Rent and interest income play significant roles in macroeconomics as key components of national income and factors influencing economic behavior. Rent, typically derived from the use of land, property, or natural resources, represents a return on ownership and is a critical element in the distribution of income within an economy. Interest, on the other hand, is the income earned from lending capital, reflecting the cost of borrowing and the return on savings. Together, these income streams contribute to the overall income flow in an economy, affecting consumption, investment, and savings patterns. In macroeconomic analysis, understanding how rent and interest income are generated, distributed, and utilized is essential for assessing economic stability, wealth inequality, and the efficiency of resource allocation. Additionally, policies related to taxation, monetary regulation, and property rights often target these income sources to achieve broader economic objectives, such as stimulating growth or reducing disparities. Thus, rent and interest income are not only fundamental to individual financial well-being but also integral to the functioning and policy framework of macroeconomic systems.

| Characteristics | Values |

|---|---|

| Definition of Rent Income | Payment received by landowners for the use of their land or property. |

| Definition of Interest Income | Payment received by lenders for the use of their money (capital). |

| Factor of Production | Rent: Land; Interest: Capital |

| Source | Rent: Land ownership; Interest: Lending or investing capital. |

| Role in Macroeconomics | Both are components of national income (GDP) under the income approach. |

| Determinants | Rent: Demand for land, location; Interest: Interest rates, credit demand. |

| Tax Treatment | Both are typically taxable as passive income in most economies. |

| Impact on Investment | High rent may reduce investment in land; high interest may reduce borrowing. |

| Elasticity | Rent: Inelastic (land supply fixed); Interest: Elastic (capital supply adjustable). |

| Global Trends (Latest Data) | Rent: Rising in urban areas (e.g., 5-10% YoY in major cities); Interest: Fluctuating with central bank rates (e.g., 4-5% in 2023). |

| Inflation Sensitivity | Rent: Often increases with inflation; Interest: Real interest rates adjust for inflation. |

| Policy Influence | Rent: Controlled by housing policies; Interest: Controlled by monetary policy. |

Explore related products

$54.99 $54.99

What You'll Learn

- Rent as Factor Payment: Compensation for land use in production, reflecting scarcity and demand in macroeconomics

- Interest as Opportunity Cost: Payment for borrowing funds, balancing current consumption vs. future investment

- Rent in Housing Markets: Macroeconomic impacts of housing supply, demand, and price inflation

- Interest Rates and Investment: How interest rates influence capital investment and economic growth

- Rent-Seeking Behavior: Economic inefficiencies from competing for existing wealth rather than creating new value

![]()

Rent as Factor Payment: Compensation for land use in production, reflecting scarcity and demand in macroeconomics

In macroeconomics, rent serves as a critical factor payment, compensating landowners for the use of their land in production processes. This payment is not arbitrary; it is deeply rooted in the principles of scarcity and demand. Land, unlike other factors of production such as labor or capital, is finite and immobile. Its fixed supply means that as demand for land increases—whether for residential, commercial, or industrial purposes—the price to use it, or rent, rises accordingly. This dynamic highlights rent as a reflection of economic forces rather than a mere cost of doing business.

Consider the example of urban real estate markets. In cities like New York or Tokyo, where demand for space is exceptionally high, rents soar to levels that might seem disproportionate to the physical attributes of the land itself. This phenomenon is not a failure of the market but a signal of the land’s economic value. Rent in these cases acts as a price mechanism, allocating scarce land resources to their highest-valued uses. For instance, a plot of land in Manhattan might be used for a skyscraper instead of a parking lot because the rent reflects the greater economic contribution of the former.

Analytically, rent as a factor payment can be understood through the lens of marginal productivity theory. Landowners are compensated based on the marginal product of their land—the additional output generated by using that land in production. However, this theory must be nuanced to account for external factors like zoning laws, infrastructure development, and speculative demand, which can artificially inflate or deflate rents. For policymakers, recognizing these distortions is crucial for designing interventions that ensure rent remains a fair compensation mechanism rather than a barrier to economic participation.

From a practical standpoint, understanding rent as a factor payment has direct implications for businesses and individuals. For businesses, rent represents a significant operational cost that must be factored into pricing and location decisions. A startup, for example, might opt for a co-working space in a less central area to minimize rent expenses, even if it means longer commutes for employees. For individuals, rent consumption decisions are equally strategic. A household might choose to live farther from the city center to access lower rents, trading off time and transportation costs for housing affordability.

In conclusion, rent as a factor payment is more than just a transaction between landowners and users; it is a macroeconomic tool that balances scarcity and demand. By reflecting the economic value of land, rent ensures that this finite resource is allocated efficiently. However, its role is not without challenges, particularly in markets distorted by external factors. For stakeholders, from policymakers to everyday renters, grasping the mechanics of rent is essential for making informed decisions in an increasingly resource-constrained world.

Vacate Notices: Standard Procedure for Late Rent Payments?

You may want to see also

Explore related products

![]()

Interest as Opportunity Cost: Payment for borrowing funds, balancing current consumption vs. future investment

Interest rates serve as a critical mechanism for allocating resources in an economy, acting as the price paid for borrowing funds. At its core, interest represents the opportunity cost of consuming today versus saving for tomorrow. When an individual or business borrows money, they are essentially paying for the privilege of using someone else’s savings now, rather than waiting to accumulate those funds through future income. This trade-off is central to macroeconomic dynamics, influencing decisions about consumption, investment, and economic growth.

Consider a young entrepreneur seeking to start a business. By borrowing $50,000 at an annual interest rate of 6%, they gain immediate access to capital but incur a future obligation. The $3,000 in annual interest payments reflects the cost of forgoing the lender’s alternative uses of that money, such as investing in stocks or bonds. For the borrower, this expense must be weighed against the potential returns of the business. If the venture generates $8,000 in annual profit, the net gain justifies the interest cost. However, if profits fall short, the interest becomes a burden, illustrating the risk inherent in balancing current consumption against future investment.

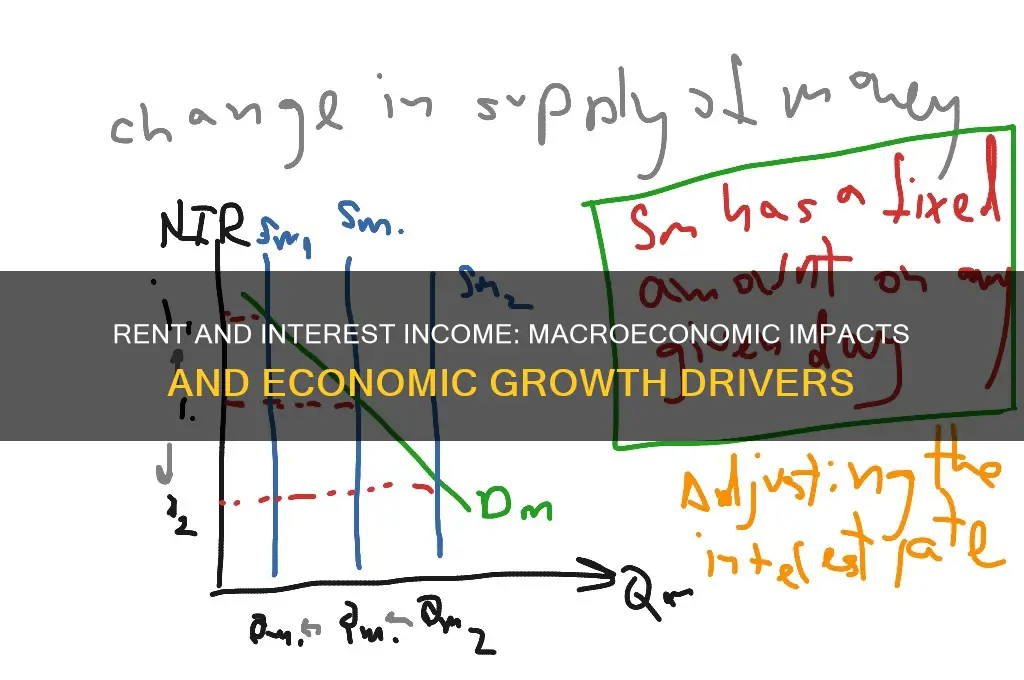

This principle extends to macroeconomic policy, where central banks manipulate interest rates to steer economic activity. Lower rates reduce the cost of borrowing, encouraging businesses to invest in expansion and consumers to spend on durable goods like homes or cars. Conversely, higher rates increase the opportunity cost of borrowing, discouraging consumption and investment while promoting saving. For instance, during the 2008 financial crisis, the Federal Reserve slashed interest rates to near zero to stimulate borrowing and spending, aiming to revive a faltering economy. Such actions highlight how interest rates act as a lever for managing the trade-offs between present and future economic activity.

Practical implications abound for individuals and policymakers alike. For households, understanding interest as an opportunity cost can inform decisions about mortgages, student loans, or credit cards. A 30-year mortgage at 4% interest means paying over $70,000 in interest on a $200,000 loan—a significant cost that should be weighed against the benefits of homeownership. Similarly, policymakers must consider how interest rate adjustments ripple through the economy, affecting inflation, employment, and growth. For example, persistently low rates can fuel asset bubbles, while high rates may stifle innovation by limiting access to capital for startups.

In essence, interest as an opportunity cost is a fundamental concept that bridges microeconomic decisions and macroeconomic outcomes. It underscores the inevitability of trade-offs in resource allocation, reminding us that every choice to consume now comes with a price on future possibilities. Whether for a small business owner, a homeowner, or a central banker, recognizing this dynamic is key to making informed decisions in an interconnected economic landscape.

Top Generator Rental Options in Maine: Your Ultimate Guide

You may want to see also

Explore related products

![]()

Rent in Housing Markets: Macroeconomic impacts of housing supply, demand, and price inflation

Housing markets are a cornerstone of macroeconomic stability, and rent—a critical component of these markets—serves as both a barometer of economic health and a driver of inflationary pressures. When housing supply fails to keep pace with demand, rents surge, triggering a ripple effect across the economy. For instance, in cities like San Francisco and New York, rent increases have outpaced wage growth, forcing households to allocate a larger share of their income to housing. This reduces discretionary spending, dampening consumer demand in other sectors. Conversely, regions with elastic housing supply, such as Texas, have seen more moderate rent growth, supporting broader economic activity. The macroeconomic takeaway is clear: rent dynamics are not isolated to housing markets; they influence inflation, consumer behavior, and overall economic growth.

To understand the macroeconomic impacts of rent inflation, consider the interplay between housing supply and demand. Supply constraints—whether due to zoning laws, construction costs, or land scarcity—exacerbate rent increases during periods of high demand. For example, a 1% decrease in housing stock relative to population can lead to a 5-10% increase in rents, according to studies by the National Bureau of Economic Research. This price inflation spills over into the broader economy through two channels: first, it directly contributes to headline inflation, as housing costs account for nearly one-third of the Consumer Price Index (CPI). Second, it erodes purchasing power, particularly for low- and middle-income households, who spend a disproportionate share of their income on rent. Policymakers must therefore balance short-term demand management with long-term supply-side reforms to mitigate these effects.

A persuasive argument for addressing rent inflation lies in its distributional consequences. High rents disproportionately burden younger demographics and lower-income households, widening wealth inequality. For instance, renters aged 25-34 in the U.S. spend an average of 40% of their income on housing, compared to 30% for homeowners in the same age group. This disparity limits savings, delays homeownership, and stifles economic mobility. From a macroeconomic perspective, such imbalances reduce aggregate demand and hinder long-term productivity growth. Governments can counteract this by incentivizing affordable housing development, reforming zoning regulations, and providing targeted rent subsidies. These measures not only stabilize housing markets but also foster a more inclusive economy.

Comparatively, countries with proactive housing policies offer valuable lessons. Germany, for example, has maintained relatively stable rents through stringent rent control laws and a robust social housing sector, which accounts for 30% of its housing stock. In contrast, the U.K.’s reliance on market forces has led to rent volatility, with London rents increasing by 50% over the past decade. Such comparisons underscore the importance of policy intervention in shaping rent dynamics. For macroeconomists, the German model highlights the potential for supply-side interventions to curb inflation and support economic stability, while the U.K. case serves as a cautionary tale of market failures in housing.

In conclusion, rent in housing markets is not merely a microeconomic issue but a critical macroeconomic variable. Its fluctuations influence inflation, consumer spending, and income inequality, with far-reaching implications for economic stability. By addressing supply constraints, implementing targeted policies, and learning from international examples, policymakers can mitigate the adverse effects of rent inflation. For households, understanding these dynamics empowers better financial planning, while for economists, it underscores the need to integrate housing markets into broader macroeconomic frameworks. The challenge is urgent, but with strategic action, the macroeconomic impacts of rent can be managed to foster a more resilient and equitable economy.

Late Rent Consequences: What Happens When You Miss a Week?

You may want to see also

Explore related products

![]()

Interest Rates and Investment: How interest rates influence capital investment and economic growth

Interest rates act as a powerful lever in the economy, directly shaping the decisions businesses make about capital investment. When central banks lower interest rates, borrowing becomes cheaper, encouraging firms to take out loans for expansion projects, new equipment, or research and development. This surge in investment fuels economic growth by increasing productive capacity and creating jobs. Conversely, higher interest rates make borrowing more expensive, leading businesses to postpone or scale back investment plans, which can slow down economic activity.

Consider the following scenario: a manufacturing company is contemplating whether to purchase a new, automated production line. At a 3% interest rate, the loan payments are manageable, and the potential increase in efficiency justifies the investment. However, if interest rates rise to 6%, the cost of borrowing may outweigh the expected returns, causing the company to delay the upgrade. This example illustrates how interest rates can act as a catalyst or a barrier to capital investment, with ripple effects throughout the economy.

The relationship between interest rates and investment is not linear; it is influenced by additional factors such as business confidence, market demand, and technological advancements. For instance, during periods of high uncertainty, even low interest rates may fail to stimulate investment if businesses are hesitant about future profitability. Similarly, in sectors where technology is rapidly evolving, firms may prioritize investment regardless of interest rates to remain competitive. Policymakers must therefore consider these nuances when using interest rates as a tool to influence economic growth.

To maximize the impact of interest rate policies on investment, governments and central banks can adopt complementary strategies. Offering tax incentives for capital expenditures or investing in public infrastructure can amplify the effects of low interest rates. Conversely, during periods of high inflation, combining interest rate hikes with fiscal discipline can help stabilize the economy without stifling long-term investment. For businesses, staying informed about interest rate trends and maintaining a flexible financial strategy can mitigate risks and capitalize on opportunities.

In conclusion, interest rates play a pivotal role in shaping capital investment and, by extension, economic growth. Their influence is profound but context-dependent, requiring a nuanced understanding of both macroeconomic conditions and firm-level dynamics. By recognizing the interplay between interest rates, investment decisions, and broader economic factors, stakeholders can make more informed choices to foster sustainable growth.

Rent a Garden Tiller in Abilene, TX: Top Locations

You may want to see also

Explore related products

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)

![]()

Rent-Seeking Behavior: Economic inefficiencies from competing for existing wealth rather than creating new value

Rent-seeking behavior occurs when individuals or firms expend resources to capture a larger share of existing wealth rather than creating new value. This phenomenon is a significant source of economic inefficiency, diverting resources from productive activities into zero-sum competitions. For instance, lobbying efforts by corporations to secure tax breaks or subsidies often fall into this category. While successful lobbying may benefit the firm, it does so at the expense of taxpayers or competitors, without generating additional economic output. This misallocation of resources slows overall growth and distorts market incentives.

Consider the pharmaceutical industry, where companies may invest heavily in patent extensions or regulatory barriers to protect their market dominance. Such strategies allow firms to maintain high prices and profits without improving the product or developing new treatments. While shareholders benefit, consumers face higher costs, and innovation is stifled. Economists estimate that rent-seeking in this sector alone can reduce societal welfare by billions annually, as resources are funneled into legal battles and lobbying rather than research and development.

To mitigate rent-seeking, policymakers can implement reforms that reduce opportunities for wealth capture. For example, simplifying tax codes and minimizing loopholes can decrease the payoff from lobbying for special treatment. Similarly, strengthening antitrust enforcement can limit firms’ ability to erect barriers to entry. However, caution is necessary, as overly restrictive policies may discourage legitimate business activities. Striking the right balance requires careful analysis of industry dynamics and the potential unintended consequences of regulation.

A comparative analysis of rent-seeking across countries reveals that economies with strong institutions and transparent governance tend to exhibit lower levels of such behavior. For instance, Nordic countries, known for their robust regulatory frameworks and low corruption, have significantly less rent-seeking compared to nations with weaker institutions. This suggests that institutional quality is a critical determinant of economic efficiency. Developing countries, in particular, can benefit from investing in governance reforms to curb rent-seeking and foster a more productive economic environment.

In conclusion, rent-seeking behavior represents a pervasive challenge to economic efficiency, diverting resources from value creation into unproductive competition. By understanding its mechanisms and consequences, policymakers and businesses can take targeted steps to reduce its impact. Practical measures include regulatory reforms, institutional strengthening, and increased transparency. While eliminating rent-seeking entirely may be unrealistic, minimizing its prevalence can unlock substantial economic benefits, promoting growth and improving societal welfare.

Breaking a Lease Early: Consequences, Fees, and Legal Implications Explained

You may want to see also

Frequently asked questions

Rent income is a component of national income, specifically under the factor payments category. It represents the earnings from the use of land or property and contributes to the overall GDP (Gross Domestic Product) as part of the income approach to measuring economic activity.

Interest income is another factor payment in macroeconomics, representing earnings from lending capital. It is included in national income calculations and reflects the cost of borrowing and the return on savings, influencing investment, consumption, and monetary policy.

Both rent and interest income are included in the income approach to GDP, which sums up all factor incomes (wages, rent, interest, and profits). They are part of the total income earned by factors of production in an economy.

Fluctuations in rent and interest income can impact macroeconomic policies. For example, rising interest rates may reduce borrowing and investment, while increasing rent income could signal higher property values or inflationary pressures, prompting central banks to adjust monetary policies.

![Rent [DVD]](https://m.media-amazon.com/images/I/516CgH-EDLL._AC_UY218_.jpg)

![RENT (Original Motion Picture Soundtrack) [Explicit]](https://m.media-amazon.com/images/I/81reolbqVvL._AC_UY218_.jpg)