Recording rent expenses on a balance sheet involves categorizing the payment as a short-term liability if it is due within the next accounting period, typically listed under accrued expenses or accounts payable. If the rent expense is prepaid, it is recorded as a current asset under prepaid expenses until the rental period is realized. For long-term leases, the present value of future lease payments may be capitalized as a right-of-use asset and a corresponding lease liability on the balance sheet, in accordance with accounting standards like ASC 842 or IFRS 16. Proper classification ensures accurate financial reporting and compliance with accounting principles.

| Characteristics | Values |

|---|---|

| Account Type | Rent expense is recorded as an operating expense on the income statement, not directly on the balance sheet. |

| Balance Sheet Impact | Rent expense indirectly affects the balance sheet by reducing retained earnings (net income) and, consequently, equity. |

| Prepaid Rent | If rent is paid in advance, it is recorded as a current asset (Prepaid Rent) on the balance sheet until the rental period is consumed. |

| Journal Entry (Expense) | Debit: Rent Expense (Income Statement) Credit: Cash/Accounts Payable (Balance Sheet) |

| Journal Entry (Prepaid Rent) | Debit: Prepaid Rent (Balance Sheet) Credit: Cash (Balance Sheet) |

| Amortization of Prepaid Rent | When prepaid rent is consumed, debit Rent Expense and credit Prepaid Rent, reducing the asset and recognizing the expense. |

| Classification | Rent expense is classified as an operating expense, reflecting the cost of using rented assets for business operations. |

| Frequency | Recorded periodically (e.g., monthly) based on the rental agreement terms. |

| Tax Treatment | Rent expense is generally tax-deductible, reducing taxable income. |

| Disclosure | Rent commitments (e.g., future lease payments) may be disclosed in the notes to the financial statements. |

Explore related products

What You'll Learn

- Rent Classification: Determine if rent is prepaid, accrued, or due; classify as current or long-term liability

- Prepaid Rent: Record advance payments as assets; amortize over the rental period

- Accrued Rent: Recognize unpaid rent expenses as liabilities at period-end

- Journal Entries: Debit rent expense, credit cash/prepaid rent/accrued rent based on timing

- Balance Sheet Impact: Prepaid rent as asset; accrued rent as liability; no direct equity impact

![]()

Rent Classification: Determine if rent is prepaid, accrued, or due; classify as current or long-term liability

When recording rent expenses on a balance sheet, proper classification is crucial for accurate financial reporting. Rent can be categorized into three main types: prepaid, accrued, or due, each requiring distinct treatment. Prepaid rent occurs when a tenant pays rent in advance for a future period. This amount is recorded as a current asset on the balance sheet because it represents a benefit that will be consumed within the next 12 months. For example, if a company pays $12,000 for the next six months of rent, $6,000 would be recorded as prepaid rent (asset) and $6,000 as rent expense for the current period.

Accrued rent, on the other hand, refers to rent expenses that have been incurred but not yet paid. This is recorded as a current liability on the balance sheet, as it represents an obligation due within the next year. For instance, if a company occupies a space in December but pays rent in January, the December rent is accrued as a liability at year-end. The journal entry would debit rent expense and credit accrued rent payable. This ensures that expenses are matched to the period in which they are incurred, adhering to the accrual accounting principle.

Rent due is the simplest classification, representing rent that is currently payable. It is recorded as a current liability if payment is due within 12 months or as a long-term liability if it extends beyond that period. For example, if a lease agreement requires monthly payments, each month’s rent is classified as a current liability until paid. However, if a lease spans multiple years with payments due beyond 12 months, the portion due after one year is classified as a long-term liability, while the current year’s payments remain under current liabilities.

Classifying rent as a current or long-term liability depends on the timing of the payment obligation. Current liabilities are obligations expected to be settled within one year or the operating cycle, whichever is longer. Rent payments due within this timeframe fall under current liabilities. Conversely, long-term liabilities are obligations due beyond one year. For example, if a lease agreement spans five years, the rent payable after the first year is classified as a long-term liability, while the first year’s payments are current. This distinction ensures the balance sheet accurately reflects short-term and long-term financial obligations.

To summarize, rent classification involves determining whether it is prepaid, accrued, or due, followed by categorizing it as a current or long-term liability based on payment timing. Prepaid rent is an asset, accrued rent is a current liability, and rent due is classified based on its payment timeline. Proper classification ensures compliance with accounting standards and provides a clear picture of a company’s financial position. By meticulously recording rent expenses, businesses maintain transparency and accuracy in their financial statements.

Ace Rentals: Under 25 in Puerto Rico?

You may want to see also

Explore related products

![]()

Prepaid Rent: Record advance payments as assets; amortize over the rental period

When dealing with prepaid rent, it's essential to understand that advance payments for rent should be recorded as assets on the balance sheet. This is because the payment represents a future economic benefit that the company will receive over the rental period. To properly account for prepaid rent, you need to follow a systematic approach that involves initial recognition and subsequent amortization. At the time of payment, you would debit the prepaid rent account (an asset account) and credit the cash account, reflecting the outflow of cash and the creation of an asset.

The prepaid rent account is classified as a current asset on the balance sheet, assuming the rental period is within one year. If the rental period extends beyond one year, a portion of the prepaid rent may be classified as a long-term asset. This classification is crucial for financial reporting purposes, as it provides a clear picture of the company's short-term and long-term financial obligations. By recording prepaid rent as an asset, you ensure that the company's financial statements accurately represent its financial position and the resources it controls.

Amortization of prepaid rent is the process of systematically allocating the prepaid amount as rent expense over the rental period. This is done to match the expense with the period in which the benefit is received, in accordance with the matching principle of accounting. To amortize prepaid rent, you would debit the rent expense account (an expense account) and credit the prepaid rent account, reducing the asset balance and recognizing the expense. The amortization schedule should be based on the specific terms of the lease agreement, ensuring that the rent expense is recognized evenly over the rental period.

For example, if a company pays $12,000 in advance for a one-year lease, it would record the prepaid rent as an asset on the balance sheet. Each month, the company would amortize $1,000 ($12,000 / 12 months) by debiting rent expense and crediting prepaid rent. This process continues until the prepaid rent balance is fully amortized, and the asset is reduced to zero. By following this approach, the company ensures that its financial statements accurately reflect the rent expense and the remaining prepaid rent asset.

It's important to note that the amortization of prepaid rent should be reviewed periodically to ensure accuracy. If there are any changes to the lease agreement or rental period, adjustments may be necessary to reflect the updated terms. Additionally, companies should establish internal controls to monitor and manage prepaid rent, ensuring that advance payments are properly recorded, amortized, and reconciled. By maintaining accurate records and following a consistent amortization process, companies can effectively manage their prepaid rent and ensure compliance with accounting standards.

In summary, recording prepaid rent as an asset and amortizing it over the rental period is a critical aspect of accounting for rent expenses on a balance sheet. By following a systematic approach that involves initial recognition, classification, and amortization, companies can ensure that their financial statements accurately reflect their financial position and the resources they control. Proper management of prepaid rent not only ensures compliance with accounting standards but also provides valuable insights into a company's short-term and long-term financial obligations.

Renting Rights: Understanding Your Legal Protections

You may want to see also

Explore related products

![]()

Accrued Rent: Recognize unpaid rent expenses as liabilities at period-end

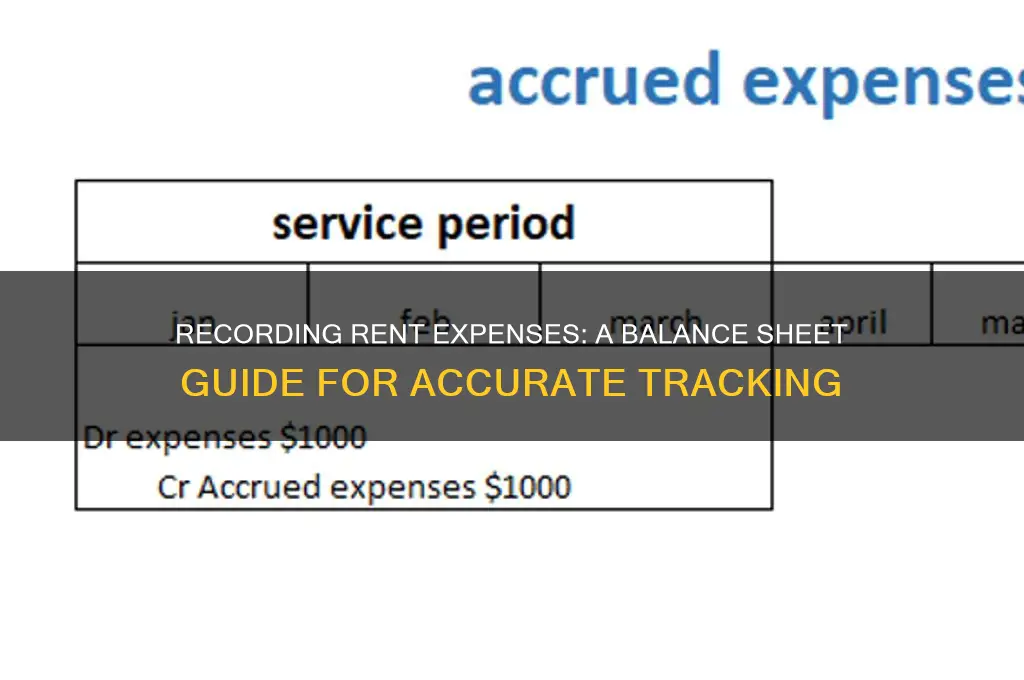

Accrued rent is a critical concept in accounting that ensures a company’s financial statements accurately reflect its financial obligations, even if payment has not yet been made. When rent expenses are incurred but remain unpaid at the end of an accounting period, they must be recognized as liabilities on the balance sheet. This process aligns with the accrual accounting principle, which requires expenses to be recorded in the period they are incurred, regardless of when payment is made. To record accrued rent, the accountant must first identify the amount of rent owed for the period. This is typically calculated based on the lease agreement and the number of days or months the rent covers. For example, if a company occupies a property from the 1st to the 25th of a month but pays rent on the 1st of the following month, the rent for the 25 days must be accrued at the end of the current period.

The journal entry to record accrued rent involves debiting the "Rent Expense" account, which is an income statement account, and crediting the "Accrued Rent Payable" account, which is a liability account on the balance sheet. For instance, if the accrued rent for the period is $5,000, the entry would be: *Debit Rent Expense $5,000, Credit Accrued Rent Payable $5,000*. This entry ensures that the expense is recognized in the current period, and the liability is reported on the balance sheet. It is essential to ensure that the amount accrued is accurate, as over- or under-accruing rent can distort financial statements and misrepresent the company’s financial health.

At the time of payment, the accrued rent liability is reversed. When the company pays the rent in the subsequent period, the accountant debits the "Accrued Rent Payable" account and credits the "Cash" account. Using the previous example, the entry would be: *Debit Accrued Rent Payable $5,000, Credit Cash $5,000*. This removes the liability from the balance sheet and reflects the outflow of cash. Properly managing this reversal is crucial to avoid double-counting expenses or liabilities in the financial statements.

Accrued rent is particularly important for companies with lease agreements that span multiple accounting periods. It ensures that the matching principle is upheld, where expenses are matched with the revenues they help generate in the same period. For example, if a retail store incurs rent for a month during which it generates sales, recognizing the rent expense in that month provides a more accurate picture of profitability. Failure to accrue rent would result in understated expenses and overstated net income in the current period, followed by the opposite effect in the subsequent period when the payment is made.

Finally, maintaining accurate records of accrued rent is essential for financial reporting, audits, and decision-making. Auditors often scrutinize accrued expenses to ensure compliance with accounting standards, such as GAAP or IFRS. Companies should establish clear policies and procedures for identifying, calculating, and recording accrued rent to minimize errors and ensure consistency. Regular reviews of lease agreements and rent schedules can also help in accurately determining the amounts to be accrued. By properly recognizing unpaid rent expenses as liabilities, companies can maintain transparency and reliability in their financial statements.

Renting Mike Tyson's Fight: A Step-by-Step Guide for Fans

You may want to see also

Explore related products

![]()

Journal Entries: Debit rent expense, credit cash/prepaid rent/accrued rent based on timing

Recording rent expenses on a balance sheet involves specific journal entries that depend on the timing of the payment and the accounting method used. The key principle is to match the expense with the period in which it is incurred, ensuring accurate financial reporting. Here’s how to record rent expenses using journal entries, focusing on debiting rent expense and crediting cash, prepaid rent, or accrued rent based on timing.

When Rent is Paid in Advance (Prepaid Rent):

If rent is paid before the rental period begins, it is recorded as a prepaid expense. In this case, the journal entry involves debiting the prepaid rent account (an asset) and crediting the cash account. For example, if a company pays $12,000 for six months of rent in advance, the entry would be: *Debit Prepaid Rent $12,000, Credit Cash $12,000*. As each month passes, the prepaid rent is recognized as an expense. The adjusting entry would be: *Debit Rent Expense $2,000, Credit Prepaid Rent $2,000*. This ensures the expense is matched to the period it benefits.

When Rent is Paid in the Same Period (Cash Basis):

If rent is paid in the same period it is incurred, the expense is recorded directly. The journal entry involves debiting rent expense (an expense account) and crediting cash. For instance, if a company pays $2,000 for the current month’s rent, the entry would be: *Debit Rent Expense $2,000, Credit Cash $2,000*. This method is straightforward and commonly used by small businesses or when the payment aligns with the rental period.

When Rent is Accrued (Accrued Rent):

If rent is owed but not yet paid at the end of an accounting period, it is recorded as an accrued expense. The journal entry involves debiting rent expense and crediting accrued rent (a liability account). For example, if $1,500 of rent is due but unpaid at month-end, the entry would be: *Debit Rent Expense $1,500, Credit Accrued Rent $1,500*. When the rent is paid in the following period, the entry would be: *Debit Accrued Rent $1,500, Credit Cash $1,500*. This ensures the expense is recognized in the correct period, adhering to the accrual accounting principle.

Adjusting Entries for Timing Differences:

Adjusting entries are crucial to align rent expenses with the periods they relate to. For prepaid rent, the adjusting entry transfers the expense from the asset account to the expense account over time. For accrued rent, the adjusting entry recognizes the expense before payment. These entries ensure the balance sheet and income statement reflect the true financial position and performance of the business. Proper timing in recording rent expenses is essential for compliance with accounting standards and accurate financial reporting.

In summary, recording rent expenses on a balance sheet requires careful consideration of timing. Whether debiting rent expense and crediting cash, prepaid rent, or accrued rent, the goal is to match the expense with the period it benefits. Understanding these journal entries ensures that financial statements are accurate and reflective of the business’s financial health.

Renting History: A Prerequisite for Buying Land?

You may want to see also

Explore related products

![]()

Balance Sheet Impact: Prepaid rent as asset; accrued rent as liability; no direct equity impact

When recording rent expenses on a balance sheet, it’s essential to understand how prepaid rent and accrued rent impact the financial statement. Prepaid rent occurs when a tenant pays rent in advance for a future period. This amount is not immediately recognized as an expense but is instead recorded as a current asset on the balance sheet. The rationale is that the tenant has paid for a benefit that will be consumed over time. For example, if a company pays $12,000 for six months of rent in advance, $12,000 is recorded as a prepaid rent asset. As each month passes, $2,000 is expensed, and the prepaid rent asset is reduced by the same amount. This ensures the expense is matched to the period in which the benefit is received, aligning with the accrual accounting principle.

On the other hand, accrued rent represents rent expenses that have been incurred but not yet paid. This is recorded as a current liability on the balance sheet, reflecting the obligation to pay the landlord. For instance, if a company occupies a property for a month but has not yet paid the $2,000 rent, an accrued rent liability of $2,000 is recorded, along with a rent expense of $2,000. When the payment is made, the liability is reduced, and cash is decreased. Accrued rent ensures that expenses are recognized in the period they are incurred, regardless of when the payment is made, maintaining the accuracy of financial statements.

Importantly, neither prepaid rent nor accrued rent directly impacts the equity section of the balance sheet. Equity represents the owners’ residual interest in the assets after deducting liabilities, and rent transactions do not alter ownership claims. Prepaid rent increases assets, while accrued rent increases liabilities, both of which affect the overall financial position but not equity. However, the rent expense associated with these transactions will eventually flow through the income statement, impacting retained earnings (a component of equity) over time.

The balance sheet impact of these rent transactions is straightforward: prepaid rent is an asset, accrued rent is a liability, and neither directly affects equity. This treatment ensures that the balance sheet remains balanced, with assets equaling liabilities plus equity. For example, if a company has $5,000 in prepaid rent and $3,000 in accrued rent, the net effect is an increase in assets by $5,000 and an increase in liabilities by $3,000, with no change to equity. This clear classification helps stakeholders understand the company’s short-term financial obligations and resources related to rent.

In summary, recording rent expenses on a balance sheet involves classifying prepaid rent as a current asset and accrued rent as a current liability, with no direct impact on equity. Prepaid rent reflects advance payments for future benefits, while accrued rent represents unpaid obligations. Both treatments adhere to accrual accounting principles, ensuring expenses and liabilities are recognized in the appropriate periods. By properly categorizing these items, companies maintain transparency and accuracy in their financial reporting, providing a clear picture of their financial health.

Boating in Wisconsin: License Requirements for Renters

You may want to see also

Frequently asked questions

Rent expense is not directly recorded on a balance sheet. It is an income statement item, reflecting the cost of renting property over a specific period. However, prepaid rent (rent paid in advance) is recorded as a current asset on the balance sheet until it is expensed over time.

Prepaid rent is recorded as a current asset on the balance sheet under the "Prepaid Expenses" or "Other Current Assets" section. It represents rent paid in advance and is gradually expensed to the income statement as the rental period progresses.

Once rent is paid, it is initially recorded as a prepaid expense (asset) if paid in advance. As the rental period elapses, the prepaid rent is expensed to the income statement as "Rent Expense," reducing the asset balance on the balance sheet.

Rent expense is treated as an operating expense on the income statement, reflecting the cost of using rented property. If rent is paid in advance, the prepaid portion is recorded as an asset on the balance sheet and expensed over the rental period using the matching principle.