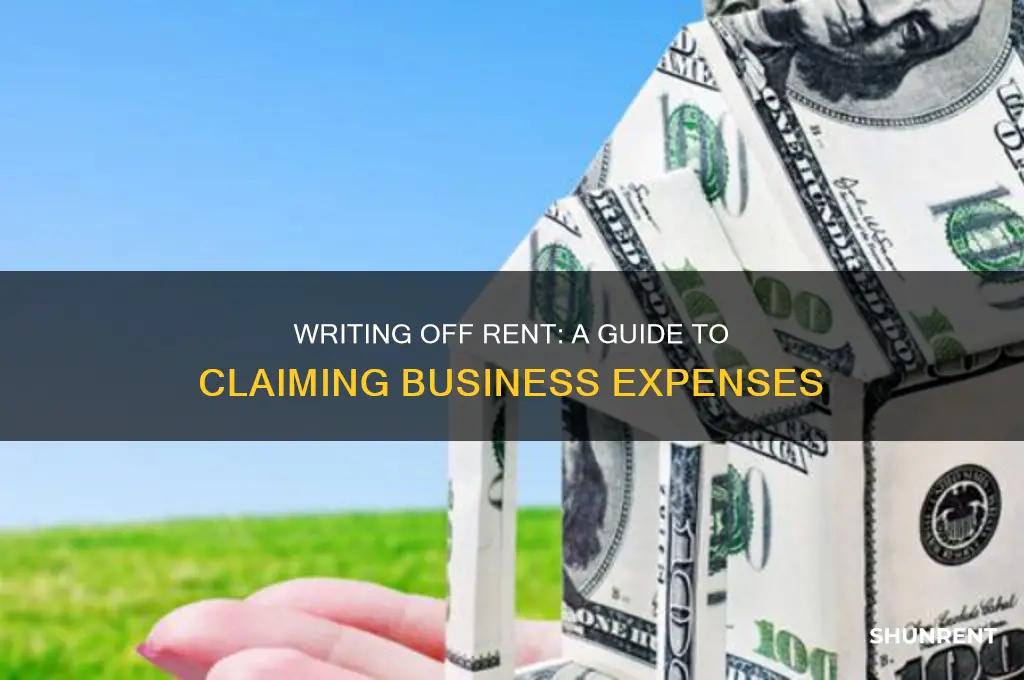

Writing off rent as a business expense can be a valuable tax strategy for entrepreneurs and small business owners, but it requires careful consideration of IRS guidelines and proper documentation. To qualify, the rented space must be used regularly and exclusively for business purposes, whether it’s a home office, storefront, or separate commercial property. For home offices, the space must be clearly delineated and used solely for work, while commercial rentals must directly support business operations. Expenses such as rent, utilities, insurance, and maintenance may be deductible, but personal use portions must be excluded. Maintaining detailed records, including lease agreements, receipts, and usage logs, is essential to substantiate the claim and avoid audits. Consulting a tax professional can ensure compliance and maximize deductions while minimizing risks.

| Characteristics | Values |

|---|---|

| Eligibility | You must use the rented space regularly and exclusively for business purposes. Partial business use may qualify for a partial deduction. |

| Documentation | Lease agreement, rent receipts, utility bills, and proof of business use (e.g., photos, client records) are required. |

| Home Office Deduction | If using part of your home, calculate the percentage of space used for business and deduct that portion of rent, utilities, insurance, etc. |

| Simplified Option (Home Office) | Instead of actual expenses, use $5 per square foot (up to 300 sq. ft.) for a simplified deduction. |

| Depreciation | If you own the property and rent it to your business, you may be able to depreciate the building over time. |

| Limitations | Deductions cannot exceed your business income. Excess deductions can be carried forward to future tax years. |

| Tax Form | Report rent expenses on Schedule C (Sole Proprietorship) or the appropriate business tax form. |

| Professional Advice | Consult a tax professional for specific guidance based on your situation and location. |

Explore related products

What You'll Learn

- Home Office Deduction Rules: Criteria for claiming rent as a business expense for home offices

- Percentage of Space Used: Calculating deductible rent based on business-exclusive space in your home

- Documentation Requirements: Records needed to prove rent expenses are business-related for tax purposes

- Sole Proprietorship vs. LLC: How business structure affects rent write-offs for different entities

- Partial Rent Deductions: Claiming a portion of rent when space is used for both business and personal use

![]()

Home Office Deduction Rules: Criteria for claiming rent as a business expense for home offices

To claim rent as a business expense through the home office deduction, the space must meet specific IRS criteria. First, the area designated as your home office must be used *exclusively and regularly* for business purposes. This means the space cannot double as a guest room, gym, or recreational area; it must be solely dedicated to work-related activities. For example, if you use a spare bedroom exclusively for client meetings and administrative tasks, it qualifies. However, if the same room is used for personal activities, it does not meet the exclusivity requirement.

Second, the home office must be the *principal place of business* for your company. This means it is the primary location where you conduct business activities, such as managing operations, meeting clients, or handling administrative tasks. If you have an external office but also work from home, the home office must still be essential to the operation of your business. For instance, freelancers or consultants who work primarily from home would likely qualify, while employees who occasionally work remotely may not, unless their employer lacks a physical office.

Third, the deduction method you choose—*simplified or actual expenses*—impacts how you calculate the write-off. The simplified method allows a deduction of $5 per square foot, up to 300 square feet, totaling $1,500 annually. This method is straightforward but may result in a smaller deduction. Alternatively, the actual expense method requires calculating the percentage of your home used for business and applying that to expenses like rent, utilities, insurance, and repairs. While more complex, this method can yield a larger deduction if your home office is substantial or expenses are high.

Fourth, if you rent your home, the deduction is limited to the *net earnings* from your business. For example, if your business earns $30,000 annually and your home office expenses total $5,000, you can only deduct up to $30,000. Any excess can be carried forward to future tax years. Additionally, landlords cannot claim home office deductions for rental properties unless they actively use part of the property for their own business, separate from rental activities.

Finally, maintaining *detailed records* is critical to substantiating your claim. Document the square footage of your home office, business income and expenses, and how the space is used exclusively for work. If audited, the IRS may require proof, such as floor plans, utility bills, or logs of business activities. Adhering to these rules ensures compliance and maximizes your potential deduction while minimizing the risk of penalties.

Gary Coleman's Tragic End: Unraveling His Death from Different Strokes

You may want to see also

Explore related products

![]()

Percentage of Space Used: Calculating deductible rent based on business-exclusive space in your home

When writing off rent as a business expense, one of the most common methods for homeowners is to calculate the deductible amount based on the Percentage of Space Used exclusively for business purposes. This approach is particularly relevant if you use a portion of your home as a dedicated office, studio, or workspace. The Internal Revenue Service (IRS) allows you to deduct a portion of your rent or home expenses if you meet specific criteria, including the exclusive and regular use of the space for business activities. To begin, you’ll need to determine the total square footage of your home and the square footage of the area used solely for business. For example, if your home is 2,000 square feet and your office space is 200 square feet, the business-exclusive space represents 10% of your total home area.

Once you’ve calculated the percentage of space used for business, you can apply this ratio to your total rent or home expenses to determine the deductible amount. Home expenses eligible for this deduction typically include rent, utilities, insurance, property taxes, and maintenance costs. For instance, if your monthly rent is $1,500 and 10% of your home is used for business, you could deduct $150 per month as a business expense. It’s crucial to maintain accurate records of your expenses and measurements to support your deduction in case of an audit. Additionally, ensure that the space in question is used regularly and exclusively for business—occasional or personal use of the area can disqualify it from this deduction.

To accurately calculate the deductible rent, measure the length and width of both your entire home and the business-exclusive space. Multiply these dimensions to find the square footage for each area. If your home has multiple stories, include only the floors where business space is located, unless the entire home is used for business. For example, if your office is on the first floor and your home has two floors, only consider the square footage of the first floor in your calculations. This ensures that your percentage is based on the relevant living space.

It’s important to note that the Percentage of Space Used method applies not only to rent but also to other home-related expenses. For instance, if you’re deducting utilities, apply the same percentage to your monthly utility bills. However, certain expenses, like mortgage interest or property taxes, are handled differently and may be claimed as itemized deductions on your personal taxes rather than as business expenses. Always consult IRS Publication 587, *Business Use of Your Home*, for detailed guidelines on what qualifies and how to calculate deductions accurately.

Finally, keep detailed records of your calculations, measurements, and expenses to substantiate your deductions. This includes floor plans, utility bills, rent receipts, and any other documentation that verifies the business use of your home. Proper record-keeping not only ensures compliance with IRS rules but also simplifies the process if you’re ever audited. By carefully calculating the Percentage of Space Used and applying it to your eligible expenses, you can maximize your deductions while staying within the bounds of tax regulations.

Rent vs Lease: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Documentation Requirements: Records needed to prove rent expenses are business-related for tax purposes

When claiming rent as a business expense, maintaining thorough and accurate documentation is crucial to substantiate your claims to tax authorities. The primary requirement is a lease or rental agreement that clearly outlines the terms of the rental, including the property address, lease duration, monthly rent amount, and the names of the involved parties. This document serves as the foundational proof that the rent expense exists and is associated with your business. Ensure the agreement is signed by both the landlord and the tenant to validate its authenticity.

In addition to the lease agreement, payment records are essential to demonstrate that rent payments were actually made. These records can include canceled checks, bank statements showing rent payments, or receipts from the landlord. For digital transactions, maintain screenshots or transaction confirmations from online payment platforms. It’s important to ensure these records align with the rent amount and frequency specified in the lease agreement. Consistency between the agreement and payment records is critical to avoid discrepancies that could raise red flags during an audit.

Another key piece of documentation is evidence of business use for the rented property. If the property is used partially for business and partially for personal purposes, you must clearly document the percentage of space dedicated to business activities. This can be done through floor plans, photographs, or detailed descriptions of how the space is utilized. For example, if a home office occupies 20% of the property, you can claim 20% of the rent as a business expense. Keeping a log or journal that tracks business-related activities conducted at the property can further support your claim.

Utility bills and maintenance records can also be used to reinforce the business nature of the rent expense, especially if these costs are included in the rent or paid separately. If utilities or maintenance are directly related to the business use of the property, document these expenses and their connection to your business operations. For instance, if you’re running a home-based business, utility bills that reflect increased usage due to business activities can be relevant. However, only the portion attributable to business use should be documented.

Lastly, tax filings and financial statements should consistently reflect the rent expense as a business deduction. Ensure your bookkeeping and accounting records accurately categorize rent payments as a business expense. If you’re audited, tax authorities will likely request these records to verify that the expense was properly reported. Using accounting software or working with a professional accountant can help ensure compliance and proper documentation. By maintaining these detailed records, you can confidently claim rent as a business expense while minimizing the risk of disputes with tax authorities.

Finding Rental Demand: Area Analysis Techniques

You may want to see also

Explore related products

![]()

Sole Proprietorship vs. LLC: How business structure affects rent write-offs for different entities

When considering how to write off rent as a business expense, understanding the impact of your business structure is crucial. Sole Proprietorships and LLCs (Limited Liability Companies) are two common structures, but they differ significantly in how rent expenses are treated for tax purposes. In a Sole Proprietorship, the business and the owner are considered the same entity for tax purposes. This means that rent paid for a home office or business space can often be deducted directly on Schedule C of the owner’s personal tax return (Form 1040). However, if the rented space is also used for personal purposes, only the portion used exclusively for business is deductible. For example, if 20% of your home is used as an office, you can write off 20% of the rent. The simplicity of this structure makes it easier to claim rent deductions, but it also means the owner is personally liable for business debts.

In contrast, an LLC offers more flexibility and protection but requires a more structured approach to rent write-offs. If the LLC is taxed as a sole proprietorship (single-member LLC), the rules are similar to those of a sole proprietorship, with rent deductions claimed on Schedule C. However, if the LLC is taxed as a partnership or corporation, the rent deduction process changes. For instance, in a multi-member LLC taxed as a partnership, rent expenses are reported on Form 1065, and each member claims their share of the deduction on their individual tax returns. For LLCs taxed as S-Corporations or C-Corporations, rent is deducted on the corporate tax return (Form 1120 or 1120-S), and proper documentation is essential to ensure compliance with IRS regulations.

One key difference between the two structures is how home office deductions are handled. For sole proprietors, the home office deduction is straightforward and can be claimed using the simplified method (up to $1,500 per year) or the actual expense method. For LLCs, especially those taxed as corporations, the home office deduction is more complex and may require detailed records to prove business usage. Additionally, LLCs must ensure that rent payments between members or owners are structured as legitimate business transactions to avoid scrutiny from the IRS.

Another important factor is pass-through taxation versus corporate taxation. Sole proprietorships and single-member LLCs benefit from pass-through taxation, where business income and expenses are reported on the owner’s personal return. This simplifies rent write-offs but limits liability protection. LLCs taxed as corporations, however, face double taxation unless they elect S-Corporation status, which can complicate rent deductions but offers greater liability protection and credibility.

Ultimately, the choice between a Sole Proprietorship and an LLC depends on your business needs, risk tolerance, and tax strategy. Sole proprietorships offer simplicity and ease in claiming rent deductions but lack liability protection. LLCs provide more flexibility and protection but require careful planning and documentation to maximize rent write-offs. Consulting a tax professional can help you navigate these differences and choose the structure that best aligns with your business goals.

San Francisco vs Hong Kong: Rental Rates Compared

You may want to see also

Explore related products

![]()

Partial Rent Deductions: Claiming a portion of rent when space is used for both business and personal use

When your rental space serves both personal and business purposes, you can claim partial rent deductions on your taxes, but it requires careful calculation and documentation. The key principle is to allocate the rent proportionally based on the space used exclusively for business. For example, if you use a spare room in your apartment as a home office and it constitutes 15% of the total square footage, you can deduct 15% of the rent as a business expense. This method ensures compliance with tax regulations and avoids overclaiming.

To determine the deductible portion, measure the area dedicated solely to business activities and divide it by the total rentable space. Multiply this percentage by the total rent paid annually to calculate the allowable deduction. For instance, if your monthly rent is $1,200 and your home office occupies 20% of the space, your annual deduction would be $2,880 ($1,200 x 12 x 0.20). Keep detailed records of these calculations, as the IRS may require proof of your allocation method during an audit.

It’s important to note that the space claimed must be used regularly and exclusively for business. This means personal activities should not take place in the designated area. For example, a room used as both a guest bedroom and a part-time office would not qualify for the deduction. Ensure the space is clearly defined and primarily functional for business operations, such as client meetings, inventory storage, or administrative work.

In addition to rent, you can also deduct a portion of related expenses like utilities, insurance, and property taxes, using the same percentage allocation. For instance, if your home office occupies 20% of the space, you can deduct 20% of your electricity bill, internet costs, and other applicable expenses. However, expenses tied to the entire property, such as mortgage interest or structural repairs, are not eligible for partial deductions unless they directly benefit the business space.

Finally, maintain thorough documentation to support your partial rent deduction claims. This includes lease agreements, floor plans, utility bills, and any other records that demonstrate the business use of the space. If you’re unsure about your eligibility or calculations, consult a tax professional to ensure accuracy and maximize your deductions while staying within legal boundaries. Partial rent deductions can significantly reduce your taxable income, but they require precision and adherence to IRS guidelines.

The Cost of Renting a U-Haul: How Much Does It Really Cost?

You may want to see also

Frequently asked questions

Yes, you can write off a portion of your rent as a business expense if you use part of your home exclusively and regularly for business. The deductible amount is typically based on the percentage of your home used for business.

To calculate the rent write-off, multiply your total rent by the percentage of your home used for business. For example, if you use 20% of your home for business, you can deduct 20% of your rent as a business expense.

Yes, the space must be used exclusively and regularly for business purposes. Additionally, if you’re renting from a related party (e.g., a family member), the IRS may scrutinize the arrangement to ensure it’s legitimate and at fair market value.

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/71crDiqBzUL._AC_UL320_.jpg)