The prevalence of renting in the United States has become a significant aspect of the country's housing landscape, with millions of Americans opting for rental accommodations over homeownership. Understanding how many people in the U.S. live in rent is crucial for grasping the dynamics of the housing market, economic trends, and societal shifts. Recent data indicates that approximately one-third of the U.S. population resides in rental properties, a figure that has steadily risen due to factors such as increasing home prices, student debt, and changing lifestyle preferences, particularly among younger generations. This trend not only reflects broader economic challenges but also highlights the growing importance of rental housing as a vital component of the nation's residential infrastructure.

| Characteristics | Values (as of latest data, 2023) |

|---|---|

| Total U.S. Population | ~333.3 million |

| Percentage of Renters | ~35% |

| Number of Renters | ~116.7 million |

| Median Monthly Rent (National) | ~$1,300 |

| States with Highest Renter Rates | New York (48%), California (45%), Nevada (44%) |

| States with Lowest Renter Rates | West Virginia (26%), Mississippi (28%), Alabama (29%) |

| Age Group with Highest Renter Rate | 25-34 years old (50%) |

| Age Group with Lowest Renter Rate | 65+ years old (20%) |

| Average Household Size (Renters) | 2.1 persons |

| Percentage of Income Spent on Rent | ~30% (for many renters) |

| Rent Burdened Households | ~46% (spending >30% of income on rent) |

| Growth in Renter Population (2010-2023) | Increased by ~10 million |

Explore related products

$129.99 $137

What You'll Learn

- Rental Population Trends: Recent data on the number of renters in the United States

- Rent Burden Statistics: Percentage of income spent on rent by U.S. households

- Demographics of Renters: Age, income, and ethnicity distribution among renters in the U.S

- Urban vs. Rural Renting: Comparison of rental rates in cities versus rural areas

- Affordable Housing Crisis: Impact of rising rents on low-income households in the U.S

![]()

Rental Population Trends: Recent data on the number of renters in the United States

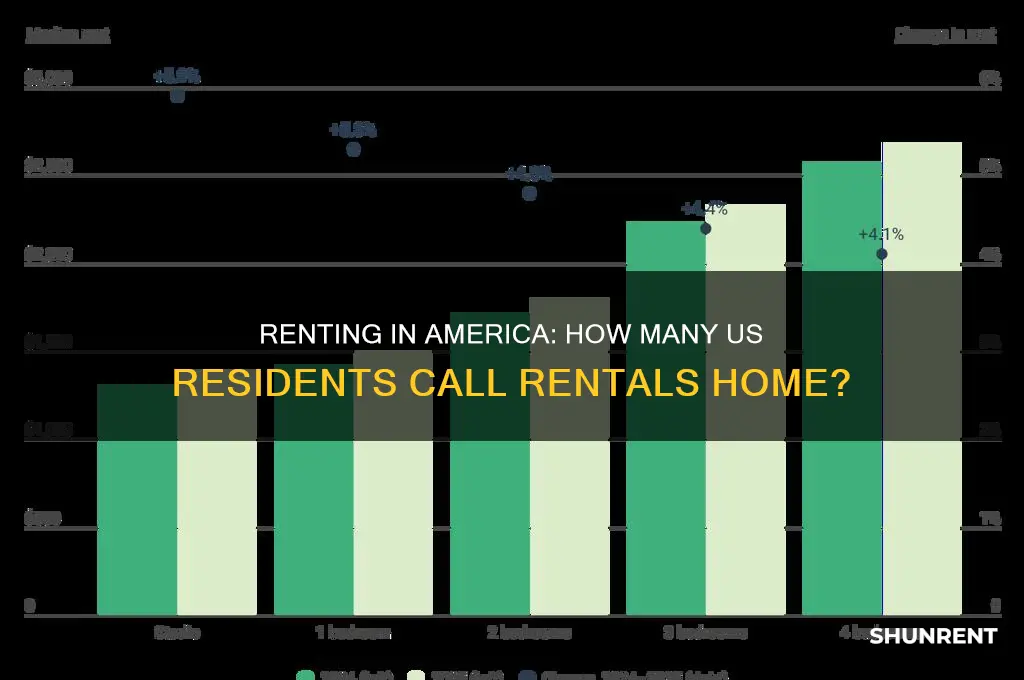

The rental population in the United States has been steadily growing over the past few decades, reflecting broader shifts in housing preferences, economic conditions, and demographic changes. Recent data from the U.S. Census Bureau indicates that approximately 36% of U.S. households are occupied by renters, translating to roughly 44 million rental units nationwide. This figure represents a significant portion of the population, highlighting the importance of the rental market in the overall housing landscape. The rise in renting can be attributed to factors such as increasing home prices, student loan debt, and a preference for flexibility among younger generations, particularly Millennials and Gen Z.

One of the most notable trends in rental population growth is the shift in urban and suburban dynamics. While urban areas have traditionally been hotspots for renters, recent years have seen a surge in suburban rental demand. This trend was accelerated by the COVID-19 pandemic, as remote work allowed individuals and families to seek more affordable and spacious housing outside city centers. As a result, suburban rental markets have experienced higher occupancy rates and rent growth, narrowing the gap between urban and suburban rental trends. This shift underscores the evolving preferences of renters, who increasingly prioritize value, space, and quality of life.

Demographic factors also play a crucial role in shaping rental population trends. Younger adults, particularly those aged 25 to 34, are the largest cohort of renters, with many delaying homeownership due to financial constraints and lifestyle choices. Additionally, minority populations, including Hispanic and Black households, are overrepresented in the rental market, often facing barriers to homeownership such as income disparities and limited access to credit. Understanding these demographic nuances is essential for policymakers and housing developers to address affordability and equity concerns in the rental sector.

Economic conditions have further influenced rental trends, with affordability emerging as a pressing issue. Rising rents, coupled with stagnant wage growth, have made it increasingly challenging for low- and middle-income households to secure adequate housing. In high-cost metropolitan areas like New York, San Francisco, and Los Angeles, rent burdens are particularly acute, with many renters spending more than 30% of their income on housing. This has led to a growing demand for affordable housing initiatives and rent control policies to mitigate the financial strain on renters.

Finally, the rental market is also being shaped by changes in housing supply and investment patterns. Institutional investors have become major players in the single-family rental market, acquiring properties and converting them into rental units. This trend has raised concerns about housing affordability and the potential for rent increases driven by profit motives. Simultaneously, there is a growing need for new rental construction to meet demand, particularly in fast-growing regions. Policymakers and stakeholders must balance these dynamics to ensure a sustainable and equitable rental housing market for the millions of Americans who call rental units home.

Jonesville, Michigan Rent-A-Center Hours: Late Night Options Available

You may want to see also

Explore related products

$55.47 $72.99

![]()

Rent Burden Statistics: Percentage of income spent on rent by U.S. households

According to recent data, approximately 36% of households in the United States are occupied by renters, which translates to around 44 million households. With such a significant portion of the population living in rented accommodations, understanding the financial implications of renting is crucial. One key aspect to consider is the rent burden, which refers to the percentage of income spent on rent by U.S. households. The U.S. Department of Housing and Urban Development (HUD) defines a household as being rent-burdened if it spends more than 30% of its income on rent and utility costs.

Rent burden statistics reveal that a substantial number of U.S. households are struggling to make ends meet due to high rental costs. As of 2022, approximately 46% of renter households in the U.S. are considered rent-burdened, spending over 30% of their income on rent. Furthermore, around 23% of renter households are severely rent-burdened, allocating more than 50% of their income towards rent. These figures highlight the growing affordability crisis in the rental market, particularly in urban areas where rental prices are soaring. Low-income households, in particular, are disproportionately affected by rent burdens, with many forced to make difficult choices between paying rent and covering other essential expenses.

The rent burden is not limited to low-income households; middle-income households are also feeling the pinch. In recent years, the percentage of middle-income renter households spending more than 30% of their income on rent has increased significantly. This trend can be attributed to various factors, including stagnant wages, rising rental prices, and limited housing supply. As a result, many households are being forced to compromise on other aspects of their lives, such as healthcare, education, and retirement savings, to keep up with rental costs. The consequences of rent burdens can be far-reaching, impacting not only individual households but also the broader economy.

Geographic location plays a significant role in determining the severity of rent burdens. Coastal cities, such as New York, Los Angeles, and San Francisco, have some of the highest rental prices in the country, making it challenging for residents to find affordable housing. In these areas, the percentage of rent-burdened households can exceed 50%, with many residents spending upwards of 50-60% of their income on rent. In contrast, smaller cities and rural areas tend to have lower rental prices, resulting in lower rent burdens. However, even in these areas, the lack of affordable housing options can still pose challenges for low-income households.

To address the issue of rent burdens, policymakers and housing advocates are exploring various solutions, including increasing the supply of affordable housing, implementing rent control measures, and expanding housing assistance programs. Additionally, initiatives aimed at increasing wages and providing financial literacy education can help households better manage their rental expenses. By understanding the rent burden statistics and the factors contributing to them, stakeholders can work towards developing effective strategies to alleviate the financial strain on U.S. households living in rented accommodations. Ultimately, addressing the rent burden crisis is essential for promoting economic stability, reducing poverty, and improving the overall well-being of millions of Americans.

Palm Beach ZEE: Power Chair Rentals Available?

You may want to see also

Explore related products

![]()

Demographics of Renters: Age, income, and ethnicity distribution among renters in the U.S

The demographics of renters in the United States reveal a diverse and multifaceted landscape, shaped by age, income, and ethnicity. According to recent data from the U.S. Census Bureau, approximately 36% of households in the U.S. are occupied by renters, totaling around 44 million households. This significant portion of the population highlights the importance of understanding who these renters are and the factors influencing their housing choices.

Age Distribution Among Renters

Renters in the U.S. span a wide range of age groups, but younger adults dominate this demographic. Approximately 60% of renters are under the age of 45, with the largest share (around 30%) falling between the ages of 25 and 34. This age group often includes young professionals, recent college graduates, and individuals starting families who may not yet be ready or able to purchase a home. Renting provides flexibility and lower upfront costs, making it an attractive option for this cohort. Conversely, older adults aged 65 and above make up a smaller but notable portion of renters, often due to downsizing or financial constraints.

Income Levels and Renting

Income plays a critical role in determining who rents in the U.S. A significant percentage of renters fall into lower- and middle-income brackets. Data indicates that nearly 50% of renters have household incomes below $50,000 annually, with many relying on renting as a more affordable housing option compared to homeownership. Conversely, high-income earners are less likely to rent, as they often have the financial means to purchase property. However, in expensive urban markets like New York or San Francisco, even higher-income individuals may choose to rent due to the high cost of buying a home.

Ethnicity and Racial Distribution

Ethnicity and race are key factors in the renter demographic. Minority groups are overrepresented among renters, with Hispanic and Black households accounting for a disproportionately large share. Approximately 45% of Hispanic households and 42% of Black households rent their homes, compared to 28% of white households. This disparity is often linked to historical and systemic factors, including income inequality, limited access to credit, and housing discrimination. Asian households, while diverse in their housing choices, also have a notable renter population, particularly in urban areas.

Urban vs. Rural Renting Trends

Geography further influences renter demographics. Urban areas, where housing costs are typically higher, have a larger concentration of renters. In cities like Los Angeles, New York, and Miami, renting is the norm, with rates often exceeding 50% of households. In contrast, rural areas tend to have lower renting rates, as homeownership is more feasible due to lower property prices. However, even in rural regions, renting remains a critical option for low-income individuals and families who cannot afford to buy homes.

Understanding the demographics of renters in the U.S. is essential for policymakers, developers, and advocates working to address housing affordability and equity. By examining age, income, ethnicity, and geographic trends, stakeholders can better tailor solutions to meet the diverse needs of the millions of Americans who call rental properties home.

Illinois Renters' Rights: AC Requirements Explained

You may want to see also

Explore related products

![]()

Urban vs. Rural Renting: Comparison of rental rates in cities versus rural areas

The rental landscape in the United States presents a stark contrast between urban and rural areas, with significant differences in rental rates, housing availability, and tenant demographics. According to recent data, approximately 36% of households in the U.S. are renter-occupied, totaling around 44 million households. This figure highlights the substantial portion of the population that relies on renting as a housing solution. When comparing urban and rural renting, several key factors emerge, primarily driven by demand, cost of living, and local economies.

In urban areas, rental rates are generally higher due to increased demand for housing in densely populated cities. Metropolitan hubs like New York, San Francisco, and Los Angeles often see median rents exceeding $2,000 per month for one-bedroom apartments. This is largely attributed to limited land availability, high construction costs, and the concentration of job opportunities. Urban renters are often willing to pay a premium for proximity to workplaces, cultural amenities, and public transportation. However, the high cost of urban renting can lead to housing affordability challenges, with many households spending a disproportionate share of their income on rent.

In contrast, rural areas typically offer significantly lower rental rates, with median rents often falling below $1,000 per month. This affordability is driven by lower demand, larger land availability, and a slower pace of economic activity. Rural renting is particularly attractive for those seeking cost-effective housing, larger living spaces, and a quieter lifestyle. However, rural renters may face limited access to job opportunities, healthcare, and other essential services, which can offset the financial benefits of lower rent. Additionally, the rental market in rural areas is often less dynamic, with fewer options and slower turnover compared to urban centers.

Another critical aspect of urban vs. rural renting is the type of housing available. Urban areas dominate the multifamily rental market, with apartments and condos being the most common options. In rural areas, single-family homes and mobile homes are more prevalent, offering renters more space and privacy at a lower cost. This difference in housing stock reflects the varying preferences and needs of urban and rural tenants. For instance, urban renters often prioritize convenience and accessibility, while rural renters may value larger yards and a sense of community.

Economic factors also play a significant role in the urban-rural rental divide. Urban areas, being centers of economic activity, attract a diverse range of renters, including young professionals, students, and families. In contrast, rural areas often have smaller, more homogeneous renter populations, including low-income households, retirees, and individuals seeking affordable housing. Government policies and subsidies, such as Section 8 vouchers, are more frequently utilized in rural areas to address housing affordability, whereas urban areas may rely on market-driven solutions and rent control measures.

In conclusion, the comparison of rental rates in urban versus rural areas reveals a clear dichotomy shaped by demand, cost of living, and local economies. While urban renting offers proximity to opportunities and amenities at a higher cost, rural renting provides affordability and space but with potential trade-offs in accessibility and services. Understanding these differences is essential for renters, policymakers, and investors navigating the diverse rental market across the United States. As the number of renters continues to grow, addressing the unique challenges of both urban and rural renting will be crucial in ensuring housing stability for millions of Americans.

Calculating Percentage Rent: Understanding Artificial Breakpoint Examples

You may want to see also

Explore related products

![]()

Affordable Housing Crisis: Impact of rising rents on low-income households in the U.S

The affordable housing crisis in the United States has reached a critical point, with rising rents disproportionately affecting low-income households. According to recent data, approximately 43 million households in the U.S. are renters, accounting for about 35% of the total population. Among these renters, a significant portion are low-income families who spend a staggering 30% or more of their income on housing, a threshold that the U.S. Department of Housing and Urban Development (HUD) defines as cost-burdened. This financial strain leaves little room for other essential expenses like food, healthcare, and education, exacerbating the cycle of poverty.

One of the most direct impacts of rising rents is the increased risk of eviction and homelessness. As rents outpace wage growth, low-income households are often forced to choose between paying rent and meeting other basic needs. This precarious situation is further compounded by the lack of available affordable housing units. The National Low Income Housing Coalition reports that no state in the U.S. has an adequate supply of rental homes affordable to extremely low-income renters, who make up nearly a quarter of all renter households. Consequently, many families are pushed into substandard living conditions or face the constant threat of displacement.

The crisis also has long-term economic and social implications for low-income households. High housing costs limit the ability of families to save for emergencies, invest in education, or pursue economic opportunities. Children growing up in cost-burdened households often face barriers to academic success due to housing instability, which can lead to frequent school changes and inadequate living environments. Additionally, the stress of housing insecurity contributes to mental and physical health issues, further entrenching families in poverty. These challenges highlight the urgent need for comprehensive solutions to address the affordable housing shortage.

Policy interventions are critical to mitigating the impact of rising rents on low-income households. Expanding federal programs like the Housing Choice Voucher (HCV) program, commonly known as Section 8, could provide more families with rental assistance. However, only one in four eligible households currently receive such aid due to funding limitations. Increasing investments in the construction and preservation of affordable housing units, as well as implementing rent control measures in high-cost areas, could also help stabilize housing markets. Local governments and nonprofits play a vital role in these efforts by identifying and addressing the unique needs of their communities.

Ultimately, the affordable housing crisis is not just a housing issue but a broader social and economic challenge that requires immediate attention. Rising rents are pushing low-income households to the brink, threatening their stability and well-being. Addressing this crisis demands a multi-faceted approach that includes increased funding, policy reforms, and community-driven initiatives. Without decisive action, millions of Americans will continue to struggle under the weight of unaffordable housing, perpetuating inequality and hindering economic mobility for generations to come.

Aaron's and Rent-A-Center: Different Brands, Same Company?

You may want to see also

Frequently asked questions

As of recent data, approximately 2.5 million people in the US live in rent-controlled housing, primarily in states like New York, California, and New Jersey.

About 36% of the US population, or roughly 115 million people, live in rental housing as of the latest census data.

There are approximately 44 million renter households in the US, compared to about 82 million homeowner households.

The average rent in the US is around $1,700 per month, though this varies significantly by location, with cities like San Francisco and New York having much higher averages.