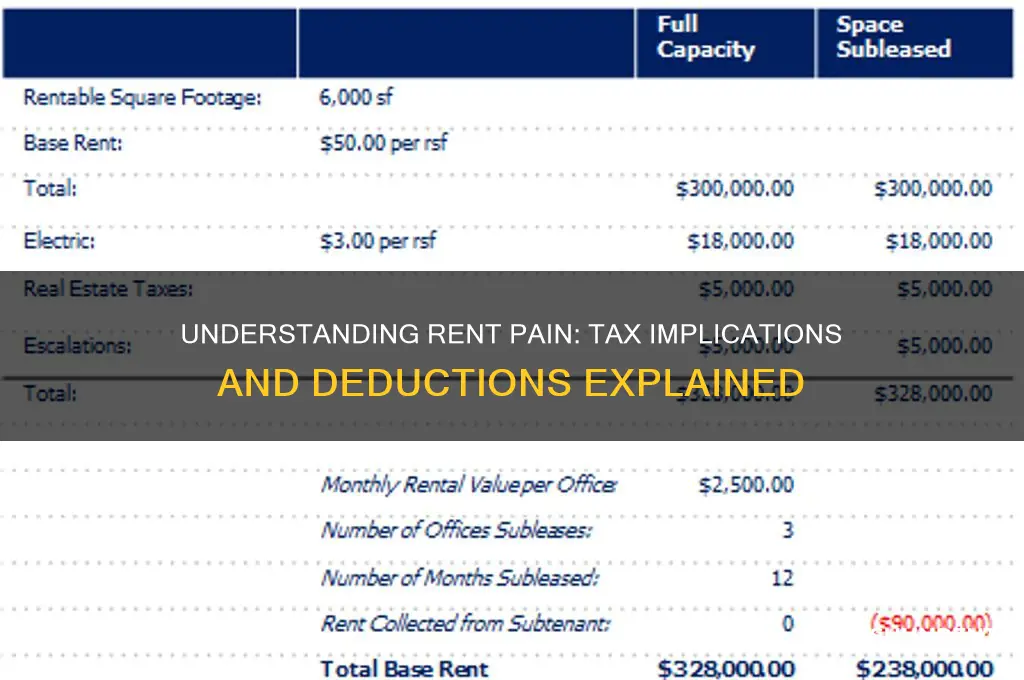

Understanding how rent payments affect your taxes is crucial for both tenants and landlords. For tenants, rent itself is typically not tax-deductible unless it falls under specific circumstances, such as home office expenses for self-employed individuals. However, certain related expenses, like moving costs for work or rent paid for a property used for business purposes, may qualify for deductions. For landlords, rental income is generally taxable, but they can offset this income by deducting eligible expenses, such as property maintenance, mortgage interest, and depreciation. Navigating these tax implications requires careful record-keeping and an understanding of IRS guidelines to ensure compliance and maximize potential savings.

Explore related products

What You'll Learn

- Rent Payments Deductions: Can renters claim deductions for rent payments on their tax returns

- Property Tax Pass-Through: How landlords passing property taxes to tenants impacts renter taxes

- Home Office Deduction: Renters working from home may qualify for home office tax deductions

- Moving Expenses: Tax benefits for renters relocating for work-related reasons

- Rent Assistance Taxation: Are government rent subsidies or assistance programs taxable income

![]()

Rent Payments Deductions: Can renters claim deductions for rent payments on their tax returns?

Rent payments are typically one of the largest monthly expenses for tenants, yet the tax code offers limited relief for renters. Unlike homeowners who can deduct mortgage interest and property taxes, renters generally cannot claim their monthly rent payments as a deduction on their federal tax returns. This disparity stems from the tax system’s focus on incentivizing homeownership over renting. However, there are specific circumstances and strategies renters can explore to potentially reduce their tax burden indirectly related to their housing costs.

One notable exception to the no-deduction rule is for renters who use part of their home exclusively for business purposes. If you’re self-employed and have a dedicated home office, you may qualify for the home office deduction. This allows you to deduct a portion of your rent proportional to the space used for business. For example, if your home office occupies 10% of your apartment’s total square footage, you can deduct 10% of your annual rent as a business expense. Keep detailed records of your space usage and expenses to support this claim during an audit.

Renters in certain states may also benefit from state-level tax deductions or credits. Some states, like California and Maryland, offer renter’s tax credits for low- to moderate-income individuals and families. These credits are typically based on factors like income, rent paid, and household size. For instance, California’s Renter’s Credit provides up to $1,050 for married couples filing jointly with qualifying rent expenses. Check your state’s tax guidelines to determine eligibility and application requirements.

Another indirect way renters can save on taxes is by maximizing other deductions and credits to offset their overall tax liability. For example, contributing to a retirement account like a traditional IRA or 401(k) can lower your taxable income, effectively reducing the impact of your rent burden. Similarly, claiming education credits, child care expenses, or medical deductions can free up funds that might otherwise go toward rent. While these strategies don’t directly deduct rent payments, they can improve your financial flexibility.

In conclusion, while renters cannot directly deduct their rent payments on federal tax returns, there are avenues to explore for potential savings. From leveraging the home office deduction to taking advantage of state-specific credits and optimizing other tax benefits, renters can strategically reduce their tax burden. Always consult a tax professional to ensure compliance with current laws and to identify opportunities tailored to your situation.

Renting Homemade Cartoon Character Props: Legal Considerations Explained

You may want to see also

Explore related products

![]()

Property Tax Pass-Through: How landlords passing property taxes to tenants impacts renter taxes

Landlords often pass property taxes onto tenants through rent increases, a practice known as property tax pass-through. This shift can directly impact renters’ financial burden, but it also raises questions about how this affects their taxes. Unlike homeowners who may deduct property taxes, renters generally cannot claim these expenses on their federal tax returns. However, understanding how property tax pass-through works is crucial for renters to assess their overall financial health and plan accordingly.

Consider a scenario where a landlord’s property tax bill increases by $1,200 annually. To offset this cost, the landlord raises monthly rent by $100 for a one-year lease. While this increase is a direct result of property taxes, the IRS does not allow renters to deduct this portion of their rent as a property tax expense. This means renters absorb the cost without tax relief, effectively paying more in rent without the ability to offset it on their tax returns. For renters in high-tax areas, this can significantly reduce disposable income over time.

From a comparative perspective, homeowners benefit from property tax deductions if they itemize their deductions on Schedule A of Form 1040. Renters, however, are left with fewer options. Some states offer renter’s tax credits or deductions, but these are often limited and vary widely. For example, California’s Renter’s Credit provides up to $120 for married couples filing jointly, but this pales in comparison to potential property tax deductions for homeowners. Renters should research state-specific programs to determine if they qualify for any relief.

To mitigate the impact of property tax pass-through, renters can adopt practical strategies. First, negotiate lease terms with landlords, especially if the property tax increase is substantial. Some landlords may agree to a smaller rent increase or spread it over multiple years. Second, track rent payments and property tax-related increases separately for personal financial planning. While this won’t directly impact taxes, it helps renters understand their expenses and budget effectively. Finally, advocate for policy changes at the state or local level to expand renter tax credits or deductions, addressing the inequity between renters and homeowners.

In conclusion, property tax pass-through increases renters’ financial burden without offering federal tax relief. While renters cannot deduct these costs, understanding this mechanism empowers them to make informed decisions. By exploring state-specific programs, negotiating with landlords, and advocating for policy changes, renters can better navigate the financial implications of this practice. Awareness and proactive planning are key to managing the indirect tax consequences of rent increases tied to property taxes.

Understanding Rent Guarantees in Tijuana: A Comprehensive Guide for Tenants

You may want to see also

Explore related products

![]()

Home Office Deduction: Renters working from home may qualify for home office tax deductions

Renters who work from home often overlook a valuable tax benefit: the home office deduction. This deduction allows you to claim a portion of your rent and related expenses as business costs, reducing your taxable income. To qualify, your home office must be used regularly and exclusively for business purposes—no multitasking as a guest room or gym. If you meet these criteria, you can deduct a percentage of your rent, utilities, and other home-related expenses based on the square footage of your office compared to your total living space.

For example, if your home office occupies 10% of your apartment’s total square footage, you can deduct 10% of your rent, electricity, and internet bills. Let’s say your monthly rent is $1,500, and your utilities average $200. Your annual deduction for these expenses would be $2,040 (10% of $20,400). Additionally, you can deduct expenses like homeowners’ insurance, repairs, and depreciation, though renters typically focus on rent and utilities. Keep detailed records of your expenses and measurements of your workspace to support your claim.

However, there’s a catch: the simplified method. Instead of calculating actual expenses, you can deduct $5 per square foot of your home office, up to 300 square feet ($1,500 maximum). This method is easier but may yield a smaller deduction if your actual expenses are higher. Compare both approaches to determine which benefits you more. For instance, if your office is 200 square feet, the simplified method gives you a $1,000 deduction, while the regular method might offer more if your rent and utilities are high.

One common misconception is that claiming this deduction increases your risk of an audit. While it’s true that home office deductions can attract IRS scrutiny, accurately documenting your eligibility and expenses minimizes this risk. Use tools like tax software or consult a professional to ensure compliance. Another tip: if you’re self-employed, this deduction reduces both your income tax and self-employment tax, providing double the savings.

In conclusion, renters working from home should not ignore the home office deduction. By understanding the eligibility rules, choosing the right calculation method, and maintaining thorough records, you can significantly reduce your tax burden. Whether you’re a freelancer, remote employee, or small business owner, this deduction turns your rent pain into tax relief—a win-win for your wallet.

Rents During the Great Depression: Did Prices Plummet Nationwide?

You may want to see also

Explore related products

![]()

Moving Expenses: Tax benefits for renters relocating for work-related reasons

Relocating for work can be a financial strain, but renters may find some relief through tax benefits designed to offset moving expenses. The IRS allows taxpayers to deduct certain costs associated with work-related moves, provided they meet specific criteria. To qualify, the new job location must be at least 50 miles farther from your old home than your previous workplace. Additionally, you must work full-time for at least 39 weeks during the first 12 months after the move, either as an employee or self-employed. These rules ensure the deduction is reserved for those genuinely relocating for career advancement.

The deductible expenses include transportation and storage of household goods, travel costs (including lodging) for you and your family, and costs associated with connecting or disconnecting utilities. Notably, meals are not deductible. For renters, this means expenses like hiring a moving company, renting a truck, or storing furniture temporarily can be claimed. Keep detailed records, including receipts and mileage logs, as documentation is crucial for substantiating these deductions. While the Tax Cuts and Jobs Act suspended moving expense deductions for most taxpayers through 2025, members of the military relocating due to military orders can still claim these benefits.

For renters, understanding the nuances of these deductions can significantly reduce the financial burden of a work-related move. For instance, if you rent a moving truck for $300, pay $200 for storage, and spend $150 on travel, these $650 in expenses could directly lower your taxable income. However, it’s essential to differentiate between deductible and non-deductible costs. Rent payments themselves, whether at the old or new location, are not eligible for this deduction. Focus instead on the direct costs of the move itself.

To maximize these benefits, plan your move strategically. If possible, time your relocation to align with the start of a new job to ensure you meet the 39-week employment requirement. Use IRS Form 3903 to calculate and claim your moving expense deduction when filing your taxes. For military personnel, consult the IRS guidelines specific to your situation, as the rules may differ. While the process requires attention to detail, the potential tax savings make it a worthwhile endeavor for eligible renters.

Understanding Rent Classification in QuickBooks: Expense or Fixed Asset?

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![]()

Rent Assistance Taxation: Are government rent subsidies or assistance programs taxable income?

Government rent assistance programs are a lifeline for many, but their tax implications often remain shrouded in confusion. The central question: Is rent assistance considered taxable income? The answer, like many tax-related queries, is nuanced. Generally, government rent subsidies are not taxable income in the United States. Programs like Section 8 Housing Choice Vouchers, public housing assistance, and Low-Income Housing Tax Credit (LIHTC) properties are designed to alleviate housing burdens without adding to recipients' tax liabilities. The IRS classifies these benefits as non-taxable because they are intended to directly offset housing costs, not augment personal income.

However, exceptions exist. For instance, if a landlord reduces rent in exchange for services (e.g., maintenance work), the value of the rent reduction may be considered taxable income. Similarly, certain state-specific programs or lump-sum payments might have different tax treatments, so it’s crucial to verify the rules for your particular program. For example, the Emergency Rental Assistance (ERA) program, established during the COVID-19 pandemic, explicitly states that funds received are not taxable, but recipients should retain documentation to prove eligibility if questioned by the IRS.

To navigate this landscape, keep detailed records of all rent assistance received, including program names, amounts, and dates. If you’re unsure about the taxability of a specific benefit, consult IRS Publication 526 or seek advice from a tax professional. Proactive documentation can prevent headaches during tax season and ensure compliance with federal and state regulations.

A comparative analysis reveals that while rent assistance is typically non-taxable, other forms of government aid, like unemployment benefits, are taxable. This distinction underscores the importance of understanding the purpose and structure of each program. Rent assistance is designed to reduce housing expenses, whereas unemployment benefits replace lost wages, thus treated as income. Recognizing these differences can help recipients avoid unexpected tax bills and maximize their financial stability.

In conclusion, government rent subsidies are generally not taxable income, but vigilance is key. Stay informed about the specifics of your assistance program, maintain thorough records, and seek professional guidance when in doubt. By doing so, you can focus on the relief these programs provide without the added stress of tax complications.

Understanding Rent Assistance: Which Government Program Offers Housing Support?

You may want to see also

Frequently asked questions

Rent pain refers to the financial strain caused by high rental costs relative to income. While rent itself is not directly tax-deductible for most taxpayers, it may indirectly affect your taxes if you itemize deductions and claim certain credits, such as the Earned Income Tax Credit (EITC), which considers your overall financial situation.

A: Generally, no. Rent payments for personal residences are not tax-deductible for most taxpayers. However, if you use part of your rental property for business purposes, you may be able to deduct a portion of the rent as a business expense.

A: High rent can reduce your disposable income, which may increase your eligibility for certain tax credits like the EITC or housing-related deductions if you qualify. Additionally, if you live in a rent-controlled area or receive rental assistance, those factors could influence your taxable income or eligibility for specific programs.

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)