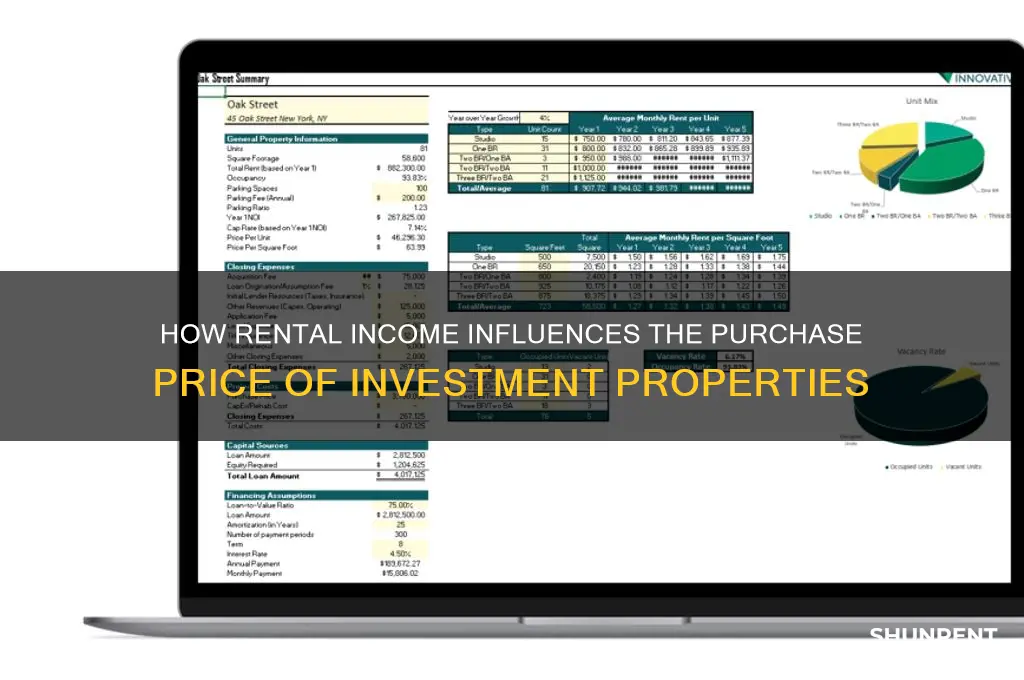

The relationship between rent and the purchase price of a rental building is a critical aspect of real estate investment, as it directly influences the property's valuation and potential return on investment. Essentially, the purchase price of a rental building is often determined by its income-generating potential, which is primarily driven by the rental income it can produce. Investors and appraisers commonly use methods like the Gross Rent Multiplier (GRM) or the capitalization rate (cap rate) to assess this value, where the GRM compares the property’s price to its annual rental income, and the cap rate measures the property’s net operating income relative to its purchase price. Higher rents typically justify a higher purchase price, assuming stable occupancy and market demand, while factors such as location, property condition, and operating expenses also play significant roles in the final valuation. Understanding this dynamic is essential for both buyers and sellers to make informed decisions in the rental property market.

Explore related products

What You'll Learn

- Market Rent Comparison: Analyze current rental rates to assess building's income potential and value

- Capitalization Rate (Cap Rate): Calculate return on investment using net operating income and purchase price

- Gross Rent Multiplier (GRM): Estimate value by comparing sale price to annual rental income

- Operating Expenses Impact: Evaluate how maintenance, taxes, and utilities affect net income and price

- Vacancy and Risk Adjustment: Factor in potential vacancies and market risks to determine fair purchase price

![]()

Market Rent Comparison: Analyze current rental rates to assess building's income potential and value

When evaluating the purchase price of a rental building, Market Rent Comparison is a critical step in assessing the property's income potential and overall value. This process involves analyzing current rental rates in the surrounding area to determine how the subject property stacks up against its competitors. By comparing the property's rental income to market averages, investors can gauge whether the asking price is justified or if there's room for negotiation. The first step is to gather data on comparable rental properties, including their location, size, amenities, and monthly rent. This information can be sourced from real estate listings, property management companies, or local market reports.

To conduct an effective Market Rent Comparison, it's essential to identify properties that are similar in terms of size, condition, and location. For instance, a multifamily building in an urban area should be compared to other multifamily buildings in the same neighborhood or nearby districts with similar demographics and demand drivers. Adjustments should be made for differences in unit size, lease terms, and property features, such as parking availability or on-site laundry facilities. By standardizing these variables, investors can obtain a more accurate picture of how the subject property's rental rates compare to the market. This analysis helps in estimating the property's potential gross income and identifying any gaps that may need to be addressed through rent adjustments or property improvements.

Once the comparison data is compiled, the next step is to calculate key metrics such as Gross Rent Multiplier (GRM) and Cap Rate. The GRM is derived by dividing the property's purchase price by its annual gross rental income, providing a quick snapshot of the property's value relative to its income. A lower GRM indicates a potentially better investment, assuming other factors are favorable. The Cap Rate, on the other hand, is calculated by dividing the property's net operating income (NOI) by its purchase price, offering insight into the property's potential return on investment. Comparing these metrics to those of similar properties in the market helps investors assess whether the subject property is priced competitively or if it presents an opportunity for higher returns.

Another important aspect of Market Rent Comparison is understanding the local rental market trends and demand dynamics. Factors such as population growth, employment rates, and new development projects can significantly impact rental rates and occupancy levels. For example, a building in an area with high demand and limited supply may command higher rents and justify a higher purchase price. Conversely, properties in oversaturated markets may face downward pressure on rents, affecting their income potential and valuation. By staying informed about market trends, investors can make more accurate predictions about future rental income and the property's long-term value.

Finally, Market Rent Comparison should also consider the potential for rent growth and value-add opportunities. If the subject property’s rents are below market rates, there may be an opportunity to increase income through strategic rent adjustments or property upgrades. For instance, renovating units, adding amenities, or improving curb appeal can justify higher rents and enhance the property's overall value. However, investors must balance these opportunities with the associated costs and potential risks. By thoroughly analyzing current rental rates and market conditions, investors can make informed decisions about the property's income potential and determine a fair purchase price that aligns with their investment goals.

Ocean Reef Condos: Available for Rent?

You may want to see also

Explore related products

![]()

Capitalization Rate (Cap Rate): Calculate return on investment using net operating income and purchase price

The Capitalization Rate (Cap Rate) is a critical metric used to determine the purchase price of a rental building by evaluating its potential return on investment (ROI). It is calculated by dividing the property’s Net Operating Income (NOI) by its purchase price. The formula is: Cap Rate = NOI / Purchase Price. This ratio provides investors with a clear understanding of the property’s income-generating potential relative to its cost. For example, if a building generates an NOI of $50,000 annually and is priced at $1,000,000, the cap rate would be 5% ($50,000 / $1,000,000). A higher cap rate generally indicates a higher return on investment, assuming all other factors are equal.

Rent plays a pivotal role in determining the NOI, which is a key component of the cap rate calculation. NOI is derived by subtracting operating expenses (such as maintenance, property management fees, and taxes) from the total rental income. Therefore, higher rental income directly increases the NOI, potentially leading to a more attractive cap rate. For instance, if a property’s rent increases from $5,000 to $6,000 per month, the annual NOI would rise by $12,000, assuming expenses remain constant. This increase in NOI would either justify a higher purchase price or improve the cap rate if the price remains the same.

When using the cap rate to determine the purchase price of a rental building, investors often work backward from the desired cap rate. For example, if an investor seeks a 6% cap rate and the property’s NOI is $60,000, the maximum purchase price would be $1,000,000 ($60,000 / 0.06). This approach ensures the investment aligns with the investor’s return expectations. Rent is a driving factor here, as it directly impacts the NOI and, consequently, the maximum price an investor should pay to achieve the target cap rate.

It’s important to note that cap rates are influenced by market conditions, property location, and risk factors. Properties in high-demand areas with stable rental income may have lower cap rates due to higher purchase prices, while properties in less desirable areas may offer higher cap rates to compensate for increased risk. Investors must consider these factors alongside rent and NOI when using the cap rate to evaluate a rental building’s purchase price.

In summary, the capitalization rate is a powerful tool for assessing the relationship between rent, NOI, and the purchase price of a rental building. By focusing on the cap rate, investors can make informed decisions about the property’s value and potential ROI. Rent is a foundational element in this calculation, as it directly influences the NOI, which in turn determines the cap rate and, ultimately, the property’s purchase price. Understanding this dynamic is essential for anyone looking to invest in rental properties.

Vehicle Rentals: License Requirements and Rules

You may want to see also

Explore related products

![]()

Gross Rent Multiplier (GRM): Estimate value by comparing sale price to annual rental income

The Gross Rent Multiplier (GRM) is a straightforward yet powerful tool used to estimate the value of a rental property by comparing its sale price to its annual rental income. It provides a quick snapshot of how much an investor is paying for each dollar of rental income generated by the property. The formula for GRM is simple: GRM = Property Sale Price / Annual Gross Rental Income. For example, if a building sells for $500,000 and generates $50,000 in annual rental income, the GRM would be 10 ($500,000 / $50,000). This means the investor is paying $10 for every $1 of annual rental income.

To effectively use GRM, it’s essential to understand its context and limitations. GRM is most useful for comparing similar properties within the same market. For instance, if two apartment buildings in the same neighborhood have GRMs of 8 and 12, the one with the lower GRM may be a better value, assuming other factors are equal. However, GRM does not account for operating expenses, vacancies, or financing costs, which are critical components of a property’s overall profitability. Therefore, while GRM is a quick metric, it should be used in conjunction with other financial analysis tools.

One of the key advantages of GRM is its simplicity and ease of calculation. Investors can quickly assess whether a property is priced reasonably relative to its income-generating potential. For example, if the average GRM for rental properties in a specific area is 9, and a property is listed with a GRM of 14, it may be overpriced unless it has unique features or growth potential that justify the higher multiplier. Conversely, a property with a GRM significantly below the market average could be undervalued or may have hidden issues.

It’s important to note that GRM relies on gross rental income, which is the total rental income before any expenses are deducted. This means it does not reflect the property’s net operating income (NOI) or cash flow. For a more comprehensive analysis, investors should also consider metrics like Cap Rate, which factors in operating expenses and provides a clearer picture of the property’s return on investment. However, for a quick initial assessment, GRM remains a valuable tool.

Finally, when using GRM to determine the purchase price of a rental building, investors should gather data on recent sales of comparable properties to establish a benchmark. This helps in setting a realistic GRM range for the target market. Additionally, investors should adjust their expectations based on market conditions, such as high demand or limited supply, which can drive GRMs higher. By combining GRM with other analytical methods and due diligence, investors can make more informed decisions about the value and potential of a rental property.

Business Licenses for Airbnb: Are They Necessary?

You may want to see also

Explore related products

![]()

Operating Expenses Impact: Evaluate how maintenance, taxes, and utilities affect net income and price

When evaluating the purchase price of a rental building, understanding the impact of operating expenses is crucial, as these directly affect the net income generated by the property. Operating expenses, including maintenance, taxes, and utilities, are key components that influence the overall profitability and, consequently, the building's valuation. Maintenance costs, for instance, can vary significantly depending on the age and condition of the property. Older buildings may require more frequent repairs and upgrades, which can reduce net income if not properly budgeted. Prospective buyers must assess historical maintenance records and anticipate future needs to ensure these expenses do not erode the property's cash flow. A well-maintained property not only sustains higher rents but also commands a higher purchase price due to its longevity and lower risk of unexpected costs.

Taxes are another critical operating expense that impacts the net income and purchase price of a rental building. Property taxes vary by location and are often reassessed periodically, potentially increasing over time. High property taxes can significantly reduce the net operating income (NOI), which is a primary factor in determining the building's value. Investors should analyze local tax rates, assess the potential for future increases, and factor these into their calculations. Additionally, understanding tax incentives or abatements available for rental properties in the area can provide opportunities to enhance net income and justify a higher purchase price.

Utilities, including water, electricity, gas, and waste management, also play a substantial role in operating expenses. In some rental markets, landlords are responsible for covering these costs, which can fluctuate based on usage and external factors like weather conditions. High utility expenses can diminish net income, making the property less attractive to buyers. To mitigate this, investors should evaluate the property's energy efficiency, consider upgrades to reduce utility costs, and determine if these expenses can be passed on to tenants through rent or separate billing. Properties with lower utility expenses or mechanisms to offset these costs are often valued higher in the market.

The cumulative effect of maintenance, taxes, and utilities on net income is a critical determinant of a rental building's purchase price. Investors typically use metrics like the capitalization rate (cap rate) or gross rent multiplier (GRM) to assess value, both of which are heavily influenced by NOI. Higher operating expenses reduce NOI, leading to a lower valuation, while efficient management of these costs can increase NOI and support a higher purchase price. Therefore, a thorough analysis of operating expenses is essential to accurately determine the property's worth and ensure a sound investment decision.

Finally, it is important to consider how operating expenses align with the rental income generated by the property. If rent levels are insufficient to cover these expenses and provide a reasonable return on investment, the property may be overpriced. Conversely, properties with rents that comfortably exceed operating costs are more likely to attract buyers willing to pay a premium. Investors should conduct a detailed cash flow analysis, comparing rental income to operating expenses, to gauge the property's financial health and negotiate a fair purchase price. By carefully evaluating the impact of maintenance, taxes, and utilities, buyers can make informed decisions that maximize both current income and long-term property value.

Rent-A-Center: Carrboro to Siler City Delivery?

You may want to see also

Explore related products

![]()

Vacancy and Risk Adjustment: Factor in potential vacancies and market risks to determine fair purchase price

When determining the fair purchase price of a rental building, it's essential to consider vacancy and risk adjustments. These factors directly impact the property's income potential and, consequently, its value. Vacancy rates in the local market should be analyzed to estimate the likelihood of unoccupied units. A higher vacancy rate implies greater risk and reduced income, which should be reflected in a lower purchase price. To adjust for vacancy, investors often use a vacancy factor, typically expressed as a percentage of potential gross income. For instance, if the market vacancy rate is 5%, the investor might deduct 5% from the total potential rent to arrive at a more realistic net operating income (NOI). This adjusted NOI becomes the basis for calculating the property's value using methods like capitalization rates or cash-on-cash returns.

Market risks, such as economic downturns, changing tenant demographics, or increased competition from new developments, must also be factored into the purchase price. These risks can affect both occupancy rates and rental income stability. To account for market risks, investors may apply a risk-adjusted capitalization rate, which is higher than the standard cap rate to compensate for the added uncertainty. For example, if a comparable property in a stable market has a cap rate of 6%, an investor might use a 7% or 8% cap rate for a property in a riskier market. This adjustment ensures that the purchase price aligns with the potential return relative to the perceived risk.

Another critical aspect of vacancy and risk adjustment is the consideration of historical and projected vacancy trends. Investors should examine the property's historical vacancy rates and compare them to market averages. If a property has consistently higher vacancies than the market, it may indicate underlying issues, such as poor management or less desirable location. In such cases, the purchase price should be further discounted to account for these risks. Additionally, analyzing local economic indicators, employment trends, and population growth can help forecast future vacancy risks and inform a more accurate pricing decision.

Implementing a vacancy reserve is another strategy to mitigate risk when determining the purchase price. This involves setting aside a portion of the rental income to cover potential losses during vacancy periods. For example, an investor might allocate 3-5% of the annual rental income into a reserve fund. By incorporating this reserve into the financial model, the investor can ensure that the property remains financially viable even during periods of lower occupancy. This approach provides a buffer against unexpected vacancies and enhances the overall stability of the investment.

Lastly, stress testing the investment under various vacancy and risk scenarios is crucial for a robust purchase price determination. This involves modeling the property's performance under different vacancy rates, rental income fluctuations, and market conditions. For instance, an investor might assess how the property would fare with a 10% vacancy rate or a 5% decline in rental prices. By evaluating the property's resilience under adverse conditions, investors can identify a price point that offers a reasonable return even in less favorable circumstances. This proactive approach ensures that the purchase price is not only based on current market conditions but also accounts for potential future challenges.

Rent Your Chicago Photo Studio: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The current rental income directly impacts the purchase price through capitalization rates or the income approach. Investors often use the formula: Purchase Price = Net Operating Income (NOI) / Capitalization Rate. Higher rental income typically increases the NOI, leading to a higher purchase price, assuming the cap rate remains constant.

Yes, the potential for future rent increases can significantly impact the purchase price. Buyers often assess the property’s upside potential by evaluating market rent trends, lease expiration dates, and local demand. A building with below-market rents and room for growth may command a higher purchase price due to its income-increasing potential.

Rent control laws can lower the purchase price by limiting rental income growth and increasing operational risks. Buyers factor in reduced cash flow potential and the complexity of managing rent-controlled units. However, in some cases, properties in rent-controlled areas may still attract buyers if the cap rates are adjusted to account for these restrictions.