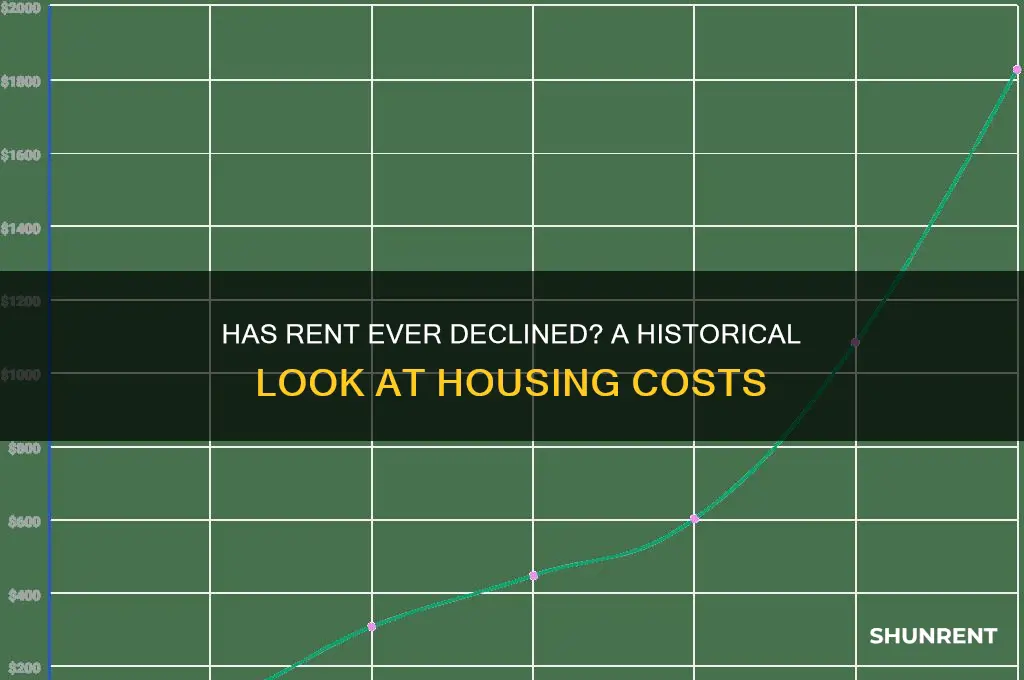

Throughout history, rent prices have fluctuated in response to economic, social, and political factors, but instances of significant or sustained rent decreases are relatively rare. Typically, rent trends upward due to population growth, urbanization, and inflation, with occasional dips during economic crises, wars, or periods of oversupply. For example, the Great Depression in the 1930s saw rent declines as unemployment soared and demand plummeted, while more recently, the COVID-19 pandemic caused temporary rent reductions in some cities due to remote work and migration patterns. However, such decreases are often localized and short-lived, as landlords and markets adjust to new conditions. Examining these historical exceptions provides insight into the complex dynamics that influence housing costs and the rarity of rent declines in the broader arc of history.

| Characteristics | Values |

|---|---|

| Historical Rent Trends | Rent has decreased in specific periods, such as during the Great Depression (1930s), post-WWII housing boom (1950s), and the 2008 financial crisis in some U.S. cities. |

| Global Examples | Rent declines in Tokyo (1990s-2000s), Dublin (post-2008), and San Francisco (2020-2021 due to remote work). |

| Causes of Rent Decline | Economic recessions, oversupply of housing, population decline, and shifts in demand (e.g., remote work). |

| Duration of Declines | Typically short-term (1-3 years) unless tied to prolonged economic stagnation or structural changes. |

| Regional Variations | Rent decreases are localized, not universal, depending on market conditions and external factors. |

| Post-Decline Recovery | Rents often rebound as economies recover, demand increases, or supply constraints re-emerge. |

| Recent Trends (2020-2023) | Pandemic-driven rent drops in urban centers (e.g., NYC, SF) reversed by 2022-2023 due to inflation and demand recovery. |

| Policy Impact | Rent control or stabilization policies can artificially suppress rent increases but rarely cause declines. |

| Long-Term Trend | Historically, rents rise with inflation and population growth, with declines being exceptions. |

Explore related products

What You'll Learn

![]()

Historical rent trends during economic recessions

Economic recessions often bring a paradoxical shift in rent trends, challenging the assumption that housing costs always rise. During the Great Recession of 2008, for instance, U.S. rents declined in many metropolitan areas as unemployment soared and homeownership became less attainable. Cities like Phoenix and Miami saw rent reductions of up to 10%, as landlords struggled to fill vacancies in a shrinking job market. This pattern illustrates how recessions can temporarily reverse the upward trajectory of rents, particularly in regions heavily reliant on cyclical industries like finance or construction.

Analyzing these trends reveals a critical interplay between supply, demand, and economic conditions. In recessions, reduced consumer spending and job losses decrease demand for rental housing, while foreclosures often increase the supply of available units as homeowners transition to renting. For example, during the early 1990s recession, rent growth slowed significantly in California due to aerospace industry layoffs, which disproportionately affected high-income renters. Landlords, facing higher vacancy rates, were forced to lower rents or offer incentives like free parking or reduced security deposits to attract tenants.

However, not all recessions lead to uniform rent declines. The COVID-19 recession of 2020 highlighted regional disparities, with rents plummeting in urban centers like San Francisco and New York City as remote work enabled migration to lower-cost areas. Conversely, suburban and Sun Belt markets experienced rent increases due to heightened demand. This underscores the importance of local economic factors, such as industry composition and population mobility, in shaping rent trends during downturns.

Practical takeaways for renters and landlords emerge from these historical patterns. For renters, recessions may present opportunities to negotiate lower rents or secure better lease terms, particularly in oversupplied markets. Landlords, meanwhile, should focus on retaining existing tenants through flexible terms or modest rent reductions, as turnover costs often exceed the benefits of holding out for higher rents. Monitoring local economic indicators, such as unemployment rates and job growth, can provide early signals of shifting rent dynamics during a recession.

In conclusion, while rent declines during recessions are not universal, they are a recurring phenomenon tied to specific economic and regional conditions. Understanding these trends empowers both renters and landlords to make informed decisions, mitigating risks and capitalizing on opportunities in uncertain times. Historical data serves as a valuable guide, but adaptability to local market nuances remains key.

Audiobooks: Rent or Keep? Amazon's Audiobook Options Explored

You may want to see also

Explore related products

![]()

Impact of housing oversupply on rental prices

Housing oversupply occurs when the number of available units exceeds demand, often leading to a downward pressure on rental prices. Historically, this phenomenon has been observed in various markets, such as post-2008 Dublin, where a surge in construction following the housing bubble collapse resulted in a 20% rent decrease between 2007 and 2010. Similarly, Houston in the 1980s experienced a 15% rent decline after an oil industry downturn left thousands of newly built apartments vacant. These examples illustrate that oversupply can indeed cause rents to drop, but the magnitude and duration depend on local economic conditions and the extent of the imbalance.

To understand the impact of oversupply, consider it as a supply-demand equation. When supply outstrips demand, landlords compete for tenants by lowering rents or offering incentives like free months or reduced deposits. For instance, in 2019, San Francisco’s luxury apartment market saw a 10% rent reduction after a wave of high-end developments saturated the area. Tenants benefited from this oversupply, securing better deals in a previously competitive market. However, this dynamic is temporary unless demand increases or supply is absorbed through population growth or economic recovery.

While oversupply benefits renters in the short term, it poses risks for developers and investors. Prolonged rent declines can lead to reduced property values, lower returns on investment, and even foreclosures. For example, Spain’s 2008 housing crisis saw rents drop by 30% in some regions, exacerbating financial strain on landlords and banks. To mitigate this, policymakers can incentivize affordable housing conversions or impose moratoriums on new construction, as seen in cities like Vancouver and Sydney. Renters should monitor oversupply trends to capitalize on lower prices, while investors must conduct thorough market research to avoid overexposure.

Comparatively, oversupply’s impact varies across housing types. High-end markets are more susceptible to rent declines because their demand is often tied to economic prosperity. In contrast, affordable housing remains relatively stable due to consistent demand from lower-income households. For instance, during the 2020 pandemic, rents for luxury apartments in New York City fell by 15%, while those for budget units remained flat. This disparity highlights the importance of segment-specific analysis when assessing oversupply’s effects.

In conclusion, housing oversupply is a proven catalyst for rent reductions, as evidenced by historical examples and market dynamics. Renters can leverage this trend to secure better deals, but stakeholders must navigate its risks through strategic planning and policy intervention. By understanding oversupply’s mechanisms and variability, individuals and institutions can adapt to shifting housing landscapes effectively.

Top Profitable Rental Ideas: Maximize Earnings with Smart Assets

You may want to see also

Explore related products

![]()

Rent control policies and their effects

Rent control policies, designed to cap rental prices and protect tenants from steep increases, have been implemented in various cities worldwide, from New York to Berlin. While their intent is noble—to ensure affordable housing for low- and middle-income residents—their effects are often complex and multifaceted. Proponents argue that rent control stabilizes communities by preventing displacement, while critics claim it reduces housing supply and leads to property deterioration. To understand whether rent has ever gone down in history, examining the impact of these policies is essential.

Consider the case of San Francisco, a city with some of the strictest rent control laws in the U.S. While these measures have provided relief for long-term tenants, they have also discouraged new construction and incentivized landlords to convert rental units into condos or Airbnb listings. The result? A shrinking rental market and skyrocketing prices for uncontrolled units. This paradox highlights a critical issue: rent control can temporarily lower costs for some but may exacerbate affordability for others. For instance, a 2019 study by Stanford researchers found that San Francisco’s rent control policies reduced tenant mobility but also decreased the overall housing supply by 15%.

To implement rent control effectively, policymakers must balance tenant protection with incentives for landlords and developers. One approach is to pair rent control with subsidies or tax breaks for property owners, ensuring they can maintain their buildings without passing costs onto tenants. For example, Vienna, Austria, has successfully managed rent control by investing heavily in public housing, which accounts for 60% of the city’s housing stock. This dual strategy keeps rents affordable while maintaining a healthy supply of quality housing.

However, rent control is not a one-size-fits-all solution. In cities with rapidly growing populations, such as Seattle, rent control has been criticized for stifling new development. Developers, facing capped returns on investment, may opt to build luxury condos instead of affordable rentals. To mitigate this, cities could adopt hybrid models, such as rent stabilization, which allows for modest annual increases tied to inflation. This approach ensures predictability for tenants while preserving incentives for landlords.

Ultimately, the question of whether rent has ever gone down in history is tied to the broader context of housing policies and market dynamics. Rent control can be a powerful tool for affordability, but its success depends on careful design and complementary measures. For individuals navigating rent-controlled markets, practical tips include researching local laws, understanding lease terms, and advocating for policies that address both supply and demand. While rent control alone cannot solve the housing crisis, it can be part of a comprehensive strategy to make cities more livable for all.

Top Locations to Rent the Freelancer MAX in Star Citizen

You may want to see also

Explore related products

![]()

Post-war periods and rent fluctuations

Post-war periods often serve as critical junctures for rent fluctuations, shaped by the interplay of economic recovery, population shifts, and government policies. After World War II, for instance, the United States experienced a housing boom as returning soldiers and their families sought homes, driving rents upward due to high demand and limited supply. However, in contrast, post-war Japan saw rents stabilize and even decline in some areas during the 1950s, as rapid reconstruction efforts outpaced population growth, creating a surplus of housing. These examples highlight how the pace of rebuilding and demographic changes can dictate rent trends in the aftermath of conflict.

To understand rent behavior post-war, consider the role of government intervention. In the UK following World War II, rent controls were implemented to protect tenants from skyrocketing costs amid housing shortages. While this initially stabilized rents, it also discouraged new construction, leading to long-term housing deficits. Conversely, post-war Germany adopted a more market-oriented approach, incentivizing private investment in housing, which helped prevent rent spikes by increasing supply. These contrasting policies demonstrate how regulatory decisions can either mitigate or exacerbate rent fluctuations during recovery periods.

A comparative analysis of post-war rent trends reveals that the presence of economic stimulus plays a pivotal role. In the 1990s, post-Cold War Eastern Europe saw rents rise sharply as economies transitioned to capitalism and foreign investment poured in, yet this was often accompanied by gentrification and displacement. Meanwhile, in post-war South Korea, government-led industrialization and housing projects kept rents relatively affordable, even as urban populations surged. This underscores the importance of aligning economic growth with inclusive housing strategies to prevent rent volatility.

Practical takeaways for policymakers and investors include prioritizing rapid, affordable housing construction and avoiding overly restrictive rent controls that stifle supply. For instance, modular housing and public-private partnerships can accelerate post-war rebuilding, as seen in post-earthquake Christchurch, New Zealand, where rents remained stable due to swift housing solutions. Additionally, monitoring migration patterns and investing in infrastructure in growing areas can preempt rent spikes. By learning from historical post-war periods, stakeholders can navigate future crises with strategies that balance demand and supply, ensuring housing remains accessible.

Is Rent-A-Center Open or Closed on Memorial Day?

You may want to see also

Explore related products

![]()

Technological advancements reducing housing costs

Rent has historically been a one-way street: upward. However, technological advancements are carving out exceptions, offering a glimmer of hope for affordability. Consider 3D printing, a disruptive force in construction. Companies like ICON are already printing homes in under 24 hours at a fraction of traditional costs. This isn't science fiction; it's happening now, with projects like the world's first 3D-printed neighborhood in Mexico, where homes cost as little as $4,000. As the technology matures and scales, we could see a significant reduction in construction costs, potentially trickling down to rental prices.

Imagine a future where modular construction, another tech-driven innovation, becomes the norm. These prefabricated units, assembled on-site like Lego blocks, slash construction time and waste. Companies like Katerra were pioneers in this space, demonstrating how streamlined processes can drive down costs. While Katerra faced challenges, the concept remains viable, and other players are stepping in to refine the model. If widely adopted, modular construction could make housing development more efficient and affordable, easing the pressure on rental markets.

The impact of technology extends beyond construction methods. Smart home systems, powered by AI and IoT, are optimizing energy usage and maintenance, reducing operational costs for landlords. These savings, if passed on, could translate to lower rents. For instance, Nest thermostats can cut energy bills by up to 12%, while predictive maintenance tools minimize costly repairs. Tenants benefit from lower utility bills, and landlords from reduced overhead, creating a win-win scenario that could stabilize or even lower rental prices over time.

However, technology alone isn't a silver bullet. Regulatory barriers, such as zoning laws and building codes, often stifle innovation. Policymakers must adapt to enable these advancements to reach their full potential. For example, cities could incentivize 3D-printed or modular housing projects through tax breaks or expedited permits. Without such support, technological solutions risk remaining niche, failing to make a dent in the broader housing affordability crisis.

In conclusion, while rent has rarely gone down in history, technological advancements offer a promising pathway to change this trajectory. From 3D printing to smart home systems, innovation is driving down costs at every stage of housing development and management. Yet, realizing this potential requires collaboration between tech pioneers, policymakers, and the housing industry. The question isn't whether technology can reduce housing costs—it's whether we'll harness it effectively to make rent more affordable for all.

Renting Scooters in Mesa, AZ: A Quick and Easy Guide

You may want to see also

Frequently asked questions

Yes, rent has decreased in certain periods and locations due to economic downturns, oversupply of housing, or shifts in population. For example, during the Great Depression in the 1930s, rents fell significantly in many U.S. cities as unemployment soared and demand for housing dropped.

Rent decreases are typically caused by factors such as a weak economy, high vacancy rates, decreased demand for housing, or government interventions like rent control. Natural disasters or population migration away from an area can also lead to lower rents.

Yes, during the COVID-19 pandemic, rents declined in many major cities as remote work allowed people to move to more affordable areas, and economic uncertainty reduced demand for urban housing. For instance, cities like San Francisco and New York saw notable rent decreases in 2020 and 2021.