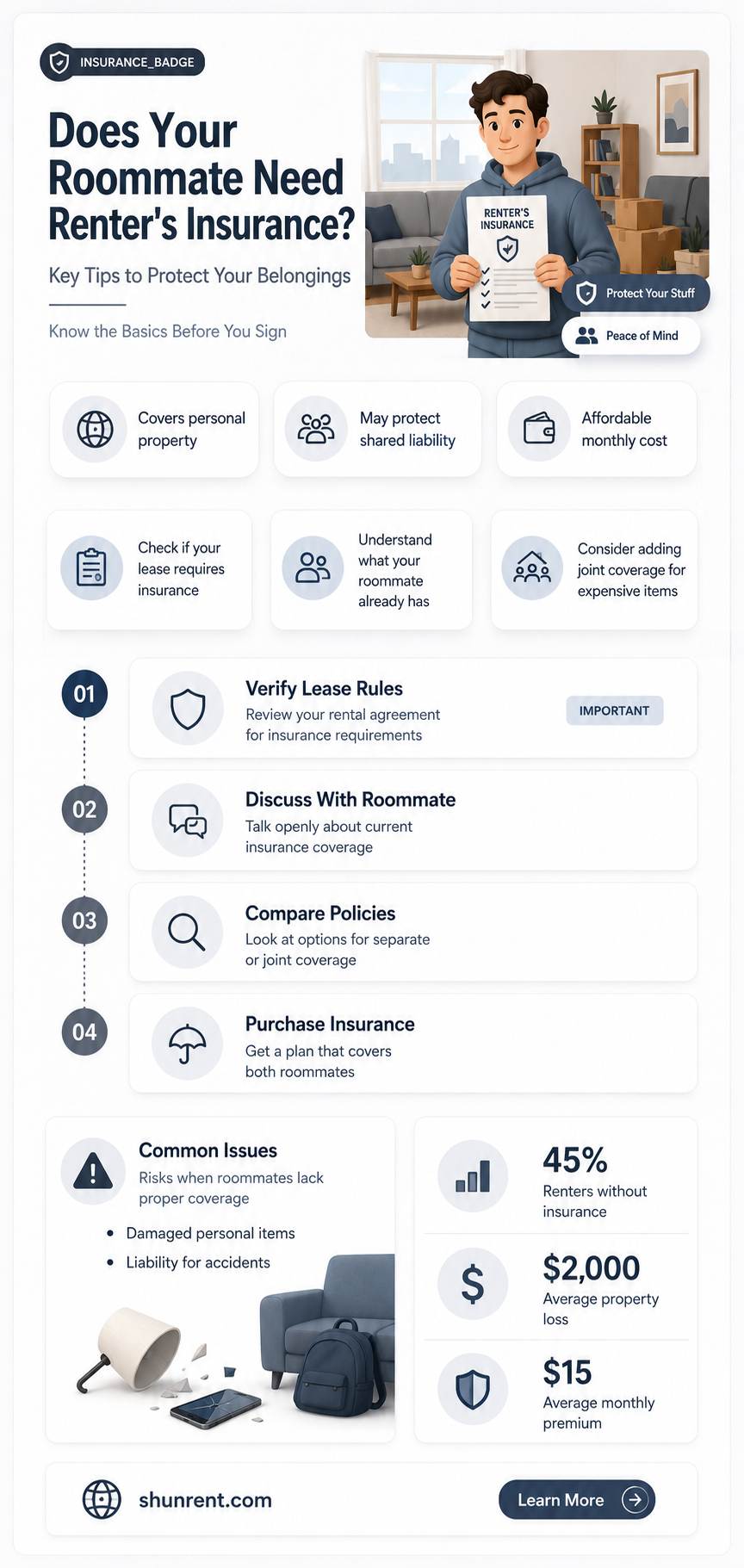

When sharing a living space, many renters assume their roommate’s insurance policy will cover their belongings, but this is often a misconception. Renter's insurance is typically individual, meaning it protects only the policyholder’s personal property and liability. If your roommate has a policy, it likely won’t extend to your possessions in the event of theft, damage, or loss. Additionally, liability coverage—which protects against claims if someone is injured in your rented space—is also specific to the policyholder. Therefore, having your own renter’s insurance ensures your belongings are protected and provides personal liability coverage, offering peace of mind and financial security in shared living situations.

| Characteristics | Values |

|---|---|

| Legal Requirement | Not legally required, but highly recommended. |

| Coverage for Personal Belongings | Protects personal property (e.g., furniture, electronics) from theft, fire, or damage. |

| Liability Protection | Covers legal costs if someone is injured in the rented space. |

| Shared Policy Feasibility | Roommates can share a policy, but individual policies are often preferred for clarity. |

| Cost of Individual Policies | Typically affordable, ranging from $15 to $30 per month. |

| Landlord's Insurance Coverage | Landlord's insurance covers the building, not tenants' personal belongings. |

| Subleasing and Coverage | Coverage may not extend to subleased roommates; they should get their own insurance. |

| Pet-Related Damages | Some policies cover pet-related damages, but exclusions may apply. |

| Living Situation Impact | Coverage needs may vary based on the number of roommates and shared items. |

| Policy Customization | Policies can be tailored to individual needs (e.g., high-value item coverage). |

| Claim Process | Claims are filed individually, even if roommates share a policy. |

| Credit Score Impact | Filing a claim may affect premiums but typically does not impact credit score. |

| State-Specific Regulations | Some states may have specific guidelines or recommendations for renters. |

| Temporary Living Arrangements | Short-term renters may still benefit from renter's insurance. |

| Roommate Conflict Protection | Does not cover disputes between roommates but protects against external liabilities. |

Explore related products

What You'll Learn

![]()

Shared Liability Risks

Living with a roommate can blur the lines of responsibility, especially when it comes to shared liability risks. If your roommate accidentally starts a fire while cooking, damages a neighbor’s property, or causes an injury within the rental unit, both of you could be held financially responsible. Landlord insurance typically covers the structure but not personal belongings or tenant-caused damages. Without individual renter’s insurance, you might be forced to split repair costs, legal fees, or medical bills out of pocket, even if you weren’t directly at fault.

Consider this scenario: Your roommate’s guest spills wine on an expensive rug owned by the landlord. The landlord demands $500 for replacement. If your roommate lacks renter’s insurance, they may turn to you for help covering the cost, regardless of your involvement. Renter’s insurance with liability coverage could shield you from such shared financial burdens by covering damages or injuries caused by anyone living in the unit, including roommates. However, relying on a roommate’s policy is risky, as their coverage limits might not fully address a claim, leaving you exposed.

A common misconception is that roommates are automatically covered under a single renter’s insurance policy. While some insurers allow listing roommates as "additional insured parties," this isn’t standard practice. Most policies only cover the named policyholder’s liability and belongings. For instance, if your roommate’s laptop is stolen during a break-in, your policy won’t compensate them unless explicitly added as an insured party. Separate policies ensure each roommate’s possessions and liability are independently protected, avoiding disputes over coverage gaps.

To mitigate shared liability risks, follow these steps: First, verify your lease agreement to understand joint liability clauses. Second, encourage your roommate to purchase their own renter’s insurance, ideally with at least $100,000 in liability coverage. Third, document shared property ownership and keep receipts for high-value items. Finally, consider a "roommate agreement" outlining financial responsibilities in case of accidents. While these steps reduce risk, they don’t replace the comprehensive protection of individual renter’s insurance.

The takeaway is clear: Shared living spaces amplify shared liability risks. Renter’s insurance isn’t just about protecting your belongings—it’s about safeguarding your finances from unforeseen accidents involving roommates or guests. Don’t assume your roommate’s policy will cover you; instead, invest in your own coverage to ensure you’re both protected. After all, the cost of a policy is negligible compared to the potential expenses of a liability claim.

Negotiating NYC Rent: Tips and Strategies for Tenants

You may want to see also

Explore related products

$10.99

![]()

Personal Property Coverage

Roommates often assume their belongings are covered under their roommate's renter's insurance policy, but this is a dangerous misconception. Personal Property Coverage, a core component of renter's insurance, typically protects only the policyholder's possessions. If your laptop gets stolen or your furniture is damaged in a fire, your roommate's policy won't cover your losses unless you're explicitly listed as an additional insured. This means you could be left financially responsible for replacing your items, highlighting the critical need for individual coverage.

Consider this scenario: You and your roommate share an apartment, and a pipe bursts, flooding the unit. Your roommate's expensive camera equipment is ruined, but your vintage record collection is also destroyed. If only your roommate has renter's insurance, their policy will cover their losses, but your cherished records are out of luck. Personal Property Coverage ensures that your belongings are protected regardless of who caused the damage or whether your roommate has insurance. It’s a safeguard that prevents you from bearing the full cost of unexpected events.

When evaluating Personal Property Coverage, it’s essential to understand the limits and types of protection available. Most policies offer either Actual Cash Value (ACV) or Replacement Cost coverage. ACV accounts for depreciation, meaning you’ll receive the item’s current value, not what it cost new. Replacement Cost, on the other hand, covers the expense of buying a new item at today’s prices. For high-value items like jewelry or electronics, you may need to add a rider to your policy to ensure full coverage. Assess your possessions and choose the option that best aligns with your needs and budget.

A common mistake roommates make is underestimating the value of their belongings. Start by creating a detailed inventory of your possessions, including electronics, furniture, clothing, and sentimental items. Use a home inventory app or spreadsheet to document each item’s purchase date, price, and current value. This not only helps you determine the appropriate coverage amount but also streamlines the claims process if you ever need to file one. Remember, Personal Property Coverage isn’t just for high-ticket items—it’s for everything that makes your space feel like home.

Finally, don’t let cost deter you from getting Personal Property Coverage. Renter’s insurance is surprisingly affordable, often costing less than your monthly streaming subscription. For as little as $15 to $30 per month, you can secure coverage that protects your belongings from theft, fire, water damage, and more. Many insurers also offer discounts for bundling policies or installing safety features like smoke detectors. Investing in Personal Property Coverage is a small price to pay for the peace of mind that comes with knowing your belongings are protected, no matter what your roommate’s insurance situation may be.

Basement Rentals: NYC's Hefty Fines for Illegal Digs

You may want to see also

Explore related products

![]()

Cost-Sharing Options

Sharing renter's insurance with a roommate can significantly reduce individual costs, but it requires careful planning and clear agreements. Start by assessing your combined coverage needs—personal property, liability, and additional living expenses. Most policies allow listing multiple occupants, but ensure the policy limit reflects the total value of both roommates’ belongings. For example, if your combined possessions are worth $40,000, opt for a policy with at least that coverage to avoid underinsurance. Divide the annual premium equally, or adjust based on income or asset value, ensuring fairness.

Before committing, evaluate the risks of joint policies. If one roommate fails to pay their share, the policy could lapse, leaving both unprotected. To mitigate this, set up a shared payment account or use a third-party app like Venmo or Splitwise to track contributions. Additionally, consider adding a "named insured" clause, which allows either roommate to manage the policy independently. This ensures continuity if one person moves out or becomes unreliable.

Another cost-sharing strategy is to split coverage types instead of premiums. For instance, one roommate could cover personal property while the other handles liability. This works best if one person owns high-value items (e.g., jewelry or electronics) and the other has greater liability risks (e.g., frequent guests). However, this approach requires trust and transparency about individual assets and lifestyles. Regularly review the arrangement to address changes in circumstances.

For roommates with mismatched budgets, explore tiered cost-sharing models. The roommate with higher income or more valuable possessions could contribute a larger percentage of the premium. For example, if one roommate earns 60% more, they might pay 60% of the cost. This approach balances financial responsibility while maintaining equitable protection. Document the agreement in writing to avoid disputes later.

Finally, consider bundling renter’s insurance with other policies for additional savings. If both roommates have auto insurance, bundling with the same provider can reduce premiums by 5–15%. Alternatively, look for group discounts through employers, alumni associations, or professional organizations. These strategies not only lower costs but also simplify management by consolidating policies under one provider. Always compare standalone and bundled quotes to ensure the savings outweigh potential drawbacks.

Rent Comparison: Los Angeles vs. Rome – Which City Costs More?

You may want to see also

Explore related products

![]()

Policy Coordination Tips

Roommates often assume their possessions are covered under a single renter’s insurance policy, but this misconception can lead to gaps in protection. Each roommate should secure their own policy to ensure personal belongings are fully insured, as most policies do not extend coverage to non-listed individuals. For instance, if one roommate’s laptop is stolen, only their policy would cover the loss, not their roommate’s. This individualized approach prevents disputes and ensures comprehensive protection.

When coordinating policies, start by comparing coverage limits and deductibles. If one roommate has a higher-value item, such as a luxury guitar or high-end electronics, their policy should reflect that with adequate coverage. Use a shared spreadsheet to list each roommate’s belongings and corresponding policy details. This transparency helps identify overlaps or gaps and ensures everyone is on the same page. For example, if both roommates own gaming consoles, verify that each device is covered under separate policies to avoid underinsurance.

Communication is key to avoiding redundancy or exclusion in coverage. Discuss liability coverage, which protects against accidents like a guest slipping in the apartment. Ensure both policies include liability, but avoid duplicating limits unnecessarily. For instance, if one roommate has $100,000 in liability coverage, the other might opt for a lower limit to save costs. Regularly review policies annually or after significant purchases to keep coverage aligned with current needs.

Finally, consider bundling policies with the same insurer for potential discounts. Some providers offer multi-policy discounts if roommates insure their belongings under the same company. However, prioritize individual needs over cost savings. For example, if one roommate requires higher coverage for valuable jewelry, they should not compromise for a group discount. Balancing coordination with personalization ensures both roommates are adequately protected without sacrificing affordability.

Rent a 12-Passenger Van in Vancouver: Top Locations & Tips

You may want to see also

Explore related products

![]()

Landlord Requirements Check

Landlords often mandate renter’s insurance as a condition of the lease, but this requirement isn’t universal. Before assuming your roommate is covered under your policy, scrutinize the lease agreement. Some landlords explicitly require each tenant to carry individual renter’s insurance, while others may accept a shared policy. This distinction matters because shared policies might not cover all roommates equally, leaving gaps in liability and personal property protection. Always verify the landlord’s specific requirements to avoid lease violations or uncovered risks.

Analyzing the landlord’s insurance policy is equally critical. While landlords typically carry insurance for the building structure, this coverage doesn’t extend to tenants’ belongings or personal liability. For instance, if a fire damages your roommate’s electronics, the landlord’s policy won’t compensate them. This gap underscores why roommates should independently assess their need for renter’s insurance, regardless of the landlord’s stance. Misunderstanding this division of responsibility can lead to costly surprises in the event of damage or loss.

Persuading a reluctant roommate to get renter’s insurance becomes easier when framed as a shared risk mitigation strategy. Highlight scenarios like water damage from a burst pipe or theft during a break-in, where both parties could face financial loss. Emphasize that renter’s insurance typically costs $15–$30 per month—a small price for peace of mind. If the landlord requires individual policies, present it as a non-negotiable compliance issue rather than an optional expense. Practical tip: Some insurers offer discounts for bundling renter’s insurance with auto or other policies, making it more affordable.

Comparing the risks of having versus not having renter’s insurance reveals a clear advantage. Without it, roommates risk paying out-of-pocket for damages to their belongings or lawsuits stemming from accidents in the rental. For example, if a guest slips and falls in the apartment, both roommates could be held liable. Renter’s insurance typically includes liability coverage up to $100,000 or more, shielding tenants from such financial burdens. Conversely, relying solely on the landlord’s insurance or a roommate’s policy leaves significant vulnerabilities, especially if the policy limits are insufficient or exclusions apply.

Descriptive scenarios illustrate the importance of this check. Imagine a kitchen fire caused by an unattended stove—a common hazard in shared living spaces. If only one roommate has renter’s insurance, the other might lose all their possessions without reimbursement. Alternatively, consider a situation where a roommate’s pet damages the apartment, leading to repair costs and potential legal fees. Renter’s insurance with liability coverage would handle these expenses, but only if both roommates are adequately insured. Such examples underscore why verifying and meeting landlord requirements is a proactive step toward protecting everyone involved.

Mausoleum Spaces: Rented or Perpetual?

You may want to see also

Frequently asked questions

Yes, your roommate should have their own renter's insurance policy. Most policies only cover the named policyholder and their belongings, so your roommate’s possessions may not be protected under your coverage.

Some insurers allow roommates to be listed on the same policy, but it’s not always the best option. Separate policies ensure each roommate’s belongings are fully covered and prevent complications if one roommate moves out or files a claim.

If your roommate has renter's insurance, their liability coverage may help pay for damages caused by their guest. Without insurance, your roommate could be personally responsible for the costs, potentially affecting both of you if the landlord seeks compensation.

Some landlords require all tenants, including roommates, to have renter's insurance as part of the lease agreement. Even if it’s not required, it’s highly recommended to protect both personal belongings and liability risks.