Determining how many times rent should be relative to one's salary is a crucial financial consideration for individuals and families alike. A widely accepted guideline suggests that rent should not exceed 30% of a person's gross monthly income, ensuring that individuals can comfortably manage other essential expenses such as utilities, groceries, and savings. This rule of thumb, often referred to as the 30% rule, helps prevent financial strain and promotes a balanced budget. However, the ideal ratio may vary depending on factors like location, cost of living, and personal financial goals, making it essential for individuals to assess their unique circumstances when deciding on an appropriate rent-to-salary ratio.

| Characteristics | Values |

|---|---|

| General Rule of Thumb | Salary should be 3 times the monthly rent (widely accepted standard) |

| Source | Financial advisors, real estate experts, and government guidelines |

| Purpose | Ensures affordability and prevents financial strain |

| Applicability | Most commonly used in the U.S. and other Western countries |

| Variations by Location | Higher multiples (e.g., 4x) in expensive cities like New York or San Francisco |

| Income Calculation | Gross monthly income (before taxes and deductions) |

| Rent Calculation | Total monthly rent (including utilities if applicable) |

| Alternative Metrics | 30% of income rule (rent should not exceed 30% of monthly income) |

| Exceptions | May vary based on lifestyle, debt, or other financial obligations |

| Latest Data (as of 2023) | 3x rule remains the most cited standard in financial planning |

| Impact on Credit | Landlords often verify income to ensure compliance with this rule |

| Flexibility | Some landlords may accept lower multiples with additional guarantees |

Explore related products

What You'll Learn

![]()

Affordable Rent Ratio Guidelines

A common rule of thumb suggests that rent should not exceed 30% of your monthly income. This guideline, often referred to as the 30% rule, has been widely adopted as a benchmark for affordable housing. However, this one-size-fits-all approach may not be suitable for everyone, as individual circumstances can significantly impact what constitutes an affordable rent ratio. For instance, a young professional in a high-cost city might struggle to find housing within this limit, while a remote worker in a rural area could comfortably allocate less than 20% of their income to rent.

To refine this guideline, consider a tiered approach based on income levels and living situations. For low-income earners (below $30,000 annually), aiming for a rent-to-income ratio of 25% or less is more realistic. This ensures that essential expenses like food, transportation, and healthcare remain manageable. Middle-income earners ($30,000–$70,000) can target the traditional 30% mark, while high-income individuals (above $70,000) might allocate up to 35% if they prioritize location or amenities. For example, a single person earning $45,000 annually should ideally spend no more than $1,125 monthly on rent, whereas a couple earning $120,000 combined could consider up to $3,500 for a premium location.

Another critical factor is regional cost of living. In high-cost cities like New York or San Francisco, even the 30% rule may be unattainable for many. Here, adjusting expectations or exploring shared housing can help. Conversely, in low-cost areas, aiming for a lower ratio (e.g., 20–25%) frees up income for savings or investments. For instance, a tenant in Des Moines, Iowa, earning $50,000 might aim for $830 monthly rent, while someone in Los Angeles with the same income may need to cap at $1,250 to stay within budget.

Practical tips for adhering to these guidelines include negotiating rent, seeking rent-controlled units, or considering roommates. Additionally, tracking expenses using budgeting apps can help ensure rent doesn’t overshadow other financial goals. For those struggling to meet these ratios, reevaluating job opportunities or relocating to a more affordable area may be necessary. Ultimately, the affordable rent ratio is not just a number but a tool to balance housing costs with overall financial health.

Renting a Basement Suite Without a Kitchen: Tips and Strategies

You may want to see also

Explore related products

$44.99 $44.99

![]()

Income-to-Rent Calculation Methods

Determining how much of your salary should go toward rent is a critical financial decision, and various methods can help you find a sustainable balance. One widely accepted rule of thumb is the 30% rule, which suggests that no more than 30% of your gross monthly income should be allocated to rent. For example, if your monthly income is $5,000, your rent should ideally not exceed $1,500. This method is straightforward and provides a quick benchmark for affordability, but it may not account for individual financial obligations like debt or savings goals.

Another approach is the 50/30/20 budget rule, which categorizes income into needs, wants, and savings. Here, 50% of your income covers necessities like rent, utilities, and groceries, while 30% goes to discretionary spending, and 20% is saved or used to pay off debt. Applying this to rent, if your income is $4,000, up to $2,000 (50%) could be allocated to essentials, but rent alone should ideally stay closer to the 30% mark to leave room for other necessities. This method offers a more holistic view of your finances but requires disciplined budgeting.

For those with fluctuating incomes, such as freelancers or commission-based workers, a dynamic calculation method may be more appropriate. Start by averaging your monthly income over the past year to create a stable baseline. Then, apply the 30% rule to this average. For instance, if your average monthly income is $3,500, aim for rent around $1,050. Additionally, maintain an emergency fund equivalent to 3–6 months of living expenses to buffer against income variability.

Lastly, consider the rent-to-income ratio, a metric used by landlords to assess affordability. Many landlords require that your annual income be at least 40–50 times your monthly rent. For example, if rent is $1,200, your annual income should be at least $48,000–$60,000. While this method is landlord-focused, it’s a useful reverse calculation for tenants to ensure they meet rental qualifications. However, it doesn’t account for personal financial health, so pair it with other methods for a comprehensive assessment.

In practice, the best method depends on your financial situation and goals. Combine these approaches by starting with the 30% rule, then adjust based on your budget using the 50/30/20 framework. If you’re in a high-cost-of-living area, prioritize the rent-to-income ratio to avoid rejection from landlords. Always factor in additional expenses like utilities, transportation, and savings to ensure rent doesn’t strain your overall financial stability.

Choosing the Right Wood Chipper Rental Size for Your Project

You may want to see also

Explore related products

![]()

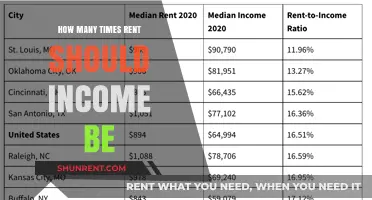

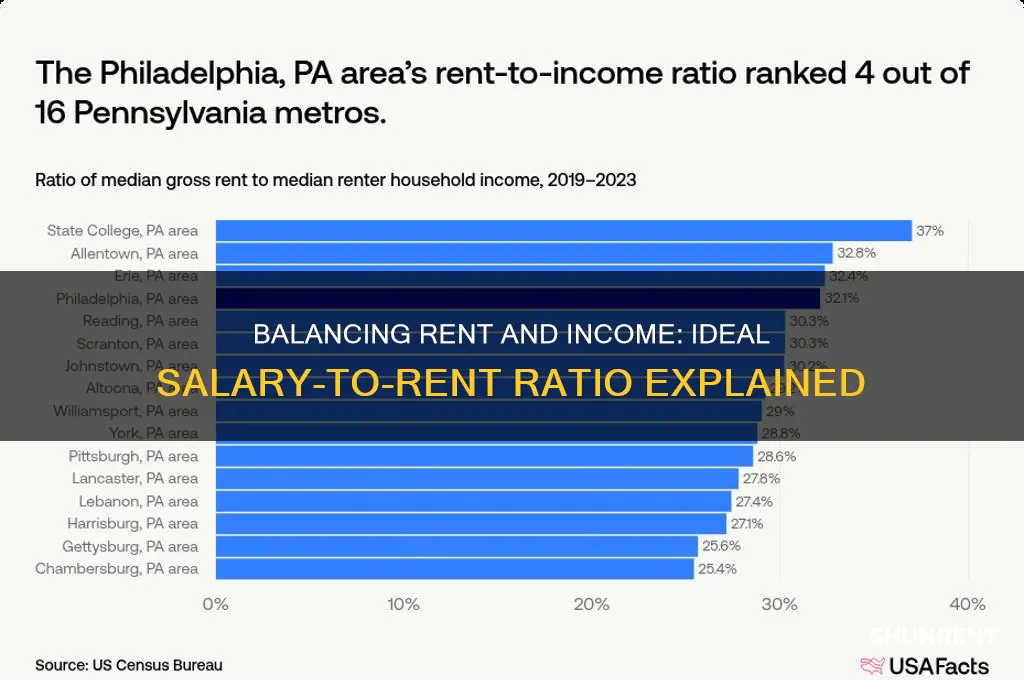

Regional Rent-to-Salary Variations

The rent-to-salary ratio varies dramatically across regions, influenced by local economies, housing markets, and cost of living. In high-cost urban centers like New York City or San Francisco, renters often allocate 40–50% of their income to housing, far exceeding the commonly recommended 30% threshold. Conversely, in more affordable areas like the Midwest or Southeast, this ratio drops to 20–25%, allowing residents to save more or allocate funds to other expenses. This disparity highlights the need for region-specific financial planning when considering housing costs.

Analyzing these variations reveals a clear pattern: income growth rarely keeps pace with rent increases in high-demand areas. For instance, in Los Angeles, the median rent is approximately $2,500 per month, while the median household income hovers around $65,000 annually. This translates to a rent-to-salary ratio of nearly 46%, straining budgets and limiting financial flexibility. In contrast, cities like Indianapolis, with a median rent of $1,100 and a median income of $50,000, maintain a more manageable 26% ratio. Such differences underscore the importance of aligning career choices and housing decisions with regional economic realities.

For those relocating or negotiating salaries, understanding these regional disparities is crucial. A practical tip is to research the local rent-to-salary ratio before accepting a job offer. Websites like Numbeo or Zillow provide city-specific data, enabling informed decisions. For example, if moving to Seattle, where the ratio averages 35%, negotiate a higher salary or remote work flexibility to offset housing costs. Conversely, in Austin, Texas, where the ratio is closer to 28%, prioritize savings or investments with the extra disposable income.

A comparative analysis of international cities further illustrates this point. In Tokyo, despite high living costs, efficient public transportation and smaller living spaces keep the rent-to-salary ratio around 30%. Meanwhile, in Dublin, Ireland, rapid rent increases have pushed the ratio to 40%, outpacing wage growth. These examples demonstrate how cultural norms, urban planning, and policy decisions shape housing affordability, offering lessons for both individuals and policymakers.

In conclusion, regional rent-to-salary variations demand tailored financial strategies. Whether adjusting budgets, negotiating salaries, or choosing locations, awareness of these disparities empowers individuals to make smarter housing decisions. By focusing on local data and trends, renters can navigate the complex interplay between income and housing costs, ensuring long-term financial stability.

Bobcat Rental Costs at United Rentals: What You Need to Know

You may want to see also

![]()

Budgeting for Rent and Expenses

A common rule of thumb suggests that rent should not exceed 30% of your monthly income. This guideline, often referred to as the 30% rule, has been a longstanding benchmark for financial advisors and renters alike. However, this one-size-fits-all approach may not account for the diverse financial landscapes individuals navigate. For instance, a recent graduate with student loans might find this ratio challenging, while a high-income earner could comfortably allocate more without strain. The key is to tailor this principle to your unique financial situation, considering not just rent but all living expenses.

Analyzing the 30% Rule: A Practical Example

Imagine a young professional earning $4,000 per month. Adhering to the 30% rule, their rent should ideally be $1,200 or less. However, in cities with high living costs, this might only secure a modest studio apartment. Here, the rule’s practicality is tested. Should they compromise on location or size, or is it wiser to allocate a slightly higher percentage, say 35%, to secure a more suitable home? This decision requires a deeper dive into their overall budget, including utilities, groceries, transportation, and savings.

Budgeting Beyond Rent: A Holistic Approach

Effective budgeting for rent and expenses demands a comprehensive view of your financial obligations. Start by listing all monthly expenses, categorizing them into essentials (rent, utilities, groceries) and discretionary spending (entertainment, dining out). Allocate funds accordingly, ensuring that essentials are covered first. For instance, if your rent is $1,500 and your income is $5,000, you’re at 30%. But if utilities, internet, and groceries add another $800, you’re left with $2,700 for other expenses and savings. Prioritize building an emergency fund, typically 3-6 months’ worth of living expenses, to safeguard against unforeseen circumstances.

Adapting to Financial Realities: Flexibility is Key

Life’s unpredictability often requires flexibility in budgeting. For instance, a sudden job loss or medical emergency can disrupt even the most meticulously planned budget. In such cases, consider temporary adjustments, like downsizing or finding a roommate, to reduce rent burden. Conversely, if you receive a raise or bonus, resist the urge to immediately increase rent spending. Instead, allocate the extra income to savings, investments, or paying off debt. This adaptive approach ensures financial stability, even when circumstances change.

Practical Tips for Rent and Expense Management

- Track Spending: Use budgeting apps or spreadsheets to monitor monthly expenses, identifying areas for cuts if rent consumes too much of your income.

- Negotiate Rent: Don’t hesitate to negotiate with landlords, especially if you’re a long-term tenant or the market is slow.

- Consider Roommates: Sharing living space can significantly reduce rent and utility costs, freeing up funds for other priorities.

- Save on Utilities: Opt for energy-efficient appliances, unplug devices when not in use, and use public transportation to lower utility and transportation expenses.

By adopting a nuanced approach to budgeting for rent and expenses, you can achieve financial balance, ensuring that your housing costs support, rather than hinder, your overall financial health.

Understanding the Minimum Age Requirement to Rent a B&B

You may want to see also

![]()

Impact of Debt on Rent Affordability

Debt reshapes the calculus of rent affordability, turning a straightforward ratio—like the oft-cited "30% rule"—into a complex equation. For instance, a tenant earning $4,000 monthly might comfortably afford $1,200 rent under normal circumstances. However, with $500 in monthly student loan payments and $300 in credit card debt, their effective disposable income shrinks to $2,200. Suddenly, that same $1,200 rent consumes 55% of their remaining funds, pushing them into financially precarious territory. This illustrates how debt distorts the perceived affordability of rent, even when income aligns with traditional guidelines.

Consider the compounding effect of high-interest debt. A tenant with $10,000 in credit card debt at 20% APR faces not only the principal but also escalating interest charges. If they allocate $300 monthly toward this debt, only $60 goes toward reducing the balance, while $240 covers interest. This cycle reduces their ability to save for emergencies or absorb rent increases. In contrast, tenants without such debt can allocate those funds toward higher rent or savings, creating a stark disparity in financial resilience.

To mitigate debt’s impact on rent affordability, prioritize debt repayment strategies. The *debt snowball method*—paying off the smallest debts first—provides psychological wins that sustain motivation. Alternatively, the *debt avalanche method* targets high-interest debts first, minimizing long-term costs. For example, a tenant with both a $5,000 credit card balance (20% APR) and a $10,000 student loan (5% APR) should focus on the credit card debt first. By eliminating high-interest obligations, they free up more income to allocate toward rent or savings.

Another practical step is negotiating rent terms or seeking debt consolidation. Tenants with stable income but temporary cash flow issues might propose a rent-smoothing agreement, where payments are split unevenly across months. Simultaneously, consolidating debt into a lower-interest loan reduces monthly obligations, freeing up funds for rent. For instance, refinancing $20,000 in debt from 18% to 8% APR could lower monthly payments by $200—a sum that could make the difference between affordable and unaffordable rent.

Ultimately, the interplay between debt and rent affordability demands proactive management. Ignoring debt while adhering to rent-to-income ratios is a recipe for financial strain. By addressing debt head-on—through strategic repayment, negotiation, or consolidation—tenants can restore balance to their budgets. The goal isn’t just to meet rent obligations but to build a financial foundation resilient enough to withstand unexpected challenges.

Proving Intent for Rent-to-Flip: Legal Strategies and Documentation Tips

You may want to see also

Frequently asked questions

A common rule of thumb is that rent should not exceed 30% of your gross monthly income. This ensures you have enough left for other expenses and savings.

Rent being 50% of your salary is generally considered too high, as it leaves limited funds for essentials like utilities, groceries, and savings. Aim to keep it closer to 30% if possible.

If your rent exceeds 30% of your salary, consider finding a more affordable place, increasing your income, or reducing other expenses to balance your budget.

The 30% rule is a guideline, not a one-size-fits-all solution. Factors like location, income, and personal financial goals may require adjustments to this rule.