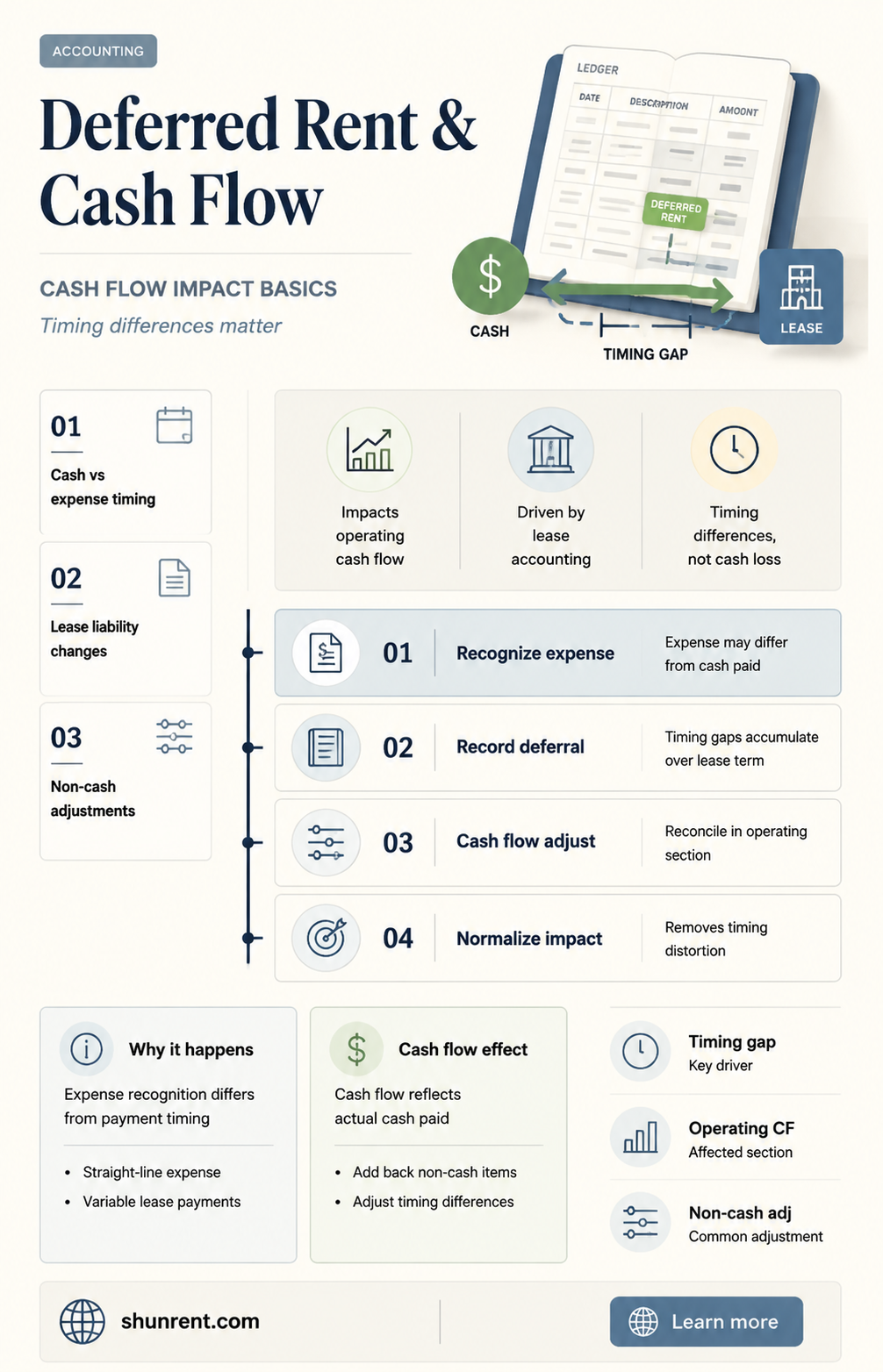

Deferred rent is a common accounting strategy used by businesses to manage expenses by spreading rent evenly over the lease term, offering financial flexibility and stability. It arises when a tenant is given free rent for a specific period, usually at the beginning of a lease agreement. This results in a discrepancy between the straight-line expense recorded and the actual cash payments made for rent. While deferred rent does not directly affect cash flow as it is a non-cash accounting adjustment, it is reflected on the lessor's balance sheet during the free rent term. This strategy helps businesses manage their cash flow by keeping cash outflow consistent throughout the lease term.

| Characteristics | Values |

|---|---|

| Definition | Deferred rent arises when a tenant is given free rent in one or more periods, usually at the beginning of a lease agreement. |

| Accounting Treatment | Deferred rent is a non-cash accounting adjustment that aligns rent expense recognition with the straight-line method rather than the timing of actual payments. |

| Impact on Cash Flow | Deferred rent does not directly affect cash flow. |

| Example | If a business rents a facility for three years with the first two months free, this results in a deferred rent situation. The tenant would charge the average monthly rental rate to expense, recognizing rent expense during any free rent periods. |

| Balance Sheet Presentation | Deferred rent is typically recorded as a liability on the balance sheet, representing the cumulative rent expense that exceeds all cash payments up to that point in time. |

Explore related products

What You'll Learn

![]()

Deferred rent is a non-cash accounting adjustment

In such cases, the tenant is supposed to charge the average monthly rental rate to expense, irrespective of the actual monthly payment made. This means that the tenant will recognize rent expense during any free rent periods. To account for the free periods in a deferred rent arrangement, the total cost of the lease for the entire period is calculated by compiling the total cost of the lease, including all free occupancy months. This amount is then divided by the total number of periods covered by the lease.

The deferred rent adjustment helps business owners manage expenses by spreading rent evenly over the lease term, offering financial flexibility and stability. It aligns rent expense recognition with the straight-line method rather than the timing of actual payments.

It is important to note that under the new lease accounting standard ASC 842, deferred rent is no longer recorded and is replaced by a Right-of-Use (ROU) Asset and Lease Liability.

Renting Commercial Spaces for Residential Purposes: Is It Legal?

You may want to see also

Explore related products

![]()

It helps businesses manage expenses

Deferred rent is a valuable tool for businesses, helping them manage expenses and providing financial relief. It is a non-cash accounting adjustment that does not directly affect cash flow. It is the outcome of a lease payment that is less than the recognised expense on financial statements. This typically occurs when a tenant is offered free or reduced-rate rent, often at the beginning of a lease as an incentive.

For example, if a business rents a facility for three years with the first two months rent-free, this results in a deferred rent situation. The business would charge the average monthly rental rate to expense, recognising rent expense during any free rent periods. So, if the monthly payment for the lease is $1,000, the total cost of the lease is $11,000. The business would divide this amount by the total number of periods covered by the lease, including the free months, and recognise this as a monthly expense.

The benefit of this system is that it spreads rent evenly over the lease term, offering financial flexibility and stability. It helps businesses manage cash flow during tough economic times, ensuring they can cover other operational costs and maintain business continuity. For instance, during periods of low revenue, deferring rent can help businesses stay afloat and manage expenses more effectively.

However, it is important to note that deferred rent is a temporary solution. Businesses should use the relief period to improve their financial stability and plan for future rent obligations. This may involve budgeting adjustments, seeking additional income sources, or implementing cost-saving measures to ensure long-term financial health.

U-Haul Light Kit Rental: Is It Necessary?

You may want to see also

Explore related products

![]()

It arises when a tenant is given free rent

Deferred rent is a liability that arises when a tenant is given free rent for a certain period, usually at the beginning of a lease agreement. For example, if a business rents a facility for three years with the first two months rent-free, this results in a deferred rent situation.

In this scenario, the tenant is required to charge the average monthly rental rate to expense, irrespective of the actual monthly payment made. This means that during the free rent period, the tenant will recognize a rent expense. To calculate this, the total cost of the lease for the entire period is divided by the total number of periods covered by the lease, including the free months. This results in a recognized monthly expense, even during the months where no payment is made. This difference between the recognized expense and the actual payment is the liability that is accounted for as deferred rent.

For example, let's consider a lease with a term of one year and agreed-upon monthly payments of $10,000. The total expense of this lease would normally be $120,000. However, if the tenant is offered three months of free rent, the total expense is reduced to $90,000. To calculate the recognized monthly expense, this total expense is divided by the number of rent periods, resulting in a recognized monthly expense of $7,500. So, during the first three rent-free months, there is still a recognized expense of $7,500, despite no payment being made. This difference of $7,500 is the deferred rent liability.

As the lease progresses and payments are made, the deferred rent balance decreases. Using the previous example, if the monthly payment is $10,000 and the recognized monthly expense is $7,500, the deferred rent balance will decrease by $2,500 every month until it reaches $0 at the end of the lease term. This reduction in the deferred rent liability continues until it is fully offset by rent payments.

It is important to note that deferred rent does not directly affect cash flow as it is a non-cash accounting adjustment. Instead, it helps businesses manage expenses by spreading rent evenly over the lease term, offering financial flexibility and stability.

Rent-to-Own Appliances: Worth the Cost?

You may want to see also

Explore related products

$2.99 $19.95

![]()

It is a liability or credit balance

Deferred rent is a liability that occurs when a tenant is given free rent, usually at the beginning of a lease agreement, or when rent payments are increasing. It is a non-cash accounting adjustment that helps businesses manage expenses by spreading rent evenly over the lease term, offering financial flexibility and stability.

In the context of accounting, the total rent expense for the entire lease term is calculated on a straight-line basis, regardless of whether individual payments differ. Any deferred rent is then treated as a liability on the balance sheet, offsetting the total rent expense. For example, if a lease agreement includes three months of free rent, the total expense of the lease would be lower, and this reduced amount would be divided by the number of months to calculate the recognised monthly expense.

In the first month of a lease, if there is no actual payment due to a free month of occupancy, the debit to expense is offset by a credit to the deferred rent account, which is a liability account. In subsequent months, the same average amount is charged to expense, and if the rent payment is higher than the expense, the difference is used to reduce the deferred rent liability. This process continues until the deferred rent liability reaches zero at the end of the lease term.

The treatment of deferred rent has evolved with new accounting standards, such as ASC 842, where deferred rent is no longer recorded separately. Instead, it is replaced by a Right-of-Use (ROU) Asset and Lease Liability, which are reduced in subsequent periods, ultimately reaching zero balances by the end of the lease. The ROU Asset represents the lessee's right to use the leased asset, while the Lease Liability reflects the present value of the lessee's obligations under the lease terms.

Company Perks: Rent Discounts for High-Performing Employees

You may want to see also

Explore related products

![]()

It is recorded in the operating cash flows

Deferred rent is a liability that arises when there is a discrepancy between the straight-line expense recorded and the cash paid for rent in a reporting period. This often occurs when a lessee is given free rent for one or more periods, typically at the beginning of a lease agreement. For example, if a business rents a facility for three years with the first two months rent-free, this results in a deferred rent situation.

In this case, the tenant is supposed to charge the average monthly rental rate to expense, irrespective of the actual monthly payment made. This means that they will recognize rent expense during any free rent periods. The total cost of the lease is divided by the total number of periods covered by the lease, including all free occupancy months. This results in an average monthly rate that is charged to expense each month, irrespective of whether there is a actual payment made in that month.

Any difference between the offsetting rent payment and the expense is charged to the deferred rent liability account. This account is used to balance the imbalance between the straight-line expense and the actual cash payments made. By the end of the lease term, the deferred rent gradually decreases to zero as the liability is reduced in consecutive periods.

Therefore, deferred rent does not directly affect cash flow as it is a non-cash accounting adjustment. However, it helps business owners manage expenses by spreading rent evenly over the lease term, offering financial flexibility and stability.

Bobby and Giada: Cooking Up Romance?

You may want to see also

Frequently asked questions

Deferred rent is a liability or credit balance that represents cumulative rent expense, where the total rent expense recognized exceeds all cash payments up to that point in time. It occurs when a tenant is given free rent in one or more periods, usually at the beginning of a lease agreement.

Deferred rent does not directly affect cash flow because it is a non-cash accounting adjustment. However, it can impact cash flow by helping businesses manage expenses, spreading rent evenly over the lease term, and offering financial flexibility and stability.

Deferred rent is reflected on the lessor's balance sheet during the free rent term. It is reported as a straight-line expenditure, with the difference between the expense and cash payment recorded in a deferred rent liability account.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61gNC08X3PL._AC_UY218_.jpg)

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![Rent: Filmed Live on Broadway [Blu-ray]](https://m.media-amazon.com/images/I/51SDxJNQfVL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)