Determining how much of one's income should be allocated to rent is a critical financial decision that impacts overall stability and well-being. A widely accepted guideline, often referred to as the 30% rule, suggests that individuals should spend no more than 30% of their gross monthly income on housing costs, including rent. This rule aims to ensure that renters have enough funds left for other essential expenses, savings, and discretionary spending. However, factors such as location, income level, and personal financial goals can influence this percentage, making it important to assess individual circumstances. In high-cost urban areas, for instance, renters may need to allocate a higher portion of their income to housing, while those in more affordable regions might aim for a lower percentage. Understanding this balance is key to maintaining financial health and avoiding rent burden.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less of gross monthly income (widely accepted rule of thumb) |

| Average Rent Burden in the U.S. | ~30-40% of income (varies by location and income level) |

| Low-Income Households | Often spend 50% or more of income on rent |

| High-Cost Urban Areas | Rent can exceed 50% of income (e.g., San Francisco, New York City) |

| Affordable Housing Definition | Housing costs ≤ 30% of household income (U.S. Department of Housing and Urban Development) |

| Median Rent-to-Income Ratio (U.S.) | ~25-35% (as of recent data) |

| International Averages | Varies; e.g., 20-30% in Europe, higher in developing countries |

| Impact of Inflation | Rising rents outpace income growth, increasing rent burden |

| Government Assistance Threshold | Households spending >30% on rent are considered cost-burdened |

| Generational Differences | Younger generations (Millennials, Gen Z) often spend >40% on rent |

Explore related products

What You'll Learn

- Affordable Rent Thresholds: Guidelines for determining a sustainable rent percentage based on income levels

- Regional Cost Variations: How rent-to-income ratios differ across cities and countries

- Budgeting Strategies: Tips for allocating income to rent while covering other expenses

- Housing Market Trends: Impact of market fluctuations on rent affordability percentages

- Government Assistance Programs: Subsidies and policies to reduce rent burden on low-income households

![]()

Affordable Rent Thresholds: Guidelines for determining a sustainable rent percentage based on income levels

A widely accepted rule of thumb suggests allocating 30% of gross income to rent, a guideline rooted in decades of housing policy. This benchmark, however, oversimplifies the complexities of modern financial realities. For instance, a single earner making $40,000 annually would theoretically spend $1,000 monthly on rent, leaving $2,000 for utilities, groceries, transportation, healthcare, and savings—a tightrope walk for many. This one-size-fits-all approach fails to account for regional cost disparities, debt obligations, and fluctuating income levels, particularly among younger or lower-income households.

To refine this threshold, consider a tiered approach based on income brackets. For households earning below the median income, a 25% rent-to-income ratio may be more sustainable, allowing greater flexibility for essentials and emergencies. Conversely, higher earners might comfortably allocate 35–40% without compromising financial stability, provided they maintain robust savings and investment habits. For example, a dual-income household earning $120,000 could afford $3,000 monthly rent while still saving 20% of their income, a luxury unattainable for those in lower brackets.

Practical implementation requires a reality check. Start by calculating your gross monthly income and multiplying it by your target percentage (e.g., 0.25 for lower incomes, 0.30 for middle incomes). Next, subtract fixed expenses like student loans or childcare to determine your *effective* rent budget. For instance, a $3,500 monthly income with $500 in fixed expenses would yield a realistic rent cap of $875 (25% of $3,500 minus $500). Tools like budgeting apps or rent calculators can streamline this process, ensuring alignment with your financial goals.

Critics argue that income-based thresholds ignore systemic issues like wage stagnation and housing supply shortages. While true, these guidelines serve as a starting point for individual decision-making, not a solution to broader affordability crises. Pairing them with strategies like roommate sharing, rent negotiation, or relocating to lower-cost areas can bridge the gap between theory and practice. Ultimately, the goal is not rigid adherence to a percentage but fostering financial resilience through informed, context-specific choices.

Rent-to-Own Businesses: Current Trends, Challenges, and Future Outlook

You may want to see also

Explore related products

![]()

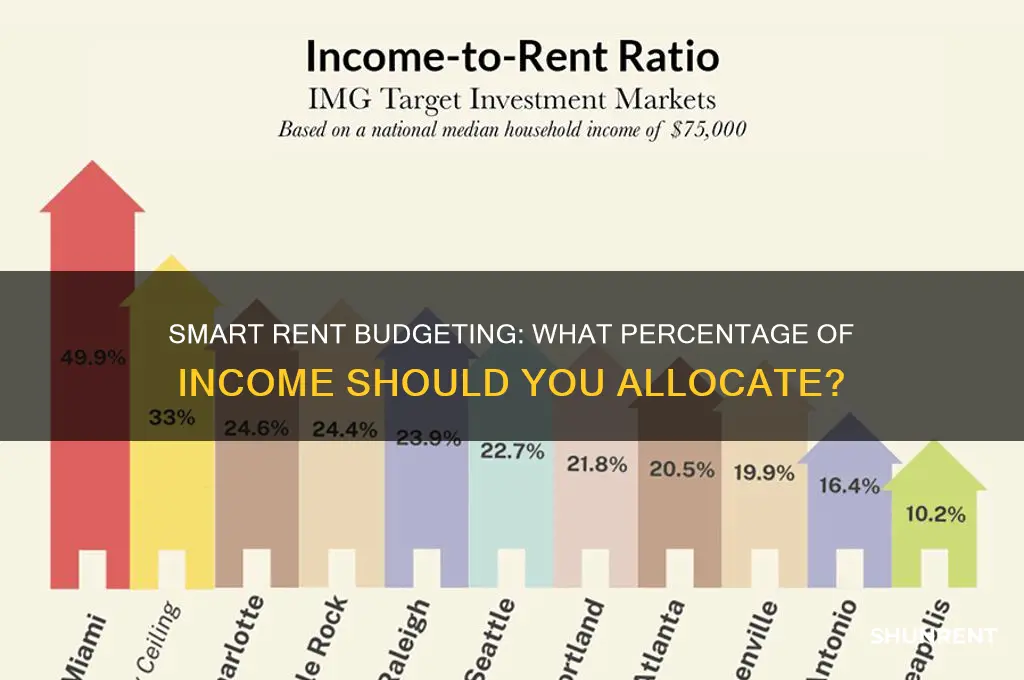

Regional Cost Variations: How rent-to-income ratios differ across cities and countries

Rent-to-income ratios are not one-size-fits-all; they fluctuate dramatically based on geographic location, reflecting disparities in local economies, housing markets, and living standards. For instance, in New York City, renters often allocate 40–50% of their income to housing, far exceeding the commonly recommended 30% threshold. In contrast, cities like Berlin or Tokyo maintain ratios closer to 20–25%, thanks to robust tenant protections and denser housing supply. These variations underscore the importance of contextualizing affordability rather than applying a universal benchmark.

To navigate these differences, consider the 50/30/20 rule as a flexible framework: 50% of income for necessities (including rent), 30% for discretionary spending, and 20% for savings. However, in high-cost cities like San Francisco or London, this model may require adjustments, such as reducing discretionary spending or seeking roommates to lower rent burdens. Conversely, in lower-cost regions like Lisbon or Mexico City, renters might allocate less than 25% of income to housing, freeing up funds for savings or investments.

A comparative analysis reveals that rent-to-income ratios are shaped by policy and market dynamics. In Munich, strict rent control laws keep ratios at 25%, while in Miami, a lack of such protections pushes ratios to 35–40%. Similarly, in Singapore, government-subsidized housing lowers ratios to 20%, whereas in Sydney, limited supply drives ratios above 40%. These examples highlight how regional policies and market conditions directly influence affordability.

For practical decision-making, research local averages before relocating or renegotiating rent. Tools like Numbeo or government housing reports provide city-specific data. If moving internationally, factor in currency exchange rates and local taxes, as these can skew perceived affordability. For example, a 30% rent-to-income ratio in Zurich feels manageable due to high wages, while the same ratio in Rio de Janeiro may strain budgets due to lower average incomes.

Ultimately, understanding regional cost variations empowers renters to make informed choices. Instead of fixating on a single percentage, adopt a dynamic approach tailored to your location. In expensive cities, prioritize budgeting strategies like shared housing or remote work to offset high rents. In affordable areas, leverage lower housing costs to accelerate savings or investments. By aligning rent-to-income ratios with local realities, you can achieve financial stability regardless of where you live.

Navigating Rent Increases: A Guide to Communicating with Tenants Effectively

You may want to see also

Explore related products

![]()

Budgeting Strategies: Tips for allocating income to rent while covering other expenses

A common rule of thumb suggests allocating no more than 30% of your income to rent, but this guideline often oversimplifies the complexities of personal finance. For instance, a young professional in a high-cost city like San Francisco might spend closer to 50% of their income on rent, while someone in a rural area could allocate as little as 20%. The key lies in balancing this expense with other financial obligations, such as groceries, transportation, and savings. To achieve this, start by categorizing your income into essential and discretionary spending, ensuring rent doesn’t overshadow critical needs like emergency funds or debt repayment.

One effective strategy is the 50/30/20 rule, which divides income into 50% for necessities (including rent), 30% for wants, and 20% for savings and debt. However, this framework may not fit everyone. For example, a freelancer with irregular income might prioritize a larger emergency fund, reducing their rent allocation to 25% or less. Conversely, a dual-income household with stable jobs could comfortably allocate closer to 35% for housing if it aligns with their long-term goals. The takeaway? Flexibility is crucial—adjust percentages based on your unique circumstances.

Another practical tip is to negotiate rent or explore cost-saving housing options. For instance, sharing a living space can reduce rent by 30–50%, freeing up funds for other expenses. Alternatively, consider relocating to a more affordable neighborhood or opting for a smaller unit. Pair this with a zero-based budget, where every dollar is assigned a purpose, to ensure rent doesn’t cannibalize savings or leisure spending. Tools like budgeting apps can automate this process, providing real-time insights into your financial health.

Finally, prioritize long-term financial goals when allocating income to rent. For young adults in their 20s and 30s, building a robust savings foundation—such as a 3–6 month emergency fund or retirement contributions—should take precedence over luxurious housing. For older individuals nearing retirement, minimizing rent to 20–25% of income can accelerate debt payoff and retirement savings. By viewing rent as part of a broader financial strategy, you can avoid the trap of overspending on housing while neglecting other critical areas of your budget.

Exploring Andover: Do People Rent and Visit This Charming Town?

You may want to see also

Explore related products

$9.99

![]()

Housing Market Trends: Impact of market fluctuations on rent affordability percentages

The 30% rule, a long-standing guideline suggesting households should allocate no more than 30% of their income to rent, is increasingly under pressure due to volatile housing market trends. In cities like San Francisco and New York, where rent-to-income ratios often exceed 40%, this rule feels outdated. Market fluctuations, driven by factors like interest rates, supply shortages, and economic shifts, have pushed rental prices upward, forcing renters to adjust their budgets dramatically. For instance, a 2022 study revealed that in 90% of U.S. metro areas, renters earning the median income spend more than 30% on housing, highlighting the rule’s diminishing practicality.

Analyzing the impact of market fluctuations reveals a stark disparity between high-demand urban centers and smaller, more stable markets. In Austin, Texas, for example, a 25% surge in rental prices over two years has pushed the average rent-to-income ratio to 38%, leaving many residents cost-burdened. Conversely, in cities like Cleveland, where rental prices have remained relatively stable, the 30% threshold remains achievable for most households. This contrast underscores how localized market dynamics dictate affordability, making a one-size-fits-all rule like the 30% guideline increasingly insufficient.

For renters navigating these trends, adaptability is key. A practical strategy is to reassess housing priorities and explore alternatives like roommate arrangements or suburban living, which can reduce rent-to-income ratios by 10–15 percentage points. Additionally, tracking local market indicators, such as vacancy rates and new construction pipelines, can provide early warnings of impending price shifts. For instance, a vacancy rate below 4% often signals an impending rent hike, prompting renters to lock in leases or consider relocation before costs escalate further.

Persuasively, policymakers must address the root causes of market volatility to restore rent affordability. Incentivizing affordable housing development, implementing rent control measures in overheated markets, and expanding housing vouchers are proven strategies to mitigate the impact of fluctuations. Without intervention, the growing gap between income and rent will exacerbate housing insecurity, particularly for low- and middle-income households. The 30% rule, while aspirational, cannot serve as the sole benchmark in a market where external forces continually reshape affordability.

In conclusion, the interplay between housing market trends and rent affordability percentages demands a nuanced approach. Renters must stay informed and flexible, while policymakers need to enact targeted solutions to stabilize volatile markets. The 30% rule, though widely cited, is no longer a universal standard but rather a starting point for understanding the complex dynamics of rent affordability in an ever-changing landscape.

Rent Paid Certificates: What's Their Role in Tax Filing?

You may want to see also

Explore related products

![]()

Government Assistance Programs: Subsidies and policies to reduce rent burden on low-income households

A common rule of thumb suggests that households should spend no more than 30% of their income on rent to maintain financial stability. However, for low-income families, this threshold is often unattainable, leading to housing insecurity and economic strain. Government assistance programs have emerged as a critical tool to bridge this gap, offering subsidies and policies designed to alleviate the rent burden on vulnerable populations. These initiatives not only provide immediate relief but also aim to foster long-term housing affordability and stability.

One of the most prominent examples is the Housing Choice Voucher Program, commonly known as Section 8, in the United States. This program provides eligible low-income households with vouchers that cover the difference between 30% of their income and the rent of a qualifying unit. For instance, a family earning $2,000 per month would pay $600 toward rent, with the voucher covering the remainder. This model ensures that families are not forced to allocate an unsustainable portion of their income to housing, allowing them to allocate resources to other essential needs like food, healthcare, and education.

Another approach is the implementation of rent control policies, which cap annual rent increases to prevent sudden, unaffordable hikes. Cities like Berlin and New York have experimented with such measures, though their effectiveness varies. While rent control can provide short-term relief, it may also discourage new housing development, potentially exacerbating long-term affordability issues. Governments must therefore balance immediate needs with strategies that encourage housing supply growth, such as tax incentives for developers building affordable units.

In addition to direct subsidies, some governments offer tax credits to low-income renters. The Low-Income Housing Tax Credit (LIHTC) program in the U.S., for example, incentivizes private developers to build affordable housing by providing tax credits in exchange for reduced rents. This policy not only increases the availability of affordable units but also leverages private investment to address public housing needs. Similarly, programs like the Earned Income Tax Credit (EITC) indirectly support renters by increasing disposable income, though they are not specifically targeted at housing.

Critically, the success of these programs hinges on accessibility and awareness. Many eligible households remain unenrolled due to complex application processes or lack of information. Streamlining applications, increasing outreach, and leveraging technology can improve participation rates. For example, online portals and multilingual resources can make it easier for diverse populations to access assistance. Furthermore, collaboration between federal, state, and local agencies can ensure that programs are tailored to regional housing markets and demographic needs.

In conclusion, government assistance programs play a vital role in reducing the rent burden on low-income households, offering a mix of subsidies, policies, and incentives. While no single solution is universally effective, a combination of direct aid, regulatory measures, and innovative partnerships can create a more equitable housing landscape. By addressing both immediate and systemic challenges, these initiatives not only provide relief but also pave the way for long-term financial stability and housing security.

Rent Party in 'Blacker the Berry': Unpacking Cultural Significance

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This helps ensure you have enough left for other expenses and savings.

While the 30% rule is a guideline, it may be necessary to exceed it in high-cost areas. However, aim to keep housing costs as close to 30% as possible to avoid financial strain.

Calculate your rent-to-income ratio by dividing your monthly rent by your gross monthly income. If the result is significantly above 30%, you may be spending too much and should consider adjusting your budget or housing situation.