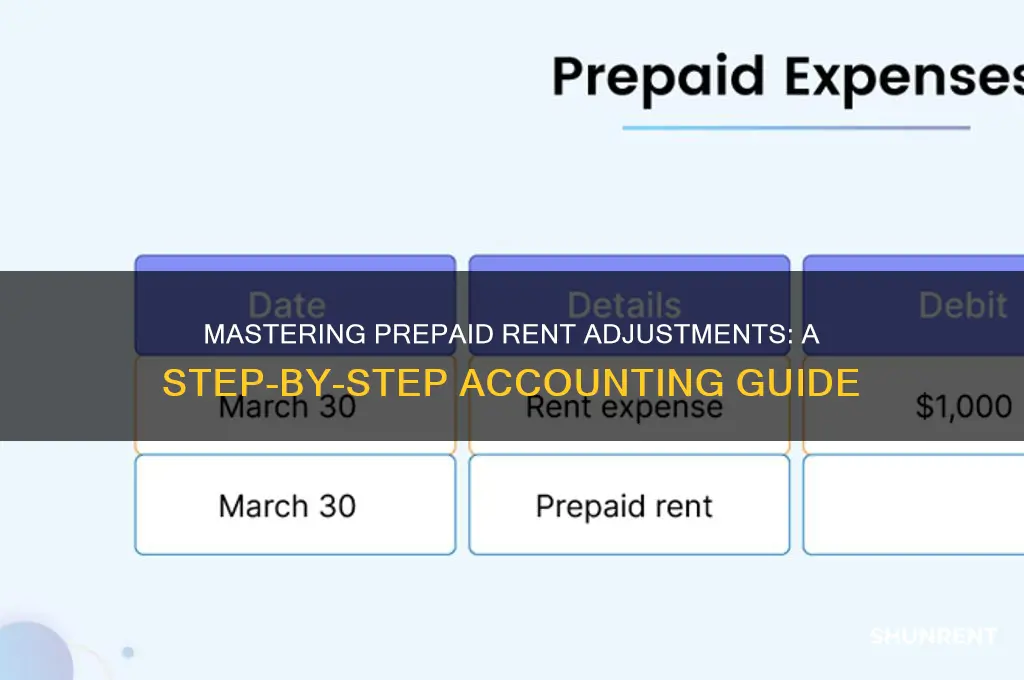

Adjusting the prepaid rent account is a crucial task in accounting to accurately reflect the portion of rent expense that applies to the current accounting period. Prepaid rent represents payments made in advance for future occupancy, and it is initially recorded as an asset. As time passes and the rental period is utilized, a portion of this prepaid amount must be recognized as an expense, reducing the asset balance. This adjustment is typically done through a journal entry, debiting rent expense and crediting prepaid rent, ensuring that financial statements present a true and fair view of the company’s financial position and performance. Proper management of this account is essential for compliance with accounting principles and for maintaining accurate financial records.

| Characteristics | Values |

|---|---|

| Definition | Prepaid rent is an asset account representing rent paid in advance for future periods. |

| Adjustment Method | Adjusted monthly by recognizing a portion of prepaid rent as rent expense. |

| Journal Entry | Debit: Rent Expense, Credit: Prepaid Rent (monthly adjustment). |

| Frequency | Adjusted monthly based on the rental period covered by the prepaid amount. |

| Accounting Principle | Follows the matching principle (expenses matched to the period incurred). |

| Financial Statement Impact | Reduces prepaid rent (asset) and increases rent expense on the income statement. |

| Documentation Required | Lease agreement, payment receipts, and amortization schedule. |

| Software Tools | Accounting software (e.g., QuickBooks, Xero) for automated adjustments. |

| Tax Treatment | Prepaid rent is deductible in the period it is expensed, not when paid. |

| Common Mistakes | Forgetting to adjust monthly, misclassifying as an expense upfront. |

| Example | $12,000 prepaid for 12 months: $1,000 expensed monthly, reducing prepaid rent by $1,000 each month. |

Explore related products

What You'll Learn

- Initial Prepaid Rent Entry: Record full payment in prepaid rent account, not rent expense, for accurate financial reporting

- Monthly Amortization Process: Allocate prepaid rent expense monthly based on lease term for consistent cost recognition

- Journal Entry Adjustments: Debit rent expense, credit prepaid rent monthly to reflect used portion

- Year-End Balance Review: Verify prepaid rent balance matches unexpired term to avoid misstatement in financials

- Short-Term vs. Long-Term: Classify prepaid rent as current or non-current asset based on remaining term

![]()

Initial Prepaid Rent Entry: Record full payment in prepaid rent account, not rent expense, for accurate financial reporting

Recording the initial prepaid rent entry correctly is crucial for maintaining accurate financial statements. When a business pays rent in advance, the full payment should be recorded in the prepaid rent account, not directly to rent expense. This is because the expense hasn’t yet been incurred; the payment represents a future benefit. For example, if a company pays $12,000 for six months of rent upfront, the journal entry would debit Prepaid Rent for $12,000 and credit Cash for $12,000. This ensures the balance sheet reflects the asset (prepaid rent) accurately, while the income statement remains unaffected until the rent period begins.

The distinction between prepaid rent and rent expense is fundamental to accrual accounting. Prepaid rent is a current asset, representing cash paid for future use, while rent expense is a cost recognized as the rented period elapses. Misclassifying prepaid rent as an immediate expense distorts both the income statement and balance sheet. For instance, if the $12,000 payment were recorded as rent expense, the company would overstate its expenses in the current period and understate its assets, misleading stakeholders about its financial health.

To avoid errors, follow a systematic approach. First, identify the payment as prepaid rent if it covers a future period. Second, use the appropriate journal entry: debit Prepaid Rent and credit Cash. Third, establish a schedule to amortize the prepaid rent over the rental period. For the $12,000 example, this would mean recognizing $2,000 as rent expense each month for six months. This method aligns expenses with the periods they benefit, adhering to the matching principle in accounting.

Practical tips can further streamline this process. Utilize accounting software to automate amortization schedules, reducing manual errors. For small businesses, a simple spreadsheet can track prepaid rent balances and monthly adjustments. Additionally, review prepaid rent accounts periodically to ensure accuracy and adjust for any changes in rental agreements. By treating prepaid rent as an asset initially, businesses ensure compliance with accounting standards and provide a clearer picture of their financial position.

In conclusion, recording the full payment in the prepaid rent account, rather than rent expense, is a cornerstone of accurate financial reporting. This practice not only adheres to accounting principles but also enhances transparency and reliability in financial statements. By understanding and implementing this process, businesses can avoid common pitfalls and maintain robust financial records.

Apply for Best Egg Flexible Rent: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Monthly Amortization Process: Allocate prepaid rent expense monthly based on lease term for consistent cost recognition

Prepaid rent often represents a significant cash outflow, yet its expense recognition must align with the period benefiting from its use. The monthly amortization process ensures this alignment by systematically allocating the prepaid amount over the lease term. This approach adheres to the matching principle in accounting, where expenses are recognized in the same period as the revenues they help generate. For instance, if a business prepays $12,000 for a year-long lease, allocating $1,000 monthly as rent expense ensures consistent cost recognition rather than distorting financials with a lump-sum entry.

To implement this process, start by determining the total prepaid rent amount and the lease term in months. Divide the prepaid amount by the lease term to calculate the monthly amortization. For example, a $6,000 prepayment for a six-month lease would result in a $1,000 monthly expense. Record this entry by debiting "Rent Expense" and crediting "Prepaid Rent" for the calculated amount each month. This method simplifies tracking and ensures accuracy, particularly in businesses with multiple leases or varying prepayment terms.

While straightforward, this process requires vigilance to avoid errors. Common pitfalls include miscalculating the lease term or forgetting to adjust for partial months. For example, a lease starting mid-month should prorate the first month’s expense. Additionally, ensure the prepaid rent account is reconciled regularly to reflect the remaining balance accurately. Software tools or spreadsheets can automate calculations, reducing the risk of manual errors and saving time for accounting teams.

The benefits of monthly amortization extend beyond compliance. It provides a clearer financial picture by smoothing out expenses, which is particularly valuable for budgeting and forecasting. Stakeholders gain insight into consistent monthly costs rather than erratic fluctuations caused by lump-sum entries. Moreover, this method aligns with tax reporting requirements, ensuring expenses are claimed in the appropriate periods. By mastering this process, businesses maintain accurate records and support informed decision-making.

Renting a Carpet Cleaner from Publix: A Simple Step-by-Step Guide

You may want to see also

Explore related products

![]()

Journal Entry Adjustments: Debit rent expense, credit prepaid rent monthly to reflect used portion

Prepaid rent represents an asset on the balance sheet, reflecting payments made in advance for future occupancy. As time passes and the rented space is utilized, this asset diminishes. To accurately portray the financial reality, accountants must systematically recognize the expense associated with the consumed portion of the prepaid rent. This is achieved through a straightforward yet crucial journal entry adjustment: debiting rent expense and crediting prepaid rent.

This adjustment serves a dual purpose. Firstly, it shifts the prepaid rent from the asset side of the balance sheet to the expense side of the income statement, reflecting the actual cost incurred during the accounting period. Secondly, it ensures that the remaining prepaid rent balance accurately represents the unexpired portion of the rental agreement. For instance, if a company pays $12,000 annually for rent in advance and needs to recognize monthly expenses, a monthly adjustment of $1,000 (debit rent expense, credit prepaid rent) would be made.

The frequency of this adjustment is paramount. Monthly adjustments are standard, aligning with the typical rental payment cycle and providing a granular view of expense recognition. However, depending on the accounting period and reporting requirements, adjustments could be made quarterly or annually. Consistency is key; once a frequency is established, adhering to it ensures comparability across periods and compliance with accounting standards.

While the concept is straightforward, execution requires attention to detail. Errors in calculation or timing can distort financial statements. For example, overstating rent expense inflates costs, while understating it misrepresents the true financial position. Utilizing accounting software with automated recurring journal entries can mitigate these risks, ensuring accuracy and efficiency. Additionally, regular reviews of the prepaid rent account and supporting documentation are essential to verify the correctness of adjustments.

In conclusion, the monthly journal entry adjustment of debiting rent expense and crediting prepaid rent is a fundamental practice in accounting. It transforms a prepaid asset into a recognized expense, providing a true and fair view of a company’s financial health. By understanding its mechanics, maintaining consistency, and leveraging tools for accuracy, businesses can ensure their financial statements reflect the economic reality of their operations.

Is Renting a Storage Unit a Waste of Money?

You may want to see also

Explore related products

$6.95

![]()

Year-End Balance Review: Verify prepaid rent balance matches unexpired term to avoid misstatement in financials

At year-end, reconciling prepaid rent accounts is critical to ensure financial accuracy. Start by identifying the total prepaid rent balance on the balance sheet. Next, cross-reference this with the lease agreement to determine the unexpired term—the period for which rent has been paid but not yet utilized. For example, if a company pays $12,000 annually in January and it’s now December, $1,000 should remain as prepaid rent for the unexpired month. Discrepancies here can lead to overstatement or understatement of expenses, distorting financial health.

Analyzing the prepaid rent account requires a meticulous approach. Begin by calculating the monthly rent expense based on the lease terms. Multiply this by the number of months remaining in the prepaid period to verify the correct balance. For instance, a $24,000 biennial payment with 6 months remaining should show $12,000 as prepaid rent. If the recorded balance deviates, investigate potential errors such as incorrect payment dates, miscalculated terms, or omitted adjustments. This step ensures compliance with accrual accounting principles, where expenses are matched to the period they benefit.

A persuasive argument for this review lies in its impact on financial statements. Misstated prepaid rent can inflate assets or underreport expenses, misleading stakeholders. For example, a $5,000 overstatement in prepaid rent artificially boosts the balance sheet while deferring expense recognition, skewing profitability metrics. Conversely, an understatement may signal liquidity issues or poor financial management. By aligning the prepaid rent balance with the unexpired term, companies maintain transparency and credibility, fostering trust among investors and auditors.

Practical tips streamline this process. Maintain a lease schedule detailing payment dates, amounts, and terms for quick reference. Use accounting software with automated reminders to adjust prepaid rent monthly. For complex leases, consider a spreadsheet tracker to reconcile payments against the unexpired term. Additionally, involve the real estate or legal team to confirm lease terms annually, especially if modifications occur. These practices not only prevent misstatements but also save time during year-end audits.

In conclusion, verifying that the prepaid rent balance matches the unexpired term is a non-negotiable step in year-end reviews. It safeguards financial integrity, ensures compliance, and provides a clear snapshot of a company’s obligations. By adopting structured analysis, leveraging technology, and fostering cross-departmental collaboration, businesses can avoid costly errors and maintain accurate financials. This diligence ultimately supports informed decision-making and sustains stakeholder confidence.

Discover the Most Affordable State for Renters in the U.S

You may want to see also

Explore related products

![Quick-Book Desktop Pro 2024 | LIFETIME Version | USB | Only for PC [software_key_card]](https://m.media-amazon.com/images/I/61UVBdvXIeL._AC_UL320_.jpg)

![]()

Short-Term vs. Long-Term: Classify prepaid rent as current or non-current asset based on remaining term

Prepaid rent presents an accounting conundrum: how to classify a future benefit that straddles the line between immediate and long-term value. The key differentiator lies in the remaining term of the prepaid period. Generally Accepted Accounting Principles (GAAP) dictate a clear distinction: assets expected to be consumed within one year or the operating cycle, whichever is longer, are classified as current assets. This means prepaid rent with a remaining term of less than a year falls squarely into the current asset category on the balance sheet.

For instance, imagine a company pays $12,000 in January for a year's rent. Initially, the entire $12,000 is recorded as a prepaid rent asset. However, as each month passes, $1,000 is expensed as rent, reducing the prepaid rent balance. By December, the remaining $1,000 would be classified as a current asset, reflecting its consumption within the next year.

The classification becomes more nuanced when the prepaid rent extends beyond a year. Consider a company prepaying $24,000 for a two-year lease. Initially, the entire amount is recorded as a prepaid asset. However, at the end of the first year, $12,000 would be reclassified from a non-current asset to a current asset, as it will be consumed within the next twelve months. This ensures the balance sheet accurately reflects the liquidity and near-term obligations of the company.

The distinction between current and non-current assets is crucial for financial analysis. Current assets are seen as more liquid, readily convertible to cash within a year, while non-current assets represent long-term investments. Proper classification of prepaid rent provides a clearer picture of a company's financial health and its ability to meet short-term obligations.

To ensure accurate classification, companies should carefully review lease agreements and track prepaid rent balances regularly. Adjusting entries should be made at the end of each accounting period to reflect the portion of prepaid rent that will be consumed within the next year. This meticulous approach ensures compliance with accounting standards and provides a transparent view of a company's financial position.

Yuma AZ Read Rent Hours: When Does It Open?

You may want to see also

Frequently asked questions

A pre-paid rent account is an asset account that records rent payments made in advance for future periods. It needs adjustment to recognize the portion of rent expense that applies to the current accounting period, ensuring accurate financial reporting.

To adjust the pre-paid rent account, calculate the portion of pre-paid rent that applies to the current period and record it as rent expense. Debit rent expense and credit pre-paid rent for the amount allocated to the period.

The journal entry to adjust pre-paid rent is: Debit Rent Expense (to recognize the expense) and Credit Pre-paid Rent (to reduce the asset account) for the amount of rent applicable to the current period.

![Quick Books Desktop Pro Plus 2024 | LIFETIME Version | USB | Only for Mac [software_key_card]](https://m.media-amazon.com/images/I/41xG2aOWLLL._AC_UL320_.jpg)

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UL320_.jpg)