Renting has become an increasingly prevalent housing choice in the United States, driven by factors such as rising home prices, shifting lifestyle preferences, and economic uncertainties. As of recent data, approximately 36% of U.S. households, or roughly 44 million homes, are occupied by renters, marking a significant portion of the population that relies on rental housing. This trend is particularly pronounced among younger generations, such as millennials and Gen Z, who often prioritize flexibility and affordability over homeownership. Additionally, urban areas and high-cost cities like New York, Los Angeles, and San Francisco have some of the highest rental rates in the country, reflecting the challenges of purchasing property in these markets. Understanding the scale and dynamics of renting in the U.S. is crucial for addressing housing affordability, policy development, and the broader economic landscape.

Explore related products

$179224 $383418

What You'll Learn

- Rental Trends by Age Group: Analyzes renting demographics across different age brackets in the U.S

- Urban vs. Rural Renting Rates: Compares rental prevalence in cities versus rural areas nationwide

- Rent Burden Statistics: Examines percentage of income spent on rent by U.S. households

- Rental Growth Over Decades: Tracks historical increases in renting population in the United States

- State-by-State Rental Data: Highlights states with highest and lowest renting populations

![]()

Rental Trends by Age Group: Analyzes renting demographics across different age brackets in the U.S

The U.S. rental market is a mosaic of age-driven preferences and behaviors, with distinct trends emerging across generational lines. Millennials (ages 25–40) currently dominate the rental landscape, accounting for over 35% of all renters. Burdened by student debt, delayed homeownership, and a preference for urban flexibility, this cohort often prioritizes affordability and proximity to city centers. For instance, 60% of millennial renters in cities like Austin and Denver report choosing renting over buying due to financial constraints and lifestyle choices.

In contrast, Gen Z (ages 18–24) is rapidly entering the rental market, driven by educational pursuits and early career mobility. This group tends to seek shared living arrangements or micro-apartments to manage costs, with 45% living with roommates. Their tech-savvy nature also influences their rental decisions, favoring platforms that offer virtual tours and seamless digital leasing processes. However, their long-term impact on the market remains uncertain as they age into higher earning brackets.

Baby Boomers (ages 57–75), traditionally associated with homeownership, are increasingly turning to renting in retirement. Approximately 20% of renters in this age group cite downsizing and maintenance-free living as primary motivations. Luxury rental communities catering to seniors, often featuring amenities like fitness centers and social activities, are seeing a surge in demand. This shift challenges the stereotype of renting as a transient phase, positioning it as a lifestyle choice across all life stages.

Gen X (ages 41–56) represents a transitional demographic, balancing family needs with financial stability. While 30% of this group still rents, many are sandwiched between supporting children and aging parents, limiting their ability to transition to homeownership. They often seek suburban rentals with more space and school district access, reflecting a pragmatic approach to housing.

Understanding these age-specific trends is critical for landlords, developers, and policymakers. Tailoring rental offerings to meet the unique needs of each demographic—whether through affordable urban units for millennials, tech-integrated spaces for Gen Z, senior-friendly amenities for Boomers, or family-oriented rentals for Gen X—can optimize occupancy rates and tenant satisfaction. As generational priorities evolve, so too must the rental market to remain relevant and responsive.

Renting Office Space in Clonmel: A Comprehensive Guide for Businesses

You may want to see also

Explore related products

![]()

Urban vs. Rural Renting Rates: Compares rental prevalence in cities versus rural areas nationwide

The rental landscape in the United States is starkly divided between urban and rural areas, with cities often experiencing higher rental rates due to increased demand and limited space. For instance, in metropolitan areas like New York City or San Francisco, over 60% of residents rent their homes, compared to roughly 30% in rural counties. This disparity is driven by factors such as job opportunities, population density, and housing availability, making urban centers magnets for renters despite higher costs.

To understand this divide, consider the economic incentives. Urban areas offer more job opportunities, cultural amenities, and public transportation, attracting young professionals and families who prioritize convenience. In contrast, rural areas often have lower rental rates but fewer employment options, leading to a smaller renter population. For example, while a one-bedroom apartment in Manhattan averages $3,500 monthly, a similar unit in rural Iowa might cost $600. This price gap reflects the trade-off between accessibility and affordability.

However, rural renting is not without its challenges. Limited inventory and aging housing stock can make finding quality rentals difficult. In some rural counties, only 10–15% of housing units are available for rent, compared to 40–50% in urban areas. This scarcity can force renters into suboptimal conditions or longer commutes. For those considering rural renting, it’s essential to research local markets, inspect properties thoroughly, and negotiate lease terms to secure the best value.

A persuasive argument for urban renting lies in its long-term financial benefits. Despite higher costs, urban renters often save on transportation and have access to higher-paying jobs, potentially offsetting rental expenses. For instance, a study found that urban renters in tech hubs like Seattle or Austin earn, on average, 30% more than their rural counterparts. Conversely, rural renting appeals to those seeking lower living costs and a slower pace of life, making it ideal for retirees or remote workers.

In conclusion, the choice between urban and rural renting hinges on lifestyle priorities and financial circumstances. Urban areas offer convenience and opportunity at a premium, while rural areas provide affordability and space with fewer amenities. By analyzing local rental markets, understanding economic factors, and aligning choices with personal goals, renters can navigate this divide effectively. Whether in a bustling city or a quiet countryside, the key is to balance cost, quality, and lifestyle to find the ideal rental situation.

Accepting Late Rent in Massachusetts: A Guide for Landlords and Tenants

You may want to see also

Explore related products

![]()

Rent Burden Statistics: Examines percentage of income spent on rent by U.S. households

In the United States, nearly 43 million households are currently renting their homes, representing about 35% of all occupied housing units. This significant portion of the population faces varying degrees of financial strain due to housing costs, a phenomenon quantified by rent burden statistics. These metrics reveal that a household is considered rent-burdened if it spends more than 30% of its income on rent and utilities, a threshold established by the U.S. Department of Housing and Urban Development (HUD). Alarmingly, nearly half of all renting households—approximately 21 million—exceed this limit, with 11 million spending over 50% of their income on housing, a condition known as severe rent burden.

Analyzing these figures, it becomes clear that rent burden disproportionately affects low-income households. For instance, among renters earning less than $30,000 annually, 73% are rent-burdened, compared to just 14% of those earning over $75,000. This disparity highlights the economic vulnerability of lower-income families, who often face difficult trade-offs between housing, food, healthcare, and other essentials. Geographically, rent burden is most acute in metropolitan areas with high housing costs, such as New York, Los Angeles, and San Francisco, where even middle-income households struggle to keep up with rising rents.

To mitigate rent burden, policymakers and advocates propose several strategies. Expanding affordable housing programs, such as Housing Choice Vouchers, can provide direct relief to low-income renters. Additionally, increasing the minimum wage and promoting rent control policies in high-cost areas could help balance housing expenses with income levels. For individuals, practical steps include seeking roommate arrangements, negotiating lease terms, and exploring government assistance programs like the Low-Income Home Energy Assistance Program (LIHEAP) to offset utility costs.

Comparatively, the U.S. rent burden situation contrasts with countries like Germany, where robust tenant protections and a larger supply of social housing keep rental costs more manageable. This suggests that structural changes, such as incentivizing the construction of affordable units and reforming zoning laws, could address the root causes of rent burden in the U.S. Without such interventions, the number of rent-burdened households is likely to grow, exacerbating economic inequality and housing instability.

In conclusion, rent burden statistics serve as a critical indicator of housing affordability and financial stress among U.S. renters. By understanding these metrics and their implications, stakeholders can develop targeted solutions to alleviate the strain on millions of households. Whether through policy reforms, community initiatives, or individual strategies, addressing rent burden is essential for ensuring stable, accessible housing for all.

Discover the Average Rent in Monterey, CA: A Comprehensive Guide

You may want to see also

Explore related products

![]()

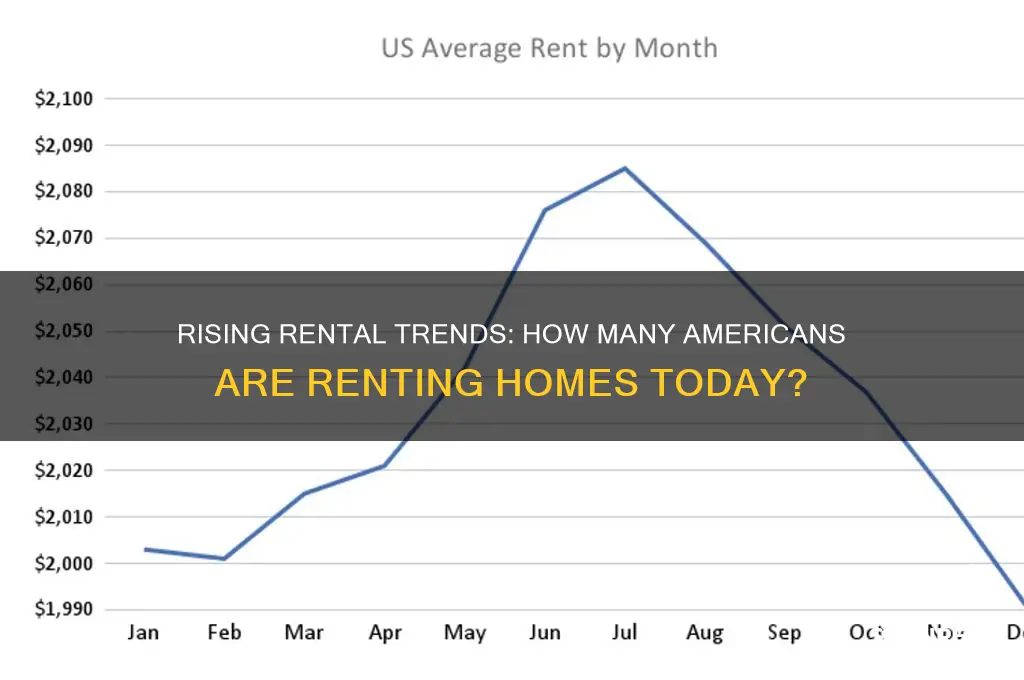

Rental Growth Over Decades: Tracks historical increases in renting population in the United States

The U.S. Census Bureau reports that the percentage of households renting their homes has risen from 31% in 1960 to nearly 36% in 2021. This steady climb reflects a seismic shift in American housing preferences, driven by factors like urbanization, economic instability, and changing lifestyle priorities. For instance, the post-World War II era saw a surge in homeownership due to government incentives, but the 2008 housing crisis reversed this trend, pushing many into the rental market. Understanding this historical trajectory is crucial for policymakers, investors, and renters alike, as it underscores the growing demand for affordable, quality rental housing.

Analyzing the data reveals distinct phases of rental growth. The 1980s and 1990s witnessed a plateau in renting rates, hovering around 34%, as the economy stabilized and homeownership regained appeal. However, the early 2000s marked a turning point, with renting populations increasing sharply, particularly among millennials. This demographic, aged 25–40, now constitutes the largest share of renters, often delaying homeownership due to student debt, high property prices, and a preference for flexibility. For example, in 2020, 45% of millennials were renters, compared to 30% of Gen Xers at the same age. This generational shift highlights the need for rental policies that address affordability and tenant protections.

A comparative analysis of urban and rural renting trends further illuminates this growth. Metropolitan areas like New York, Los Angeles, and San Francisco have seen renting rates exceed 50%, driven by high living costs and limited housing supply. In contrast, rural areas maintain lower renting rates, around 25%, due to lower property prices and a cultural preference for homeownership. However, even these regions are experiencing gradual increases, as younger populations migrate to cities for employment opportunities. This urban-rural divide underscores the importance of localized rental strategies, such as incentivizing multi-family housing development in high-demand areas.

Persuasively, the historical rise in renting populations demands a reevaluation of housing policies. While homeownership remains a cornerstone of the American Dream, the rental market’s expansion necessitates investments in infrastructure, tenant rights, and affordable housing initiatives. For instance, expanding the Low-Income Housing Tax Credit (LIHTC) program could encourage developers to build more affordable units. Additionally, renters should prioritize financial literacy, such as understanding lease agreements and saving for potential homeownership. By addressing these challenges, society can ensure that renting remains a viable, dignified housing option for millions.

Descriptively, the rental landscape has evolved from a temporary housing solution to a long-term lifestyle choice. Modern rentals often include amenities like gyms, co-working spaces, and pet-friendly policies, catering to diverse tenant needs. For example, luxury apartment complexes in cities like Austin and Nashville attract young professionals seeking convenience and community. Meanwhile, single-family rentals in suburban areas appeal to families desiring space without the commitment of ownership. This diversification reflects the rental market’s adaptability, making it a dynamic sector poised for continued growth. As the renting population expands, stakeholders must collaborate to balance profitability with accessibility, ensuring a sustainable housing future.

Unveiling the Tenant: Who Rented 12 8th Street West?

You may want to see also

Explore related products

![]()

State-by-State Rental Data: Highlights states with highest and lowest renting populations

The United States is a patchwork of rental markets, with significant variations in renting populations across states. At one end of the spectrum, states like New York and California boast some of the highest percentages of renters, driven by dense urban centers, high housing costs, and robust job markets. New York, for instance, has over 45% of its population renting, while California hovers around 44%. These states reflect the challenges of homeownership in areas with skyrocketing property values and limited housing supply. On the flip side, states like West Virginia and Mississippi have the lowest renting populations, with only about 25% of residents renting. These states often feature lower housing costs, more rural landscapes, and a cultural preference for homeownership.

Analyzing these disparities reveals deeper economic and demographic trends. High-renting states often correlate with younger, more mobile populations drawn to urban job opportunities. For example, in New York City, nearly two-thirds of residents rent, a statistic underscoring the city’s role as a magnet for young professionals and immigrants. Conversely, low-renting states like Mississippi tend to have older, more settled populations with stronger ties to homeownership. These states also face slower economic growth, reducing the demand for rental housing. Policymakers and investors can use this data to tailor housing strategies, such as increasing affordable rental units in high-demand areas or incentivizing homeownership in regions with surplus housing stock.

For individuals navigating the rental market, understanding these state-by-state differences is crucial. In high-renting states, renters should prioritize early lease renewals and consider roommates to offset rising costs. For instance, in California, where rent control laws vary by city, tenants in Los Angeles or San Francisco should familiarize themselves with local ordinances to protect against excessive rent hikes. In contrast, renters in low-renting states like West Virginia may find more flexibility in lease terms but fewer amenities or modern housing options. Here, negotiating rent or seeking long-term leases can provide stability in a market with fewer competitors.

A comparative analysis of these states also highlights the role of policy in shaping rental markets. States with high renting populations often have stricter tenant protections, such as New Jersey’s robust eviction safeguards, which can stabilize rental markets but may also deter landlords from investing. In contrast, states with low renting populations, like Alabama, often have fewer tenant protections, making renting riskier for tenants but more attractive for landlords. Advocates for housing equity can use this data to push for balanced policies that protect renters without stifling housing development.

Finally, investors and developers should take note of these trends when planning projects. High-renting states offer lucrative opportunities but require careful consideration of affordability and competition. For example, building mid-range rental units in New York’s outer boroughs could tap into demand from middle-income renters priced out of Manhattan. In low-renting states, focusing on single-family rental homes or mixed-use developments in growing towns could attract both locals and newcomers. By aligning strategies with state-specific rental data, stakeholders can maximize returns while addressing local housing needs.

Orlando's Rental Speed: How Quickly Can You Secure a Lease?

You may want to see also

Frequently asked questions

As of recent data, approximately 44 million households in the US are renting their homes, representing about 36% of all occupied housing units.

About 36% of the US population lives in rental housing, with the number of renters steadily increasing over the past few decades.

Young adults aged 25–34 have the highest percentage of renters, with over 50% of this age group choosing to rent rather than own homes.