Renting is a prevalent housing choice in the UK, with a significant portion of the population opting for rental properties over homeownership. Recent statistics reveal that approximately 4.4 million households in the UK are privately rented, accounting for around 19% of all households. This trend is particularly prominent among younger generations, as many millennials and Gen Z individuals face challenges in entering the property market due to rising house prices and stricter mortgage requirements. The rental market's growth can be attributed to various factors, including increased flexibility, urban migration, and the appeal of a more transient lifestyle. Understanding the scale of renting in the UK is essential to grasp the dynamics of the housing market and the evolving preferences of its residents.

| Characteristics | Values |

|---|---|

| Total number of renters in the UK | Approximately 11.3 million households (as of 2023) |

| Percentage of households renting | Around 36% of households in England (private and social renting) |

| Private renters | 4.6 million households (England, 2022/23) |

| Social renters | 4.1 million households (England, 2022/23) |

| Renters in London | Over 50% of households rent (highest in the UK) |

| Age group most likely to rent | 25-34 years old (48% of this age group rent) |

| Average monthly rent (UK) | £1,007 (as of 2023, excluding London) |

| Average monthly rent (London) | £2,000+ (as of 2023) |

| Renting growth trend | Increased by 1.5 million households since 2007 (England) |

| Renters with children | 1.3 million renting households with dependent children (England, 2022) |

| Rent burden (spending >30% on rent) | 30% of private renters face affordability issues (2022 data) |

Explore related products

$18.79 $20.99

What You'll Learn

- Renting Demographics: Age groups, income levels, and family sizes of UK renters

- Regional Variations: Renting rates in London vs. other UK cities and regions

- Renting Trends: Historical growth and future projections of UK rental market

- Affordability Crisis: Challenges faced by renters due to rising costs and low supply

- Policy Impact: Government housing policies and their effects on renting population

![]()

Renting Demographics: Age groups, income levels, and family sizes of UK renters

In the UK, approximately 4.4 million households rent their homes from private landlords, and an additional 4 million rent from housing associations or local authorities. This significant portion of the population—nearly 20% of all households—highlights the importance of understanding who these renters are. Demographics such as age, income, and family size paint a vivid picture of the renting landscape, revealing trends that shape housing policies, investment strategies, and societal norms.

Consider the age groups dominating the rental market: young adults aged 25–34 make up the largest share, with over 40% of this demographic renting. This is no surprise, as this age bracket often includes individuals starting careers, saving for deposits, or avoiding long-term commitments. However, renting is no longer just a "young person’s game." The number of renters aged 35–44 has surged by 25% over the past decade, driven by factors like delayed homeownership, divorce, or lifestyle flexibility. Even among those aged 65 and over, renting is on the rise, with a 39% increase since 2010, as older adults seek maintenance-free living or downsize post-retirement.

Income levels further stratify the renting population. While it’s a common misconception that renters are predominantly low-income, data shows a diverse economic profile. Middle-income households (earning £30,000–£50,000 annually) constitute the largest group, accounting for 35% of renters. This challenges the stereotype of renting as a last resort, as many in this bracket choose renting for financial flexibility or lifestyle preferences. Conversely, high-income earners (over £70,000) are increasingly renting in urban centers, valuing proximity to work and amenities over homeownership. Yet, low-income renters (under £20,000) face the most challenges, with 40% spending over a third of their income on rent, underscoring affordability crises in cities like London and Manchester.

Family size adds another layer of complexity to renting demographics. Single-person households represent 40% of all renters, reflecting the growing trend of solo living, particularly among young professionals and older adults. Families with children, however, make up 30% of renters, often facing limited options due to high costs and a shortage of family-sized properties. This segment is particularly vulnerable, with 25% of renting families living in overcrowded conditions, compared to 2% of homeowners. Meanwhile, couples without children account for 20% of renters, frequently prioritizing location and convenience over space.

Understanding these demographics is not just academic—it has practical implications. For policymakers, it highlights the need for diverse housing stock, from studio apartments to three-bedroom homes. For landlords, it underscores the importance of catering to varied tenant profiles, such as offering pet-friendly properties for young professionals or accessible homes for older renters. For individuals, it provides context for navigating the rental market, whether negotiating leases or planning long-term housing strategies. By dissecting these trends, we can move beyond broad generalizations and address the nuanced needs of UK renters.

How to Report Rent Payments on Your Tax Refund: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Regional Variations: Renting rates in London vs. other UK cities and regions

London's renting rates stand as a stark outlier in the UK housing landscape. Data from the English Housing Survey reveals that a staggering 49% of London households rent, compared to a national average of 36%. This disparity isn't merely a statistical quirk; it's a reflection of the capital's unique economic and demographic pressures. Sky-high property prices, fueled by global investment and limited space, push homeownership out of reach for many, leaving renting as the only viable option.

This phenomenon creates a ripple effect, influencing everything from commuting patterns to social mobility.

Beyond London, the renting picture diversifies significantly. Northern cities like Manchester and Liverpool exhibit renting rates closer to the national average, hovering around 35%. Here, a combination of more affordable housing stock and a historically stronger culture of homeownership tempers the rental market's dominance. However, even within these regions, pockets of high renting rates emerge, often correlated with student populations and urban regeneration zones.

For instance, areas surrounding universities in Leeds and Newcastle see renting rates climb above 40%, mirroring the student-driven rental hotspots found in London boroughs like Camden and Islington.

The rural-urban divide further complicates the regional renting narrative. In rural areas, renting rates traditionally lag behind urban centers, often dipping below 25%. This can be attributed to a higher prevalence of homeownership, driven by factors like intergenerational wealth transfer and a preference for settled, community-oriented lifestyles. However, this trend is not absolute. Tourist hotspots and areas with limited housing development can experience rental spikes, as seasonal demand and restricted supply drive up prices, pushing renting rates closer to urban levels.

The Cotswolds, for example, while predominantly owner-occupied, sees renting rates climb in picturesque villages catering to second-home owners and holidaymakers.

Understanding these regional variations is crucial for policymakers, investors, and individuals navigating the UK housing market. It highlights the need for tailored solutions that address the specific challenges faced by different areas. While London's rental crisis demands innovative approaches to increase housing supply and affordability, other regions may require initiatives promoting homeownership or addressing the unique needs of rural communities. By acknowledging these regional nuances, we can move beyond one-size-fits-all policies and work towards a more equitable and sustainable housing system for all.

When Can You Rent Joker? Availability Dates and Streaming Options

You may want to see also

Explore related products

![]()

Renting Trends: Historical growth and future projections of UK rental market

The UK rental market has undergone significant transformation over the past few decades, with the proportion of households renting their homes rising steadily. In the 1960s, only about 8% of households in England were private renters, while the majority were owner-occupiers or lived in social housing. Fast forward to 2021, and the English Housing Survey reveals that 20% of households now rent privately, with an additional 17% residing in social rented homes. This shift underscores a broader trend: renting is no longer a temporary phase but a long-term lifestyle choice for millions.

Analyzing the drivers behind this growth, several factors stand out. First, soaring house prices have made homeownership increasingly unattainable, particularly for younger generations. Between 1997 and 2022, average house prices in the UK increased by over 250%, far outpacing wage growth. Second, demographic changes, such as delayed marriage and smaller household sizes, have fueled demand for flexible living arrangements. Third, government policies, including the Right to Buy scheme, have reduced the stock of social housing, pushing more people into the private rental sector. These factors collectively explain why renting has become a dominant housing tenure.

Looking ahead, projections suggest the rental market will continue to expand, albeit with nuances. By 2030, some forecasts estimate that nearly 25% of UK households will be private renters, driven by persistent affordability challenges in the housing market. However, this growth is not without risks. Rising rents, currently outpacing inflation in many cities, could exacerbate housing insecurity for low-income households. Additionally, the quality of rental properties remains a concern, with 21% of private rented homes failing to meet the Decent Homes Standard in 2021. Policymakers and landlords must address these issues to ensure the sector’s sustainability.

A comparative analysis with other European countries highlights the UK’s unique position. In Germany, for instance, nearly 50% of households rent, thanks to robust tenant protections and a large social housing sector. In contrast, the UK’s rental market is characterized by shorter tenancies and higher costs, reflecting a more market-driven approach. To emulate the stability seen in countries like Germany, the UK could introduce reforms such as indefinite tenancies and stricter rent controls. Such measures would not only protect tenants but also foster a more balanced housing ecosystem.

For individuals navigating the rental market, practical strategies can mitigate challenges. Prospective renters should prioritize locations with strong tenant rights, such as London boroughs with active rent stabilization programs. Additionally, leveraging online platforms to compare rents and property conditions can help secure better deals. Finally, joining tenant unions or advocacy groups can provide support and amplify calls for policy changes. As the rental market evolves, staying informed and proactive will be key to thriving in this increasingly dominant housing sector.

Should Landlords Ask for Your Social Security Number?

You may want to see also

Explore related products

![]()

Affordability Crisis: Challenges faced by renters due to rising costs and low supply

In the UK, approximately 4.4 million households rent their homes from private landlords, a figure that has nearly doubled since 2007. This surge reflects a broader shift in housing dynamics, but it also underscores a growing crisis: affordability. Renters are increasingly squeezed by rising costs and a chronic shortage of available properties, creating a perfect storm of financial strain and insecurity.

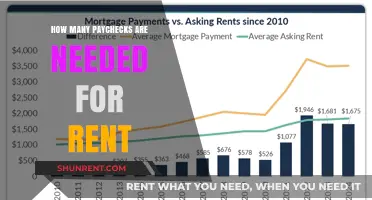

Consider the numbers: between 2015 and 2023, average rents in the UK rose by over 20%, outpacing wage growth in nearly every region. In London, renters now spend an average of 45% of their income on housing, compared to 30% a decade ago. This disparity isn’t limited to the capital; cities like Manchester, Bristol, and Edinburgh have seen similar spikes. For context, the Office for National Statistics recommends that housing costs should not exceed 30% of income to maintain financial stability. Yet, millions of renters are forced to allocate far more, leaving little room for savings, emergencies, or quality of life.

The root of this crisis lies in supply and demand. The UK has a housing deficit estimated at 4.3 million homes, with new builds failing to keep pace with population growth and changing household structures. Simultaneously, buy-to-let landlords are exiting the market due to tax changes and regulatory pressures, reducing available rental stock. This imbalance empowers landlords to raise rents, knowing tenants have few alternatives. For renters, this means constant competition for limited properties, often resulting in bidding wars that drive prices even higher.

The human cost of this crisis is profound. Young professionals delay starting families, unable to afford larger homes. Families are forced to move frequently, disrupting children’s education and social stability. Low-income households face the starkest choices: cut back on essentials like food and healthcare, or risk eviction. A 2022 Shelter report revealed that 1 in 5 renters had skipped meals to pay rent, while 1 in 10 had fallen behind on payments, risking homelessness.

To navigate this crisis, renters must adopt practical strategies. First, negotiate rent renewals by researching local market rates and presenting evidence of comparable properties. Second, consider shared housing or co-living arrangements to split costs, though this may sacrifice privacy. Third, explore government schemes like the Housing Benefit or Universal Credit, which can provide partial rent assistance for eligible households. Finally, advocate for policy changes, such as rent controls or increased investment in social housing, to address the systemic issues driving the crisis.

The affordability crisis isn’t just a financial issue—it’s a threat to social cohesion and individual well-being. Without urgent action, the gap between renters’ incomes and housing costs will only widen, leaving millions trapped in a cycle of instability. The question isn’t whether the crisis exists, but how long it will take to address it.

Renting Custom-Made Exhibitions in Belgium: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Policy Impact: Government housing policies and their effects on renting population

The UK's renting population has surged over the past two decades, with approximately 4.4 million households now renting privately and 4.1 million in social housing. This shift reflects broader trends in housing affordability, wage stagnation, and government policies. Among the most influential factors are government housing policies, which have both direct and indirect effects on the renting population. Understanding these policies and their impacts is crucial for tenants, landlords, and policymakers alike.

Consider the Help to Buy scheme, introduced in 2013, which aimed to boost homeownership by offering equity loans for new-build purchases. While it succeeded in increasing homeownership rates marginally, it inadvertently inflated house prices, making it harder for first-time buyers to enter the market without assistance. This price inflation has pushed more people into renting for longer periods, as saving for a deposit becomes increasingly unattainable. For instance, the average deposit in London now exceeds £100,000, a figure out of reach for many, especially younger renters under 35, who make up 45% of the private rental sector.

Another critical policy is the reduction in Local Housing Allowance (LHA) rates, which since 2020 have been frozen despite rising rents. This freeze has widened the gap between LHA rates and actual rental costs, leaving many low-income households vulnerable to homelessness or rent arrears. For example, in Manchester, the LHA covers only 78% of the median rent, forcing tenants to bridge the shortfall with other benefits or income. This policy not only exacerbates financial strain but also discourages landlords from accepting tenants on benefits, further limiting housing options for this demographic.

In contrast, the introduction of Section 21 'no-fault' eviction reforms in 2023 aims to provide greater security for renters by abolishing no-fault evictions. This policy shift is expected to reduce tenant turnover and encourage longer tenancies, which could improve stability for families and reduce the financial burden of frequent moves. However, landlords argue that removing this eviction mechanism may deter new entrants to the rental market, potentially reducing the overall supply of available properties. Early data suggests a 5% decrease in new rental listings in areas where the reforms have been piloted, highlighting the delicate balance between tenant protection and market dynamics.

Finally, the Right to Buy scheme, which allows social housing tenants to purchase their homes at a discount, has had a dual impact on the renting population. While it has enabled thousands to achieve homeownership, it has also depleted the social housing stock, with only one in five homes sold under the scheme being replaced. This reduction has increased competition for remaining social housing units, with waiting lists in some areas exceeding 10 years. Consequently, more households are forced into the private rental sector, where rents are typically higher and protections weaker.

In summary, government housing policies have profound and often unintended consequences for the UK's renting population. While initiatives like Help to Buy and Right to Buy aim to promote homeownership, they have inadvertently exacerbated rental demand and affordability issues. Meanwhile, policies like the LHA freeze and Section 21 reforms highlight the tension between protecting tenants and maintaining a viable rental market. For renters, staying informed about these policies and their implications is essential for navigating an increasingly complex housing landscape.

Renter Rights: Can You Deny Police Entry?

You may want to see also

Frequently asked questions

As of recent data, approximately 36% of households in the UK rent their homes, which equates to around 9 million households.

About 20% of UK households rent from private landlords, while the remaining 16% rent from housing associations or local authorities.

The number of renters in the UK has been steadily increasing over the past two decades, driven by factors such as rising house prices, tighter mortgage lending criteria, and a growing preference for flexibility among younger generations.