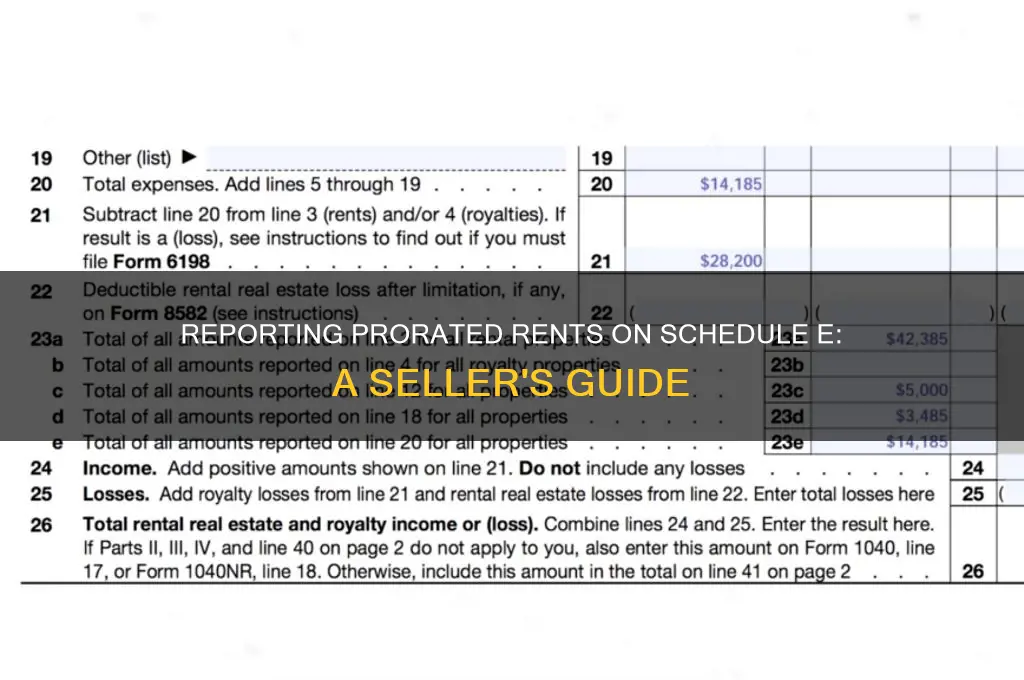

Reporting prorated rents as a seller on Schedule E of your tax return requires careful attention to detail to ensure compliance with IRS regulations. Prorated rent occurs when a tenant pays a portion of the rent for a partial month, typically during a property sale or lease transition. As the seller, you must report the prorated rent received as rental income on Schedule E, Form 1040. This involves calculating the exact amount of rent attributable to the period you owned the property and including it in the Rents Received section. Additionally, any associated expenses, such as property taxes or maintenance, should be prorated and deducted accordingly. Proper documentation of the proration agreement and clear communication with the buyer are essential to avoid discrepancies. Accurate reporting ensures you meet tax obligations while reflecting the true financial impact of the transaction.

| Characteristics | Values |

|---|---|

| Reporting Method | Prorated rents are reported on Schedule E (Form 1040) as rental income. |

| Line Item | Enter the prorated rent amount on Line 3 (Rents received) of Schedule E. |

| Calculation | Prorate rent based on the number of days of ownership in the tax year. For example, if you sold the property mid-month, only include rent for the days you owned it. |

| Documentation | Keep records of the sale date, rent amount, and proration calculation to support your reporting. |

| Buyer's Responsibility | The buyer is typically responsible for reporting their portion of the prorated rent on their own tax return. |

| IRS Guidance | Refer to IRS Publication 527 (Residential Rental Property) for detailed instructions on reporting rental income, including prorated rents. |

| Tax Implications | Prorated rents are taxable income and must be reported in the year received, even if the rental period extends into the next year. |

| State Tax Considerations | State tax rules may vary; check your state's tax guidelines for reporting prorated rents. |

| Professional Advice | Consult a tax professional or CPA for specific guidance on your situation, especially if the transaction is complex. |

| Form 1099-S | If the sale involves a real estate transaction, the closing agent may issue Form 1099-S, which should reflect the prorated rent allocation. |

Explore related products

What You'll Learn

![]()

Identifying Prorated Rent Periods

When identifying prorated rent periods for reporting on Schedule E as a seller, it's essential to first understand the timeframe involved in the property sale and the corresponding rental income. Prorated rent occurs when the property changes hands mid-rental period, meaning the seller is entitled to a portion of the rent for the days they owned the property during that period. To accurately identify these periods, start by noting the closing date of the sale, as this marks the point where ownership and rental income responsibilities shift from the seller to the buyer. The rental period in question is typically the month in which the closing occurs, but it could also span multiple months depending on the rent collection schedule.

Next, determine the specific start and end dates of the rental period that overlaps with your ownership. For example, if the closing date is October 15th and the rent is collected monthly on the 1st, the prorated period would be from October 1st to October 15th. The seller is entitled to rent for the first 15 days of October, while the buyer is responsible for the remaining 16 days. Clearly identifying these dates is crucial for calculating the prorated amount and ensuring accurate reporting on Schedule E.

To further refine the identification process, review the lease agreement for any specific terms related to rent proration or ownership transfer. Some leases may include clauses that dictate how rent is prorated upon sale, which can provide additional guidance. Additionally, consider the method of rent collection—whether it’s monthly, bi-weekly, or another schedule—as this affects how the prorated period is calculated. For instance, if rent is collected bi-weekly, the prorated period would align with the specific bi-weekly cycle that overlaps with the closing date.

Another important step is to verify the actual rent payment dates and amounts during the prorated period. If the tenant paid rent in advance or if there were any adjustments (e.g., partial payments or credits), these details must be accounted for when identifying the prorated period. Cross-referencing bank statements or rent receipts with the lease agreement ensures that the identified period aligns with the actual financial transactions.

Finally, document the identified prorated rent period clearly for reporting purposes. On Schedule E, you’ll need to report the prorated rental income under the appropriate line item, typically as a portion of the total rent received for the year. Accurate identification and documentation of the prorated period not only ensure compliance with IRS requirements but also provide transparency for both the seller and buyer in the property transaction. By methodically identifying the prorated rent period, you can confidently report the correct figures on Schedule E and avoid potential discrepancies or audits.

Rent-A-Center: Stackable Washer-Dryers for Your Home

You may want to see also

Explore related products

![]()

Calculating Prorated Rent Amounts

When calculating prorated rent amounts for reporting on Schedule E as a seller, it's essential to understand the prorating process. Prorated rent is the portion of the rent that corresponds to the number of days the seller owned the property during the rental period. To begin, determine the total monthly rent agreed upon in the lease. For example, if the monthly rent is $1,200, this is your starting point. Next, identify the exact dates of ownership transfer. If the seller owned the property for 20 days in a 30-day month, the prorated rent is calculated based on this fraction of the month.

The formula to calculate prorated rent is straightforward: divide the number of days the seller owned the property by the total days in the month, then multiply by the monthly rent. Using the example above, the calculation would be (20 days / 30 days) * $1,200 = $800. This $800 is the prorated rent amount the seller should report on Schedule E. Ensure accuracy by double-checking the dates and calculations, as errors can lead to discrepancies in reporting.

When reporting prorated rents on Schedule E, the prorated amount is typically recorded as rental income. It’s important to differentiate this from the full monthly rent, as only the portion corresponding to the seller’s ownership period is reportable. Additionally, if the tenant paid rent in advance or if there were prepaid rents, adjust the prorated amount accordingly. For instance, if the tenant paid the full month’s rent but the seller only owned the property for part of the month, the seller should only report the prorated portion as income.

Another consideration is how to handle security deposits or prepaid rents. If the seller received a security deposit that was not refunded to the tenant, it should not be included in the prorated rent calculation. Security deposits are generally not considered income unless they are forfeited by the tenant and applied to unpaid rent or damages. Focus solely on the rent income for the period of ownership when calculating prorated amounts for Schedule E.

Finally, document all calculations and supporting details for tax purposes. Keep records of the lease agreement, ownership transfer dates, and rent payment receipts. Clear documentation ensures compliance with IRS requirements and simplifies the reporting process. By accurately calculating and reporting prorated rent amounts, sellers can avoid potential audits and ensure their Schedule E reflects the correct rental income for the period they owned the property.

Airbnb's Travel Trailer Rentals: What You Need to Know

You may want to see also

Explore related products

![]()

Reporting on Schedule E Line Items

When reporting prorated rents as a seller on Schedule E of your tax return, it’s essential to understand how to allocate rental income and expenses accurately. Schedule E is used to report income and expenses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in real estate mortgage investment conduits (REMICs). For prorated rents, the focus is on the *Rental Real Estate Income and Expenses* section. The key is to report the portion of rent you received for the period you owned the property. For example, if you sold the property mid-month, you would only report the rent income and associated expenses up to the date of sale.

To report prorated rents, start by entering the total rental income received during the period you owned the property on Line 1 (Rents received) of Schedule E. If the tenant paid rent in advance or if you received a security deposit that you kept as rent, include these amounts as well, but only for the period you owned the property. For instance, if the tenant paid $1,200 in rent for the month but you sold the property on the 15th, you would report $600 (half of the rent) on Line 1, assuming a 30-day month. Ensure that the prorated amount reflects the exact number of days you owned the property during the rental period.

Next, report any *expenses* related to the rental property on the appropriate lines of Schedule E, prorated for the same period. Common expenses include mortgage interest, property taxes, insurance, maintenance, and depreciation. For example, if you paid $100 in property taxes for the month but sold the property on the 15th, you would report $50 on Line 16 (Taxes). Similarly, prorate other expenses like utilities, repairs, and property management fees for the period you owned the property. It’s crucial to maintain detailed records of all income and expenses to ensure accurate reporting.

When calculating *net rental income or loss*, subtract the prorated expenses from the prorated rental income. The result goes on Line 19 (Net rental income or loss). If you sold the property and had a gain or loss from the sale, this is reported separately on Schedule D (Capital Gains and Losses), not on Schedule E. Schedule E is strictly for rental income and expenses, not for the sale of the property itself.

Finally, ensure that the prorated amounts are clearly documented and supported by lease agreements, sale documents, and receipts. If the buyer and seller agreed to a specific proration method at closing, ensure your Schedule E reporting aligns with that agreement. Accuracy in prorating rents and expenses is critical to avoid IRS scrutiny and to ensure compliance with tax laws. If unsure, consult a tax professional to ensure proper reporting on Schedule E.

Surviving the City: How Community College Professors Afford Rent

You may want to see also

Explore related products

![]()

Documenting Proration Agreements

When documenting proration agreements for prorated rents as a seller on Schedule E, clarity and precision are essential to ensure accurate reporting and compliance with IRS regulations. Begin by clearly identifying the property and the specific rental period involved in the proration. Include the tenant’s name, lease agreement details, and the exact dates for which rent is being prorated. This foundational information sets the context for the proration and helps avoid confusion during tax preparation.

Next, specify the proration calculation method in the agreement. Detail the total rent due for the period, the portion allocated to the seller, and the portion allocated to the buyer. For example, if a tenant pays $1,200 monthly rent and the seller transfers ownership mid-month, the agreement should explicitly state how the rent is divided between the parties. Use a consistent and transparent formula, such as a per diem calculation, to ensure fairness and accuracy.

Include a breakdown of any prepaid or uncollected rents that affect the proration. If the tenant has prepaid rent beyond the closing date, document this amount and clarify how it is credited or debited between the buyer and seller. Similarly, if there are outstanding rents owed by the tenant, specify how this liability is handled in the proration agreement. This ensures that all parties are aware of their financial responsibilities.

Formalize the proration agreement in writing and ensure it is signed by both the buyer and seller. Attach this document to the closing statement for reference. When reporting on Schedule E, use the prorated rent amount as the rental income received during your ownership period. Clearly label this amount in the appropriate line item, typically under rental income, and retain the proration agreement as supporting documentation in case of an IRS audit.

Finally, coordinate with your tax preparer or accountant to ensure the prorated rent is reported correctly on Schedule E. Double-check that the figures align with the proration agreement and the closing statement. Proper documentation not only simplifies tax reporting but also protects all parties involved by providing a clear record of the financial transaction. By following these steps, you can confidently document proration agreements and accurately report prorated rents on Schedule E.

Loss of Use Coverage: Can You Claim Lost Rent?

You may want to see also

Explore related products

![]()

Handling Tax Implications of Prorated Rents

When handling the tax implications of prorated rents as a seller, it's essential to accurately report these amounts on Schedule E of your IRS Form 1040. Prorated rents occur when a property sale closes mid-rental period, and the buyer and seller agree to split the rent based on the number of days each party owns the property. To report prorated rents correctly, start by identifying the total rent due for the month and calculate the portion attributable to your ownership period. This amount is considered rental income and must be reported on Schedule E, Part I (Rental Income and Expenses). Ensure you include only the prorated amount, not the full month’s rent, to avoid overreporting income.

Next, allocate any prepaid rents received from the tenant but earned by the buyer. For example, if the tenant paid rent for the entire month but you only owned the property for half of it, the portion of rent corresponding to the buyer’s ownership period should be deducted from your rental income. This adjustment ensures that only the income you actually earned is reported. Clearly document these calculations to support your reporting in case of an IRS inquiry. Additionally, if you received a lump sum for prorated rents at closing, this amount should still be reported as rental income on Schedule E for the tax year in which the sale occurred.

Expenses related to the rental property must also be prorated and reported on Schedule E. Deductible expenses, such as property taxes, mortgage interest, and maintenance costs, should be allocated based on the period you owned the property. For instance, if you owned the property for 15 days in January, you would report 15/31 of the monthly expenses. Ensure that expenses are not duplicated or omitted, as this could affect your taxable rental income. Properly prorating both income and expenses provides an accurate reflection of your rental activity for the tax year.

It’s crucial to coordinate with the buyer and closing agent to obtain accurate figures for prorated rents and expenses. The settlement statement (HUD-1 or ALTA) typically outlines these amounts, which can serve as a reference for your Schedule E reporting. If discrepancies arise, consult a tax professional to ensure compliance with IRS rules. Misreporting prorated rents can lead to audits or penalties, so meticulous record-keeping and clear documentation are vital.

Finally, consider the timing of the sale and its impact on your tax obligations. If the sale occurs late in the year, you may need to file an extension to accurately report prorated rents and related expenses. Additionally, if you have multiple rental properties or complex transactions, consult a tax advisor to ensure proper reporting. Handling prorated rents correctly on Schedule E not only ensures compliance but also maximizes your tax efficiency by accurately reflecting your rental income and expenses for the period of ownership.

How to Avoid Renting a Modem from Comcast

You may want to see also

Frequently asked questions

Prorated rents received as a seller should be reported on Schedule E, line 3 (Rents Received) for the period you owned the property. Only include rents for the days you were the landlord.

Yes, you must report prorated rents for the portion of the month you owned the property, even if the sale occurred mid-month.

Prorated expenses (e.g., property taxes, mortgage interest) should be allocated for the period you owned the property and reported on the appropriate lines of Schedule E (e.g., line 14 for taxes, line 15 for interest).

Only report the prorated rent amount you received for the days you owned the property. Do not include rent collected by the buyer for the period after the sale.

Security deposits are not considered rent income unless they are forfeited. Do not include security deposits in your prorated rent calculations on Schedule E.