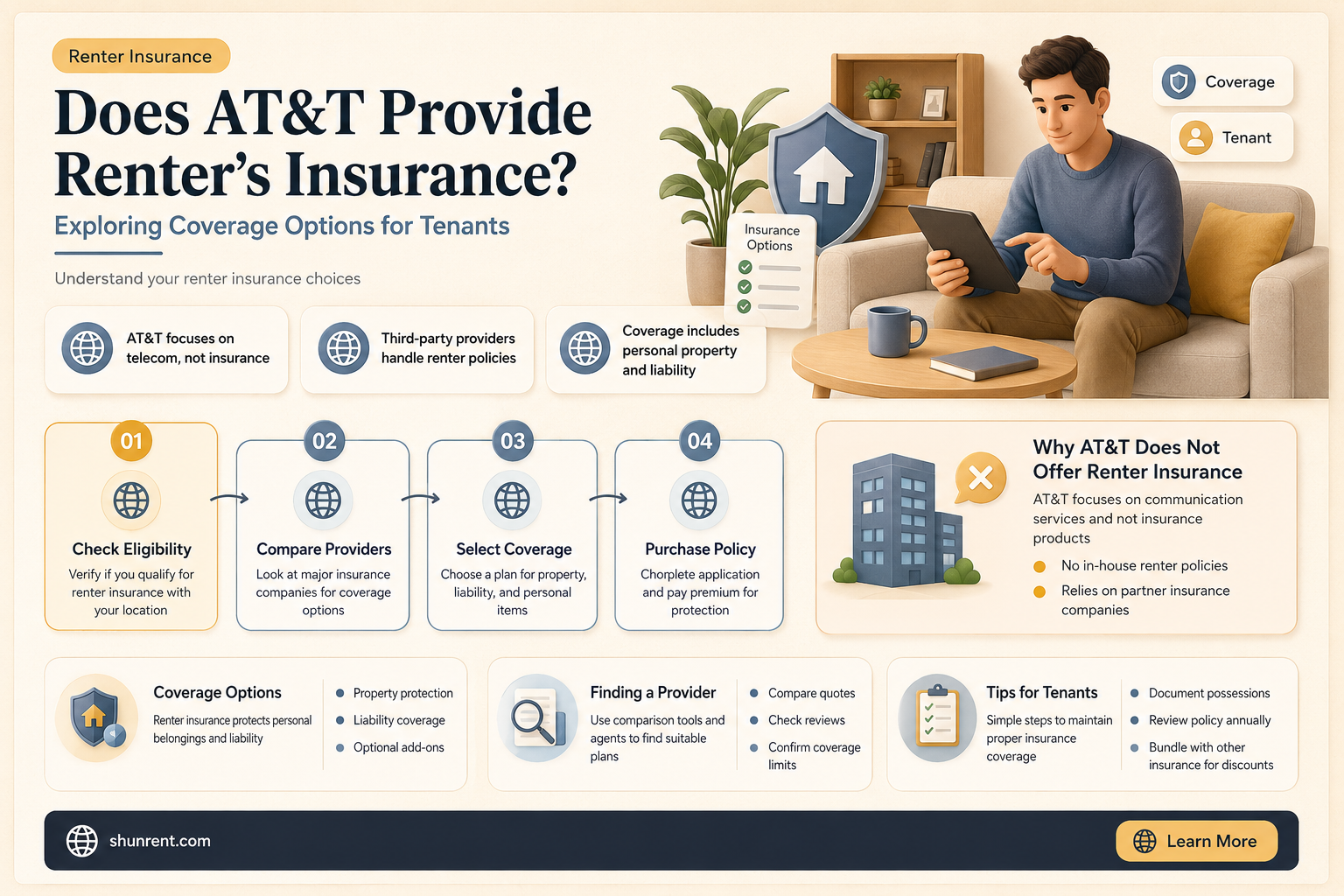

When considering insurance options, many renters wonder if their service providers, such as AT&T, offer renter's insurance as part of their portfolio. While AT&T is primarily known for its telecommunications services, including mobile, internet, and television, it does not directly provide renter's insurance. However, AT&T has partnered with various insurance companies to offer bundled services or discounts to its customers. Renters looking for insurance coverage should explore dedicated insurance providers or compare options through third-party platforms to find the best policy for their needs.

| Characteristics | Values |

|---|---|

| Does AT&T offer renter's insurance directly? | No |

| Does AT&T partner with insurance providers for renter's insurance? | No |

| Can AT&T customers get discounts on renter's insurance? | No specific discounts mentioned |

| Alternative options for AT&T customers seeking renter's insurance | Customers can explore independent insurance providers or compare quotes online |

| Relevance of AT&T to renter's insurance | None, as AT&T primarily offers telecommunications and entertainment services |

| Last Updated | June 2024 |

Explore related products

What You'll Learn

![]()

AT&T's partnership with insurance providers

AT&T, primarily known for its telecommunications services, has expanded its offerings through strategic partnerships with insurance providers. These collaborations aim to provide customers with bundled services that go beyond traditional telecom solutions. For instance, AT&T has partnered with companies like Allstate and State Farm to offer renters insurance as an add-on to their existing plans. This approach not only enhances customer convenience but also leverages AT&T’s vast customer base to tap into new markets. By integrating insurance options, AT&T positions itself as a one-stop shop for essential services, appealing to tech-savvy consumers who value simplicity and efficiency.

Analyzing these partnerships reveals a broader trend in the telecom industry: diversification. Companies like AT&T are increasingly venturing into adjacent markets to drive revenue growth and customer retention. Renters insurance, in particular, is a natural fit due to its relevance to a broad demographic, especially younger, urban customers who are more likely to rent rather than own homes. AT&T’s partnerships often include digital tools that streamline the insurance purchasing process, such as mobile apps for policy management and claims filing. This tech-driven approach aligns with the company’s core strengths and enhances the overall customer experience.

For consumers, the benefits of AT&T’s insurance partnerships are clear. Bundling renters insurance with telecom services can lead to cost savings through discounts or promotional rates. Additionally, the convenience of managing multiple services through a single provider reduces administrative hassle. However, it’s essential for customers to compare policies carefully, as bundled options may not always offer the best coverage or pricing. Practical tips include reviewing policy details, checking for hidden fees, and assessing whether the bundled plan meets individual needs. For example, a 25-year-old renter in an urban area might prioritize liability coverage over personal property protection, depending on their lifestyle.

Comparatively, AT&T’s approach differs from competitors like Verizon or T-Mobile, which have yet to establish similar insurance partnerships. This distinction gives AT&T a competitive edge in attracting and retaining customers who value comprehensive service offerings. However, the success of these partnerships hinges on effective marketing and customer education. AT&T must clearly communicate the value proposition of bundled insurance to avoid confusion or skepticism. For instance, highlighting success stories or case studies of customers who benefited from the partnership could strengthen trust and adoption.

In conclusion, AT&T’s partnerships with insurance providers represent a strategic move to diversify its offerings and enhance customer value. By focusing on renters insurance, the company addresses a growing market need while leveraging its technological expertise. For consumers, these partnerships offer convenience and potential cost savings, but careful evaluation is key to ensuring the right fit. As AT&T continues to expand into new markets, its ability to innovate and educate will determine the long-term success of these initiatives.

Top RV Parking Spots in Riverside: Where to Rent Your Space

You may want to see also

Explore related products

$10.99

![]()

Bundling options for renters

AT&T does not directly offer renter's insurance, but bundling options for renters can still be a strategic move to save money and streamline services. Many insurance providers partner with telecom companies or offer discounts when you combine policies. For instance, bundling your renter’s insurance with auto or life insurance from a provider like State Farm, Allstate, or Lemonade can reduce premiums by 5–15%. If you’re an AT&T customer, explore partnerships or discounts through their affiliated services, such as AT&T’s home security offerings, which sometimes include insurance incentives when paired with other plans.

To maximize bundling benefits, start by evaluating your current AT&T services, such as internet, TV, or mobile plans. Some providers offer loyalty discounts or promotional rates when you add a third-party insurance policy to your existing telecom bundle. For example, if you have AT&T Fiber, check if your insurance provider offers a discount for bundling renter’s insurance with your internet plan. Additionally, consider using aggregator platforms like Policygenius or Gabi to compare bundled quotes from multiple insurers, ensuring you’re getting the best deal without switching telecom providers.

A lesser-known strategy is leveraging credit card rewards or membership programs tied to your AT&T account. Some cards, like the AT&T Access Card, offer cashback or points that can offset insurance costs. Pairing this with a renter’s insurance policy from a provider like Lemonade or Liberty Mutual, which often have digital-first platforms, can simplify management and amplify savings. For renters aged 25–35, this approach is particularly effective, as it aligns with tech-savvy habits and budget-conscious priorities.

Finally, bundling isn’t just about cost—it’s about convenience. Opt for providers that offer a single dashboard for managing both telecom and insurance services. For example, if you bundle renter’s insurance with a provider like Progressive, which has partnerships with telecom companies, you might gain access to a unified app for billing and claims. This reduces administrative hassle and ensures you’re not missing out on hidden discounts. Always read the fine print, though, as some bundles may lock you into long-term contracts or exclude certain coverage options.

What Are Utilities, Rent, and Food Expenses?

You may want to see also

Explore related products

![]()

Coverage details and limits

AT&T, primarily known for telecommunications services, does not directly offer renter's insurance. However, understanding coverage details and limits is crucial when selecting a policy from actual insurance providers. Here’s a focused guide to navigating these aspects effectively.

Analytical Insight: Renter’s insurance policies typically cover personal property, liability, and additional living expenses. Personal property coverage protects belongings like furniture, electronics, and clothing, often up to a limit of $20,000 to $50,000, depending on the plan. Liability coverage, usually ranging from $100,000 to $500,000, shields against claims if someone is injured in your rented space. Additional living expenses cover temporary housing and meals if your home becomes uninhabitable, often capped at 20-40% of the total policy value.

Instructive Steps: When evaluating coverage limits, assess your possessions’ total value using a home inventory. For high-value items like jewelry or art, consider scheduling them separately, as standard policies may impose sub-limits (e.g., $1,000 for jewelry). Review liability limits based on your risk exposure—higher limits are advisable if you frequently host guests. Ensure additional living expense coverage aligns with local rental costs to avoid out-of-pocket expenses during displacement.

Comparative Perspective: Unlike homeowners’ insurance, renter’s insurance excludes structural coverage since the landlord’s policy typically covers the building. However, renters’ policies often include broader liability protection, such as legal fees for covered incidents. Compare policies to ensure they cover perils like fire, theft, and water damage, as exclusions vary by provider.

Practical Tips: Opt for replacement cost coverage over actual cash value to receive the full cost of replacing damaged items, not their depreciated value. Review policy deductibles, typically $500 to $2,000, and choose one that balances affordability with out-of-pocket risk. Bundle renter’s insurance with auto or other policies for potential discounts, even if not through AT&T.

Takeaway: While AT&T doesn’t offer renter’s insurance, understanding coverage details and limits empowers you to select a policy that safeguards your belongings, liability, and financial stability. Tailor limits to your needs, and don’t overlook add-ons for comprehensive protection.

Rent Live in Seattle: Show Time and Viewing Details Revealed

You may want to see also

Explore related products

![]()

Cost and discounts available

AT&T does not directly offer renter’s insurance, but understanding the cost and discounts available in the broader market can help renters make informed decisions. On average, renter’s insurance costs between $15 and $30 per month, depending on factors like location, coverage limits, and deductible amounts. For instance, policies in areas prone to natural disasters like hurricanes or earthquakes tend to be more expensive. Conversely, renters in low-crime neighborhoods may enjoy lower premiums. Knowing these benchmarks allows you to assess whether a quote is competitive, even if it’s not from AT&T.

To maximize savings, renters should explore common discounts offered by insurance providers. Bundling renter’s insurance with auto or other policies can yield discounts of up to 15%. Many insurers also offer reductions for safety features like smoke detectors, security systems, or fire extinguishers in the rental unit. For example, having a monitored security system could save you 5% on your premium. Additionally, some companies provide discounts for policyholders who pay annually instead of monthly or for those with a claims-free history. These discounts can significantly reduce costs, making comprehensive coverage more affordable.

Another cost-saving strategy is to adjust your policy’s deductible and coverage limits. A higher deductible—say, $1,000 instead of $500—can lower your monthly premium, but ensure you can afford the out-of-pocket cost in case of a claim. Similarly, evaluate whether you need additional coverage for high-value items like jewelry or electronics, as this will increase your premium. For instance, adding $5,000 in jewelry coverage might raise your annual cost by $50 to $100. Tailoring your policy to your specific needs prevents overpaying for unnecessary coverage.

Lastly, take advantage of lesser-known discounts that could apply to your situation. Some insurers offer discounts for renters who are non-smokers, work in certain professions (e.g., teachers or first responders), or belong to specific organizations like alumni associations. For example, being a member of AARP or a credit union might qualify you for a 5% discount. Even small discounts can add up, so it’s worth asking your provider about all available options. By combining these strategies, renters can secure robust coverage at a price that fits their budget, even if AT&T isn’t their insurer.

Homeowner's Guide: Safeguarding Your Property and Rights as a Landlord

You may want to see also

Explore related products

![]()

Customer reviews and satisfaction

AT&T, primarily known for telecommunications services, does not directly offer renter's insurance. However, customer reviews and satisfaction in this context often revolve around bundled services or partnerships. For instance, AT&T’s collaborations with third-party providers like Allstate or State Farm are frequently mentioned in reviews. Customers appreciate the convenience of managing multiple services through a single provider, though some express confusion about whether AT&T is the actual insurer. This highlights a critical takeaway: clarity in partnerships is essential for customer trust.

Analyzing reviews reveals a pattern: bundled discounts are a significant driver of satisfaction. Customers who pair renter’s insurance with AT&T’s internet or TV services often report savings of 10–15%. However, dissatisfaction arises when these discounts expire or when billing issues occur. For example, one reviewer noted a $20 monthly increase after the first year, leading to frustration. To maximize satisfaction, customers should scrutinize contract terms and set calendar reminders to review rates annually.

Persuasive arguments in reviews often center on the perceived reliability of AT&T’s brand extending to insurance offerings. Many customers assume that AT&T’s involvement guarantees quality, even when the insurance is underwritten by another company. This trust, however, can backfire if claims processing or customer service falls short. A comparative analysis shows that standalone insurance providers consistently outperform bundled options in claims satisfaction, suggesting customers should weigh convenience against potential trade-offs.

Descriptive reviews paint a picture of the claims process, which is a critical factor in satisfaction. Customers who filed claims through AT&T’s partnered insurance reported mixed experiences. While some praised the seamless integration with their existing AT&T account, others faced delays due to unclear communication between AT&T and the insurer. Practical advice from reviewers includes documenting all interactions and using AT&T’s app for tracking claims, as it often provides faster updates than phone support.

Instructive feedback from customers emphasizes the importance of understanding coverage limits. Many reviewers were unaware that their bundled renter’s insurance excluded high-value items like jewelry or electronics unless explicitly added. To avoid dissatisfaction, customers should request a detailed policy breakdown and consider supplemental coverage for valuable possessions. This proactive approach ensures expectations align with reality, fostering long-term satisfaction.

Understanding Federal Rent Checks: Benefits, Eligibility, and Application Process

You may want to see also

Frequently asked questions

No, AT&T does not offer renter's insurance directly. They primarily provide telecommunications and technology services.

AT&T does not offer bundling options for renter's insurance, as it is not part of their service portfolio.

AT&T does not have partnerships with insurance companies to provide renter's insurance. Customers would need to seek coverage from dedicated insurance providers.

You can find renter's insurance through traditional insurance companies, online providers, or independent agents specializing in insurance products.