Whether you're a homeowner or a renter, your housing payment is considered a necessary expense and is included in your debt-to-income ratio (DTI). Lenders use this ratio to determine whether to grant you credit and how much. The DTI compares your monthly debt payments to your income, and lenders assess it when evaluating your financial ability to take on a new loan. The front-end ratio compares your monthly housing expenses to your gross monthly income, while the back-end ratio includes other monthly obligations like credit card payments, student loans, vehicle loans, and alimony. If you're a renter, your monthly rent is typically included in your front-end ratio, and if you're an investor with rental income, it can be counted as income after appearing on your tax returns for a certain period.

| Characteristics | Values |

|---|---|

| Definition | Debt-to-income (DTI) ratio is a calculation that compares what you earn to what you owe. |

| Purpose | Lenders use the DTI ratio to decide whether to grant credit and how much. |

| Calculation | DTI is calculated by dividing your monthly debt payments by your gross monthly income before taxes. |

| Components | DTI includes monthly housing costs, mortgage principal and interest, property taxes, insurance, credit card payments, student loans, vehicle loans, and alimony or child support obligations. |

| Impact of Rent | Rent affects the DTI ratio as it is considered a necessary expense. It is included in the calculation as a monthly housing cost. |

| Rental Property Ownership | Rental property ownership impacts the DTI ratio by affecting both the debt and revenue components. The net income or debt for the property is added to one side of the ratio. |

| Solutions to High DTI | High DTI ratios can be improved by increasing income, paying off debt, or finding more lenient lenders. |

Explore related products

What You'll Learn

![]()

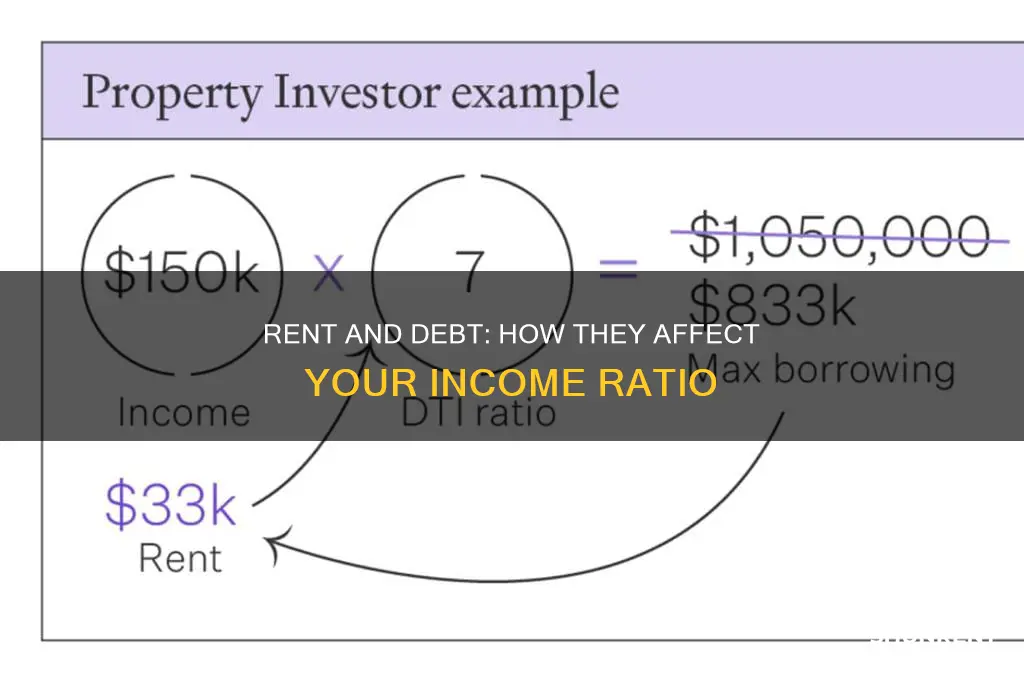

Rental income and debt

When applying for a loan, your debt-to-income (DTI) ratio is a crucial calculation that lenders use to assess whether to grant you credit and how much. The DTI compares your monthly debt payments to your income. Lenders often distinguish between borrower front-end and back-end ratios. The front-end ratio compares a person's monthly rental expenses to their gross monthly income. The back-end ratio adds other monthly obligations to the total, such as credit card payments, student loans, vehicle loans, and alimony or child support obligations.

If you are renting a property, your monthly rent is typically included in your debt-to-income ratio. Your housing payment is considered a necessary expense, even if you rent. If you have signed a lease for a property, you are committed to paying the rent each month, similar to a mortgage or student loan payment.

If you own a rental property, the net income or debt for the property is added to one side of the ratio or the other. If the property cash flows, the mortgage on that property does not count on the debt side of your debt-to-income ratio. The income portion typically does not include anticipated bonuses or overtime payments.

Different lenders may use different methods to calculate the DTI. Some lenders may not count rental property profits until they show up on your taxes, while others may count 75% of it if you are an experienced investor. Lenders may also consider the depreciation of investment properties when determining your loan amount and count it against you.

To reduce the impact of a high debt-to-income ratio, you can make a larger down payment, improve your credit score, pay down debt, or increase your income.

Rent-to-Own Appliances: What You Need to Know

You may want to see also

Explore related products

![]()

Lender's calculations

Lenders use your debt-to-income ratio (DTI) to determine the risk associated with you taking on another payment. The DTI compares how much you owe each month to how much you earn. It is calculated by dividing your monthly debt payments by your monthly gross income (before taxes). The lower the DTI, the less risky you are to lenders.

Lenders may calculate two different ratios: the housing to income ratio (HTI) and the back-end DTI. The HTI equals the sum of your monthly housing payment (including mortgage, insurance, homeowners' association fees, and property taxes) divided by your current income. The back-end DTI consists of your monthly housing payment plus all other monthly debt, such as credit card bills, student loans, auto payments, and possibly alimony or child support payments.

The ideal front-end ratio (HTI) should be no more than 28%, and the ideal back-end ratio should be no more than 36%. However, lenders can and do accept higher ratios, especially if you have other "compensating factors" such as a bigger down payment or a high credit score.

When it comes to rental properties, the financial impact of your investment property affects both sides of the DTI calculation. The mortgage obligation contributes to your debt expenses, and the rental income is partially eligible for inclusion. Typically, lenders will calculate income using only 75% of the average rent. This is because the other 25% accounts for things like vacancy, management, maintenance, and capex. However, some lenders may not count rental income until it shows up on your taxes, while others may count 75% of it if you're an experienced investor.

In summary, lenders use the DTI ratio to assess your ability to take on additional debt. They consider both your monthly debt payments and your monthly income, including rental income and expenses if applicable. The ideal ratios are below 28% for the front-end and below 36% for the back-end, but higher ratios may be accepted depending on other factors.

U-Haul Rentals: Do You Need Extra Insurance Coverage?

You may want to see also

Explore related products

![]()

DTI ratio and credit

Your debt-to-income (DTI) ratio is an important metric that lenders use to determine your eligibility for a loan or credit card. It is calculated by dividing your total monthly debt payments by your gross monthly income (before taxes and deductions). This ratio is expressed as a percentage, and a lower DTI indicates less risk to lenders.

When calculating your DTI ratio, lenders consider various factors, including mortgage or rental payments, credit card debt, student loans, vehicle loans, and other personal loans. For rental properties, lenders may consider up to 75% of the market rate of rent as income, although this can vary. It's important to note that expenses like groceries, utilities, and gas are generally not included in the calculation.

A high DTI ratio can negatively impact your ability to obtain credit or loans. Lenders typically prefer a DTI ratio of 35% or lower, and a ratio above 50% may significantly limit your credit options. However, it's worth noting that different lenders have different thresholds, and some may approve loans with higher DTIs under certain circumstances. Improving your credit score can also help compensate for a higher DTI ratio.

To improve your DTI ratio, you can focus on reducing your debt or increasing your income. This can be achieved by paying off debts with the highest interest rates, avoiding unnecessary debt, or exploring options to increase your earnings. Additionally, if rental properties are a small portion of your financial picture, you may want to consider refinancing at lower interest rates or improving the property to increase its income potential.

While your DTI ratio does not directly affect your credit score, it is an important factor in assessing your overall financial health and eligibility for credit. Lenders use this ratio to evaluate the risk associated with lending you money and determining your ability to make loan payments and repay debt. Therefore, maintaining a favourable DTI ratio is crucial when seeking credit or loan approvals.

Barbados Jeep Rental: Is it a Must?

You may want to see also

Explore related products

![]()

Reducing debt-to-income ratio

Debt-to-income ratio (DTI) is a crucial calculation used by lenders to decide whether to grant credit to an individual and how much. It compares an individual's monthly debt payments to their monthly gross income. A low DTI indicates that a person has a lot of leftover funds after paying what they owe each month, while a high DTI indicates that a person may struggle financially if they borrow more money.

If your DTI is higher than 36%, you may want to take steps to reduce it. Here are some ways to do so:

- Make a plan for paying off your credit cards.

- Increase the amount you pay monthly toward your debts. Extra payments can help lower your overall debt more quickly.

- Ask creditors to reduce your interest rate, which would lead to savings that you could use to pay down debt.

- Avoid taking on more debt.

- Increase your income with a new job, pay increase, side hustle, or by joining the gig economy or freelancing.

- Refinance existing loans to lower your monthly payments. You can reduce your monthly financial obligations by securing a lower interest rate or extending the loan term.

- Consolidate high-interest debts into a single, lower-interest loan to simplify your payments and provide more financial flexibility.

- Make a larger down payment.

- Improve your credit score.

Website Ownership: Renting vs Owning

You may want to see also

Explore related products

![]()

Front-end and back-end ratios

The debt-to-income (DTI) ratio is a crucial calculation used by lenders to assess an individual's ability to repay a loan and how much credit they can be granted. This ratio compares what a person earns to what they owe. Lenders distinguish between the borrower's front-end and back-end ratios.

The front-end ratio compares a borrower's monthly mortgage or rental expenses to their gross monthly income. It reflects the percentage of monthly gross income that comprises expected monthly housing expenses. The front-end ratio includes not only rental or mortgage payments but also other costs associated with housing, like insurance, property taxes, and HOA fees. It is calculated by dividing total monthly housing costs by monthly gross income. A front-end ratio of 28% is a common upper limit imposed by mortgage companies, though some may allow a higher ratio if the borrower has other positive factors, such as good credit or reliable income.

The back-end ratio, also known as the DTI ratio, measures the percentage of a borrower's gross monthly income used to pay total monthly debt obligations. It includes all monthly debt obligations, such as credit card payments, student loans, vehicle loans, alimony, and child support, in addition to total housing expenses. The back-end ratio is calculated by dividing total monthly debt expenses by gross monthly income and multiplying by 100. Lenders typically prefer a back-end ratio of no more than 33% to 36%, though some may allow up to 50% for borrowers with good credit.

Both the front-end and back-end ratios are used by lenders to assess the borrower's risk and determine their ability to repay a home mortgage loan. A higher DTI indicates that the borrower may be financially stretched, while a lower DTI suggests higher monthly disposable income.

Rent Assistance in Wisconsin: How to Apply

You may want to see also

Frequently asked questions

Debt-to-income ratio (DTI) is a calculation that compares what you earn to what you owe. Lenders use this ratio to decide whether to grant you credit and how much.

Calculate your DTI by dividing your total monthly debt payments by your gross monthly income (before taxes). The result will be a percentage.

Yes, your monthly rent is typically included in your debt-to-income ratio. Your housing payment is considered a necessary expense, even if you rent.

Rental income is counted as income, but only after it shows up on your taxes. Some lenders may consider 75% of the market rate of rent.

You can improve your DTI by paying off existing debt, increasing your income, or purchasing a lower-priced home.