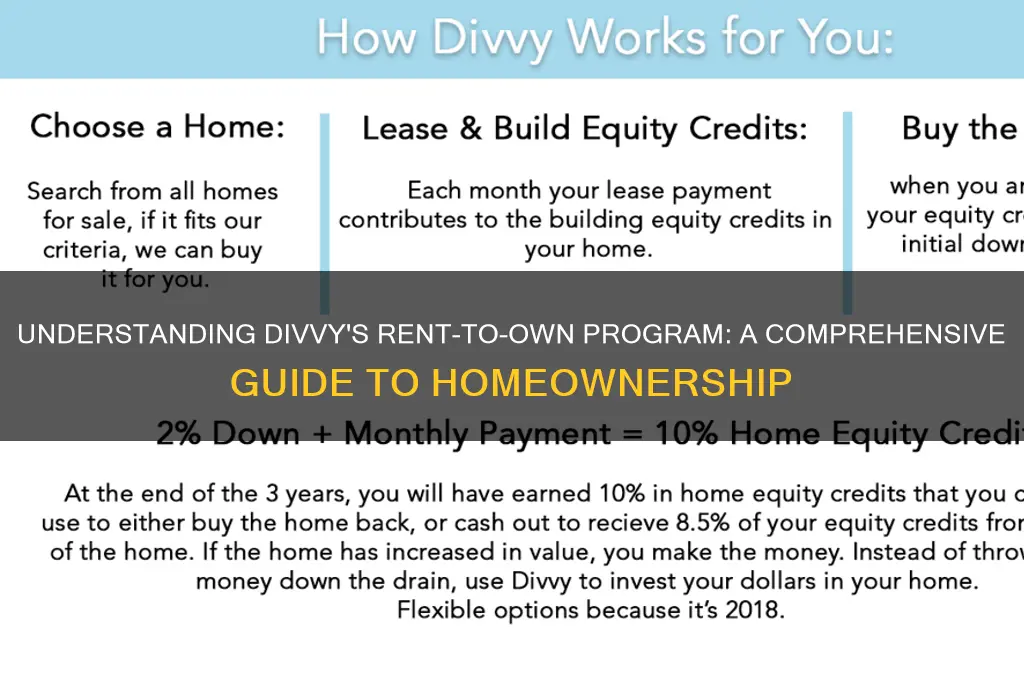

Divvy's rent-to-own program offers a unique pathway to homeownership for those who may not qualify for a traditional mortgage or prefer a more flexible approach. It works by allowing renters to move into a home immediately, with a portion of their monthly rent payments going toward building equity in the property. After a set period, typically three years, renters have the option to purchase the home at a pre-agreed price, using the accumulated equity as a down payment. This model eliminates the need for a large upfront down payment and provides time to improve credit or save additional funds, making homeownership more accessible and achievable for many.

Explore related products

What You'll Learn

- Eligibility Requirements: Credit score, income verification, and employment status needed to qualify for Divvy's program

- Monthly Payments: Rent, home equity savings, and portion applied toward purchase price breakdown

- Lease Term: Standard 3-year lease with option to buy or renew annually

- Purchase Process: How to exercise the purchase option and finalize home ownership

- Maintenance Responsibilities: Tenant duties for repairs, upkeep, and property maintenance during the lease

![]()

Eligibility Requirements: Credit score, income verification, and employment status needed to qualify for Divvy's program

Divvy's rent-to-own program is designed to be more accessible than traditional mortgage options, but it still requires applicants to meet specific eligibility criteria. One of the primary factors is your credit score. Unlike conventional home loans that often demand scores above 620, Divvy’s program is more flexible, typically accepting scores as low as 550. This lower threshold opens the door for individuals with less-than-perfect credit histories, though it’s important to note that a higher score may improve your chances of approval and potentially secure more favorable terms.

Income verification is another critical component of Divvy’s eligibility requirements. Applicants must provide proof of steady income to demonstrate their ability to make monthly payments. This typically involves submitting recent pay stubs, tax returns, or bank statements. Divvy generally looks for an income-to-debt ratio that ensures you can comfortably afford the rent-to-own payments while managing other financial obligations. For example, if your monthly income is $4,000, your total debt payments (including the Divvy payment) should ideally not exceed $1,600 to maintain a healthy 40% ratio.

Your employment status also plays a significant role in qualifying for Divvy’s program. While traditional lenders often prefer full-time, salaried employees, Divvy is more accommodating of alternative employment arrangements. Freelancers, gig workers, and self-employed individuals can qualify as long as they can provide consistent proof of income. However, those with unstable or sporadic income may face additional scrutiny or be required to meet higher income thresholds to compensate for the perceived risk.

To maximize your chances of approval, consider these practical tips: First, review your credit report for inaccuracies and dispute any errors before applying. Second, gather all necessary income documentation in advance to streamline the verification process. Finally, if your employment status is non-traditional, prepare a detailed explanation of your income sources and stability to reassure Divvy of your financial reliability. By addressing these eligibility requirements proactively, you can position yourself as a strong candidate for Divvy’s rent-to-own program.

Average U-Haul Truck Rental Costs: What to Expect When Moving

You may want to see also

Explore related products

![]()

Monthly Payments: Rent, home equity savings, and portion applied toward purchase price breakdown

Divvy's rent-to-own model revolutionizes the path to homeownership by breaking down monthly payments into three distinct components: rent, home equity savings, and a portion applied toward the purchase price. This structure not only makes homeownership more accessible but also provides clarity and financial discipline for aspiring homeowners. Let’s dissect how each component works and why it matters.

Rent: The first portion of your monthly payment covers the rent, which is the cost of living in the home. Unlike traditional renting, Divvy calculates this amount based on the home’s market value and local rental rates. For example, if the home’s market rent is $1,800 per month, this is the baseline you’ll pay for occupancy. Think of this as your "cost of living" in the home, similar to any rental agreement. However, the key difference is that this payment is not just an expense—it’s part of a larger strategy to build equity.

Home Equity Savings: Here’s where Divvy stands out. A portion of your monthly payment is allocated to a dedicated savings account, which acts as your home equity fund. Typically, this amount ranges from $100 to $500 per month, depending on your financial situation and the home’s value. For instance, if your monthly payment is $2,200, $400 might go into this savings account. This fund grows over time and is used as a down payment when you’re ready to purchase the home. It’s a forced savings mechanism that ensures you’re actively building equity with every payment.

Portion Applied Toward Purchase Price: The final component is the amount that directly reduces the home’s purchase price. This is often the smallest portion of the monthly payment but carries significant long-term value. For example, if your total monthly payment is $2,200, and $1,800 covers rent while $400 goes into savings, the remaining $200 might be applied toward reducing the home’s purchase price. Over a 3-year term, this could reduce the price by $7,200, making the home more affordable when you’re ready to buy.

To illustrate, consider a $300,000 home. Your monthly payment might break down as follows: $1,800 (rent), $400 (equity savings), and $200 (purchase price reduction). Over 3 years, you’d save $14,400 in equity and reduce the purchase price by $7,200, effectively lowering the amount you need to finance to $278,400. This structured approach not only makes homeownership more attainable but also educates participants on financial planning and equity building.

Practical tip: To maximize this program, aim to increase your equity savings contribution whenever possible. Even an extra $50 per month can significantly boost your down payment fund. Additionally, treat the portion applied toward the purchase price as a long-term investment—it’s a silent partner in reducing your future mortgage burden. By understanding and optimizing these three components, you’re not just renting a home; you’re strategically paving the way to ownership.

Understanding Gross Rent in Commercial Real Estate: Definition and Implications

You may want to see also

Explore related products

![]()

Lease Term: Standard 3-year lease with option to buy or renew annually

Divvy's rent-to-own program hinges on a structured lease term designed to balance flexibility and commitment. The standard 3-year lease forms the backbone of this model, offering tenants a clear timeline to build equity while renting. This period is neither too short to feel rushed nor too long to feel trapped, striking a pragmatic middle ground for those exploring homeownership.

Consider the mechanics: during these 3 years, a portion of your monthly rent is allocated to a "purchase credit." This credit accumulates, reducing the home's purchase price if you decide to buy. For instance, if your monthly rent is $2,000 and $500 goes toward the credit, you’ll have $18,000 toward the down payment by the end of the term. This structured saving mechanism differentiates Divvy from traditional renting, where every dollar paid disappears into the landlord’s pocket.

However, the 3-year term isn’t set in stone. Divvy builds in annual renewal options, providing an escape hatch for those whose circumstances change. Life happens—job relocations, financial shifts, or simply a change of heart—and the ability to renew annually ensures you’re not locked into a long-term commitment if homeownership no longer aligns with your goals. This flexibility is a safety net, reducing the risk of feeling trapped in a contract.

A critical takeaway is the importance of timing. If you’re confident about buying within 3 years, the program maximizes your equity-building potential. But if your timeline is uncertain, treat the annual renewal as a checkpoint to reassess. For example, if you’re 2 years in and realize you’re not ready to buy, renewing for another year allows you to continue building credit without losing progress. Conversely, if you’re ahead of schedule, you can exercise the purchase option early, provided you’ve met the minimum credit requirements.

Practical tip: Use the 3-year term as a financial planning horizon. Calculate how much purchase credit you’ll accumulate and align it with your savings goals. For instance, if you aim to save $20,000 for a down payment, ensure your monthly allocation and timeline align with this target. Additionally, monitor your credit score during this period, as it’s a key factor in securing a mortgage when you’re ready to buy. The 3-year lease isn’t just a contract—it’s a roadmap to homeownership, with built-in flexibility for life’s unpredictability.

Understanding HUD's Gross Rent Calculation for PBV Programs

You may want to see also

Explore related products

![]()

Purchase Process: How to exercise the purchase option and finalize home ownership

Exercising the purchase option in a rent-to-own agreement with Divvy marks the culmination of your journey toward homeownership. This process begins with a clear understanding of your agreement terms, which outline the specific conditions under which you can transition from renting to owning. Typically, these terms include a predetermined purchase price, the duration of the rental period, and the portion of your monthly payments that contribute to the down payment. Reviewing these details ensures you’re fully prepared to take the next step.

Once you’ve decided to exercise the purchase option, the first actionable step is to notify Divvy in writing, expressing your intent to buy the home. This triggers a formal process where Divvy will provide you with an updated purchase agreement reflecting any changes in the home’s value or terms since the agreement began. It’s crucial to secure financing at this stage, whether through a mortgage lender or other means, as you’ll need to cover the remaining balance of the home’s purchase price. Divvy often works with preferred lenders to streamline this process, but you’re free to shop around for the best rates and terms.

A critical aspect of finalizing homeownership is the appraisal and inspection. Even if Divvy has maintained the property, it’s wise to conduct an independent inspection to identify any issues that may affect the home’s value or your decision to proceed. Simultaneously, an appraisal ensures the purchase price aligns with the home’s current market value, protecting both you and the lender. If discrepancies arise, negotiate with Divvy to adjust the terms or address necessary repairs before closing.

Closing the deal involves standard real estate procedures, including signing legal documents, paying closing costs, and transferring the title into your name. Divvy will coordinate with a title company or attorney to facilitate this process, ensuring all paperwork is in order. Be prepared for closing costs, which typically range from 2% to 5% of the home’s purchase price, and factor these expenses into your budget. Once completed, you’ll officially own the home, and your rent-to-own journey will transition into full-fledged homeownership.

Finally, reflect on the advantages of this process: it provides a structured path to ownership, builds equity over time, and offers flexibility for those who may not qualify for a mortgage initially. However, remain vigilant about meeting payment deadlines and maintaining the property, as these factors directly impact your ability to finalize the purchase. With careful planning and adherence to the agreement, exercising the purchase option becomes a rewarding milestone in achieving your homeownership goals.

Early Lease Termination: Steps for Renters to Vacate Legally

You may want to see also

Explore related products

![]()

Maintenance Responsibilities: Tenant duties for repairs, upkeep, and property maintenance during the lease

Tenants in a rent-to-own agreement with Divvy assume a unique blend of renter and homeowner responsibilities, particularly when it comes to maintenance. Unlike traditional renting, where landlords handle most repairs, Divvy tenants are expected to take a proactive role in keeping the property in good condition. This includes routine tasks like changing air filters every 1–3 months, depending on usage and filter type, and ensuring that gutters are cleared at least twice a year to prevent water damage. Neglecting these duties can lead to costly repairs that may affect your ability to eventually purchase the home.

Consider the seasonal upkeep required to maintain the property’s value. In winter, tenants should insulate pipes to prevent freezing and clear snow from walkways promptly to avoid liability issues. During summer, mowing the lawn weekly and trimming hedges every 4–6 weeks are essential to keep the exterior presentable. These tasks not only preserve the home’s condition but also demonstrate your commitment to the property, which can strengthen your case when it’s time to exercise the purchase option.

While tenants are responsible for minor repairs, such as fixing leaky faucets or replacing light bulbs, major issues like roof damage or HVAC failures typically fall under the landlord’s purview. However, tenants must report these problems immediately to prevent further damage. For instance, a small roof leak, if ignored, can lead to mold growth, which is far more expensive to remedy. Divvy’s program often includes a maintenance reserve fund, but tenants should clarify how and when this fund can be accessed to avoid out-of-pocket expenses.

A comparative analysis reveals that Divvy’s maintenance expectations align more closely with homeownership than traditional renting. For example, while renters might wait for a landlord to fix a broken appliance, Divvy tenants are encouraged to address such issues promptly, either through self-repair or hiring a professional. This shift in responsibility prepares tenants for the realities of owning a home, where proactive maintenance is key to avoiding long-term costs.

In conclusion, understanding and fulfilling maintenance responsibilities is critical in a Divvy rent-to-own agreement. By treating the property as if it were already yours, you not only protect its value but also build the skills and habits necessary for successful homeownership. Keep a detailed log of all maintenance activities, as this documentation can be valuable when transitioning from renter to owner.

Mid-Month Rent Due? Tips to Manage Your Budget Effectively

You may want to see also

Frequently asked questions

Divvy's rent-to-own program allows you to move into a home you love while you work towards qualifying for a mortgage. You rent the home with the option to purchase it later, and a portion of your rent payments goes toward the down payment if you decide to buy.

First, you apply and get approved by Divvy. Then, Divvy purchases the home you choose. You move in as a renter, paying monthly rent, and a portion of that rent is credited toward your future down payment. You have the option to buy the home within 3-5 years, using the accumulated credits.

Eligibility requirements include a minimum credit score (typically around 550), stable income, and the ability to cover the initial rent and fees. Divvy also evaluates your financial situation to ensure you’re on track to qualify for a mortgage by the end of the term.

A portion of your monthly rent, typically 5-10%, is credited toward your down payment if you decide to purchase the home. The exact percentage depends on your agreement with Divvy.

If you choose not to purchase the home, you can move out at the end of your lease term. However, the rent credits you’ve accumulated will not be refunded, as they are part of the option to buy the home. You’ll need to find new housing, and Divvy will sell the property.