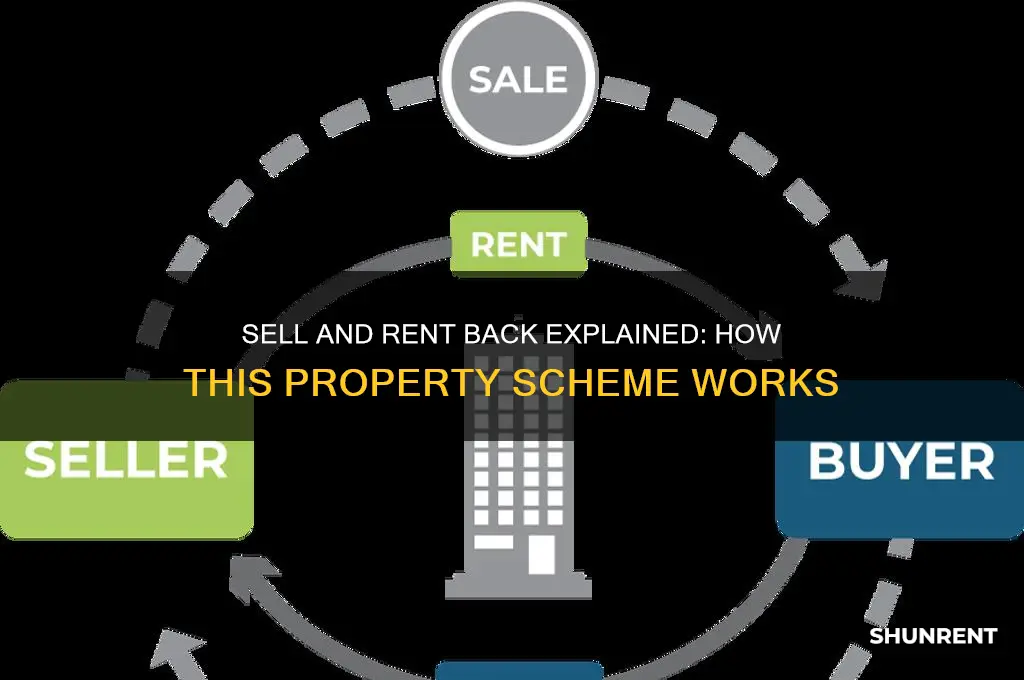

Sell and rent back schemes allow homeowners to sell their property to a company or investor while continuing to live in it as tenants, paying rent instead of a mortgage. This arrangement can provide immediate financial relief by unlocking equity tied up in the home, which can be particularly appealing for those facing financial difficulties or needing quick access to cash. However, it’s crucial to carefully consider the terms, as rent amounts may be higher than typical market rates, and there could be long-term implications for homeownership. Additionally, regulatory protections vary, so seeking independent legal and financial advice is essential to ensure the arrangement aligns with one’s needs and circumstances.

Explore related products

What You'll Learn

![]()

Understanding Sell and Rent Back

Sell and rent back schemes offer homeowners a way to unlock equity from their property without the need to move. In this arrangement, you sell your home to a company or investor, who then rents it back to you, allowing you to remain in the property as a tenant. This can be particularly appealing if you’re facing financial difficulties, need quick access to cash, or want to avoid the stress of relocating. However, it’s crucial to understand the mechanics and implications of such agreements before proceeding.

Consider the process step-by-step. First, a valuation of your property is conducted, often below market value, as the buyer assumes risks like property maintenance and rental management. Next, you receive a lump sum for the sale, typically less than what you’d get on the open market. Finally, you sign a rental agreement, usually with the option to repurchase the property later, though terms vary widely. For instance, some schemes offer fixed-term rentals (e.g., 5–10 years), while others provide indefinite tenancy. Always scrutinize the contract for clauses related to rent increases, repurchase conditions, and eviction policies.

One of the most persuasive arguments for sell and rent back is its speed and convenience. Traditional house sales can take months, involving estate agents, viewings, and protracted negotiations. In contrast, sell and rent back transactions often complete within weeks, providing immediate financial relief. This makes it an attractive option for those facing repossession, divorce, or urgent debt repayment. However, the trade-off is a significant reduction in the equity you receive, which can range from 20% to 50% below market value, depending on the provider and your circumstances.

A comparative analysis reveals both advantages and pitfalls. On the positive side, you gain access to cash without the upheaval of moving, and some schemes allow you to repurchase the property at a later date, potentially at a discounted rate. However, the risks are substantial. Rent payments may increase over time, eroding your financial stability, and there’s no guarantee you’ll be able to buy back the property. Additionally, unscrupulous providers have been known to exploit vulnerable homeowners, leading to regulatory crackdowns in some regions. For example, in the UK, sell and rent back schemes are regulated by the Financial Conduct Authority (FCA), requiring providers to be authorized and adhere to strict guidelines.

To navigate this arrangement safely, follow these practical tips. First, seek independent legal and financial advice to ensure you fully understand the terms and potential long-term consequences. Second, verify the credibility of the buyer by checking their FCA authorization (if applicable) and reading reviews from previous clients. Third, explore alternative options, such as equity release schemes, remortgaging, or government-assisted programs, which may offer better terms. Finally, ensure the rental agreement is fair, with capped rent increases and clear repurchase conditions. By approaching sell and rent back with caution and due diligence, you can make an informed decision that aligns with your financial goals.

Top UTV Rental Spots in Moab, Utah for Adventure Seekers

You may want to see also

Explore related products

![]()

Benefits of Sell and Rent Back

Sell and rent back schemes offer homeowners a unique financial strategy, allowing them to unlock equity in their property without the upheaval of moving. This arrangement provides immediate access to cash, which can be a lifeline for those facing financial pressures or seeking to invest in other opportunities. For instance, a homeowner with a property valued at £300,000 could sell it to a company, receive a lump sum (often 70-85% of the market value), and continue living in the home as a tenant. This approach eliminates the stress of selling on the open market, including viewings, negotiations, and potential chains collapsing.

One of the standout benefits of sell and rent back is its ability to provide financial flexibility. For retirees or individuals with limited income, releasing equity can supplement pensions or cover unexpected expenses. Consider a 65-year-old homeowner with a mortgage-free property worth £400,000. By selling and renting back, they could access £280,000 to £340,000, ensuring a comfortable retirement without the burden of property maintenance. This option is particularly appealing for those who wish to downsize but are emotionally attached to their current home.

Another advantage lies in the simplicity and speed of the process. Traditional property sales can take months, involving estate agents, solicitors, and potential buyers. In contrast, sell and rent back transactions often complete within weeks. This rapid turnaround is ideal for homeowners facing urgent financial needs, such as debt consolidation or medical expenses. For example, a family with £50,000 in high-interest debt could sell their £250,000 home, clear their debts, and rent back at a market rate, improving their financial stability.

However, it’s crucial to approach this strategy with caution. While the benefits are significant, renters must ensure the rental agreement is fair and sustainable. Rent levels should align with local market rates, and tenants should clarify responsibilities for maintenance and repairs. Additionally, homeowners should verify the credibility of the buying company to avoid scams. For instance, checking if the company is a member of a reputable trade body, such as the Property Redress Scheme, can provide peace of mind.

In conclusion, sell and rent back schemes offer a practical solution for homeowners seeking liquidity without relocation. By providing quick access to equity, financial flexibility, and a streamlined process, this arrangement caters to diverse needs, from retirement planning to debt management. Yet, careful consideration of terms and due diligence on the buyer’s reputation are essential to maximize benefits and minimize risks.

Understanding Late Rent Payment Rules in Los Angeles: What You Need to Know

You may want to see also

Explore related products

![]()

Risks and Considerations

Sell and rent back schemes promise homeowners a quick financial solution, but they come with significant risks that demand careful scrutiny. One of the primary dangers is the potential for equity erosion. In these arrangements, homeowners often sell their property at a discounted price, sometimes as much as 25-50% below market value, to secure immediate cash. While this provides short-term relief, it permanently reduces the homeowner’s equity, leaving them with less financial cushion for the future. For example, a £300,000 home sold in such a scheme might fetch only £200,000, effectively stripping the homeowner of £100,000 in equity.

Another critical risk lies in the terms of the rental agreement, which can trap homeowners in unfavorable conditions. Rent prices are often set at or above market rates, and tenants (the former homeowners) may face strict terms regarding maintenance, repairs, and lease duration. Failure to meet these obligations can lead to eviction, leaving individuals without a home or financial recourse. For instance, a homeowner who falls behind on rent might face legal action, despite having lived in the property for decades. This lack of security contrasts sharply with traditional homeownership, where equity builds over time and eviction is far less likely.

Regulatory gaps further exacerbate the risks associated with sell and rent back schemes. While the UK introduced stricter regulations in 2010, requiring providers to be authorized by the Financial Conduct Authority (FCA), loopholes remain. Unscrupulous operators may exploit these gaps, offering deals that appear legitimate but lack proper oversight. Homeowners must verify a provider’s FCA authorization and seek independent legal advice before proceeding. Without due diligence, they risk falling victim to fraudulent schemes that prioritize the provider’s profit over the homeowner’s welfare.

Finally, the emotional and psychological toll of relinquishing homeownership cannot be overlooked. For many, a home represents more than just an asset—it’s a source of stability, identity, and family heritage. Entering a sell and rent back agreement means surrendering control over the property, which can lead to feelings of loss and insecurity. This emotional cost, though intangible, is a significant consideration, especially for long-term homeowners or those with deep roots in their communities. Balancing financial need against emotional attachment requires careful introspection and, ideally, consultation with trusted advisors.

In summary, while sell and rent back schemes offer a quick financial fix, they carry substantial risks that extend beyond mere equity loss. From unfavorable rental terms and regulatory vulnerabilities to emotional strain, homeowners must weigh these factors critically. Practical steps, such as verifying FCA authorization, seeking independent legal advice, and exploring alternative financial solutions, can mitigate some risks. However, the decision should never be taken lightly, as the consequences can be long-lasting and irreversible.

Torrey Gardens Rent: Monthly Costs After the First Year Explained

You may want to see also

Explore related products

![]()

Legal and Financial Aspects

Sell and rent back schemes, while offering a quick financial solution, are fraught with legal and financial complexities that demand careful scrutiny. Legally, these arrangements often blur the line between a sale and a tenancy agreement, raising questions about the homeowner’s rights and protections. In the UK, for instance, the Financial Conduct Authority (FCA) regulates such schemes to prevent exploitation, requiring providers to be authorised and adhere to strict guidelines. This regulatory oversight is critical, as it ensures transparency and fairness, particularly in cases where homeowners may be vulnerable due to financial distress. Without such safeguards, the risk of unfair terms, hidden fees, or even eviction looms large, underscoring the importance of understanding the legal framework before entering into such agreements.

Financially, the structure of sell and rent back schemes can be deceptive, often presenting as a lifeline but potentially leading to long-term financial strain. Homeowners typically receive a lump sum, usually below market value, in exchange for transferring ownership of their property. They then become tenants, paying rent to the new owner. While this provides immediate cash relief, the rent payments may be set at market rates or higher, eroding the financial benefit over time. Additionally, the homeowner loses the opportunity to benefit from future property appreciation, a significant drawback in rising markets. A comparative analysis reveals that traditional options like equity release or secured loans may offer better financial outcomes, depending on individual circumstances, highlighting the need for a thorough financial assessment before committing to a sell and rent back arrangement.

One critical financial aspect often overlooked is the tax implications of such schemes. In some jurisdictions, the sale of a primary residence may be exempt from capital gains tax, but this exemption could be jeopardised if the homeowner continues to occupy the property as a tenant. For example, in the UK, the Principal Private Residence Relief may not apply if the homeowner retains a financial interest in the property or if the sale is deemed artificial. This could result in unexpected tax liabilities, further diminishing the financial viability of the arrangement. Homeowners must seek professional tax advice to navigate these complexities and avoid costly surprises.

Legally, the tenancy agreement in a sell and rent back scheme warrants close examination. Unlike standard rental contracts, these agreements often include clauses that favour the new owner, such as shorter notice periods or restrictions on subletting. In extreme cases, providers may insert clauses allowing them to terminate the tenancy prematurely, leaving the former homeowner without a home. To mitigate these risks, homeowners should insist on a fair and transparent tenancy agreement, ideally reviewed by a solicitor. Practical steps include ensuring the agreement complies with local tenancy laws, verifying the provider’s credentials, and understanding the dispute resolution mechanisms in place.

In conclusion, while sell and rent back schemes may appear as a quick fix for financial difficulties, their legal and financial aspects require meticulous attention. From regulatory compliance and tax implications to the terms of the tenancy agreement, each element carries significant weight. Homeowners must approach these arrangements with caution, seeking professional advice to ensure they are fully informed and protected. By doing so, they can make a decision that aligns with their long-term financial and housing needs, rather than falling prey to a scheme that may exacerbate their challenges.

Average Rent in Santa Barbara: What to Expect in 2023

You may want to see also

Explore related products

![Gentle Yoga for Back Pain and Prevention: 2, 30-minute relaxing, simple practices designed in conjunction with a back pain specialist [DVD]](https://m.media-amazon.com/images/I/71qoksxOxTL._AC_UY218_.jpg)

![]()

Finding Reputable Providers

Reputable sell and rent back providers are distinguished by their transparency, regulatory compliance, and customer-centric practices. Unlike unscrupulous operators who exploit homeowners’ financial distress, ethical providers disclose all terms upfront, including rental rates, contract lengths, and exit conditions. For instance, a trustworthy provider will clearly state whether the rental agreement is assured shorthold tenancy (AST) or a license to occupy, each with distinct legal implications. Always verify if the company is registered with the Property Redress Scheme (PRS) or The Property Ombudsman (TPO), as these memberships mandate adherence to industry standards and provide recourse in disputes.

To identify a reputable provider, scrutinize their track record and client testimonials. Legitimate companies often have case studies or reviews detailing how they’ve helped homeowners avoid repossession or bridge financial gaps. Cross-reference these testimonials with independent platforms like Trustpilot or Google Reviews, as curated website feedback may omit negative experiences. Additionally, check if the provider is a member of industry bodies such as the National Association of Property Buyers (NAPB), which enforces a code of conduct emphasizing fairness and honesty. Providers affiliated with such organizations are more likely to prioritize long-term relationships over quick profits.

A critical step in vetting providers is understanding their funding sources. Reputable companies typically operate with their own capital or established investor networks, reducing reliance on third-party lenders that may impose predatory terms. Ask for proof of funds or references from previous transactions to confirm financial stability. Beware of providers offering overly generous purchase prices or guaranteed lifetime tenancies, as these may mask hidden fees or unsustainable business models. A reliable provider will conduct a fair market valuation and explain how the offer aligns with current property values.

Finally, consult independent legal and financial advisors before committing to any agreement. A reputable provider will encourage this step, understanding that informed decisions protect both parties. Solicitors can review contracts for unfair clauses, such as excessive rent increases or restrictive exit terms, while financial advisors can assess whether the arrangement aligns with your long-term goals. For example, if you’re over 55, consider whether equity release schemes might offer a more suitable alternative. By combining due diligence with professional guidance, you can navigate the sell and rent back market with confidence and security.

How Lot Rent Covers Water and Sewer Expenses

You may want to see also

Frequently asked questions

Sell and rent back is a scheme where a homeowner sells their property to a company or individual, and then rents it back from them, allowing the homeowner to remain in the property as a tenant.

In a sell and rent back arrangement, the homeowner receives a lump sum or agreed-upon price for their property, which is typically below market value. They then pay rent to the new owner to continue living in the property, often at a market rate or slightly below.

Sell and rent back can provide temporary relief for homeowners facing financial difficulties, such as mortgage arrears or debt. However, it's essential to carefully consider the long-term implications, as the homeowner may lose equity in their property and face potential rent increases or eviction if they cannot keep up with rental payments.

Risks associated with sell and rent back include: selling the property below market value, facing rent increases or eviction, dealing with unregulated companies, and potentially losing the right to buy back the property. It's crucial to seek independent legal and financial advice before entering into such an arrangement.

Some sell and rent back agreements may include an option to buy back the property after a certain period, but this is not always the case. The terms and conditions of the buy-back option, if available, will vary depending on the agreement and should be carefully reviewed by a legal professional before signing any contract.

![Back to the Future: The Complete Trilogy [DVD]](https://m.media-amazon.com/images/I/819CLf3RK6L._AC_UY218_.jpg)