In the United States, renting has become an increasingly prevalent housing choice, with millions of households opting for rental properties over homeownership. As of recent data, approximately one-third of all U.S. households are renter-occupied, reflecting a significant shift in housing preferences driven by factors such as affordability, flexibility, and changing lifestyle priorities. This trend is particularly pronounced in urban areas, where high home prices and a desire for mobility make renting a more attractive option. Understanding the scale and dynamics of renting in the U.S. is crucial for policymakers, real estate professionals, and individuals navigating the housing market, as it highlights the growing importance of rental housing in the nation’s economic and social landscape.

Explore related products

What You'll Learn

- Rental Trends by State: Regional variations in rental rates across the United States

- Demographics of Renters: Age, income, and family size of households renting homes

- Affordable Housing Crisis: Challenges in finding affordable rental options nationwide

- Rent vs. Own Comparison: Percentage of households renting versus owning homes

- Impact of Urbanization: How city growth affects rental demand and availability

![]()

Rental Trends by State: Regional variations in rental rates across the United States

In the United States, approximately 36% of households rent their homes, a figure that masks significant regional disparities. These variations are driven by factors such as local economies, population density, and housing supply. For instance, in states like New York and California, where job opportunities are abundant but land is scarce, rental rates soar, with median rents exceeding $2,000 per month. Conversely, in states like Mississippi and Arkansas, where economic growth is slower and land is plentiful, median rents hover around $800, making housing more accessible to lower-income households.

Analyzing these trends reveals a clear divide between coastal and inland states. Coastal regions, particularly in the Northeast and West, face acute housing shortages due to high demand and strict zoning laws, driving up rental costs. For example, in San Francisco, the average rent for a one-bedroom apartment is over $3,500, while in Texas, a state with more relaxed zoning regulations and rapid housing development, the same unit averages $1,200. This comparison underscores the impact of policy and geography on rental affordability.

To navigate these regional variations, renters should consider their long-term financial goals and lifestyle needs. For young professionals seeking career growth, high-rent states may offer better opportunities despite the cost. However, families or retirees might prioritize affordability, opting for states with lower rental rates and a slower pace of life. Tools like rent-to-income ratios (ideally below 30%) can help determine if a region’s rental market aligns with one’s budget. For instance, in Nebraska, where the median rent is $900, a household earning $36,000 annually would meet this threshold comfortably.

A comparative analysis of states like Florida and Illinois highlights another trend: the role of tourism and seasonal demand. Florida’s rental market spikes during winter months due to snowbirds, while Illinois’s rates remain relatively stable year-round. This volatility can affect long-term renters, who may face unexpected increases or competition for leases. Prospective renters in such states should research seasonal patterns and consider signing longer-term leases to lock in rates.

Finally, understanding regional rental trends requires examining local policies and economic indicators. States with strong tenant protections, like Oregon, may have slower rent growth but stricter lease terms. Conversely, states with fewer regulations, like Georgia, might offer more flexibility but at the risk of rapid rent increases. By staying informed about these factors, renters can make strategic decisions, whether relocating for affordability or staying put and negotiating lease terms based on local market conditions.

Harassing Roommates for Rent: Legal Boundaries and Consequences Explained

You may want to see also

Explore related products

![]()

Demographics of Renters: Age, income, and family size of households renting homes

In the United States, approximately 36% of households rent their homes, a figure that has steadily risen over the past few decades. This shift reflects broader economic and social changes, but who exactly are these renters? Understanding the demographics—specifically age, income, and family size—provides critical insights into this growing segment of the population.

Age Distribution: The Youthful Majority

Renters are disproportionately younger compared to homeowners. Census data reveals that nearly 60% of renters are under the age of 45, with millennials (ages 25–40) and Gen Z (ages 18–24) forming the largest cohorts. This trend is driven by factors like delayed homeownership, student debt, and lifestyle preferences for flexibility. For instance, 70% of individuals under 30 rent, often choosing urban areas for proximity to jobs and amenities. However, renting isn’t exclusive to the young; 15% of renters are over 65, many opting for maintenance-free living or downsizing post-retirement.

Income Levels: A Spectrum of Affordability

Renters span a wide income range, but a significant portion falls into lower to middle-income brackets. Approximately 40% of renter households earn less than $35,000 annually, making them cost-burdened, spending over 30% of their income on rent. Conversely, high-income earners (over $100,000) are increasingly renting by choice, particularly in luxury apartments or single-family rentals. This duality highlights the need for diverse housing options, from affordable units to high-end rentals, to meet varying financial capacities.

Family Size: Beyond the Single Renter Stereotype

While single individuals and young couples dominate rental statistics, families with children constitute a notable 30% of renters. These households often face challenges like limited space and higher costs, as larger units are scarcer and pricier. Interestingly, the average family size in rental homes is 2.4 people, slightly lower than the national average of 2.6. This gap underscores the need for family-friendly rental designs, such as multi-bedroom units and access to schools and parks.

Practical Takeaways for Policymakers and Developers

To address the needs of this diverse demographic, targeted solutions are essential. For younger renters, incentivizing affordable housing near job hubs can reduce financial strain. For families, increasing the supply of larger units and implementing rent stabilization policies can provide stability. High-income renters, meanwhile, seek amenities like gyms, co-working spaces, and concierge services, presenting opportunities for premium developments. By tailoring housing strategies to these specific groups, stakeholders can ensure a more inclusive and sustainable rental market.

Understanding these demographics isn’t just about numbers—it’s about shaping policies and designs that reflect the realities of modern renters. From age-specific preferences to income-based challenges, each factor offers a lens into how we can better serve this vital segment of the population.

Renting a Hotel Residence: A Step-by-Step Guide to Long-Term Stays

You may want to see also

Explore related products

![]()

Affordable Housing Crisis: Challenges in finding affordable rental options nationwide

In the United States, over 43 million households rent their homes, accounting for approximately 35% of all households nationwide. This significant portion of the population faces mounting challenges in securing affordable rental options, as the gap between income and housing costs continues to widen. The affordable housing crisis is not confined to urban centers like New York or San Francisco; it permeates suburban and rural areas alike, where rising rents outpace wage growth. For instance, in cities like Phoenix and Nashville, rent increases have surged by over 20% in recent years, far exceeding the national average income growth of 3%. This disparity forces many renters to allocate more than the recommended 30% of their income to housing, leaving little for other essentials like healthcare, education, and savings.

One of the primary drivers of this crisis is the imbalance between supply and demand. The construction of new rental units has failed to keep pace with population growth and household formation, particularly in high-demand areas. Additionally, the conversion of affordable units into luxury housing or short-term rentals exacerbates the shortage. For example, in Miami, over 10,000 affordable units were lost to gentrification between 2010 and 2020, displacing low-income families and individuals. This trend is compounded by federal and state policies that often prioritize market-rate housing over subsidized options, leaving millions of renters with limited choices.

Another critical challenge is the lack of robust tenant protections, which leaves renters vulnerable to unfair practices such as sudden rent hikes, no-cause evictions, and substandard living conditions. While some states, like California and New York, have implemented rent control measures, many others lack such safeguards. This absence of protection disproportionately affects marginalized communities, including seniors, people of color, and individuals with disabilities, who are more likely to face housing instability. For instance, Black and Hispanic households are twice as likely as white households to experience eviction, according to a 2021 study by the Urban Institute.

Addressing the affordable housing crisis requires a multi-faceted approach. Policymakers must invest in the development of affordable units, expand housing voucher programs, and enforce stricter tenant protections. Local governments can incentivize developers to include affordable units in new projects through tax breaks or density bonuses. Renters themselves can advocate for their rights by joining tenant unions, participating in community meetings, and staying informed about local housing policies. Practical steps include researching rent control laws in their area, documenting lease agreements, and seeking legal aid when facing eviction threats. By combining systemic solutions with individual action, the nation can begin to bridge the affordability gap and ensure that renting remains a viable option for all.

Rent-a-Center PlayStation 5 Availability: What You Need to Know

You may want to see also

Explore related products

![]()

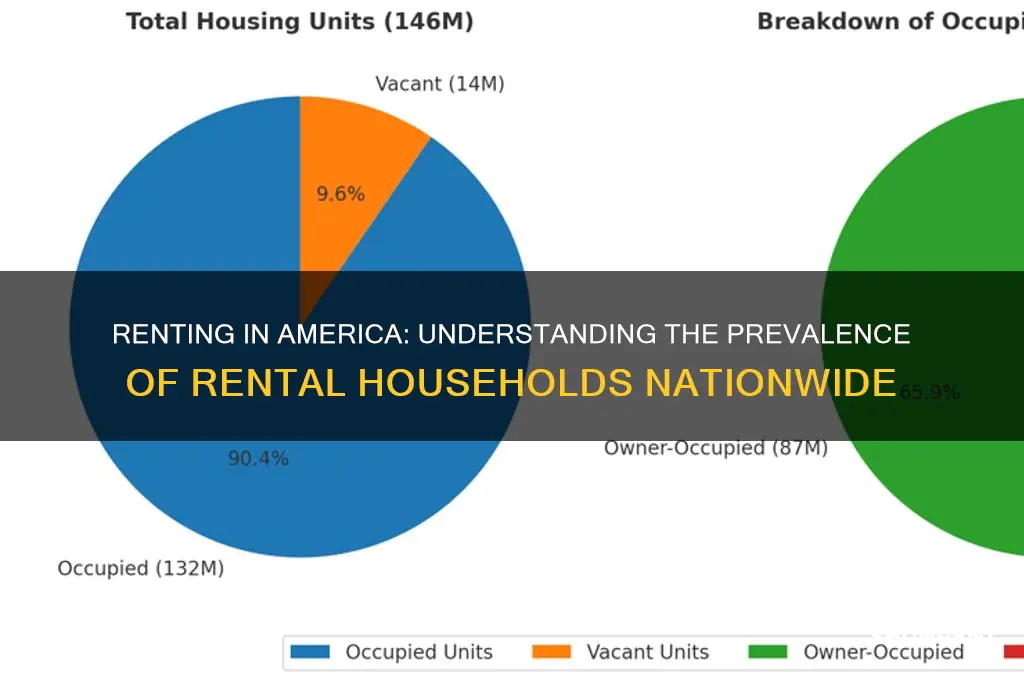

Rent vs. Own Comparison: Percentage of households renting versus owning homes

In the United States, the decision to rent or own a home is a pivotal financial and lifestyle choice, with significant implications for household stability, wealth accumulation, and community engagement. As of recent data, approximately 36% of U.S. households rent their homes, while 64% own. This divide reflects broader economic trends, including housing affordability, generational preferences, and regional disparities. For instance, urban centers like New York and Los Angeles report higher rental rates due to soaring home prices, while suburban and rural areas lean more toward homeownership. Understanding this split is crucial for policymakers, investors, and individuals navigating the housing market.

Analyzing the rent-versus-own dynamic reveals distinct advantages and trade-offs. Renting offers flexibility, lower upfront costs, and freedom from maintenance responsibilities, making it appealing to younger adults, millennials, and those in transitional life stages. Conversely, homeownership builds equity, provides tax benefits, and offers long-term financial security, though it requires a substantial down payment and ongoing maintenance. For example, a 20% down payment on a median-priced home in the U.S. ($400,000 as of 2023) would amount to $80,000—a barrier many renters struggle to overcome. This financial hurdle, coupled with rising interest rates, has kept rental rates steady despite increasing demand for housing.

From a generational perspective, the rent-versus-own gap highlights shifting priorities. Baby boomers, who own homes at a rate of 78%, contrast sharply with millennials, only 42% of whom own homes. This disparity is partly due to student loan debt, delayed marriage, and a preference for mobility among younger generations. However, as millennials age and start families, many are transitioning to homeownership, albeit at a slower pace than previous generations. This trend underscores the evolving nature of the housing market and the need for policies that address affordability and accessibility.

Regionally, the rent-versus-own divide is stark. In states like West Virginia and Mississippi, homeownership rates exceed 70%, driven by lower housing costs and a strong cultural preference for owning. Conversely, in California and New York, rental rates surpass 50%, reflecting high home prices and dense urban populations. These variations emphasize the importance of local context in housing decisions. For instance, a household earning $75,000 annually in Texas may comfortably afford a home, while the same income in California might necessitate renting due to higher costs.

Practical considerations for individuals weighing renting versus owning include long-term financial goals, job stability, and lifestyle preferences. Renters should evaluate whether their monthly payments align with their budget and if they have savings for emergencies. Prospective homeowners must assess their ability to manage a mortgage, property taxes, and maintenance costs. A rule of thumb is to ensure housing expenses do not exceed 30% of gross income. Additionally, tools like rent-versus-buy calculators can provide personalized insights based on location, income, and savings. Ultimately, the decision hinges on balancing immediate needs with future aspirations, ensuring a choice that fosters financial and personal well-being.

Renting Shows on Amazon Prime: A Step-by-Step Guide for Users

You may want to see also

Explore related products

![]()

Impact of Urbanization: How city growth affects rental demand and availability

Urbanization is reshaping the rental landscape in the United States, with cities like New York, Los Angeles, and Chicago experiencing population surges that outpace housing supply. As of 2023, approximately 36% of U.S. households rent their homes, a figure that climbs to nearly 70% in densely populated urban centers. This disparity highlights a critical imbalance: cities are magnets for job opportunities, cultural amenities, and innovation, yet their housing stock struggles to keep up with the influx of residents. The result? Skyrocketing rents and shrinking vacancy rates, leaving many households with limited options.

Consider the mechanics of this demand-supply mismatch. Urban growth often prioritizes commercial development over residential construction, as office spaces and retail hubs generate immediate economic returns. Meanwhile, zoning laws and land scarcity restrict the expansion of affordable housing. For instance, in San Francisco, where over 60% of residents rent, the average monthly rent exceeds $3,000—a figure that forces many to allocate more than 50% of their income to housing. This financial strain disproportionately affects low- and middle-income households, exacerbating income inequality and housing insecurity.

To address this crisis, cities are experimenting with innovative solutions. Some municipalities are incentivizing developers to include affordable units in new projects through tax breaks or density bonuses. Others are revisiting zoning regulations to allow for mixed-use developments and accessory dwelling units (ADUs), which can increase housing density without altering a neighborhood’s character. For renters, practical strategies include leveraging rental assistance programs, exploring co-living arrangements, or considering suburban areas with better affordability—though this often comes at the cost of longer commutes.

A comparative analysis reveals that cities with proactive housing policies fare better. For example, Minneapolis eliminated single-family zoning in 2019, paving the way for more diverse and affordable housing options. In contrast, cities like Seattle, which have struggled to balance growth with affordability, continue to see rental prices climb. The takeaway? Urbanization’s impact on rental demand and availability isn’t inevitable; it’s shaped by policy decisions, economic priorities, and community engagement.

Ultimately, the rental crisis in growing cities is a call to action for policymakers, developers, and renters alike. By understanding the interplay between urbanization and housing, stakeholders can advocate for solutions that ensure cities remain inclusive and livable. For individuals, staying informed about local housing policies and exploring alternative living arrangements can provide temporary relief. But systemic change requires collective effort—a reimagining of how cities grow and who they serve.

Rent Live on Fox: Anticipated Release Date and What to Expect

You may want to see also

Frequently asked questions

As of recent data, approximately 36% of households in the US rent their homes, while the remaining 64% own their homes.

There are roughly 44 million renter-occupied households in the US, based on the latest census and housing data.

States like New York, California, and Hawaii have some of the highest percentages of renting households, with over 40% of households renting in these areas.