Renting is a prevalent housing choice in the United States, with millions of individuals and families opting for rental properties over homeownership. As of recent data, approximately one-third of all households in the U.S. are renter-occupied, reflecting a significant portion of the population that relies on the rental market for their housing needs. This trend is driven by factors such as affordability, flexibility, and lifestyle preferences, particularly among younger generations, urban dwellers, and those in transitional life stages. Understanding the scale and dynamics of renting in the U.S. provides valuable insights into the nation’s housing landscape and the economic and social factors shaping it.

Explore related products

What You'll Learn

- Rental Trends by State: Variations in rental rates and preferences across different U.S. states

- Demographics of Renters: Age, income, and family status of people renting homes in the U.S

- Urban vs. Rural Renting: Differences in rental rates and availability between cities and rural areas

- Affordable Housing Crisis: Challenges and statistics on affordable rental housing in the U.S

- Renting vs. Owning: Comparison of the number of renters versus homeowners in the U.S

![]()

Rental Trends by State: Variations in rental rates and preferences across different U.S. states

As of recent data, approximately 36% of U.S. households are renter-occupied, translating to over 44 million renting households. This national average, however, masks significant variations across states, driven by factors like local economies, housing supply, and demographic preferences. For instance, in California, where the median rent exceeds $2,500, renters make up 45% of households, while in West Virginia, where rents average around $750, only 28% of households rent. These disparities highlight the importance of understanding state-specific rental trends for both renters and investors.

Consider the Northeast, where high population density and limited land availability have pushed rental rates upward. In Massachusetts, 37% of residents rent, with Boston’s median rent surpassing $3,000. Conversely, in the South, states like Mississippi and Arkansas report rental rates below $1,000, with renter populations hovering around 30%. These regional differences are further amplified by local economies: tech hubs like Washington (41% renters) and Colorado (36% renters) see higher demand for rentals due to job growth, while rural states like South Dakota (27% renters) maintain lower rental rates due to slower population growth.

Preferences also vary widely. In urban-centric states like New York (48% renters), studio and one-bedroom apartments dominate, catering to young professionals and students. In contrast, Sun Belt states like Texas (35% renters) and Arizona (34% renters) see higher demand for single-family rental homes, appealing to families and retirees. Amenities play a role too: in California, renters prioritize pet-friendly units and eco-friendly features, while in the Midwest, affordability and proximity to public transportation often take precedence.

For those navigating these trends, practical strategies are key. Renters in high-cost states like Hawaii (43% renters) should consider roommates or suburban relocation to offset expenses. Investors, meanwhile, can capitalize on emerging markets like Idaho (32% renters), where rental demand is growing due to migration trends. Policymakers must address supply shortages in states like Nevada (46% renters) to prevent further rent inflation. By analyzing these state-specific dynamics, stakeholders can make informed decisions in a diverse rental landscape.

Square Foot Pricing: A Guide to Setting Competitive Rent Prices

You may want to see also

Explore related products

![]()

Demographics of Renters: Age, income, and family status of people renting homes in the U.S

In the United States, approximately 36% of households rent their homes, a figure that has steadily risen over the past few decades. This shift reflects broader economic and social trends, but who exactly are these renters? Understanding the demographics—specifically age, income, and family status—provides critical insights into the rental market’s dynamics.

Age plays a pivotal role in rental demographics. Millennials, aged 25 to 40, constitute the largest share of renters, driven by factors like student debt, delayed homeownership, and urban job opportunities. However, Gen Z, now entering their 20s, is quickly becoming a significant renter cohort, particularly in metropolitan areas. Conversely, renters over 65 are the fastest-growing segment, often choosing to downsize or prioritize flexibility over homeownership. This age diversity underscores the rental market’s adaptability to varying life stages.

Income levels further stratify the renter population. While renting is often associated with lower-income households, a growing number of middle- and high-income earners are opting to rent, particularly in high-cost cities like San Francisco and New York. For instance, nearly 20% of renters earn over $100,000 annually, citing lifestyle preferences and financial flexibility as key reasons. Conversely, low-income renters, earning under $30,000, face significant challenges, with over 50% being cost-burdened, spending more than 30% of their income on rent.

Family status also shapes rental trends. Single individuals and childless couples dominate the rental market, often prioritizing proximity to work and urban amenities. However, families with children account for a substantial portion of renters, particularly in suburban areas. These families often face unique challenges, such as limited affordable housing options and the need for larger units. Interestingly, multigenerational households are increasingly renting, driven by cultural norms and economic necessity, particularly among immigrant communities.

To navigate this landscape, renters should consider their long-term financial goals and lifestyle needs. For younger renters, building credit and saving for a down payment can pave the way to homeownership. Middle-aged renters might prioritize stability and amenities, while older renters may seek low-maintenance options. Regardless of age or income, understanding these demographics empowers renters to make informed decisions in a competitive market.

Exploring Japan's Average Rent: Costs, Trends, and Regional Variations

You may want to see also

Explore related products

![]()

Urban vs. Rural Renting: Differences in rental rates and availability between cities and rural areas

In the United States, approximately 36% of households rent their homes, totaling around 44 million households. This figure highlights the significant role renting plays in the housing market. However, the rental landscape is far from uniform, with stark differences emerging between urban and rural areas. These disparities in rental rates and availability are shaped by factors such as population density, economic opportunities, and local housing demand.

Consider the cost of renting in urban centers, where rental rates often soar due to high demand and limited space. For instance, in cities like New York or San Francisco, median rents can exceed $3,000 per month for a one-bedroom apartment. This is largely driven by the concentration of jobs, cultural amenities, and infrastructure that attract residents. In contrast, rural areas typically offer more affordable options, with median rents often falling below $1,000 per month. However, these lower costs come with trade-offs, such as fewer job opportunities and limited access to services.

Availability is another critical factor distinguishing urban and rural renting. In cities, the rental market is highly competitive, with vacancy rates frequently below 5%. This scarcity forces renters to act quickly, often settling for less-than-ideal conditions or higher costs. Rural areas, on the other hand, generally have higher vacancy rates, providing renters with more options and negotiating power. Yet, the availability in rural regions is often limited by the sheer number of rental units, as these areas lack the dense housing developments common in urban centers.

For those considering a move, understanding these differences is essential. Urban renters should budget for higher costs and be prepared to navigate a fast-paced market. Rural renters, while benefiting from lower prices, may need to prioritize proximity to essential services or employment hubs. Additionally, rural renters should be aware of the potential for limited public transportation, which can impact daily commutes and accessibility.

In conclusion, the urban-rural divide in renting is characterized by contrasting rental rates and availability. Urban areas offer convenience and opportunity at a premium, while rural regions provide affordability with fewer amenities. By weighing these factors, renters can make informed decisions that align with their lifestyle and financial goals. Whether in the city or the countryside, understanding these dynamics is key to finding the right rental home.

Renting Tow-Behind Sprayers in Danville, KY: Top Locations Guide

You may want to see also

Explore related products

![]()

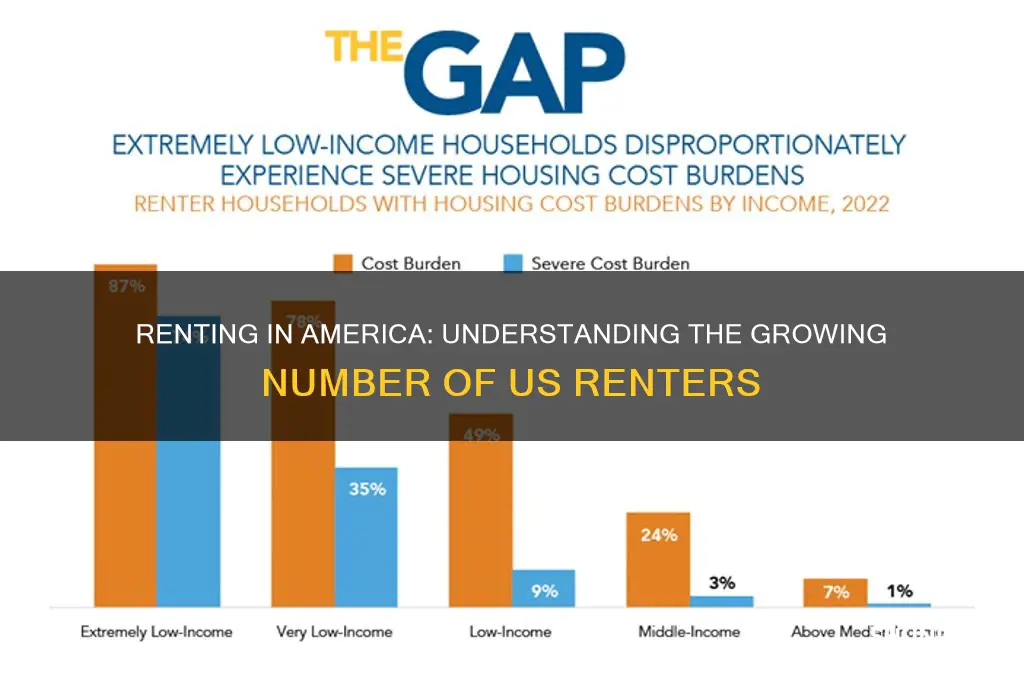

Affordable Housing Crisis: Challenges and statistics on affordable rental housing in the U.S

In the United States, over 43 million households rent their homes, accounting for nearly 36% of all occupied housing units. This staggering number highlights the critical role rental housing plays in the nation’s housing market. However, the growing affordable housing crisis has left millions of renters struggling to keep up with rising costs. According to the National Low Income Housing Coalition, a full-time worker earning the federal minimum wage cannot afford a modest two-bedroom rental in any U.S. state, underscoring the severity of the issue.

One of the primary challenges in the affordable rental housing crisis is the widening gap between supply and demand. Over the past decade, the construction of new rental units has failed to keep pace with population growth and shifting housing preferences, particularly among millennials and younger generations. Meanwhile, the loss of naturally occurring affordable housing (NOAH)—older, privately owned units that are relatively inexpensive—has accelerated due to gentrification and property conversions. This dual pressure has pushed rents upward, leaving low- and moderate-income households with fewer options.

Another critical factor exacerbating the crisis is the insufficient funding for affordable housing programs. The U.S. Department of Housing and Urban Development (HUD) estimates that only one in four eligible households receives federal rental assistance due to limited resources. Additionally, the expiration of affordability restrictions on subsidized properties further reduces the stock of low-cost units. Without significant investment in preservation and expansion efforts, the shortage of affordable rentals will continue to worsen, disproportionately affecting vulnerable populations such as seniors, people with disabilities, and families with children.

To address this crisis, policymakers and stakeholders must adopt a multi-faceted approach. First, increasing funding for programs like the Housing Choice Voucher (HCV) program and the Low-Income Housing Tax Credit (LIHTC) can help expand access to affordable units. Second, incentivizing the preservation of existing affordable housing through grants, loans, and tax incentives can prevent further loss of NOAH properties. Finally, zoning reforms that promote higher-density, mixed-income developments can encourage the construction of new affordable units in high-opportunity areas. By tackling these challenges head-on, the U.S. can move closer to ensuring that all renters have access to safe, stable, and affordable housing.

Understanding Last Month's Rent: A Comprehensive Guide for Tenants

You may want to see also

Explore related products

$16.95 $35

$2.99 $18.99

$162.09 $239

![]()

Renting vs. Owning: Comparison of the number of renters versus homeowners in the U.S

In the United States, approximately 36% of households are occupied by renters, while 64% are homeowners, according to recent Census Bureau data. This disparity highlights a significant divide in housing preferences and financial realities. Renting often appeals to younger adults, urban dwellers, and those seeking flexibility, while homeownership is more common among older, more financially established individuals. Understanding these numbers provides insight into broader economic trends, such as affordability challenges and shifting lifestyle priorities.

Analyzing the data reveals that renting is particularly prevalent among millennials and Gen Z, who face student loan debt, rising home prices, and a desire for mobility. For instance, in cities like New York and San Francisco, where median home prices exceed $1 million, renting is often the only viable option. Conversely, homeownership rates are highest in suburban and rural areas, where housing is more affordable and families seek stability. This urban-suburban divide underscores the influence of geography on housing choices.

From a financial perspective, renting can be more cost-effective in the short term, as it avoids upfront costs like down payments and closing fees. However, over time, homeowners build equity and benefit from property appreciation, making ownership a long-term investment. For example, a renter paying $1,500 monthly over 10 years spends $180,000 without building equity, whereas a homeowner’s mortgage payments contribute to an asset. This comparison emphasizes the trade-offs between immediate affordability and future wealth accumulation.

Persuasively, the rise in renting also reflects changing societal values. Younger generations increasingly prioritize experiences over assets, viewing homeownership as a burden rather than a milestone. Additionally, the gig economy and remote work have made location flexibility a priority, favoring renting. Policymakers must address this shift by expanding affordable housing options and rental protections to ensure stability for the growing renter population.

In conclusion, the renter-homeowner split in the U.S. is shaped by demographics, economics, and cultural shifts. While renting offers flexibility and accessibility, homeownership remains a cornerstone of financial stability. Balancing these dynamics requires targeted solutions, such as incentivizing affordable housing development and educating renters on pathways to ownership. Understanding these trends is essential for individuals navigating their housing choices and for policymakers addressing the nation’s housing needs.

Win Big: Rent a Lambo in Vegas Contest Guide

You may want to see also

Frequently asked questions

As of the latest data (2023), approximately 43 million households in the US rent their homes, representing about 35% of all households.

About 35-36% of the US population lives in rental housing, with the exact percentage varying slightly depending on the source and year of the data.

Younger adults, particularly those aged 25-34, are the most likely to rent, with over 50% of households in this age group renting their homes.

The number of renters in the US has been steadily increasing over the past decade, driven by factors such as rising home prices, student debt, and lifestyle preferences, especially among younger generations.