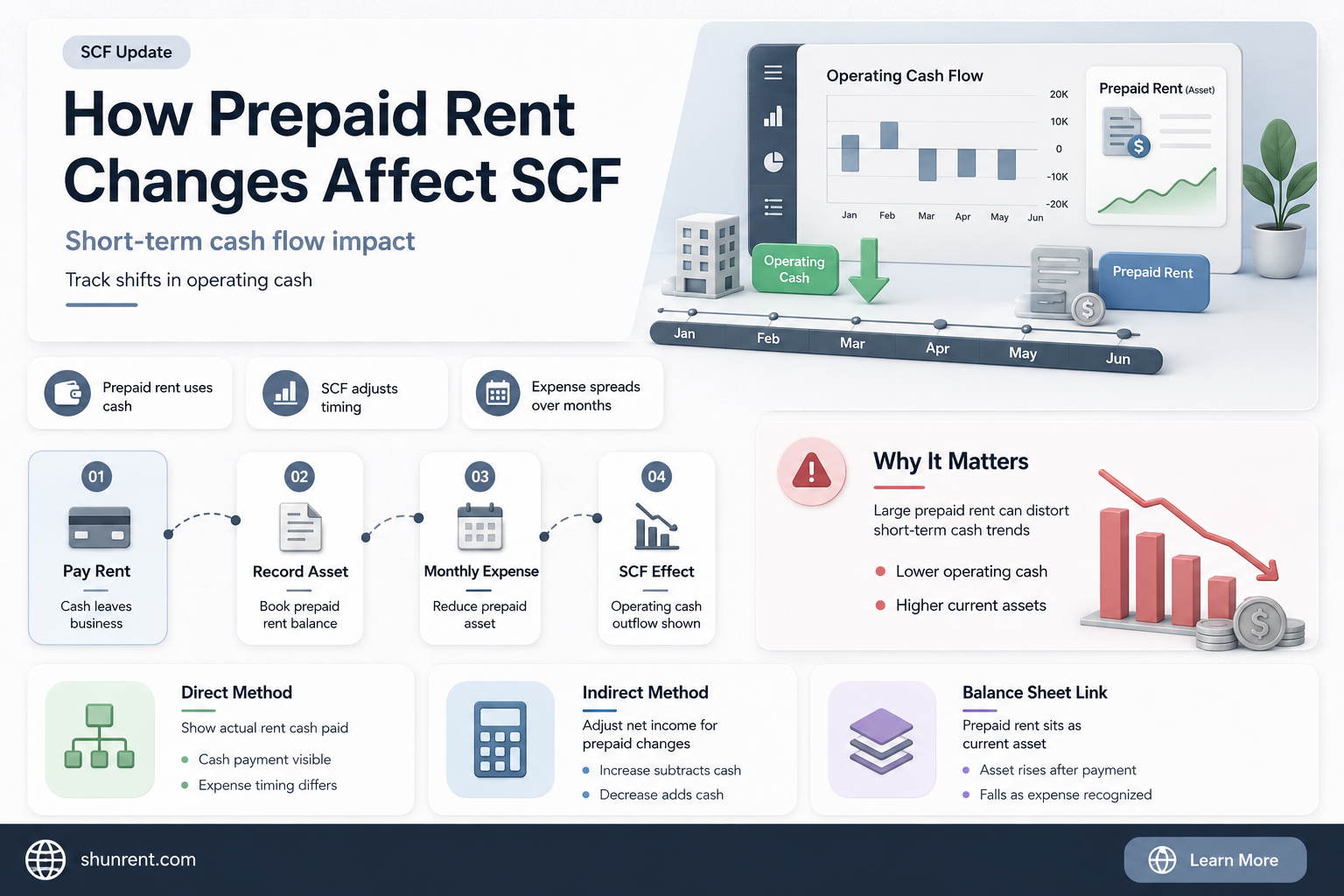

Prepaid rent refers to rent payments made before the rental period begins. For example, if a tenant pays January's rent in December, that payment is considered prepaid rent. Prepaid rent is recorded as a current asset, not income, when it is first received. It only becomes rental income once the rent period arrives, and the tenant has occupied the unit. Prepaid rent can affect cash flow, as it results in a cash outflow for expenses that have not yet been recognised in the income statement. This can lead to a decrease in net cash flow, as more cash is spent upfront for future expenses. On the other hand, a decrease in prepaid expenses can increase cash flow, providing more cash for immediate expenses and investments.

| Characteristics | Values |

|---|---|

| Definition | Prepaid rent refers to rent payments received before the rental period begins. |

| Accounting Treatment | Prepaid rent is recorded as a current asset, not income, when it's first received. It becomes rental income once the rent period arrives and the tenant has "used" the property. |

| Impact on Cash Flow | An increase in prepaid expenses results in a cash outflow, while a decrease results in a cash inflow. |

| Impact on Income Statement | Prepaid rent may make monthly income look uneven as it is reflected on the cash flow statement when cash is received, not when it's earned. |

| Tax Treatment | The IRS typically treats prepaid rent as taxable income in the year it's received, especially for cash-basis accounting. |

| Journal Entry | The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash. |

| Adjusting Journal Entry | The adjusting journal entry for prepaid rent affects both the income statement and balance sheet. It results in an expense and a decrease in assets. |

| Lease Accounting Standards | Recent updates to lease accounting standards, including ASC 842, IFRS 16, GASB 87, SFFAS 54, and FRS 102, have changed the accounting treatment for leasing arrangements. |

Explore related products

What You'll Learn

![]()

Prepaid rent is logged as a current asset, not income

Prepaid rent is logged as a current asset and not as income. This is because prepaid rent is considered a future economic benefit to the company. It is a payment for a service that has not yet been provided. In other words, it is money received for a service (rental use) that is yet to be delivered. It is only considered rental income once the rent period arrives and the tenant has "used" the property.

For example, if a tenant pays rent for October and November in September, only a part of that should count as income in September. The rest needs to be recorded in the following months as it becomes earned. This process ensures that the reported income is aligned with each rental period, even if the payment came early.

From an accounting perspective, prepaid rent is a debit to prepaid rent and a credit to cash. These are both asset accounts and do not increase or decrease a company's balance sheet. However, the adjusting journal entry for a prepaid expense does affect both a company's income statement and balance sheet. For example, an adjusting entry on January 31 would result in an expense of $10,000 (rent expense) and a decrease in assets of $10,000 (prepaid rent). The expense would show up on the income statement, while the decrease in prepaid rent would reduce the assets on the balance sheet.

It is important to note that the treatment of prepaid rent in accounting has evolved with updates to lease accounting standards, such as ASC 842, which have introduced changes in the terminology and accounting treatments related to rent expense. Under ASC 842, organizations record a lease liability and a right-of-use (ROU) asset. The amortization of the lease liability and the depreciation of the ROU asset make up the straight-line lease expense.

Randpark Cottage Rentals: Your Dream Home Away from Home

You may want to see also

Explore related products

![]()

An increase in prepaid expenses results in a cash outflow

An increase in prepaid expenses, such as rent, results in a cash outflow. This is because the company has paid for expenses that have not yet been recognised in the income statement. For example, if a company prepays rent for 12 months, the prepaid rent balance will increase for the 12 months of rent prepaid. However, on the expense side, the 12 months of expenses will not be recognised until the end of the year. This means that the company has made a cash outflow, but the expense has not yet been reflected in the company's financial statements.

Prepaid expenses directly influence cash flow. When a company makes a prepaid expense, it is essentially trading a lump sum of cash now for goods or services that will be used later. While this initially reduces the company's available cash, it prevents larger cash outflows in the future. For example, if a company prepays for a year of insurance, it will impact the company's current cash flow, but it also means that the company will not have monthly insurance payments for the next 12 months.

The impact of prepaid expenses on cash flow can be seen in the cash flow statement. The increase in prepaid expenses will result in a negative impact on the cash flow from operating activities section of the cash flow statement. This outflow represents an investment in future benefits. By making a larger one-time payment, the company avoids smaller, recurring payments in the future. This can be helpful for budgeting and forecasting, as it allows the company to predict future expenses more accurately.

It is important to note that the accounting treatment for prepaid expenses may vary depending on the specific circumstances and accounting standards being used. For example, under the old lease accounting rules, cash payments for operating leases were recorded as rent expense in the period incurred, while under the new ASC 842 standard, organisations record a lease liability equal to the present value of the remaining lease payments.

Rent Qualification: Is Three Times Rent Still Necessary?

You may want to see also

Explore related products

![]()

A decrease in prepaid expenses results in a cash inflow

Prepaid expenses are considered assets because they provide future economic benefits to a company. For example, a company might prepay rent for 12 months, increasing the prepaid rent balance for that period. However, the expense side will not be recognised until the end of the year. So, while the prepaid rent balance increases, indicating a cash outflow, the expense side remains unchanged.

When the prepaid expense balance decreases, this indicates that less cash has been spent on future expenses. In the case of prepaid rent, this could be because the 12-month lease has ended, and the company is no longer paying rent upfront. As a result, the prepaid rent balance decreases, and the expense side is recognised, indicating a cash inflow.

The adjusting journal entry for a prepaid expense affects both a company's income statement and balance sheet. For example, if a company has a prepaid rent expense of $10,000, the adjusting entry would result in an expense of $10,000 (rent expense) and a decrease in assets of $10,000 (prepaid rent). The expense would be recorded on the income statement, while the decrease in prepaid rent would reduce the assets on the balance sheet.

Overall, a decrease in prepaid expenses, such as prepaid rent, results in a cash inflow by increasing net cash flow and reducing the amount of cash spent on future expenses.

Hotel Pool Birthday Parties: Renting Options and Availability

You may want to see also

Explore related products

$2.99 $19.95

![]()

Prepaid rent can make monthly income look uneven

Prepaid rent can indeed make monthly income look uneven. This is because, when a tenant pays rent in advance, the landlord receives a large sum all at once. However, only a portion of that should count as income for that month. The rest needs to be recorded in the following months as it is earned. For example, if a tenant pays October and November's rent in September, the landlord will receive both months' rent in September. However, only the rent for September should be counted as income for that month. The rent for October and November will be recorded as income in those respective months.

This process ensures that the reported income aligns with each rental period, even if the payment was received early. On a cash flow statement, prepaid rent is reflected when the cash is received, not when it is earned. Therefore, the cash flow increases when the payment is received, but the income statement remains unchanged until the rental period starts. This timing difference is crucial to understand, especially when using reports to make monthly financial decisions. As a result, there may appear to be an income "dip" during months when no new rent is collected, even though the money came in during a previous month.

From the perspective of the tenant, prepaid rent can impact their monthly income by reducing their cash flow for the month in which they pay early. This is because they are paying for more than one month's rent in a single month, which can leave them with less cash to cover other expenses or investments.

Additionally, the treatment of prepaid rent can vary depending on the accounting method used. For example, the IRS typically treats prepaid rent as taxable income in the year it is received, especially if using cash-basis accounting. In this case, if a tenant pays January's rent in December, it counts as income for the current year, even though it is for the following year. However, with accrual-basis accounting, taxes are paid when the income is earned, so the income would be reported in January instead.

Renting a Truck? Understand Insurance Requirements First

You may want to see also

Explore related products

![]()

The IRS treats prepaid rent as taxable income in the year it's received

The IRS treats prepaid rent as taxable income in the year it is received. This is the case for both cash basis taxpayers and accrual-based taxpayers. Cash basis taxpayers are those who report income in the year they receive it, regardless of when it was earned. Prepaid rent, or advance rental payments, occur when a tenant pays rent before the applicable period. This is considered a fixed amount at receipt and provides an immediate financial benefit to the landlord or property owner.

The IRS states that prepaid rent is generally included in income in the year it is received, regardless of the accounting method or the period it covers. This means that if a tenant pays $5,000 for the first year's rent and $5,000 as rent for the last year of a 10-year lease, the landlord must include $10,000 in their income in the first year. This is also the case if a security deposit is to be used as the final payment of rent; it is considered advance rent and should be included as income when it is received, rather than when it is applied to the last month's rent.

The IRS also specifies that if a tenant pays any of the landlord's expenses, these payments are considered rental income and must be included in the landlord's income. Examples of this include a tenant paying the water and sewage bill for a rental property, or a tenant offering to paint the rental property instead of paying two months' rent. In the latter case, the landlord must include in their rental income the amount the tenant would have paid for two months' rent, and they can then include the same amount as a rental expense for painting their property.

It is important to note that security deposits are not included in rental income if they are to be returned to the tenant at the end of the lease. However, if the landlord keeps part or all of the security deposit because the tenant breaks the lease or damages the property, the amount kept must be included in income in that year. Additionally, amounts paid to cancel a lease are also considered rental income and should be reported in the year they are received.

Rent Distribution: Normal or Not?

You may want to see also

Frequently asked questions

Prepaid rent refers to rent payments received before the rental period begins. For example, if a tenant pays January's rent in December, that payment is considered prepaid rent. It is recorded as a current asset, not income, when it's first received. It only becomes rental income once the rent period arrives and the tenant has "used" the property.

Prepaid rent can make monthly income look uneven. For example, if a tenant pays rent for October and November in September, the landlord will receive a large sum all at once. However, only a part of that should count as income in September. The rest needs to be recorded in the following months as it becomes earned. Prepaid rent is reflected on the cash flow statement when cash is received, not when it's earned. This means that cash flow increases when the payment is received, but the income statement stays flat until the rental period starts. An increase in prepaid expenses results in a cash outflow, while a decrease results in a cash inflow.

The IRS typically treats prepaid rent as taxable income in the year it is received, especially if the landlord uses cash-basis accounting. This means that if a tenant pays January's rent in December, it counts as income for the current year, even though it is for the following year. Taxes are paid when the money is received, not when it is earned.