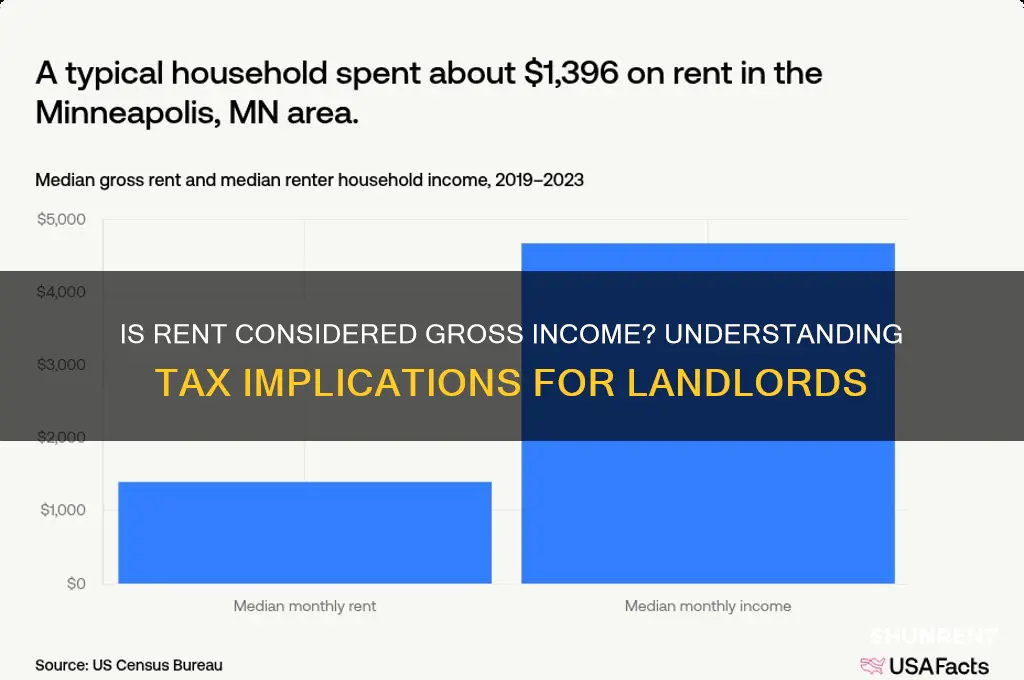

When determining whether to claim rent as gross income, it's essential to understand the tax implications and guidelines set by the Internal Revenue Service (IRS). Generally, rental income is considered taxable and must be reported on your federal tax return, as it is treated as gross income. This includes payments received for the use or occupancy of property, such as residential or commercial spaces. However, certain expenses related to the rental property, like maintenance, repairs, and property management fees, may be deductible, reducing the overall taxable income. It's crucial for landlords and property owners to maintain accurate records and consult tax professionals to ensure compliance with tax laws and to optimize their financial obligations.

| Characteristics | Values |

|---|---|

| Definition | Rent is generally considered gross income if it is received in exchange for the use of property. |

| Tax Treatment | Rent income is typically taxable and must be reported on your tax return. |

| Reporting Requirements | Report rent income on Schedule E (Form 1040) for U.S. federal taxes. |

| Deductions | Expenses directly related to renting the property (e.g., maintenance, property taxes, mortgage interest) can be deducted to reduce taxable rental income. |

| Fair Market Value | If rent is below fair market value for personal use (e.g., renting to a family member), the fair market value may still be considered taxable income. |

| Short-Term Rentals | Income from short-term rentals (e.g., Airbnb) is generally taxable as rental income. |

| Non-Cash Payments | Rent received in the form of services or property is also considered taxable income and must be reported at fair market value. |

| Partial Personal Use | If you use the property personally for part of the year, you must allocate expenses between rental and personal use based on the number of days rented. |

| Security Deposits | Security deposits are not taxable income unless they are forfeited by the tenant and used to cover damages or unpaid rent. |

| State and Local Taxes | Rent income may also be subject to state and local taxes, depending on jurisdiction. |

| 1099 Reporting | If you receive $600 or more in rent from a tenant, they may be required to issue you a Form 1099-MISC or 1099-NEC. |

| Passive Activity Rules | Rental income is generally considered passive income, subject to passive activity loss limitations unless you qualify as a real estate professional. |

Explore related products

What You'll Learn

![]()

Rent as Business Income

Rent received from a property can indeed be classified as business income, but this designation hinges on the nature and scale of the rental activity. The IRS distinguishes between passive rental income and active business income based on the taxpayer’s level of involvement. If you’re merely collecting rent with minimal effort, it’s typically treated as passive income. However, if you’re actively managing multiple properties, providing substantial services (e.g., cleaning, maintenance, or concierge services), or operating a short-term rental business, the IRS may classify this income as business income. This reclassification triggers different tax implications, including eligibility for certain deductions and self-employment taxes.

For example, consider a landlord who owns a single-family home and hires a property management company to handle all tenant interactions and maintenance. In this case, the rent is likely passive income. Contrast this with an Airbnb host who manages multiple listings, coordinates guest check-ins, and provides amenities like stocked kitchens or guided tours. Here, the activity resembles a business, and the income is treated as such. The key differentiator is the taxpayer’s material participation, defined by the IRS as spending more than 500 hours annually on the rental activity or meeting specific involvement tests.

Claiming rent as business income opens the door to additional deductions not available for passive income. Business expenses such as advertising, repairs, depreciation, and even a home office deduction (if applicable) can be written off against the rental income. However, this comes with a trade-off: business income is subject to self-employment taxes, which can increase your tax liability by 15.3%. For instance, if your rental business nets $50,000 annually, you’d owe an additional $7,650 in self-employment taxes. This makes it crucial to weigh the benefits of increased deductions against the higher tax burden.

To navigate this classification effectively, maintain meticulous records of your rental activities. Document hours spent on management, services provided, and expenses incurred. If you’re nearing the threshold for material participation, consider how additional involvement could shift your income classification. For instance, taking on tasks like landscaping or bookkeeping yourself could push you into the business income category. Consulting a tax professional is advisable, as they can help structure your rental activities to maximize deductions while minimizing tax exposure.

In conclusion, whether rent is claimed as business income depends on the taxpayer’s level of engagement and the operational structure of the rental activity. While the business income classification allows for greater deductibility, it also imposes self-employment taxes. Strategic planning and documentation are essential to optimize this classification, ensuring compliance with IRS rules while maximizing financial benefits. For those operating at scale or providing significant services, treating rent as business income can be a prudent tax strategy.

Boating in Wisconsin: License Requirements for Renters

You may want to see also

Explore related products

![]()

Reporting Rental Income

Rental income is generally reported as gross income on your tax return, but understanding the nuances can save you from overpaying or underreporting. The IRS defines gross rental income as all payments you receive for the use of your property, including advance rent, security deposits (if not returned), and any services provided in lieu of rent. For instance, if a tenant pays $1,200 monthly plus utilities valued at $200, your gross income for that month is $1,400. However, not all rental-related payments are treated equally—expenses like property maintenance, mortgage interest, and property taxes can be deducted, but only after reporting the full gross amount.

One critical distinction is how security deposits are handled. If you return the deposit at the end of the lease, it’s not considered income. However, if you retain any portion for damages or unpaid rent, that amount becomes taxable income in the year it’s kept. For example, a $1,000 deposit retained for repairs in 2023 must be reported as income that year. This rule often catches landlords off guard, as it ties taxation to the year of retention, not the year the deposit was initially received.

For those renting out part of their primary residence, the rules shift slightly. If you rent a room or portion of your home for less than 15 days annually, the income is tax-free under the "master’s rule." However, if you exceed this threshold, the entire rental income must be reported, though you can still deduct a portion of expenses based on the rental area’s square footage. For instance, renting a room for 16 days requires reporting all income, but you can deduct 10% of property expenses if the room is 10% of the home’s total area.

Finally, passive activity loss rules can limit your ability to deduct rental losses unless you’re an active participant in managing the property. Active participation requires involvement in making management decisions, not just repairs. For example, approving tenants, setting rental terms, and reviewing financial statements qualify. If your adjusted gross income exceeds $150,000, these deductions phase out, but unused losses carry forward to future years. Properly navigating these rules ensures compliance while maximizing deductions.

San Francisco Rent Guide: Understanding Average Costs in 2023

You may want to see also

Explore related products

![]()

Taxable vs. Nontaxable Rent

Rent received by a landlord is generally considered taxable income, but not all rental income is treated equally under the tax code. The distinction between taxable and nontaxable rent hinges on the nature of the rental agreement and the specific circumstances surrounding the income. For instance, if you rent out a property for long-term residential use, the entire rent payment is typically taxable. However, if you rent out a vacation home for fewer than 15 days per year, the rent is entirely nontaxable, regardless of the amount received. This exception, often referred to as the "master’s rule," is a clear example of how usage and duration can alter tax obligations.

Understanding the nuances of taxable vs. nontaxable rent requires a closer look at the Internal Revenue Service (IRS) guidelines. Taxable rent includes payments for the use or occupancy of property, such as monthly rent from a tenant or lease payments. Additionally, advance rent payments—those received before the rental period begins—are taxable in the year they are received, not when the rental period starts. On the other hand, nontaxable rent can include security deposits, provided they are used to cover damages or unpaid rent and are not returned to the tenant. Another example is rent received in exchange for services, like a tenant agreeing to maintain the property, which may reduce the taxable amount by the fair market value of the services provided.

A practical approach to distinguishing between taxable and nontaxable rent involves examining the purpose and conditions of the rental agreement. For example, if a tenant pays a fee to break a lease early, this payment is generally considered taxable income. Conversely, reimbursements for expenses, such as utility payments made directly to the landlord, are not taxable if they are separately stated and the landlord is liable for the expenses. Landlords should maintain detailed records to substantiate these distinctions, as the IRS may scrutinize rental income reporting.

To navigate these complexities, landlords should adopt a proactive strategy. First, review all rental agreements to identify clauses that could affect taxability, such as service exchanges or expense reimbursements. Second, consult IRS Publication 527, *Residential Rental Property*, for detailed guidance on reporting rental income and expenses. Third, consider using accounting software or a tax professional to ensure accurate classification and reporting. By taking these steps, landlords can minimize the risk of errors and potential audits while maximizing compliance with tax laws.

In conclusion, the difference between taxable and nontaxable rent lies in the specifics of the rental arrangement and the intent behind the payments. While most rent is taxable, exceptions exist for certain scenarios, such as short-term vacation rentals or reimbursements for expenses. Landlords must carefully analyze each transaction, maintain thorough documentation, and stay informed about IRS regulations to ensure proper reporting. This diligence not only fulfills legal obligations but also optimizes financial outcomes in the complex landscape of rental taxation.

Renting to Section 8 Tenants in Challenging Neighborhoods: Pros and Cons

You may want to see also

Explore related products

![]()

Deductions for Rental Expenses

Rental income is generally reported as gross income, but the tax code allows landlords to offset this by deducting legitimate expenses associated with maintaining and operating the rental property. These deductions can significantly reduce taxable income, making them a critical aspect of rental property management. Understanding which expenses qualify and how to document them is essential for maximizing tax benefits while staying compliant with IRS regulations.

Qualifying Expenses: What Can You Deduct?

The IRS permits deductions for expenses that are ordinary, necessary, and directly related to renting the property. Common examples include mortgage interest, property taxes, insurance premiums, maintenance and repairs, utilities (if paid by the landlord), property management fees, and depreciation. For instance, if you spend $2,000 on repairing a leaky roof, this amount can be deducted in the year the expense is incurred. However, improvements that increase the property’s value, such as adding a new room, must be depreciated over time rather than deducted immediately.

Documentation: The Key to Successful Deductions

Accurate record-keeping is non-negotiable when claiming rental expense deductions. Keep detailed receipts, invoices, and contracts for all expenses. For example, if you hire a contractor for repairs, ensure you have a signed agreement and proof of payment. Additionally, maintain a mileage log if you use your vehicle for rental-related activities, as this can be deducted at the standard mileage rate (e.g., 65.5 cents per mile in 2023). Poor documentation can lead to disallowed deductions or audits, so treat record-keeping as a priority.

Special Considerations: Home Office and Personal Use

If you use part of your home for rental management activities, you may qualify for the home office deduction. To claim this, the space must be used regularly and exclusively for business. For example, a dedicated room used solely for handling rental paperwork could qualify. However, if you occasionally rent the property to family or friends at below-market rates, the IRS may limit your deductions. Understanding these nuances ensures you claim deductions appropriately without overstepping tax rules.

Strategic Planning: Timing and Optimization

Timing can amplify the impact of your deductions. For instance, scheduling major repairs or maintenance in a high-income year can help offset taxable income more effectively. Additionally, consider segregating expenses to maximize deductions. For example, if you own multiple properties, allocate shared expenses (like advertising or travel) proportionally based on rental income generated by each property. Consulting a tax professional can provide tailored strategies to optimize your deductions while minimizing risk.

By mastering the art of rental expense deductions, landlords can transform a potentially burdensome tax obligation into a manageable—and even advantageous—aspect of property ownership. The key lies in understanding the rules, maintaining meticulous records, and leveraging strategic planning to maximize benefits.

Rent Dragon Dance Costumes in Philly: Top Spots for Cultural Celebrations

You may want to see also

Explore related products

![]()

Gross vs. Net Rental Income

Understanding the difference between gross and net rental income is crucial for landlords and property investors. Gross rental income refers to the total amount of rent collected before any expenses are deducted. This includes all payments received from tenants, such as monthly rent, parking fees, or pet deposits. For instance, if a landlord collects $1,500 in monthly rent and an additional $100 for a pet fee, the gross rental income for that month is $1,600. This figure is straightforward and represents the full revenue generated by the property.

However, gross rental income does not provide a complete picture of profitability. To determine the actual earnings, landlords must calculate net rental income, which is derived by subtracting all associated expenses from the gross amount. Common deductions include property management fees, maintenance costs, property taxes, insurance, and mortgage payments. For example, if the total monthly expenses for a rental property amount to $800, the net rental income would be $800 ($1,600 gross income - $800 expenses). This net figure is a more accurate indicator of the property’s financial performance.

From a tax perspective, the distinction between gross and net rental income is significant. The IRS requires landlords to report all rental income, typically as gross income, on Schedule E of Form 1040. However, expenses directly related to the rental property can be deducted, effectively reducing the taxable income. For instance, if a landlord reports $18,000 in annual gross rental income but incurs $6,000 in deductible expenses, only $12,000 is subject to taxation. This highlights the importance of meticulous record-keeping to maximize tax benefits.

A practical tip for landlords is to maintain separate accounts for rental income and expenses. This simplifies the process of calculating net income and ensures accuracy during tax filings. Additionally, using property management software can automate expense tracking and generate reports, saving time and reducing errors. By focusing on both gross and net rental income, landlords can make informed decisions about property investments and optimize their financial outcomes.

In summary, while gross rental income reflects total revenue, net rental income reveals the true profitability after expenses. Both metrics are essential for financial planning and tax compliance. Landlords who understand and effectively manage these figures can enhance their investment returns and maintain a healthy cash flow. Whether for tax purposes or strategic planning, distinguishing between gross and net income is a fundamental aspect of successful property management.

How Much Does It Cost to Rent a Double Bass?

You may want to see also

Frequently asked questions

Yes, rent received from tenants is generally considered gross income and must be reported on your tax return, typically on Schedule E (Form 1040) for U.S. taxpayers.

No, claiming rent as gross income does not prevent you from deducting related expenses. You can deduct expenses like maintenance, repairs, property taxes, and mortgage interest to calculate your net rental income.

Yes, rent received from a roommate is typically considered gross income and should be reported, unless it’s a small amount for shared living expenses and not a formal rental arrangement.

Yes, you must still claim the rent as gross income, but you can only deduct expenses related to the rental portion of the property, prorated based on the percentage of rental use.

If you receive rent in the form of services (e.g., repairs or maintenance), the fair market value of those services is still considered gross income and must be reported on your tax return.