If you're a tenant, you don't need homeowners insurance as this is the responsibility of your landlord. However, you may want to consider renters insurance to protect your belongings and cover any incidents, such as water damage. On the other hand, if you're a landlord, homeowners insurance typically won't suffice, and you'll need a landlord insurance policy to protect your property and cover any liabilities.

| Characteristics | Values |

|---|---|

| Who needs homeowners insurance? | Landlords or homeowners who rent out their properties. |

| Who doesn't need homeowners insurance? | Tenants or renters. |

| What does homeowners insurance cover? | Damage to the property, liability concerns, and some personal property, such as appliances and lawn care equipment. |

| What doesn't homeowners insurance cover? | Tenants' or renters' personal belongings. |

| Who needs renters insurance? | Tenants or renters. |

| Who doesn't need renters insurance? | Landlords or homeowners. |

| What does renters insurance cover? | Tenants' or renters' personal belongings and certain incidents like water backup damage and natural disasters. |

| What doesn't renters insurance cover? | Damages to the rented property. |

Explore related products

$9.99 $19.99

What You'll Learn

![]()

Landlord insurance

If you are a tenant, you do not need homeowners insurance. However, it is recommended that you get renters insurance to protect your belongings, as your landlord's insurance will not cover your personal property.

Now, if you are a landlord, you may be wondering if you need landlord insurance. The answer depends on a few factors, such as how often you rent out your property and how long your tenants typically stay. If you are renting out your property long-term (usually considered six months or longer), then it is highly recommended that you have landlord insurance. This type of insurance protects landlords from risks associated with their rental properties, including damage to the building or its contents. It can also cover loss of rent and tenant default, as well as liability claims.

The cost of landlord insurance will depend on various factors, including the property, tenants, type of insurance chosen, and cover levels required. To get an accurate quote, you can contact an insurance provider and provide them with the necessary details. It is worth noting that landlord insurance typically costs about 25% more than standard home insurance, according to the Insurance Information Institute.

Where Can You Watch Inside Out 2?

You may want to see also

Explore related products

![]()

Renting out a primary residence

If you're renting out your primary residence, it's important to understand the differences between homeowners insurance and landlord insurance to ensure you have the right coverage. Here are some key points to consider:

Homeowners Insurance:

- Homeowners insurance is designed for owner-occupied primary residences. It typically covers the structure of the home and the owner's personal belongings.

- If you plan to rent out your entire home, your homeowners insurance may not provide adequate coverage. Standard homeowners insurance policies usually do not cover damage or liability claims arising from rental activities.

- However, if you're only renting out a room in your home while still occupying it, your homeowners insurance may extend some coverage. Be sure to verify this with your insurer, as some policies may have limitations on damage caused by tenants or their guests.

Landlord Insurance:

- Landlord insurance is specifically designed for rental properties and covers the unique risks associated with renting out a property. It typically includes coverage for premises damage, liability concerns, and loss of rental income.

- If you're renting out your entire primary residence, landlord insurance is generally recommended. It can protect you from financial losses due to property damage, legal fees, and lost income if the property becomes uninhabitable.

- The cost of landlord insurance is typically higher than homeowners insurance (around 25% more on average) due to the increased risks associated with rental properties.

Additional Considerations:

- It's important to review your insurance policy's terms and conditions to understand any exclusions or limitations. Certain types of rentals, such as short-term rentals or vacation homes, may require additional coverage or endorsements.

- Inform your insurance company about your plans to rent out your property. They can advise you on the specific coverage options and adjustments needed to ensure adequate protection.

- Consider requiring your tenants to obtain renters insurance to cover their personal belongings and liability. This can help protect you from disputes arising from damage to their belongings.

Roommate Rent: Income or Not?

You may want to see also

Explore related products

![]()

Personal belongings

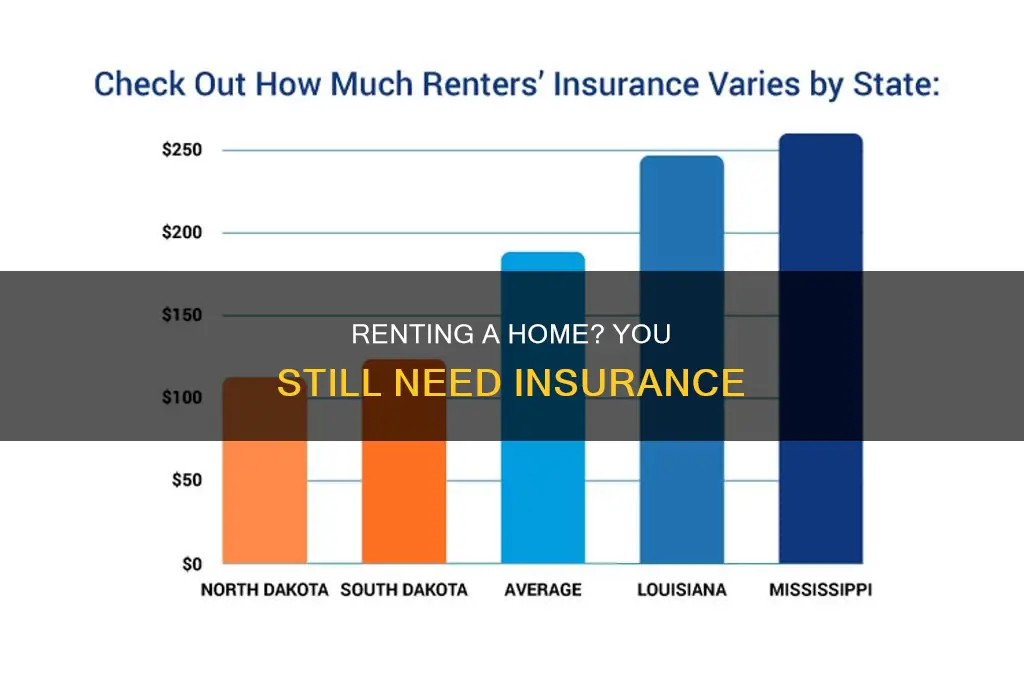

If you're renting a home, you don't need homeowners insurance as a tenant. Instead, you should consider getting renters insurance to protect your personal belongings. While it's not required by law, it's the only way to ensure your possessions are covered in the event of damage, loss, or theft. Your landlord's insurance policy will not cover your personal items.

Renters insurance provides coverage for your personal belongings, including furniture, electronics, clothing, and other valuables. It protects against incidents such as fire, water damage, theft, and certain natural disasters. By having renters insurance, you can have peace of mind knowing that you won't have to pay out of pocket to replace your belongings if something unexpected happens.

Additionally, renters insurance can provide liability protection. This means that if someone is injured on the rental property or if you accidentally cause damage to someone else's property, your insurance can help cover the associated costs, including legal fees and medical expenses. This aspect of renters insurance protects you from potential lawsuits and financial strain.

It's important to note that renters insurance does not cover the structure of the rental property. As a tenant, you are not responsible for insuring the building itself. That falls under the landlord's insurance policy, which covers premises damage and liability concerns related to the property. However, as a tenant, you should ensure that your personal belongings are adequately protected through renters insurance.

When obtaining renters insurance, it's advisable to create an inventory of your personal belongings, including their estimated value. This will help you determine the amount of coverage you need and facilitate the claims process if you ever need to file one. Remember to update your inventory periodically, especially after acquiring new valuable items.

Renting a Scooter: A Guide for Disney World Visitors

You may want to see also

Explore related products

![]()

Liability concerns

If you are a renter, you are not responsible for insuring the building as the landlord or homeowner is responsible for insuring the property. However, it is always a good idea to get renters' insurance to protect your belongings as the landlord's insurance will not cover your personal property. Renters' insurance can also protect you from liability concerns, for example, if you accidentally cause damage to the property.

If you are a homeowner renting out your property, you will need to purchase a landlord insurance policy. Standard homeowners insurance policies do not cover your home if it is used as a rental property because it is now considered a business asset. Landlord insurance policies carry higher liability insurance coverage limits than a homeowners policy, protecting landlords from lawsuits and legal fees. For example, if a tenant or one of their guests gets hurt on the property, landlord insurance would cover legal fees and medical expenses. Landlord insurance also covers loss of rental income in the event that the property cannot be rented out while it is being repaired or rebuilt due to damage.

If you are renting out your primary residence for short periods on a regular basis, this would constitute a business. In this case, you would need to purchase a business policy, such as a hotel or bed and breakfast policy. If you are renting out your home for longer periods, such as six months or a year, you will likely need a landlord or rental dwelling policy.

It is important to note that landlord insurance does not cover the renter's personal belongings. Tenants should purchase their own renters' insurance policy to protect their belongings in case of damage or loss. This will also protect them from having to pay out of pocket for incidents such as water backup damage and certain natural disasters.

Rent Payments: What the IRS Needs to Know

You may want to see also

Explore related products

![]()

Vacant home coverage

If you are a renter, you do not need homeowners insurance. However, it is recommended that you get renters insurance to protect your belongings, as your landlord's insurance will not cover your personal property.

Now, if you are a homeowner and plan to leave your home unoccupied for an extended period, you may need vacant home insurance. This is because regular homeowners insurance policies often include a vacancy clause that limits or excludes coverage if a home is left vacant for more than 30 to 60 days.

Vacant homes are more vulnerable to risks such as squatters, vandalism, theft, water damage, fire, and plumbing leaks. A vacant home insurance policy can protect you from these perils, which are typically covered by a standard homeowners policy. However, some risks, such as theft and vandalism, may be excluded from vacant home insurance policies, and liability coverage may not be included.

The cost of vacant home insurance is typically higher than a standard policy, ranging from 50% to 60% more, or even two to three times the standard rate. This is because vacant homes are at a higher risk of damage or loss, and the lack of occupancy makes them more attractive targets for criminals.

You can purchase vacant home insurance as a separate policy or as an endorsement to your existing homeowners insurance. Some insurance companies, such as Farmers and State Farm, offer flexible vacant home insurance policies that can be cancelled and reimbursed if needed. It is important to carefully review the terms, conditions, and limitations of any vacant home insurance policy before purchasing it.

Reporting Your Son's Rent: What You Need to Know

You may want to see also

Frequently asked questions

No, homeowners insurance is designed specifically for occupied primary residences. If you're renting out your property, you'll need to get landlord insurance.

Landlord insurance covers premises damage, liability concerns, and some personal property, such as appliances and lawn care equipment. It also provides coverage for loss of rental income if the property is uninhabitable due to repairs or damage.

If you're renting out your primary residence for short periods, this would constitute a business, and you would need a business policy, such as a hotel or bed and breakfast policy. If you're renting out a vacation home or investment property, you'll need landlord insurance or a rental dwelling policy.

As a tenant, you are not required by law to have renters insurance. However, it is recommended to protect your belongings and cover any incidents such as water damage or natural disasters.