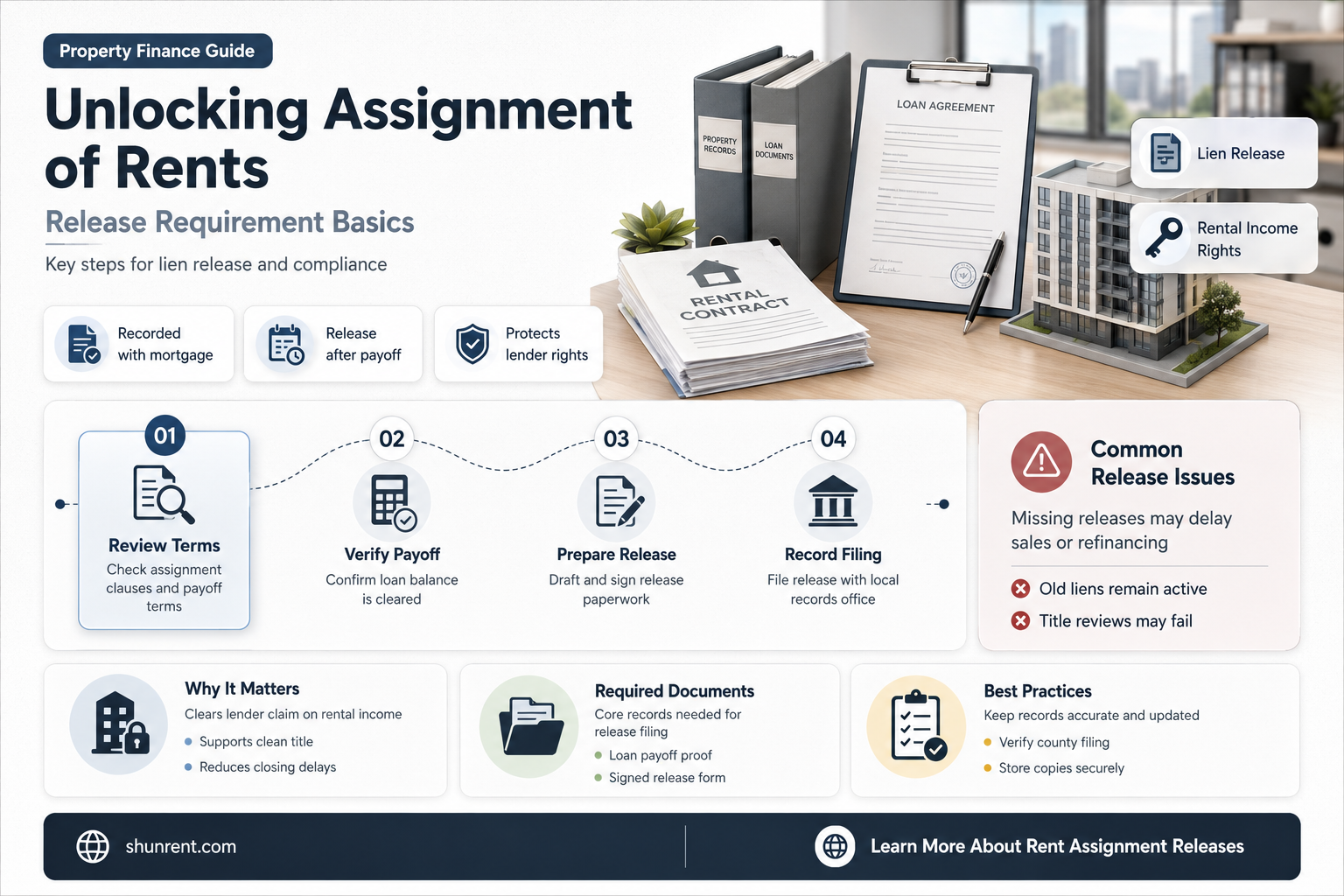

An assignment of rents is a strategic move that serves as a risk mitigation mechanism for lenders. It is an agreement between a borrower and a lender that offers financial protection in the event of a loan default. The agreement outlines the amount the lender can collect from rental income if the borrower defaults on the loan. This agreement can be released through a formal termination document outlining the terms, conditions, and effective date of the release. Both parties must execute the release agreement, with signatures often witnessed or notarized according to local laws.

| Characteristics | Values |

|---|---|

| Purpose | Risk mitigation for lenders |

| Function | Granting the lender a security interest in existing and future leases, rents, issues, or profits generated by the secured property |

| Activation | When the borrower defaults on their loan |

| Requirements | The AOR must be in writing, executed by the borrower, and recorded with the county where the property is located |

| Termination | When the loan secured by the Deed of Trust or Mortgage is fully paid off and the lender formally discharges the mortgage |

| Process | A formal agreement or termination document is drafted, outlining the terms, conditions, and effective date of the release. Both parties execute it, with signatures witnessed or notarized in accordance with local laws. |

| Additional Information | Lenders and borrowers may negotiate and agree upon how certain costs will be distributed between them. |

Explore related products

![ROOM FOR RENT [DVD]](https://m.media-amazon.com/images/I/61DHqNLhcoL._AC_UY218_.jpg)

What You'll Learn

- The assignment of rents is a risk mitigation strategy for lenders

- Absolute and collateral are two types of assignment of rents

- Lenders cannot be held liable for any action or inaction

- The release requires a mutual agreement between the property owner and the party with assignment rights

- The release is drafted as a formal agreement or termination document

![]()

The assignment of rents is a risk mitigation strategy for lenders

The assignment of rents is a legal mechanism that allows a property owner to assign the right to collect rent payments from a particular property to a third party, usually a lender. This is typically done as a form of security interest for a loan or mortgage. By doing so, the property owner provides financial protection to the lender in the event of a loan default. This serves as additional security for lenders, ensuring they have another source of income to offset any potential losses.

The assignment of rents is often included as a clause in the mortgage document or trust deed, but it can also exist as a separate document. This clause specifies the conditions under which the lender can start collecting rents from the property. Usually, this right is triggered when the borrower defaults on the loan. Once activated, the lender can either collect rents directly or appoint a receiver to manage the property and collect rents on their behalf.

There are two main types of assignment of rents: absolute assignment and collateral assignment. In an absolute assignment, property owners transfer complete control over rental income collection to the lender. This gives the lender maximum control and assurance, especially in situations with a high risk of borrower default. From the beginning of the agreement, lenders can secure a consistent revenue stream to cover mortgage payments. However, this option significantly impacts the property owner's autonomy and decision-making power regarding the property's financial aspects.

On the other hand, a collateral assignment of rents provides a more balanced approach. In this arrangement, the property owner grants the lender conditional authority over rental income collection. The lender's authority only comes into effect when the borrower fails to meet their obligations, typically by defaulting on the loan. Collateral assignment allows lenders to have a measure of security while giving property owners more control until specific conditions, such as borrower default, are met.

Overall, the assignment of rents is a strategic risk mitigation tool for lenders. It offers financial protection and ensures a consistent income stream in case of borrower default. By including this clause in loan agreements, lenders can enhance their security and minimise potential losses.

Rent-A-Center's Future: Is It Closing Down?

You may want to see also

Explore related products

![]()

Absolute and collateral are two types of assignment of rents

An assignment of rents refers to a legal agreement where a property owner assigns or transfers their right to receive rental income from tenants to another party, typically a mortgage lender or a financial institution. This agreement usually serves as collateral for a loan or mortgage and provides financial protection for lenders in the event of borrower defaults. The specifics of the agreement can vary, with some allowing the borrower to continue collecting rents until a default, while others mandate an immediate transfer of rental income to the lender upon default.

Absolute and collateral assignments of rents are the two primary types of agreements. In an absolute assignment, property owners voluntarily and unequivocally transfer total control over rental income collection to the lender. This empowers the lender with unconditional authority to directly manage and allocate rental funds, providing them with maximum control and assurance. This type of agreement is particularly relevant when there is an elevated risk of borrower default, as it ensures a consistent revenue stream to cover mortgage payments. However, it significantly impacts the property owner's autonomy and decision-making power regarding the property's financial aspects.

On the other hand, a collateral assignment of rents grants the lender more limited authority. In this arrangement, the property owner transfers control over rental income to the lender, but the lender's authority is conditional. The collateral assignment provides a balance between the interests of the property owner and the lender, allowing the owner to retain some decision-making capabilities while still offering financial protection to the lender.

The legal implications of these agreements can vary depending on the governing jurisdiction and the specific measures undertaken by the lender following a default. For example, in states operating under a ""lien theory" of mortgages, like New York, a lender must foreclose its lien before acquiring "title" to the property's rents, whereas in other states, the lender may need to take affirmative steps to establish control over rents.

Waterfront's Premium Office Space for Rent

You may want to see also

Explore related products

![]()

Lenders cannot be held liable for any action or inaction

Lenders play a crucial role in the financial ecosystem by providing loans and facilitating access to credit. While they are integral to the process, it's important to understand that lenders are not responsible or liable for the borrower's actions or inaction. This means that lenders cannot be held legally accountable if a borrower fails to meet their obligations or takes inappropriate actions.

The principle of "lenders not being held liable" is rooted in the fundamental nature of lending as a contractual agreement between two parties. When an individual or entity borrows money, they enter into a legally binding contract with the lender, agreeing to repay the loan according to specified terms and conditions. These terms outline the rights and responsibilities of both parties and serve as the foundation for their financial relationship.

By accepting the loan, the borrower assumes the responsibility to fulfill their end of the bargain, which includes making timely payments and adhering to any other agreed-upon conditions. Should they fail to do so, it is the borrower who is in breach of contract, not the lender. The lender's role is primarily confined to providing the agreed-upon funds and establishing repayment terms, and they are not responsible for ensuring the borrower's performance or guaranteeing the outcome of the loan.

Moreover, lenders cannot be expected to anticipate or prevent every possible negative consequence of a borrower's inaction or actions. Each borrower's financial situation and behavior are unique, and lenders are not privy to all the intricacies of their financial lives. Imposing liability on lenders for a borrower's behavior would be impractical and unjust, as it would require lenders to shoulder the burden of unpredictable and uncontrollable factors.

In conclusion, the principle of "lenders cannot be held liable for any action or inaction" is essential to maintaining a functional and equitable lending environment. It protects lenders from undue legal exposure and ensures that borrowers are held accountable for their financial commitments. This framework fosters a stable and predictable lending ecosystem, benefiting both lenders and borrowers alike.

Renting a Condo? You May Need Insurance

You may want to see also

Explore related products

![]()

The release requires a mutual agreement between the property owner and the party with assignment rights

The release of an assignment of rents requires a mutual agreement between the property owner and the party with assignment rights. This process involves negotiating the allocation of costs and ensuring compliance with local laws and regulations. Both parties must agree on the terms, conditions, and effective date of the release, which is typically drafted as a formal agreement or termination document. Signatures on the release agreement are often witnessed or notarized, depending on local laws.

The release of an assignment of rents is typically tied to the repayment of the underlying mortgage or loan. In most cases, the assignment is released once the mortgage or loan is fully paid off, and the lender formally discharges the mortgage. At this point, the borrower regains full control over the property's rental income.

It is important to note that the specifics of assignment of rents can vary based on the terms negotiated between the lender and borrower. Some agreements may allow the borrower to continue collecting rents until a default occurs, while others may require the automatic transfer of rental income to the lender upon default.

To ensure legal compliance and clarity, it is recommended to engage the services of a real estate lawyer. Lawyers can provide expertise in real estate law and navigate the intricacies of the legal landscape. They can also ensure that the assignment of rents complies with applicable laws, such as Alberta's Land Titles Act, and is properly registered in the land titles.

Additionally, tenants who were previously informed of the assignment should be provided with written notice of the release, along with clear instructions regarding future rent payments. This notice should be filed with the relevant land title office to update property records.

Backhoe Rentals: License Requirements and Rules

You may want to see also

Explore related products

![]()

The release is drafted as a formal agreement or termination document

The release of an assignment of rents is a formal agreement or termination document that outlines the terms, conditions, and effective date of the release. It is a collaborative process that requires mutual agreement between the property owner and the party holding the assignment rights. The release agreement is prepared and executed by both parties, with signatures witnessed or notarized according to local laws.

The release agreement should include clear instructions regarding future rent payments for tenants. It is essential to file the release agreement or necessary notices with the relevant land title office to ensure the property records are updated. For instance, in Alberta, Canada, the release agreement or notices should be filed with the Alberta Land Title Office.

The assignment of rents is a strategic move that serves as a risk mitigation mechanism for lenders. It offers financial protection in the event of a borrower's default by allowing the lender to collect rental income directly. The assignment of rents can be enforced as an alternative to foreclosure, helping to maintain a positive relationship with the borrower.

To ensure legal compliance and clarity, it is recommended to engage a lawyer with expertise in real estate law. Lawyers can tailor their services to meet the specific needs and characteristics of the property and parties involved. They play a crucial role in drafting comprehensive and legally sound assignment agreements, navigating the intricacies of the law, and advocating for their clients in disputes.

In summary, the release of an assignment of rents is a formal agreement or termination document that requires collaboration and agreement between the property owner and the party holding the assignment rights. It is essential to involve legal professionals to ensure compliance with relevant laws and regulations and to protect the interests of all parties involved.

Who Owned the Helicopter in Kobe Bryant's Tragic Crash?

You may want to see also

Frequently asked questions

An assignment of rents is an agreement between a borrower and a lender of mortgage loans that provides financial protection to the lender in the event of a loan default.

An assignment of rents is typically released when the mortgage has been paid off. Both parties must agree and sign a formal agreement or termination document outlining the terms, conditions, and effective date of the release.

In the event of a default, the lender can collect rent directly from the tenant to help satisfy the debt. The specifics of this process depend on the terms negotiated between the lender and borrower.