The question of whether rents are normally distributed is a fascinating and complex one, as it delves into the underlying patterns and variability of rental prices across different markets. A normal distribution, often referred to as a bell curve, implies that most rents cluster around a central value, with fewer outliers at the extremes. However, rental markets are influenced by a multitude of factors, including location, demand, supply, economic conditions, and local regulations, which can skew the distribution. For instance, in high-demand urban areas, rents may be right-skewed, with a higher concentration of expensive properties, while in more rural or less competitive markets, the distribution might be closer to normal. Analyzing whether rents follow a normal distribution can provide valuable insights into market dynamics, affordability, and policy implications, making it a critical area of study for economists, urban planners, and policymakers alike.

| Characteristics | Values |

|---|---|

| Distribution Type | Not perfectly normal, but often approximated as normal for analytical purposes |

| Skewness | Typically right-skewed (higher rents pull the tail to the right) |

| Kurtosis | Leptokurtic (fatter tails compared to a normal distribution) |

| Outliers | Common, especially in high-demand or luxury markets |

| Factors Influencing Distribution | Location, property type, market demand, economic conditions |

| Common Use of Normality Assumption | Simplifies statistical analysis (e.g., regression, hypothesis testing) |

| Empirical Evidence | Real-world rent data often deviates from perfect normality |

| Alternative Distributions | Log-normal, Weibull, or Gamma distributions better fit rent data in many cases |

| Practical Implications | Normality assumption may lead to biased estimates if data is highly skewed |

| Latest Data Sources | Zillow, Census Bureau, Realtor.com, local housing reports (as of 2023) |

Explore related products

$175.42 $51.99

What You'll Learn

![]()

Factors Influencing Rent Distribution

Rent distribution is not a one-size-fits-all scenario. While the concept of a normal distribution might seem appealing for its simplicity, the reality is far more complex. A normal distribution implies a symmetrical bell curve, with most rents clustering around the mean and fewer outliers at the extremes. However, in practice, rent distribution is influenced by a myriad of factors that skew this idealized model. Understanding these factors is crucial for tenants, landlords, and policymakers alike.

Geographic Location: The Primary Determinant

Location is the single most influential factor in rent distribution. Urban centers, particularly those with high demand for housing, often exhibit a right-skewed distribution, where higher rents are more common than lower ones. For instance, in cities like San Francisco or New York, the median rent can be significantly higher than the national average, with a long tail of extremely expensive properties. Conversely, rural areas or smaller towns may show a left-skewed distribution, with lower rents dominating and fewer high-end options. This geographic disparity is further exacerbated by local economic conditions, job opportunities, and population density.

Economic and Demographic Factors: Shaping the Curve

Economic indicators such as income levels, employment rates, and cost of living play a pivotal role in rent distribution. In regions with a thriving job market and higher average incomes, rents tend to be elevated, creating a distribution with a higher mean. Conversely, areas with lower income levels often exhibit a compressed rent distribution, with most properties falling within a narrower price range. Demographic factors, such as age and household size, also contribute. For example, cities with a large student population may have a bimodal distribution, with affordable shared housing and high-end luxury apartments catering to different segments.

Supply and Demand Dynamics: The Invisible Hand

The interplay between housing supply and demand is a critical factor in shaping rent distribution. In markets where demand outstrips supply, rents are driven upward, leading to a distribution with fewer low-cost options and a higher concentration of expensive properties. This is often seen in gentrifying neighborhoods or areas experiencing rapid population growth. Conversely, oversupply can lead to a left-skewed distribution, with landlords competing by offering lower rents. Government policies, such as rent control or zoning laws, can also distort the natural distribution by artificially capping rents or limiting new construction.

Property Characteristics: Adding Layers of Complexity

The physical attributes of rental properties introduce additional variability into rent distribution. Factors like property size, age, condition, and amenities significantly influence rental prices. For instance, newly constructed luxury apartments with modern amenities will occupy the higher end of the distribution, while older, smaller units without updates will cluster at the lower end. This creates a multi-modal distribution in some markets, where distinct clusters of rents correspond to different property types. Additionally, the presence of unique features, such as a view, parking, or proximity to public transportation, can further skew the distribution by increasing demand for specific properties.

Seasonality and External Shocks: Temporary Distortions

Rent distribution is not static; it can fluctuate due to seasonal trends or external shocks. For example, rents in college towns may spike during the academic year and drop in the summer, creating a cyclical pattern. Similarly, economic downturns or natural disasters can temporarily shift the distribution by reducing demand or damaging supply. These short-term fluctuations highlight the dynamic nature of rent distribution and the need for flexible analysis. While these factors may not permanently alter the distribution, they introduce noise that complicates the assumption of normality.

In conclusion, while the idea of a normal distribution of rents is conceptually appealing, the reality is shaped by a complex interplay of geographic, economic, demographic, and property-specific factors. Recognizing these influences allows for a more nuanced understanding of rent distribution, enabling better decision-making for all stakeholders involved.

Understanding Rent and Insurance: Categorizing These Essential Business Expenses

You may want to see also

Explore related products

![]()

Geographic Variations in Rent Patterns

Rent distribution is not a one-size-fits-all concept. A quick glance at rental markets across different cities reveals a striking disparity in rent patterns, challenging the notion of a universal normal distribution. For instance, in tech hubs like San Francisco and New York City, rents often follow a right-skewed distribution, with a long tail of extremely high prices. In contrast, smaller cities or rural areas might exhibit a more symmetrical distribution, with rents clustering around a moderate mean. This geographic variation is a critical factor in understanding the complexities of rent patterns.

To illustrate, consider the following scenario: in a densely populated metropolitan area, the median rent for a one-bedroom apartment can be significantly higher than in a suburban or rural setting. In New York City, for example, the median rent is approximately $3,500 per month, whereas in a smaller city like Austin, Texas, it hovers around $1,500. This disparity is not merely a result of differences in cost of living but also reflects variations in local economies, population density, and housing supply. A comparative analysis of these markets reveals that geographic factors play a pivotal role in shaping rent distributions, often overriding other variables like property type or size.

When examining rent patterns across regions, it’s essential to account for local market dynamics. In high-demand areas, rents may not only be higher but also more volatile, with prices fluctuating rapidly in response to economic shifts or policy changes. For instance, the introduction of rent control measures in certain cities can lead to a bimodal distribution, where controlled units cluster at lower prices, and uncontrolled units skew higher. Conversely, in areas with stable economies and ample housing supply, rents tend to follow a more normal distribution, providing renters with greater predictability. To navigate these variations, renters should research local market trends, consider factors like employment opportunities and transportation access, and be prepared for regional nuances in rental pricing.

A persuasive argument can be made for the importance of geographic context in rent distribution. Policymakers and urban planners must recognize that a single regulatory approach cannot address the diverse needs of all rental markets. For example, while rent stabilization might be effective in curbing skyrocketing prices in cities like Los Angeles, it could have unintended consequences in smaller markets with already affordable rents. Instead, tailored solutions—such as incentivizing affordable housing development in high-cost areas or promoting rural revitalization in low-demand regions—are necessary. By acknowledging geographic variations, stakeholders can design more equitable and effective housing policies.

In practical terms, understanding geographic rent patterns can empower individuals to make informed decisions. For renters, this might mean prioritizing location based on budget constraints or considering remote work opportunities to access more affordable markets. For investors, it could involve targeting regions with stable, normally distributed rents for lower-risk returns, or focusing on high-growth areas with skewed distributions for potential high yields. Ultimately, recognizing the geographic nuances in rent patterns is not just an academic exercise—it’s a critical tool for navigating the complexities of the housing market.

Renting in Missouri? File Your Rent Certificate

You may want to see also

Explore related products

![]()

Impact of Supply and Demand

Rents, like any price in a market economy, are fundamentally shaped by the interplay of supply and demand. When demand for rental properties exceeds the available supply, rents tend to rise as landlords capitalize on the scarcity. Conversely, when supply outstrips demand, rents often fall as landlords compete for tenants. This dynamic is not unique to the rental market but is particularly evident in urban areas where population density and economic activity are high. For instance, cities like San Francisco and New York have seen rents skyrocket due to limited housing stock and high demand from both residents and businesses. Understanding this relationship is crucial for predicting rent trends and making informed decisions, whether you’re a tenant, landlord, or policymaker.

To illustrate, consider the impact of a sudden influx of remote workers into a previously affordable city. As more people move in, the demand for housing increases, but if the supply of rental units remains static, rents will climb. This scenario played out in cities like Austin, Texas, during the COVID-19 pandemic, where remote workers flocked to the area, driving up rents by double-digit percentages in a matter of months. Conversely, in cities with declining populations, such as Detroit, rents have remained relatively stable or even decreased as demand waned. These examples highlight how shifts in supply and demand can dramatically alter rent distributions, often deviating from a normal distribution due to localized factors.

Analyzing rent distribution through the lens of supply and demand also reveals why rents are rarely normally distributed. A normal distribution assumes symmetry and predictability, but rental markets are influenced by too many variables—zoning laws, construction costs, economic growth, and tenant preferences—to conform to such a model. For example, luxury apartments in a city center may command significantly higher rents than suburban units, creating a skewed distribution. Additionally, external shocks like natural disasters or economic recessions can abruptly shift supply or demand, further distorting any semblance of normality. Policymakers often intervene with rent control or housing subsidies to stabilize markets, but these measures can also introduce new distortions, complicating the distribution further.

Practical steps can be taken to navigate this complex landscape. Tenants should monitor local housing developments and economic indicators to anticipate rent changes. For instance, if a city announces plans for a major tech hub, demand—and rents—are likely to rise in surrounding areas. Landlords, on the other hand, can benefit from diversifying their property portfolios to mitigate risks associated with supply and demand fluctuations. Investing in both urban and suburban properties, for example, can provide a buffer against localized market shifts. Policymakers must balance short-term relief measures, like rent caps, with long-term solutions, such as increasing housing supply through streamlined permitting processes or incentivizing affordable housing construction.

In conclusion, the impact of supply and demand on rents is profound but far from predictable. While these forces drive rent levels, their interaction with local conditions and external factors ensures that rent distributions rarely follow a normal curve. By understanding these dynamics and taking proactive steps, stakeholders can better navigate the rental market’s inherent volatility. Whether you’re signing a lease, setting rent prices, or crafting housing policy, recognizing the role of supply and demand is essential for making informed decisions in this ever-evolving landscape.

Understanding NY Rent Grace Period: What Tenants Need to Know

You may want to see also

Explore related products

![]()

Role of Economic Conditions

Economic conditions act as a gravitational force shaping the distribution of rents, pulling them away from a neat, normal curve. Consider the cyclical nature of economies: during booms, employment rises, incomes swell, and demand for housing surges. This heightened demand, especially in supply-constrained markets, skews rent distributions rightward, creating a long tail of higher rents as landlords capitalize on the favorable conditions. Conversely, in downturns, job losses and reduced incomes dampen demand, leading to a left-skewed distribution as rents cluster at lower levels, with fewer outliers on the high end.

To illustrate, examine cities like San Francisco during the tech boom of the 2010s. Skyrocketing demand from high-earning tech workers pushed median rents to unprecedented levels, while a limited housing supply exacerbated the rightward skew. In contrast, Rust Belt cities experiencing deindustrialization often exhibit left-skewed rent distributions, with a surplus of affordable housing and a shrinking population unable to sustain higher rents. These examples underscore how economic cycles directly influence the shape of rent distributions, rendering a normal distribution unlikely.

A persuasive argument emerges when considering the role of income inequality, a byproduct of economic conditions. In economies with widening income gaps, rent distributions become increasingly bimodal. High-income earners drive up rents in desirable areas, creating a peak at the upper end, while low-income households cluster in affordable housing, forming a second peak at the lower end. This duality fractures any semblance of normality, as rents polarize rather than conform to a symmetrical bell curve.

Practical implications abound for policymakers and investors. Understanding the economic drivers of rent distributions enables more targeted interventions. For instance, during booms, rent control measures may mitigate the rightward skew, while economic downturns call for stimulus programs to prevent a collapse in rental markets. Investors, too, can leverage this knowledge: in booming economies, focus on high-demand urban areas, but in downturns, shift toward recession-resilient markets with stable, if lower, rents.

In conclusion, economic conditions are not mere background noise in the discussion of rent distributions; they are the conductor orchestrating the symphony. By dissecting the interplay between economic cycles, income inequality, and housing demand, we move beyond simplistic assumptions of normality. Instead, we gain a nuanced understanding that informs smarter policies and investments, ensuring housing markets remain responsive to the ebb and flow of economic tides.

U-Haul Truck Options: 5th Wheel Hitch Rentals

You may want to see also

Explore related products

![]()

Statistical Analysis of Rent Data

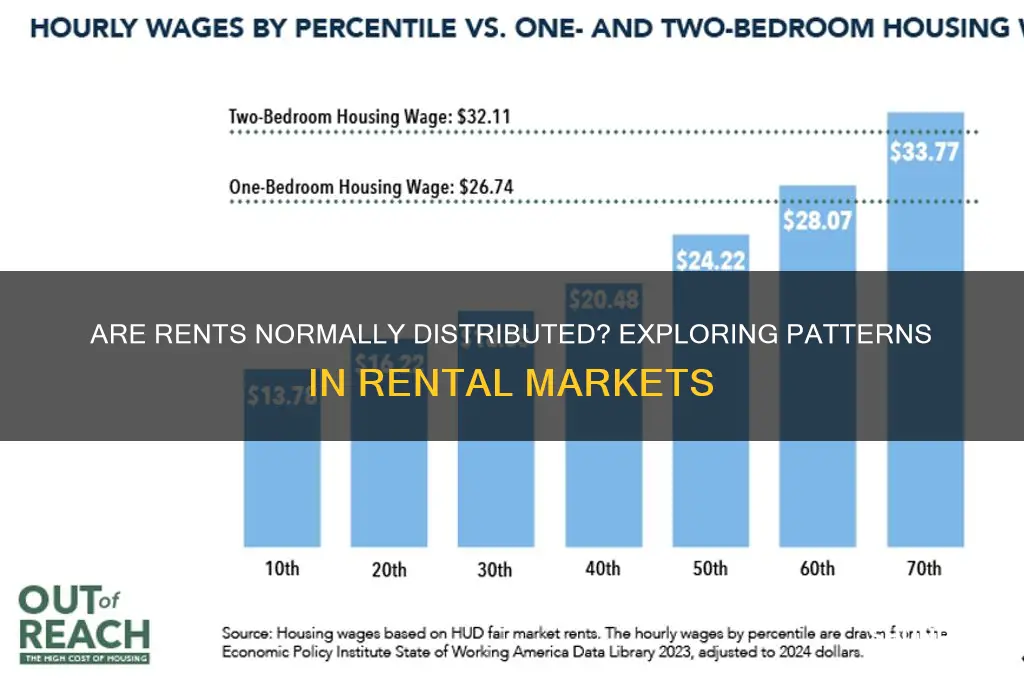

Rent distribution is often assumed to follow a normal distribution, but this assumption warrants scrutiny. A normal distribution implies that most rents cluster around a central value, with fewer outliers at the extremes. However, real-world rent data frequently deviates from this idealized pattern. For instance, in high-demand urban areas like San Francisco or New York, rent distributions are often right-skewed, with a long tail of extremely high rents. Conversely, in rural or less competitive markets, rents may cluster more tightly around a lower median, resembling a platykurtic distribution. Understanding these variations is crucial for accurate statistical modeling and policy-making.

To assess whether rent data is normally distributed, start by plotting a histogram or density curve of the dataset. Look for symmetry and the presence of outliers. Next, perform a Shapiro-Wilk test, a statistical tool that quantifies the likelihood of normality. For example, a p-value greater than 0.05 suggests the data could be normally distributed, but this should be interpreted alongside visual inspection. Caution: small sample sizes or extreme outliers can distort results, so consider data cleaning or transformation techniques like log normalization to improve normality.

When analyzing rent data, it’s instructive to compare distributions across different geographic or demographic segments. For instance, rents in luxury apartments might exhibit a bimodal distribution, reflecting a clear divide between high-end and ultra-luxury units. In contrast, affordable housing rents may follow a more uniform distribution due to rent control policies. Such comparisons highlight the importance of context in statistical analysis. Practical tip: use box plots or violin plots to visualize these differences, as they provide insights into variability and potential skewness.

Finally, the assumption of normality in rent data has significant implications for predictive modeling. If rents are not normally distributed, linear regression models may yield biased estimates, particularly for extreme values. Instead, consider robust alternatives like quantile regression or machine learning algorithms that handle non-normal data more effectively. For policymakers, recognizing non-normal distributions can inform targeted interventions, such as rent stabilization measures in skewed markets. By embracing the complexity of rent data, analysts can produce more accurate and actionable insights.

Unlocking Timeshare Rentals: A Non-Member's Guide to Vacation Success

You may want to see also

Frequently asked questions

Rents are not typically normally distributed. They often follow a right-skewed distribution, meaning there are more lower-priced rentals and fewer higher-priced ones, with a long tail of expensive outliers.

Factors like location, property size, market demand, and local regulations can cause rents to cluster at certain price points, leading to a skewed distribution rather than a normal bell curve.

In rare, highly controlled or homogeneous markets, rents might approximate a normal distribution. However, this is uncommon due to the diverse factors influencing rental prices in most real-world scenarios.