Determining how many times your rent should be in relation to your income is a crucial aspect of financial planning and budgeting. A widely accepted rule of thumb is the 30% rule, which suggests that you should aim to spend no more than 30% of your gross monthly income on rent and related housing expenses. This guideline helps ensure that you have enough funds left for other essential expenses, savings, and discretionary spending. However, the ideal ratio can vary depending on individual circumstances, such as location, lifestyle, and financial goals. For instance, in high-cost urban areas, renters might need to allocate a larger portion of their income to housing, while those in more affordable regions may be able to adhere strictly to the 30% rule. Understanding this balance is key to maintaining financial stability and avoiding the pitfalls of overspending on housing.

Explore related products

What You'll Learn

- Income-to-Rent Ratio Guidelines: Standard ratios to ensure affordability and financial stability for renters

- Local Cost of Living: Adjusting rent expectations based on regional economic differences and living expenses

- Emergency Fund Considerations: Balancing rent with savings to handle unexpected financial challenges

- Debt-to-Income Ratio: Managing debts while ensuring rent remains a sustainable portion of income

- Lifestyle and Priorities: Aligning rent costs with personal goals, savings, and desired quality of life

![]()

Income-to-Rent Ratio Guidelines: Standard ratios to ensure affordability and financial stability for renters

A common rule of thumb suggests that renters should aim to spend no more than 30% of their gross monthly income on rent. This guideline, often referred to as the 30% rule, has been widely adopted as a benchmark for affordability. For instance, if your monthly income is $5,000, your rent should ideally not exceed $1,500. This ratio ensures that you have sufficient funds left for other essential expenses, savings, and discretionary spending, promoting financial stability.

However, the 30% rule is not a one-size-fits-all solution. Regional variations in cost of living, personal financial goals, and individual circumstances can necessitate adjustments. In high-cost urban areas like New York or San Francisco, where rent prices are significantly higher, adhering strictly to the 30% rule may be impractical. In such cases, renters might need to allocate up to 40-50% of their income to housing, but this should be accompanied by a detailed budget to ensure other financial obligations are met. Conversely, in more affordable regions, aiming for a lower ratio, such as 25%, can accelerate savings and debt repayment.

To determine your ideal income-to-rent ratio, start by calculating your total monthly income and fixed expenses. Subtract essentials like utilities, groceries, transportation, and insurance from your income. The remaining amount should cover rent while leaving room for savings and leisure. For example, if your monthly income is $4,000 and your fixed expenses total $1,500, allocating $1,200 to rent (30%) leaves $1,300 for savings and discretionary spending. This method ensures a balanced approach to budgeting.

Critics argue that the 30% rule may not account for modern financial realities, such as student loan debt or fluctuating gig economy incomes. For younger renters or those with substantial debt, a more conservative ratio, like 25%, might be advisable. Additionally, building an emergency fund equivalent to 3-6 months of living expenses can provide a safety net, allowing for flexibility in rent allocation. Tools like budgeting apps or spreadsheets can help track spending and adjust ratios as needed.

Ultimately, the income-to-rent ratio is a starting point, not a rigid rule. It should be tailored to individual financial goals and circumstances. Regularly reviewing your budget and adjusting your ratio based on changes in income, expenses, or life goals ensures long-term affordability and stability. By striking the right balance, renters can enjoy their homes without compromising their financial health.

Calculating Rent: Triple the Fun

You may want to see also

Explore related products

![]()

Local Cost of Living: Adjusting rent expectations based on regional economic differences and living expenses

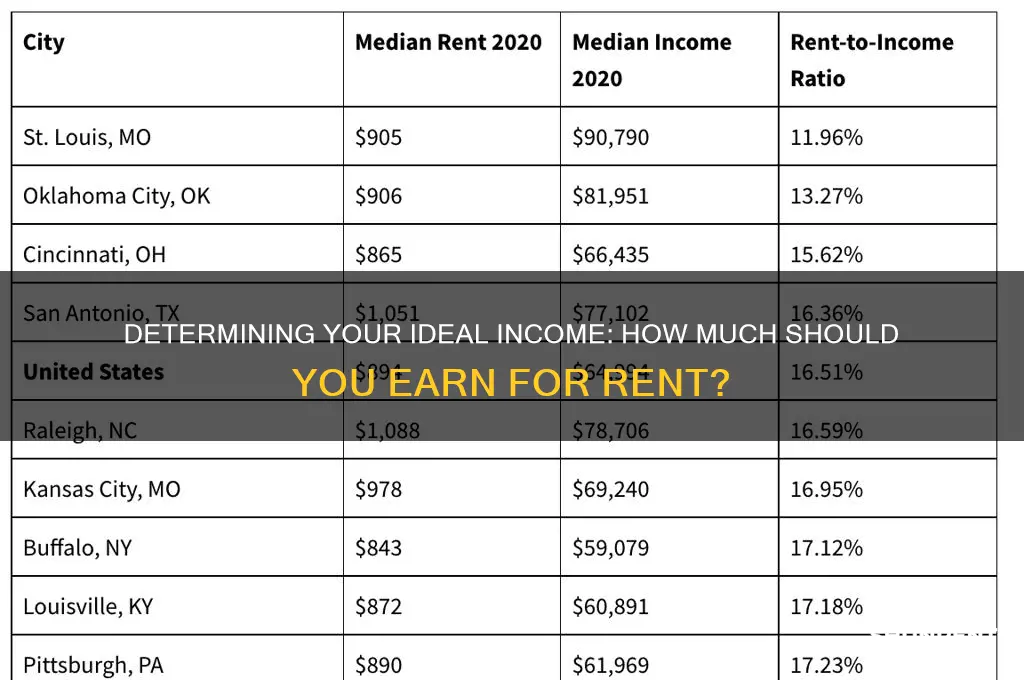

The rule of thumb that rent should not exceed 30% of your income is a widely accepted guideline, but it’s a blunt instrument in a world of sharp economic disparities. In San Francisco, where the median rent hovers around $3,700, a tenant would need to earn roughly $148,000 annually to meet this threshold. Contrast that with Tulsa, Oklahoma, where median rent is $850, requiring an income of just $34,000. These numbers underscore the absurdity of applying a one-size-fits-all approach to rent affordability. Regional economic differences demand a more nuanced calculation, one that accounts for local wages, taxes, and the cost of essentials like groceries and transportation.

To adjust rent expectations effectively, start by benchmarking the local cost of living against your income. Tools like the MIT Living Wage Calculator or the Bureau of Labor Statistics’ regional price parities can provide data-driven insights. For instance, if you’re moving from a low-cost area to a high-cost city, factor in not just rent but also the increased price of groceries (up to 20% higher in some metros) and utilities (which can double in colder climates). A practical tip: calculate your post-tax income for the region, then subtract fixed expenses like healthcare and transportation. The remaining amount should be your rent budget, ensuring it aligns with local economic realities rather than national averages.

Persuasively, it’s worth arguing that rent-to-income ratios should be inverted in high-cost areas. Instead of asking how many times your rent should be your income, consider how much of your income remains after rent. In expensive cities, a 40% or even 50% rent-to-income ratio might be unavoidable, but the focus should shift to maximizing disposable income for savings and quality of life. For example, in New York City, where the average rent is $4,000, a tenant earning $80,000 (allocating 60% to rent) would have $2,666 left monthly after taxes—a tight but manageable budget if other expenses are minimized. This approach prioritizes sustainability over adherence to outdated rules.

Comparatively, rural or low-cost regions offer flexibility to redefine affordability. In places like Iowa or Mississippi, where median rents are under $1,000, tenants can afford to allocate a smaller percentage of their income to housing, freeing up funds for investments, travel, or debt repayment. However, this luxury comes with its own caution: lower rents often correlate with lower wages, so ensure your income aligns with local job markets. For instance, a remote worker earning a San Francisco salary in a rural area could allocate just 15% of their income to rent, but a local resident earning the median wage might still struggle with a 30% threshold due to wage disparities.

In conclusion, adjusting rent expectations based on local cost of living requires a three-step process: research regional economic indicators, calculate post-tax income and essential expenses, and prioritize disposable income over rigid ratios. Whether you’re in a high-cost urban center or a low-cost rural area, the goal is not to meet a national standard but to achieve financial stability within your specific context. By tailoring your rent budget to local realities, you can avoid the pitfalls of overpaying or underestimating expenses, ensuring a sustainable living situation regardless of where you call home.

Kansas City Rent Trends: Average Costs and What to Expect

You may want to see also

Explore related products

![]()

Emergency Fund Considerations: Balancing rent with savings to handle unexpected financial challenges

A common rule of thumb suggests that your monthly income should be at least three times your rent to maintain financial stability. However, this guideline often overlooks the critical need for an emergency fund. Unexpected expenses—car repairs, medical bills, or job loss—can derail even the most meticulously planned budget. Without savings, you might find yourself choosing between paying rent and covering these unforeseen costs, a decision no one should face.

Consider this scenario: You earn $4,500 monthly and pay $1,500 in rent, meeting the three-times rule. Yet, if your car breaks down and requires a $2,000 repair, you’re suddenly short on funds. An emergency fund acts as a buffer, ensuring rent and essentials remain covered while you address the crisis. Financial experts recommend saving three to six months’ worth of living expenses, but this can feel daunting when rent consumes a significant portion of your income. Start small—aim to save at least one month’s rent initially, then gradually build from there.

Balancing rent with savings requires strategic prioritization. Allocate a fixed percentage of your income—say, 10%—to savings before addressing other expenses. If your rent is high relative to your earnings, consider downsizing or finding a roommate to free up funds for your emergency reserve. Automate your savings by setting up direct deposits into a separate account, making it easier to resist the temptation to spend. Remember, the goal isn’t to save aggressively at the expense of your well-being but to create a sustainable plan that accommodates both rent and unexpected challenges.

Finally, view your emergency fund as a non-negotiable expense, akin to rent or utilities. It’s not a luxury but a necessity for financial resilience. By integrating savings into your budget and adjusting your lifestyle if needed, you can strike a balance that ensures you’re prepared for life’s uncertainties without sacrificing your housing stability. Start today—even small contributions add up over time, providing peace of mind and a safety net when you need it most.

Top Dish Rental Options for Your Westminster, MD Wedding

You may want to see also

Explore related products

$44249 $45650

![]()

Debt-to-Income Ratio: Managing debts while ensuring rent remains a sustainable portion of income

A common rule of thumb suggests that rent should not exceed 30% of your monthly income, but this guideline often overlooks the broader financial landscape, particularly existing debts. Your debt-to-income (DTI) ratio, a critical metric lenders use, measures your monthly debt payments against your gross monthly income. For financial stability, aim to keep your DTI ratio below 36%, with housing expenses (rent included) ideally accounting for no more than 28% of that total. Exceeding these thresholds can strain your budget, leaving little room for savings, emergencies, or discretionary spending.

Consider this scenario: If your monthly income is $4,000, the 30% rule suggests a $1,200 rent limit. However, if your student loan and credit card payments total $800 monthly, your DTI ratio is already 20% before rent. Adding $1,200 in rent would push your DTI to 50%, well above the recommended 36%. In this case, capping rent at $720 (18% of income) keeps your DTI at 38%, closer to the target while ensuring debts don’t overwhelm your budget. Tools like budgeting apps or spreadsheets can help track these ratios and adjust rent expectations accordingly.

Managing debts while keeping rent sustainable requires strategic prioritization. Start by listing all monthly obligations—rent, loans, credit cards, and utilities—and compare them to your income. If your DTI exceeds 43%, lenders may view you as a high-risk borrower, complicating future financial goals like buying a home. To lower your DTI, consider refinancing high-interest debts, increasing income through side gigs, or negotiating lower rent by offering longer lease terms or prepayment. For instance, paying six months’ rent upfront might secure a 5% discount, reducing monthly outflow.

A comparative analysis reveals that renters with lower DTI ratios often have more financial flexibility. For example, a renter with a 25% DTI can allocate more to savings or investments, while someone at 50% may struggle to cover unexpected expenses. Age and life stage also play a role: younger renters with student loans might need to prioritize debt repayment over higher rent, while older renters with fewer debts could afford a larger portion of income for housing. Tailoring rent to your DTI ensures a balanced approach to financial health.

In conclusion, while the 30% rent rule is a starting point, it’s the interplay with your DTI ratio that truly determines affordability. By keeping housing costs within 28% of your DTI and the overall ratio below 36%, you create a buffer for debts and other expenses. Regularly review your financial obligations, adjust rent expectations as needed, and leverage strategies like refinancing or negotiation to maintain a sustainable balance. This approach not only ensures rent remains manageable but also fosters long-term financial stability.

Will Washington State Rent Prices Ever Decline? A Housing Market Analysis

You may want to see also

Explore related products

![]()

Lifestyle and Priorities: Aligning rent costs with personal goals, savings, and desired quality of life

Determining how much rent you should pay isn’t just about following a one-size-fits-all rule. It’s about aligning your housing costs with your lifestyle, priorities, and long-term goals. For instance, the commonly cited "30% rule" (spending no more than 30% of your income on rent) may work for some, but it ignores individual differences in financial aspirations, geographic location, and personal values. If you’re saving aggressively for early retirement, prioritizing travel, or building an emergency fund, your rent-to-income ratio might need to be significantly lower—perhaps 20% or even 15%. Conversely, if living in a vibrant urban area with access to cultural amenities is non-negotiable, you might allocate closer to 40%, but only if it doesn’t derail other financial goals.

Consider this scenario: A 28-year-old professional earning $70,000 annually wants to save $20,000 per year for a down payment on a house within five years. Following the 30% rule would allow for $1,750 in monthly rent. However, to meet her savings goal, she’d need to reduce her rent to $1,200, freeing up an additional $6,000 annually. This trade-off might mean living in a smaller space or a less trendy neighborhood, but it aligns with her priority of homeownership. The key is to reverse-engineer your rent budget from your goals, not the other way around.

For those in their 20s and 30s, rent decisions often involve balancing short-term enjoyment with long-term financial security. If your priority is building wealth, aim to keep rent below 25% of your income. For example, on a $50,000 salary, that’s $1,040 per month. This leaves room for maxing out retirement accounts, investing in stocks, or paying off student loans. Conversely, if your priority is experiencing city life to the fullest, you might allocate more to rent but ensure it doesn’t exceed 35%. At $50,000, that’s $1,458 monthly—a figure that still allows for modest savings and discretionary spending.

Geography plays a critical role in this calculus. In high-cost cities like San Francisco or New York, even 40% of income may not secure a spacious or centrally located apartment. Here, lifestyle priorities become even more crucial. If you’re willing to commute or share a space, you can significantly reduce costs. For instance, splitting a $2,500 two-bedroom apartment with a roommate in Brooklyn lowers your share to $1,250—well within the 30% threshold for a $50,000 income. Alternatively, moving to a more affordable neighborhood or city entirely could free up funds for other priorities, like starting a business or pursuing a passion project.

Ultimately, the question of "how many times rent should you make" is deeply personal. It requires a candid assessment of your values, a clear understanding of your financial goals, and a willingness to make trade-offs. Start by listing your top three priorities (e.g., travel, savings, career growth) and calculate how much rent aligns with those objectives. Use budgeting tools to model different scenarios, and don’t be afraid to adjust your lifestyle temporarily to achieve long-term gains. Remember, rent isn’t just an expense—it’s a strategic decision that shapes your quality of life and financial future.

Discover NYC Business Rent Prices: A Comprehensive Guide for Entrepreneurs

You may want to see also

Frequently asked questions

A common rule of thumb is that your monthly income should be at least 3 times your monthly rent to afford a place comfortably.

Making 2 times your rent may be manageable, but it leaves less room for other expenses and savings. It’s generally recommended to aim for 3 times or more for financial stability.

Earning 4 or 5 times your rent is ideal, as it provides a comfortable buffer for savings, emergencies, and other expenses. It’s a healthy financial position.

The rule can vary by location, especially in high-cost areas like major cities, where incomes may need to be 4 or 5 times rent to afford housing. Always consider local living costs.

It’s best to base your calculation on consistent, reliable income. While bonuses or side income can help, they shouldn’t be the primary factor in determining affordability.