its cost. For college students navigating tight budgets, this small expense is a wise investment in peace of mind and long-term financial health.

USAA Direct Deposit Setup Guide: Simplify Your Rent Payments Today

You may want to see also

Explore related products

![]()

Roommate Risks: Shared liability and protection against roommate-related damages or theft

Living with roommates can be a financial lifesaver for college students, but it also introduces a layer of risk often overlooked: shared liability. When you sign a lease with others, you’re typically jointly responsible for damages to the property, regardless of who caused them. For instance, if your roommate accidentally starts a kitchen fire while attempting to cook ramen at 2 a.m., the landlord can hold all tenants accountable for the repair costs. Renter’s insurance steps in here, covering your portion of the liability and preventing you from footing the bill for someone else’s mistake. Without it, you could be stuck paying out of pocket for damages you didn’t cause, turning a bad situation into a financial nightmare.

Consider the scenario where your roommate’s friend damages property during a visit. In many cases, the lease agreement doesn’t differentiate between tenants and their guests, meaning you could be held responsible for their actions. Renter’s insurance often includes liability coverage, protecting you from claims arising from such incidents. For example, if a guest spills red wine on the landlord’s expensive carpet, your policy could cover the cleaning or replacement costs, shielding you from unexpected expenses. This coverage is particularly crucial in shared living situations where the line between personal responsibility and collective liability blurs.

Theft is another significant risk when living with roommates, especially in dorms or shared apartments where personal boundaries are often tested. While you might trust your roommates, their friends or acquaintances could pose a threat. Renter’s insurance typically covers stolen items, such as laptops, textbooks, or clothing, up to your policy’s limits. For instance, if your $1,000 laptop goes missing after a study group session in your apartment, your insurance could reimburse you for the loss. However, it’s essential to document your belongings with photos, receipts, or a home inventory to streamline the claims process.

A common misconception is that your roommate’s insurance will cover your belongings, but this is rarely the case. Most policies only protect the policyholder’s possessions, leaving your items vulnerable. To avoid this gap, each roommate should have their own renter’s insurance policy. Additionally, some insurers offer discounts for bundling policies or referring roommates, making it a cost-effective solution. For college students on tight budgets, policies often start at around $15–$30 per month, a small price for peace of mind.

Finally, communication is key to mitigating roommate risks. Discuss expectations around guests, security, and shared spaces early on. While renter’s insurance provides a safety net, it’s not a substitute for open dialogue. For example, agreeing to lock doors when leaving or limiting unsupervised guests can reduce the likelihood of theft or damage. Pairing these precautions with the right insurance ensures you’re protected from both foreseeable and unforeseen roommate-related risks. After all, college is stressful enough without worrying about financial fallout from shared living arrangements.

Renting Made Simple: 3-Bed vs. 2-Bed – Which is Easier?

You may want to see also

Explore related products

![]()

Dorm vs. Off-Campus: Coverage differences for on-campus housing versus private rentals

College students often assume their parents’ homeowners insurance will cover their belongings, but this is a risky misconception. While some policies may extend limited coverage to dorm-dwelling students, off-campus renters are typically excluded entirely. This leaves laptops, textbooks, and furniture vulnerable to theft, fire, or water damage without dedicated renter’s insurance. Understanding the coverage gap between on-campus and off-campus living is the first step in protecting your assets.

For dorm residents, the situation is slightly more nuanced. Some homeowners policies provide 10% of personal property coverage for students living in campus housing. However, this often comes with restrictions—high-value items like jewelry or electronics may be capped at a fraction of their worth. Additionally, liability coverage (which protects against lawsuits if someone is injured in your dorm) is rarely included. Relying solely on parental insurance in this scenario is akin to playing financial roulette with your possessions.

Off-campus renters face an even starker reality. Once you step outside university housing, your parents’ policy typically stops at the door. Landlords’ insurance covers the building structure, not your personal belongings. Without renter’s insurance, a single incident—a break-in, a kitchen fire, or a burst pipe—could leave you footing the bill for thousands of dollars in losses. For example, replacing a stolen laptop (average cost: $1,200) or a damaged gaming console ($400–$500) could derail your budget for months.

The solution? Renter’s insurance policies tailored to student needs. For as little as $15–$30 per month, you can secure coverage for personal property (typically $15,000–$30,000) and liability (up to $100,000). Many insurers offer discounts for students with good grades or those living in secure buildings. For dorm residents, adding a rider to your parents’ policy might suffice, but off-campus students should invest in a standalone plan. Pro tip: Document your belongings with photos and receipts—this simplifies claims processing if disaster strikes.

In the dorm vs. off-campus debate, the coverage gap is clear. While dorm dwellers might scrape by with partial protection, off-campus renters are entirely on their own without dedicated insurance. The takeaway? Don’t gamble with your financial stability. Whether you’re bunking in a twin-sized dorm bed or a studio apartment, renter’s insurance is a small price to pay for peace of mind.

Rochester NY Tiller Rentals: Top Spots to Rent a Tiller

You may want to see also

Explore related products

![]()

Personal Property: Protection for laptops, textbooks, and other student essentials

College students often overlook the value of their personal belongings until it’s too late. A laptop worth $1,200, textbooks totaling $500 per semester, and a smartphone valued at $800—these essentials add up quickly. Without renter’s insurance, theft, fire, or water damage could leave a student financially devastated. Consider this: a single incident could cost more than a semester’s tuition, yet a basic renter’s insurance policy typically costs just $15 to $30 per month. The math is clear—protection is far cheaper than replacement.

Let’s break it down step-by-step. First, inventory your belongings. Use a spreadsheet or app to list items, their purchase dates, and values. Include electronics, clothing, furniture, and even bicycles. Next, understand your policy’s coverage limits. Most policies offer $15,000 to $30,000 in personal property protection, but high-value items like laptops may require additional riders. Finally, document everything. Keep receipts, take photos, and store them digitally for easy access in case of a claim.

Now, compare the risks. A 2022 study found that 1 in 10 college students experiences theft during their academic career. In dorms, where doors are frequently left ajar and communal spaces are common, the risk is even higher. Off-campus housing isn’t safer—burglaries in student apartments are 60% more likely than in non-student residences. Renter’s insurance covers these scenarios, ensuring you’re not left paying out of pocket when disaster strikes.

Persuasively, consider the peace of mind renter’s insurance provides. Imagine your laptop is stolen during finals week. Without insurance, you’re scrambling to replace it while juggling exams. With insurance, you file a claim, receive reimbursement, and focus on what matters—your education. For students already juggling tuition, textbooks, and living expenses, this financial safety net is invaluable. It’s not just about protecting possessions; it’s about safeguarding your academic journey.

Descriptively, picture this: a fire breaks out in your apartment building, destroying everything inside. Your textbooks, notes, and laptop—all gone. Without insurance, you’re starting from scratch. With it, you’re back on your feet within weeks. Renter’s insurance doesn’t just cover the cost of items; it covers the cost of continuity. For college students, whose lives are already in flux, this stability is priceless. Don’t wait until it’s too late—protect your essentials today.

Scissor Lift Rental: License Requirements and Safety Tips

You may want to see also

Explore related products

![]()

Liability Coverage: Financial safeguard against accidental damage or injury claims

College life often involves shared spaces, late-night gatherings, and a fair share of mishaps. Imagine this: you’re hosting a study group in your off-campus apartment, and a friend spills coffee on your roommate’s expensive laptop. Or worse, someone trips over a loose rug and sprains their ankle. Without liability coverage, these accidents could lead to costly out-of-pocket expenses or even lawsuits. Liability coverage, a key component of renter’s insurance, steps in to protect you financially from claims of accidental damage or injury to others. It’s not just about covering your belongings; it’s about shielding your future from unexpected liabilities.

Let’s break it down. Liability coverage typically includes two main protections: bodily injury and property damage. If someone is injured in your rented space, this coverage can help pay for medical bills, legal fees, and even settlements if you’re found responsible. For instance, if a guest slips on a wet floor and requires surgery, liability coverage could cover their medical expenses, preventing you from facing a financial crisis. Similarly, if you accidentally damage someone else’s property—say, knocking over a neighbor’s TV—this coverage can help repair or replace it. Most policies offer liability limits starting at $100,000, but you can increase this based on your needs and risk tolerance.

Here’s a practical tip: assess your lifestyle to determine how much liability coverage you need. Are you frequently hosting events? Do you live in a high-traffic area? If so, consider higher limits to ensure you’re fully protected. For example, a college student living in a bustling off-campus house might opt for $300,000 in liability coverage, while someone in a quieter setting could stick with the standard $100,000. Additionally, some policies include "personal liability" extensions, covering incidents that occur outside your home, such as accidentally damaging property at a friend’s place.

Now, let’s compare: liability coverage in renter’s insurance vs. relying on your parents’ homeowner’s policy. While your parents’ policy might offer some protection if you’re still listed as a dependent, it’s often limited and may not cover incidents in your rented space. Having your own renter’s insurance with liability coverage ensures you’re fully protected, regardless of your living situation. Plus, it’s surprisingly affordable—typically $15 to $30 per month, depending on your location and coverage limits.

In conclusion, liability coverage isn’t just an add-on; it’s a necessity for college students navigating shared living spaces. It provides peace of mind, knowing you’re financially protected against accidental damage or injury claims. By understanding your risks and choosing appropriate coverage limits, you can safeguard your finances and focus on what truly matters—your education and experiences. Don’t wait for an accident to happen; invest in renter’s insurance with liability coverage today.

Simplify Rent Collection: A Guide to Setting Up Direct Payments

You may want to see also

Frequently asked questions

Typically, college students living in dorms do not need renter's insurance, as their belongings may be covered under their parents' homeowners or renters insurance policy. However, it’s important to check the policy limits and exclusions to ensure adequate coverage.

Yes, college students living off-campus in apartments or rental homes should strongly consider renter's insurance. It protects their personal belongings from theft, damage, or loss and provides liability coverage if someone is injured in their rental unit.

Renter's insurance is generally affordable, often costing less than $20 per month. Many insurance companies offer discounts for students or allow them to be added to their parents' policy, making it a cost-effective way to protect their belongings.