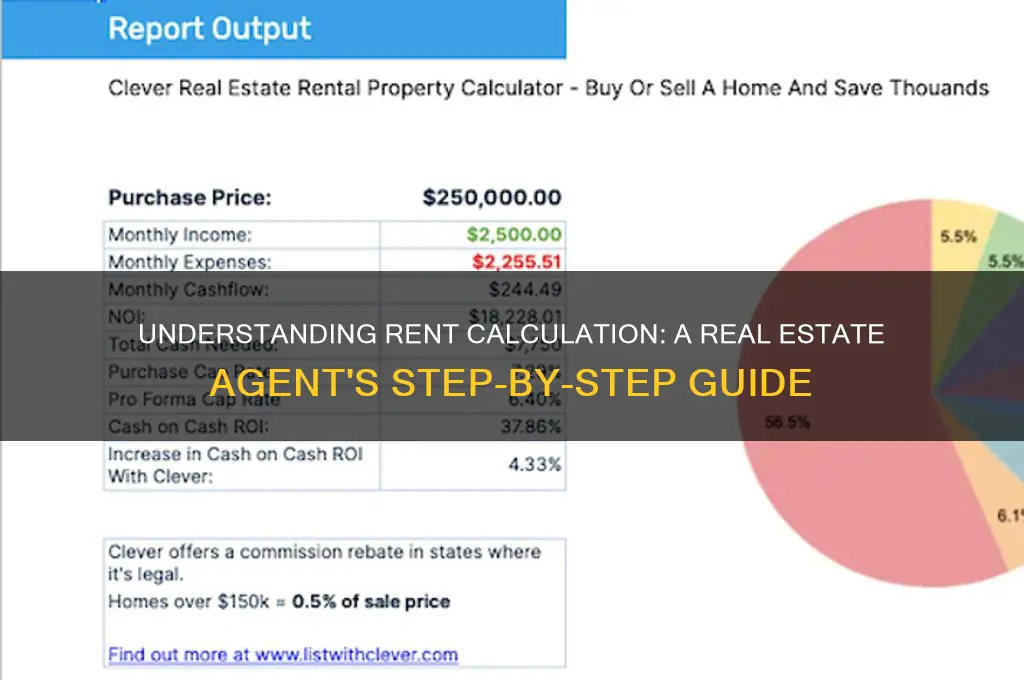

Real estate agents calculate rent using a combination of market analysis, property valuation, and local demand factors. They typically start by assessing the property’s location, size, condition, and amenities, comparing it to similar rentals in the area to determine competitive pricing. Agents also consider current market trends, vacancy rates, and economic conditions to adjust rent accordingly. Additionally, they may use formulas like the 1% rule (rent should be about 1% of the property’s purchase price) or evaluate the potential return on investment for landlords. By balancing tenant affordability with maximizing landlord income, agents aim to set a rent that attracts quality tenants while ensuring the property remains profitable.

| Characteristics | Values |

|---|---|

| Market Rent Comparison | Agents analyze comparable rental properties (comps) in the area to determine fair market rent. Factors include location, property size, condition, and amenities. |

| 1% Rule of Thumb | A quick estimate where monthly rent is roughly 1% of the property's purchase price (e.g., a $200,000 property might rent for $2,000/month). |

| Gross Rent Multiplier (GRM) | Calculated as Property Price ÷ Annual Rent. A lower GRM indicates higher potential returns. |

| Operating Expense Ratio (OER) | Total operating expenses (maintenance, taxes, insurance) ÷ Gross Rental Income. Helps assess profitability. |

| Cap Rate (Capitalization Rate) | Net Operating Income (NOI) ÷ Property Value. Used to evaluate rental property investment potential. |

| Local Demand and Vacancy Rates | High demand and low vacancy rates often justify higher rents. |

| Property Condition and Upgrades | Newly renovated or well-maintained properties typically command higher rents. |

| Seasonal Adjustments | Rent may fluctuate based on seasonality (e.g., higher in summer for vacation areas). |

| Legal and Regulatory Factors | Rent control laws, tenant protections, and local regulations influence rent pricing. |

| Tenant Profile and Screening | Agents may adjust rent based on tenant income, creditworthiness, and rental history. |

| Economic Factors | Inflation, interest rates, and local economic conditions impact rental pricing. |

| Lease Terms | Longer-term leases may offer slightly lower monthly rent compared to short-term leases. |

| Utilities and Services Included | Properties with included utilities (e.g., water, electricity) may charge higher base rent. |

| Square Footage and Layout | Rent is often calculated per square foot, with larger or better-designed spaces commanding higher rates. |

| Pet Policies | Properties allowing pets may charge additional fees or higher rent. |

Explore related products

What You'll Learn

- Market Rent Analysis: Researching comparable properties to determine competitive rental rates in the area

- Operating Expenses Calculation: Factoring in maintenance, taxes, insurance, and management costs into rent pricing

- Return on Investment (ROI): Setting rent to achieve desired ROI based on property purchase price

- Vacancy and Turnover Costs: Accounting for potential vacancy periods and turnover expenses in rent calculations

- Local Rent Control Laws: Adjusting rent to comply with local regulations and rent stabilization policies

![]()

Market Rent Analysis: Researching comparable properties to determine competitive rental rates in the area

Real estate agents often begin the rent calculation process by conducting a Market Rent Analysis, a critical step that involves researching comparable properties, or "comps," to determine competitive rental rates in the area. This method ensures that the rent is set at a price that aligns with market conditions, maximizing both occupancy and revenue. By examining similar properties in terms of size, location, amenities, and condition, agents can gauge the current demand and pricing trends. For instance, a two-bedroom apartment in a downtown area with modern finishes and proximity to public transportation will likely command a higher rent than a similar unit in a less accessible neighborhood.

To perform a Market Rent Analysis effectively, agents follow a structured approach. First, they identify a set of comparable properties within a one-mile radius, focusing on units with similar square footage, number of bedrooms, and key features like parking or in-unit laundry. Next, they gather data on these properties, including current rental rates, lease terms, and vacancy rates. Online platforms such as Zillow, Rentometer, or local MLS databases are invaluable tools for this research. Agents also consider seasonal fluctuations, as rental demand can vary significantly depending on the time of year. For example, in college towns, rents may peak during the summer months when students are searching for housing.

A key caution in this process is avoiding over-reliance on outdated or incomplete data. Rental markets can shift rapidly due to factors like economic changes, new developments, or shifts in tenant preferences. Agents must ensure their comps are recent—ideally from the past six months—and verify the accuracy of the data. For instance, a property listed as "available" might already be under contract, skewing the perceived vacancy rate. Additionally, agents should account for unique features that may justify a higher rent, such as a renovated kitchen or a pet-friendly policy, which can attract a premium.

The takeaway from a Market Rent Analysis is a competitive rental rate that balances attracting tenants with maximizing income. For example, if comparable two-bedroom units in a suburban area are renting for $1,500 to $1,700 per month, an agent might set the rent at $1,600 for a similar property, especially if it offers additional perks like a backyard or garage. However, if the analysis reveals high vacancy rates or downward pricing pressure, the agent might recommend a slightly lower rent to ensure quick occupancy. This data-driven approach not only helps landlords avoid overpricing but also prevents underpricing, which can leave money on the table.

In conclusion, a Market Rent Analysis is a cornerstone of rent calculation, providing real estate agents with actionable insights to set competitive rental rates. By meticulously researching comparable properties and considering market dynamics, agents can position their listings effectively. Practical tips include using multiple data sources, updating research regularly, and factoring in unique property features. This method ensures that both landlords and tenants benefit from a fair and market-aligned rental agreement.

Rent-A-Center Jackson, Michigan Closing Hours: What You Need to Know

You may want to see also

Explore related products

![]()

Operating Expenses Calculation: Factoring in maintenance, taxes, insurance, and management costs into rent pricing

Real estate agents don’t pull rent prices out of thin air. Behind every rental figure lies a meticulous calculation of operating expenses, which are the backbone of sustainable property management. Maintenance, taxes, insurance, and management costs aren’t just line items—they’re critical factors that determine whether a rental property turns a profit or becomes a financial drain. Ignoring these expenses can lead to underpricing, while overestimating them risks pricing out potential tenants. Striking the right balance requires a clear understanding of each cost component and how it fits into the broader financial picture.

Consider maintenance costs, which are notoriously unpredictable yet unavoidable. A rule of thumb is to set aside 1% of the property’s value annually for upkeep, but this varies based on age, location, and condition. For instance, a 20-year-old apartment building in a humid climate may require more frequent repairs than a newer property in a dry region. Agents must also account for emergency repairs, such as a burst pipe or roof damage, by adding a buffer to the maintenance budget. Without this foresight, unexpected expenses can eat into profits or force rent increases that alienate tenants.

Taxes and insurance are more predictable but equally significant. Property taxes fluctuate based on local assessments and can increase dramatically in high-demand areas. Insurance premiums depend on factors like crime rates, natural disaster risks, and building materials. For example, a property in a flood zone will carry higher insurance costs than one on higher ground. Agents should research historical tax trends and obtain multiple insurance quotes to ensure these expenses are accurately factored into rent pricing. Overlooking these details can result in a rental rate that fails to cover these mandatory costs.

Management costs, often underestimated, include fees for property managers, advertising, and legal services. If an agent outsources management, the fee typically ranges from 8% to 12% of the monthly rent. Self-managing can reduce costs but demands significant time and expertise. Additionally, vacancy rates must be considered—industry standards suggest budgeting for 5% to 10% vacancy annually. These costs, while less tangible than taxes or insurance, are essential to maintaining a well-run property and should be baked into the rent calculation from the outset.

The key to successful rent pricing lies in treating operating expenses as a dynamic, interconnected system. Agents must analyze historical data, anticipate future trends, and adjust calculations accordingly. For example, if property taxes are expected to rise due to local development, this should be reflected in the rent. Similarly, if maintenance costs are projected to decrease after a major renovation, tenants could benefit from slightly lower rent. By meticulously factoring in maintenance, taxes, insurance, and management costs, agents can set a rent price that ensures profitability while remaining competitive in the market. This approach not only protects the landlord’s investment but also fosters long-term tenant satisfaction.

Renting Your Dream Wedding Dress: A Cost-Effective Guide for Brides

You may want to see also

Explore related products

![]()

Return on Investment (ROI): Setting rent to achieve desired ROI based on property purchase price

Real estate agents often use Return on Investment (ROI) as a critical metric to determine rental pricing, ensuring the property generates income that aligns with the investor’s financial goals. ROI is calculated by dividing the annual net income from the property by the total investment cost, typically the purchase price. For example, if a property costs $200,000 and the investor seeks a 6% ROI, the annual net income must be $12,000. To achieve this, the agent first estimates annual expenses—property taxes, insurance, maintenance, and property management fees—and subtracts these from the desired annual income to determine the minimum rent required. This method ensures the rent is set not just to cover costs but to meet specific investment objectives.

Setting rent based on ROI requires a balance between maximizing income and maintaining market competitiveness. Agents analyze comparable rental properties in the area to ensure the rent is attractive to tenants while still achieving the desired ROI. For instance, if similar properties rent for $1,500 monthly, the agent might set rent at $1,600 if the property offers unique features like updated appliances or a prime location. However, if the market cannot support a higher rent, the investor may need to adjust their ROI expectations or consider value-add improvements to justify the increase. This approach combines financial precision with market awareness to strike the right balance.

A step-by-step process can guide agents in setting rent to achieve a desired ROI. First, calculate the target annual net income by multiplying the purchase price by the desired ROI percentage. Next, estimate annual expenses, including a buffer for unexpected costs. Then, determine the monthly rent needed to meet the net income goal by dividing the target annual income by 12. Finally, compare this figure to market rents and adjust as necessary. For example, if the calculation suggests a $1,800 monthly rent but comparables average $1,600, the agent might set rent at $1,700, slightly above market to attract tenants willing to pay a premium for added value.

Caution must be exercised when relying solely on ROI to set rent, as it assumes consistent occupancy and stable expenses, which may not always hold true. Vacancy rates, unexpected repairs, and market fluctuations can impact actual returns. Agents should advise investors to build a contingency fund into their calculations, typically 5–10% of annual expenses, to account for these variables. Additionally, long-term ROI may be enhanced by periodic rent increases aligned with market trends, but these must be balanced against tenant retention and legal rent control regulations. This proactive approach ensures sustainability and resilience in the investment strategy.

Ultimately, setting rent to achieve a desired ROI based on property purchase price is a strategic process that blends financial analysis with market insight. By calculating target income, estimating expenses, and benchmarking against comparables, agents can establish rent levels that meet investor goals while remaining competitive. However, flexibility and foresight are essential to navigate uncertainties and optimize long-term returns. This method not only maximizes profitability but also positions the property as a viable and attractive option in the rental market.

Understanding Pennsylvania's Assignment of Rents Document: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Vacancy and Turnover Costs: Accounting for potential vacancy periods and turnover expenses in rent calculations

Real estate agents must factor in vacancy and turnover costs when calculating rent to ensure profitability and sustainability. These costs, often overlooked by novice investors, can significantly impact cash flow and overall return on investment. Vacancy periods, during which a property sits unoccupied, result in lost rental income, while turnover expenses—such as cleaning, repairs, and marketing—add up quickly. Ignoring these factors can lead to financial strain, making it essential to incorporate them into rent calculations from the outset.

To account for vacancy costs, agents typically estimate a vacancy rate based on market trends and historical data. For instance, if a property is in an area with an average vacancy rate of 7%, the agent would set aside 7% of the annual rent as a buffer. This reserve ensures that even during unoccupied months, the property owner can cover mortgage payments, taxes, and other fixed expenses. For a property renting at $1,500 per month, this would equate to $12,750 in annual rent, with $892.50 allocated for potential vacancy losses. This proactive approach prevents cash flow disruptions and provides a safety net for unexpected downturns.

Turnover expenses, on the other hand, require a more detailed analysis. Agents should itemize costs such as professional cleaning ($200–$400), minor repairs ($300–$500), painting ($1,000–$2,000), and marketing ($200–$500 per vacancy). For a typical turnover, these expenses can total $2,000–$3,500. To offset these costs, agents often spread them across the lease term. For example, if turnover occurs every 2–3 years, an additional $83–$146 per month (based on $3,000 in expenses) can be added to the rent. This ensures that funds are available when a tenant moves out, minimizing out-of-pocket expenses for the landlord.

A comparative analysis reveals that properties with higher turnover rates or in competitive markets may require larger buffers. For instance, student housing or short-term rentals often experience higher vacancy and turnover, necessitating a 10–15% vacancy reserve and higher monthly rent to cover expenses. In contrast, long-term rentals in stable markets may only need a 5% reserve. Agents must tailor their calculations to the property’s specific risks and market dynamics, avoiding a one-size-fits-all approach.

In conclusion, accounting for vacancy and turnover costs is a critical step in rent calculation that ensures financial stability and long-term success. By estimating vacancy rates, itemizing turnover expenses, and adjusting rent accordingly, real estate agents can protect their clients’ investments and maintain consistent cash flow. This meticulous approach not only safeguards against unforeseen losses but also positions the property as a competitive and profitable asset in the rental market.

Rent Party in 'Blacker the Berry': Unpacking Cultural Significance

You may want to see also

Explore related products

![]()

Local Rent Control Laws: Adjusting rent to comply with local regulations and rent stabilization policies

Real estate agents must navigate a complex web of local rent control laws when calculating rent, as these regulations directly impact the rental amounts they can legally charge. Rent control and stabilization policies vary widely by city, county, or state, often dictating maximum allowable rent increases, tenant protections, and lease renewal terms. For instance, in New York City, rent-stabilized apartments can only increase rent by a percentage set annually by the Rent Guidelines Board, typically ranging from 1% to 5% for one-year leases. Ignoring these rules can result in fines, legal disputes, or even the loss of rental income.

To comply with local rent control laws, agents must first identify whether the property falls under regulated categories, such as rent-stabilized or rent-controlled units. This requires researching local ordinances, consulting legal experts, or using databases like those provided by the Department of Housing and Community Development. For example, in San Francisco, properties built before 1979 are often subject to rent control, while newer constructions may be exempt. Agents must also track annual rent increase caps, which may be tied to inflation rates or predetermined percentages, as seen in Oregon’s statewide rent control law limiting increases to 7% plus inflation.

Once the regulatory framework is understood, agents must adjust their rent calculations accordingly. This involves subtracting any prohibited increases from the desired market rent and ensuring lease agreements explicitly state compliance with local laws. For instance, in Los Angeles, rent increases for rent-stabilized units are capped at 3% to 8% annually, depending on inflation. Agents should also be aware of "vacancy control" vs. "vacancy decontrol" jurisdictions. In vacancy-controlled areas like Santa Monica, rent increases are limited even after a tenant moves out, whereas in decontrolled areas, rents can reset to market rates upon vacancy.

A critical step in this process is maintaining detailed records of rent adjustments, lease renewals, and communications with tenants. This documentation serves as evidence of compliance during audits or disputes. For example, if a tenant challenges a rent increase in a rent-stabilized unit in Washington, D.C., the agent must provide proof that the increase adheres to the local 3% cap. Additionally, agents should educate tenants about their rights under rent control laws to foster transparency and reduce the risk of legal challenges.

Finally, agents must stay updated on changes to local rent control policies, as these laws frequently evolve in response to housing market dynamics. Subscribing to legal updates, attending workshops, or joining local real estate associations can help agents remain informed. For instance, California’s Tenant Protection Act of 2019 introduced statewide rent caps and just-cause eviction requirements, significantly altering how agents calculate and adjust rents. Proactive compliance not only ensures legal adherence but also builds trust with tenants and safeguards the property’s long-term value.

QuickBooks Tips: Choosing the Right Account for Renting Outside Activity Spaces

You may want to see also

Frequently asked questions

Real estate agents typically calculate rent by considering factors such as local market rates, property size, location, condition, amenities, and comparable rental properties (comps) in the area.

The local rental market heavily influences rent prices. Agents analyze supply and demand, vacancy rates, and recent rental transactions to ensure the price is competitive and aligns with market trends.

While there’s no universal formula, agents often use methods like the 1% rule (rent should be about 1% of the property’s purchase price) or compare the property to similar rentals in the area to determine a fair price.

Properties in better condition or with desirable amenities (e.g., parking, laundry, updated appliances) can command higher rents. Agents factor in these features when setting the price.

Yes, agents may adjust rent based on tenant demand. High demand for rentals in a specific area or property type can lead to higher prices, while low demand may result in lower rents or incentives.