The question of whether rent expense goes into the balance sheet is a common one in accounting, often arising from the need to understand how expenses are treated in financial statements. In reality, rent expense does not appear on the balance sheet; instead, it is recorded on the income statement as a part of the operating expenses. The balance sheet, which provides a snapshot of a company's financial position at a specific point in time, focuses on assets, liabilities, and equity, while the income statement tracks revenues and expenses over a period. Rent expense, being a cost incurred in the normal course of business, reduces net income and is therefore reflected in the income statement. However, any prepaid rent or rent payable may appear on the balance sheet under current assets or current liabilities, respectively, depending on the timing of payments and the accounting treatment applied.

| Characteristics | Values |

|---|---|

| Nature of Rent Expense | Operating expense, represents cost of using rented property or equipment |

| Financial Statement Classification | Income Statement (not Balance Sheet) |

| Timing of Recognition | Recognized in the period incurred, following the matching principle |

| Impact on Balance Sheet | No direct impact; however, prepaid rent (if any) is recorded as a current asset |

| Accounting Treatment | Expensed as incurred, reducing net income |

| Relevance to Balance Sheet | Only prepaid rent or security deposits appear as assets, not the expense itself |

| Common Misconception | Rent expense is often mistakenly thought to be a balance sheet item, but it is not |

| Related Balance Sheet Accounts | Prepaid Rent (asset), Security Deposits (asset) |

| Tax Treatment | Generally tax-deductible as a business expense |

| Reporting Standard | Follows GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards) |

Explore related products

What You'll Learn

- Rent Expense Classification: Identifying if rent is an expense or asset in financial statements

- Balance Sheet vs. Income Statement: Understanding where rent expense is recorded in accounting

- Prepaid Rent Treatment: How prepaid rent is handled on the balance sheet

- Operating Lease Impact: Effects of operating leases on balance sheet liabilities and expenses

- Accrued Rent Expense: Recording unpaid rent liabilities on the balance sheet

![]()

Rent Expense Classification: Identifying if rent is an expense or asset in financial statements

Rent expense is a fundamental component of a company’s financial statements, but its classification can be a source of confusion. At first glance, it might seem straightforward: rent is a cost, so it must be an expense. However, the treatment of rent in financial statements depends on its nature and the accounting principles applied. For instance, under accrual accounting, rent is recognized as an expense in the period it is incurred, regardless of when payment is made. This contrasts with cash-basis accounting, where rent is recorded only when paid. Understanding this distinction is crucial for accurate financial reporting.

To classify rent expense correctly, consider the purpose and duration of the rental agreement. Short-term leases, such as monthly office rentals, are typically expensed directly in the income statement. These costs are considered operational expenses because they do not provide long-term benefits beyond the rental period. For example, a tech startup renting office space for $2,000 per month would record this as a rent expense each month, reducing its net income. This approach aligns with the matching principle, which pairs expenses with the revenues they help generate.

In contrast, long-term leases or leasehold improvements may blur the line between expense and asset. Under accounting standards like ASC 842 (for U.S. GAAP) or IFRS 16, leases with terms exceeding 12 months are capitalized on the balance sheet. This means the lessee records a right-of-use asset and a lease liability, with rent expense recognized over the lease term. For instance, a retailer leasing a storefront for 10 years would capitalize the lease, spreading the expense over the lease period rather than expensing it upfront. This method reflects the economic substance of the lease as a long-term investment.

Practical tips for classifying rent expense include reviewing lease agreements to determine their term and purpose. Short-term leases (less than 12 months) are typically expensed, while longer-term leases require capitalization. Additionally, ensure compliance with relevant accounting standards, as non-compliance can lead to misstated financial statements. For example, a company failing to capitalize a long-term lease under ASC 842 would understate its assets and liabilities, distorting its financial position.

In conclusion, rent expense classification hinges on the lease’s duration and purpose. Short-term rentals are expensed directly, while long-term leases are capitalized as assets and liabilities. By understanding these nuances, businesses can ensure accurate financial reporting, providing stakeholders with a clear picture of their financial health. Always consult accounting standards and, if necessary, seek professional advice to navigate complex lease agreements effectively.

Rent Regulated vs. Rent Stabilized: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Balance Sheet vs. Income Statement: Understanding where rent expense is recorded in accounting

Rent expense is a fundamental component of a company’s financial operations, but its treatment in accounting often sparks confusion. Unlike assets or liabilities, rent expense does not appear on the balance sheet. Instead, it is recorded on the income statement, where it directly impacts a company’s profitability. This distinction is critical because the balance sheet reflects a snapshot of a company’s financial position at a specific point in time, while the income statement tracks revenue and expenses over a period. Rent expense, being a cost incurred to generate revenue, belongs in the latter.

To illustrate, consider a retail business leasing a storefront. The monthly rent payment is an operating expense that reduces net income. On the income statement, it appears under operating expenses, alongside items like utilities and salaries. However, the balance sheet will show the prepaid rent (if any) as a current asset or the lease liability under long-term obligations, depending on the accounting standards (e.g., ASC 842 or IFRS 16). This separation ensures clarity between ongoing costs and long-term financial commitments.

A common misconception arises when prepayments are involved. If a company pays rent in advance, the prepaid portion is recorded as an asset on the balance sheet until the rent period begins. Once the rental period starts, the expense is recognized on the income statement, and the prepaid asset is reduced. For example, if a company prepays $12,000 for a year’s rent, $1,000 is expensed monthly, while the remaining prepaid balance decreases accordingly. This process highlights the interplay between the two financial statements.

Understanding this distinction is crucial for accurate financial analysis. Investors and stakeholders rely on the income statement to assess operational efficiency, while the balance sheet provides insight into liquidity and solvency. Misclassifying rent expense could distort profitability metrics or misrepresent a company’s financial health. For instance, recording rent as a liability on the balance sheet without expensing it would overstate net income and understate current assets.

In practice, accountants must adhere to accrual accounting principles, ensuring expenses are matched to the period in which they are incurred. For rent, this means recognizing the expense as it relates to the period, regardless of payment timing. For example, if rent is paid quarterly but covers monthly usage, the expense is allocated monthly on the income statement. This approach maintains consistency and accuracy in financial reporting, reinforcing the clear separation between the balance sheet and income statement.

Renting E-Scooters in Portland, Oregon: A Complete Guide

You may want to see also

Explore related products

![]()

Prepaid Rent Treatment: How prepaid rent is handled on the balance sheet

Prepaid rent represents a unique accounting challenge, as it straddles the line between an expense and an asset. When a business pays rent in advance, it doesn’t immediately recognize the full payment as an expense. Instead, it records the prepaid portion as a current asset on the balance sheet. This treatment aligns with the matching principle, which requires expenses to be recognized in the period they are incurred, not when they are paid. For example, if a company pays $12,000 for a year’s rent in January, only $1,000 is expensed monthly, while the remaining $11,000 is listed as prepaid rent on the balance sheet.

The balance sheet classification of prepaid rent is straightforward: it falls under current assets because it is expected to be consumed within one year or the operating cycle, whichever is longer. This categorization ensures that the financial statement accurately reflects the company’s short-term resources. However, the treatment shifts as time progresses. Each month, a portion of the prepaid rent is transferred from the asset account to the rent expense account on the income statement. This adjustment is typically done through an amortization schedule, ensuring a systematic and rational allocation of the prepaid amount over the rental period.

One critical aspect of prepaid rent treatment is its impact on financial ratios. Since prepaid rent is an asset, it contributes to metrics like the current ratio and working capital. For instance, a company with significant prepaid rent may appear more liquid than it actually is, as this asset cannot be readily converted into cash. Analysts and stakeholders must therefore scrutinize the composition of current assets to avoid misinterpretation. Additionally, the gradual expensing of prepaid rent smooths out income statement volatility, providing a more accurate representation of periodic performance.

Practical tips for handling prepaid rent include maintaining detailed records of lease agreements and payment schedules. Companies should also reconcile their prepaid rent accounts monthly to ensure accuracy and compliance with accounting standards. For small businesses or startups, using accounting software with automated amortization features can streamline this process. Finally, it’s essential to distinguish prepaid rent from security deposits. While both involve upfront payments, security deposits are typically liabilities for the landlord and do not affect the tenant’s balance sheet unless forfeited.

In conclusion, prepaid rent treatment on the balance sheet is a nuanced process that balances asset recognition with expense allocation. By understanding its mechanics, businesses can ensure financial statements accurately reflect their financial position and performance. Proper handling of prepaid rent not only adheres to accounting principles but also enhances transparency and decision-making for internal and external stakeholders.

Liability Insurance: Renting and Coverage

You may want to see also

Explore related products

![]()

Operating Lease Impact: Effects of operating leases on balance sheet liabilities and expenses

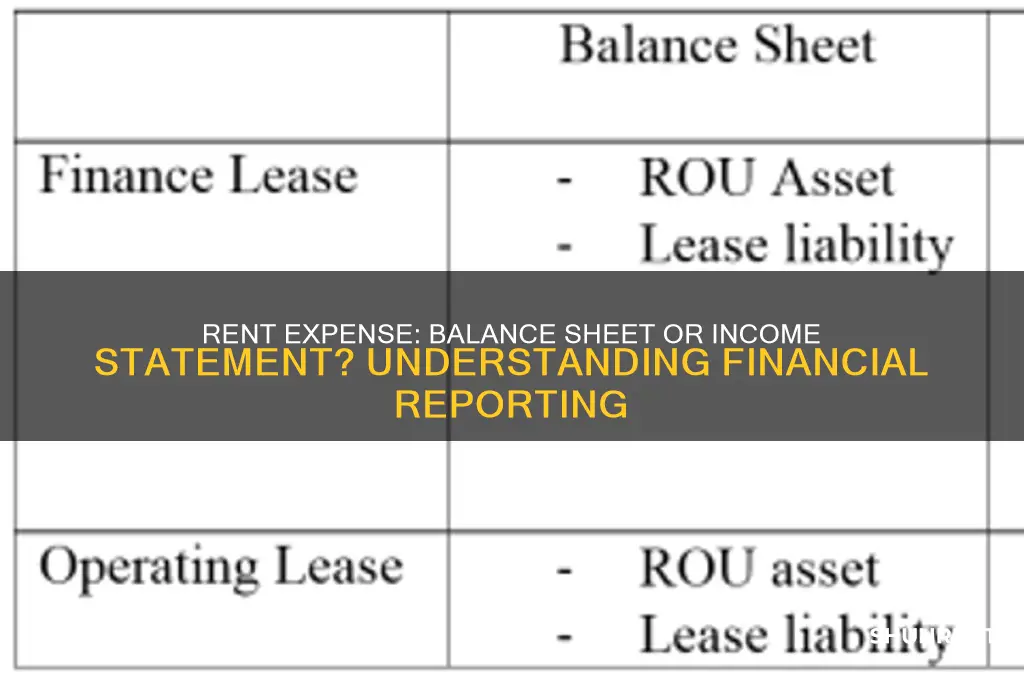

Rent expense, a common operating cost for businesses, does not directly appear on the balance sheet under traditional accounting standards. Instead, it is recognized on the income statement as a periodic expense. However, the introduction of operating leases under accounting standards like ASC 842 (for U.S. GAAP) and IFRS 16 has changed this dynamic. Operating leases, which were previously off-balance-sheet transactions, now require lessees to recognize a right-of-use (ROU) asset and a corresponding lease liability on their balance sheets. This shift has significant implications for financial reporting and analysis.

The impact of operating leases on the balance sheet is twofold. First, the recognition of an ROU asset increases the total assets of the company, reflecting the lessee’s right to use the leased asset over the lease term. Second, the lease liability represents the present value of future lease payments, increasing the company’s total liabilities. For example, a 10-year office lease with annual payments of $50,000 and a discount rate of 5% would result in an initial lease liability of approximately $386,000. This liability is then amortized over the lease term, with the interest portion recorded as lease expense on the income statement.

From an analytical perspective, the inclusion of operating leases on the balance sheet provides a more comprehensive view of a company’s financial obligations. Investors and creditors can now assess the long-term financial commitments associated with leases, which were previously hidden. For instance, a retail company with numerous store leases will show a substantial increase in liabilities, reflecting its reliance on leased properties. This transparency allows stakeholders to better evaluate the company’s leverage and liquidity risk.

However, the transition to recognizing operating leases on the balance sheet is not without challenges. Companies must carefully calculate the present value of lease payments, select an appropriate discount rate, and reassess lease terms for embedded options or extensions. Missteps in these calculations can lead to material misstatements. Additionally, the increased liabilities may affect financial ratios such as debt-to-equity, potentially impacting borrowing costs or covenant compliance.

In conclusion, the effects of operating leases on the balance sheet are profound, enhancing transparency but also introducing complexity. Companies must adapt their accounting processes and financial analysis to accurately reflect these changes. For stakeholders, understanding the nuances of lease accounting is essential to interpreting financial statements and assessing a company’s true financial health. By recognizing both the ROU asset and lease liability, operating leases now play a central role in shaping the balance sheet and, by extension, the narrative of a company’s financial position.

Where to Rent Helium Tanks for Balloon Filling Near You

You may want to see also

Explore related products

![]()

Accrued Rent Expense: Recording unpaid rent liabilities on the balance sheet

Rent expense typically flows through the income statement, reflecting the cost of occupying a property over a specific period. However, when rent remains unpaid at the end of an accounting period, it transforms into a liability that must be recorded on the balance sheet. This is where accrued rent expense comes into play, ensuring financial statements accurately represent a company’s obligations. Accrued rent expense arises when a business has incurred rent costs for a period but has not yet paid the landlord. This scenario is common in accrual accounting, where transactions are recorded when they occur, not when cash changes hands.

Recording accrued rent expense involves a two-step process. First, recognize the rent expense in the income statement for the period it pertains to, adhering to the matching principle. Simultaneously, record the unpaid rent as a current liability on the balance sheet. For example, if a company occupies a property from December 1 to December 31 but pays rent on January 1, the December rent expense is accrued in December. The journal entry would debit rent expense and credit accrued rent payable. This ensures the financial statements reflect the true financial position and performance of the company during the reporting period.

The treatment of accrued rent expense highlights a critical distinction between cash-basis and accrual-basis accounting. In cash-basis accounting, rent expense is recorded only when payment is made, which can distort financial reporting if payments and usage periods misalign. Accrual accounting, on the other hand, provides a more accurate picture by matching expenses with the period in which they are incurred. For instance, a retail store occupying a space in December but paying rent in January would misrepresent its December profitability under cash-basis accounting. Accruing the rent expense ensures December’s financial statements reflect the true cost of operations.

Practical tips for managing accrued rent expense include maintaining a rent schedule that aligns lease terms with accounting periods and reconciling this schedule regularly. Automating accrual calculations through accounting software can reduce errors and save time, especially for businesses with multiple leases. Additionally, ensure lease agreements clearly define payment terms and due dates to avoid discrepancies. For small businesses, tracking accrued rent manually in a spreadsheet can suffice, but larger entities should integrate this process into their ERP systems for efficiency and accuracy.

In conclusion, accrued rent expense is a vital component of financial reporting, bridging the gap between cash payments and the actual usage of rented property. By recording unpaid rent liabilities on the balance sheet, companies uphold the principles of accrual accounting, providing stakeholders with a transparent and accurate view of their financial health. Proper management of accrued rent expense not only ensures compliance with accounting standards but also enhances the reliability of financial statements, fostering trust among investors, creditors, and management.

California Rent Control: New Bill Limits Hikes

You may want to see also

Frequently asked questions

No, rent expense does not go into the balance sheet. It is recorded on the income statement as an operating expense.

Rent expense is recorded on the income statement under operating expenses, as it represents the cost of using a property for business operations.

Rent expense is not included in the balance sheet because it is an expense that reduces net income and does not represent an asset, liability, or equity.

Rent expense indirectly affects the balance sheet by reducing retained earnings (a component of equity) when it is deducted from revenue on the income statement.

Yes, prepaid rent is recorded on the balance sheet as a current asset, as it represents rent paid in advance for future periods.