When determining rent based on net present value (NPV), the goal is to align rental income with the property’s long-term financial worth, considering future cash flows and discounting them to their current value. This approach involves estimating the property’s future rental income, operating expenses, and potential appreciation, then discounting these cash flows using an appropriate discount rate to calculate the NPV. By setting rent at a level that reflects the property’s NPV, landlords can ensure that the rental income adequately compensates for the investment’s risks and opportunity costs while maintaining competitiveness in the market. This method is particularly useful for commercial properties or long-term leases, where a strategic, financially grounded approach to rent pricing is essential.

| Characteristics | Values |

|---|---|

| Definition | Rent based on the Net Present Value (NPV) of future cash flows from the property. |

| Purpose | To set rent that reflects the property's long-term value and profitability. |

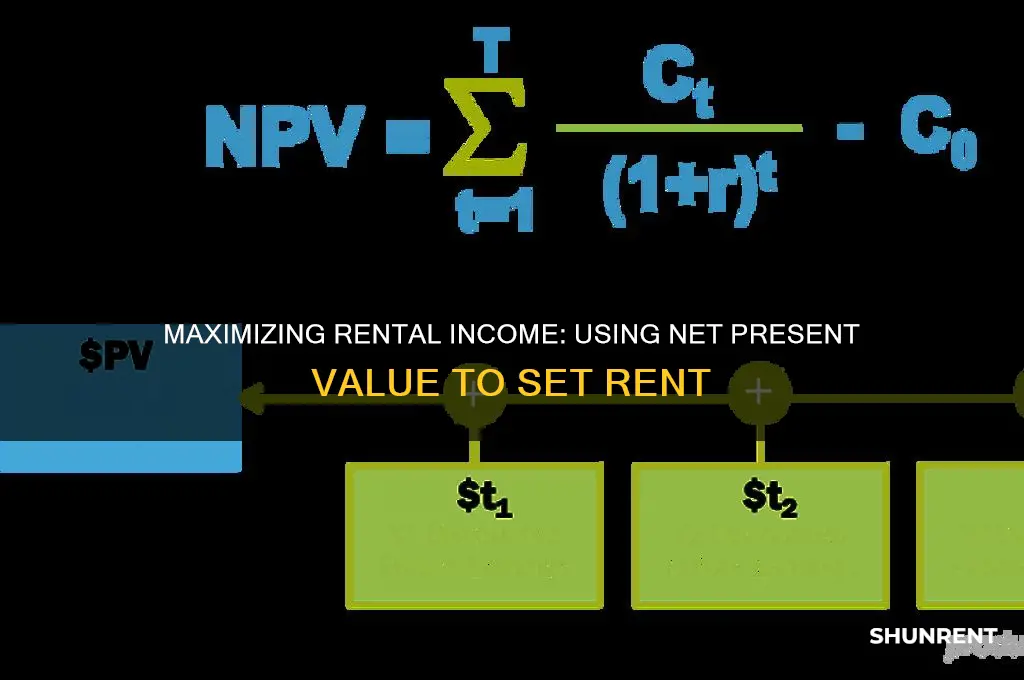

| Key Formula | ( \text = \sum_^ \frac{(1+r)^t} - \text ) |

| Discount Rate (r) | Typically 5-10%, reflecting the property's risk and market conditions. |

| Cash Flows (Cₜ) | Projected rental income, adjusted for vacancies, maintenance, and taxes. |

| Time Period (n) | Usually 5-10 years, depending on lease term and property type. |

| Initial Investment | Purchase price, renovation costs, and other upfront expenses. |

| Rent Calculation | Rent = (NPV / n) + Operating Expenses + Desired Return on Investment (ROI). |

| Market Adjustments | Adjust rent based on local market rates, demand, and comparable properties. |

| Risk Factors | Vacancy rates, inflation, interest rate changes, and property depreciation. |

| Tools | Excel, financial calculators, or real estate investment software. |

| Example | If NPV = $500,000 over 10 years, annual rent = $50,000 + expenses + ROI. |

| Advantages | Aligns rent with property value, attracts long-term tenants, maximizes ROI. |

| Disadvantages | Requires accurate projections, sensitive to discount rate and cash flow assumptions. |

| Best Use Cases | Commercial properties, long-term leases, and stable real estate markets. |

Explore related products

What You'll Learn

- Discount Rate Selection: Choose appropriate discount rate reflecting investment risk and opportunity cost

- Cash Flow Projections: Estimate future rental income and expenses accurately for NPV calculation

- Time Horizon: Define the period for analysis, aligning with investment or lease duration

- Terminal Value Calculation: Assess property value at the end of the analysis period

- Sensitivity Analysis: Test NPV under varying assumptions to ensure rent pricing robustness

![]()

Discount Rate Selection: Choose appropriate discount rate reflecting investment risk and opportunity cost

When determining how to base rent off net present value (NPV), selecting an appropriate discount rate is crucial. The discount rate serves as a bridge between future cash flows and their present value, reflecting both the investment risk and the opportunity cost of capital. It should be carefully chosen to ensure that the NPV calculation accurately represents the property’s value and aligns with the investor’s financial goals. The discount rate is not arbitrary; it must account for factors such as market volatility, inflation, and the specific risks associated with the property or tenant. For instance, a higher discount rate is typically applied to riskier investments to compensate for potential uncertainties, while a lower rate may be used for stable, low-risk assets.

To choose an appropriate discount rate, start by considering the risk-free rate, which is often based on government bond yields. This rate represents the return an investor could expect from a risk-free investment over a similar time horizon. Next, add a risk premium to account for the additional uncertainty associated with the property investment. The risk premium can vary depending on factors such as tenant creditworthiness, lease duration, property location, and market conditions. For example, a property with a long-term lease to a high-credit tenant may warrant a lower risk premium compared to a property with short-term leases in a volatile market. Additionally, the opportunity cost of capital—the return an investor could earn from alternative investments—should be factored into the discount rate to ensure the property investment is competitive.

Another important consideration is the weighted average cost of capital (WACC), which reflects the average rate of return a company is expected to pay its investors. While WACC is more commonly used in corporate finance, it can provide a benchmark for property investments, especially for commercial real estate. However, WACC may not fully capture the unique risks of a specific property, so adjustments are often necessary. For instance, if the property’s cash flows are highly dependent on market rents, the discount rate should incorporate a premium for rental market volatility. Similarly, properties in emerging markets or with unique operational risks may require a higher discount rate to account for these uncertainties.

Inflation expectations also play a significant role in discount rate selection. Since rent and property values are often tied to inflation, the discount rate should reflect the anticipated inflation rate over the investment period. Failure to account for inflation can lead to an overestimation of the property’s present value. For example, if inflation is expected to be 3% annually, the discount rate should include this component to ensure the NPV calculation remains realistic. Additionally, consider whether the rent is structured with built-in escalations tied to inflation, as this can reduce the overall risk and potentially justify a lower discount rate.

Finally, it’s essential to benchmark the discount rate against comparable investments in the market. Analyze similar properties or real estate deals to understand the range of discount rates being used. This can provide valuable context and ensure that the chosen rate is competitive and reasonable. For instance, if comparable commercial properties are using discount rates between 8% and 12%, your rate should fall within this range unless there are specific factors justifying a deviation. By combining these considerations—risk-free rate, risk premium, opportunity cost, inflation, and market benchmarks—investors can select a discount rate that accurately reflects the investment’s risk profile and ensures a fair valuation of the property’s rent based on NPV.

Leasing vs Renting: What's the Difference?

You may want to see also

Explore related products

![]()

Cash Flow Projections: Estimate future rental income and expenses accurately for NPV calculation

Accurately estimating future rental income and expenses is critical for calculating the Net Present Value (NPV) of a rental property. NPV is a financial metric that determines the profitability of an investment by discounting future cash flows to their present value. To base rent off NPV, you must first project cash flows with precision. Start by analyzing historical rental income data for similar properties in the area to establish a baseline. Consider factors such as location, property type, and market trends to forecast future rent increases or decreases. For instance, if the local market is experiencing high demand, you might project modest annual rent increases, typically between 2% and 5%, depending on inflation and supply-demand dynamics.

Expenses must also be meticulously projected to ensure an accurate NPV calculation. Categorize expenses into fixed (e.g., property taxes, insurance) and variable (e.g., maintenance, repairs) costs. Fixed expenses can often be estimated based on historical data and known future obligations, while variable expenses require a more conservative approach. For example, set aside a reserve for maintenance by allocating 1% to 4% of the property’s value annually, depending on its age and condition. Additionally, account for vacancy rates by researching local averages and adjusting rental income projections accordingly. A common practice is to assume a 5% to 10% vacancy rate, reducing expected income to reflect periods when the property may be unoccupied.

Inflation and discount rates play a significant role in cash flow projections for NPV calculations. Adjust future cash flows for inflation to ensure they are stated in today’s dollars. Use the Consumer Price Index (CPI) or a conservative inflation rate (e.g., 2% to 3%) to project increases in both income and expenses. The discount rate, which reflects the required rate of return, should be chosen based on the investor’s risk tolerance and the property’s risk profile. A higher discount rate will reduce the present value of future cash flows, making the investment appear less attractive.

To enhance accuracy, perform sensitivity analysis by varying key assumptions such as rent growth, vacancy rates, and expense levels. This helps identify how changes in these variables impact the NPV, providing a range of potential outcomes. For example, model scenarios with lower rent growth and higher vacancy rates to assess the investment’s resilience under less favorable conditions. Sensitivity analysis ensures that your projections are robust and that the rent is set at a level that maximizes NPV while accounting for potential risks.

Finally, leverage technology and tools to streamline cash flow projections. Spreadsheet software like Excel or specialized real estate investment analysis tools can automate calculations and scenario modeling. These tools allow you to input assumptions, generate cash flow statements, and calculate NPV efficiently. Regularly update your projections as market conditions evolve to ensure that the rent remains aligned with the property’s NPV. By combining thorough research, conservative assumptions, and dynamic modeling, you can estimate future rental income and expenses accurately, enabling you to base rent off NPV effectively.

Raising Rent in Michigan: Legal Steps and Tenant Communication Tips

You may want to see also

Explore related products

![]()

Time Horizon: Define the period for analysis, aligning with investment or lease duration

When basing rent off net present value (NPV), defining the time horizon is a critical step. The time horizon represents the period over which cash flows, including rental income and expenses, will be analyzed to determine the present value of the investment or lease. This period must align precisely with the investment or lease duration to ensure accuracy in NPV calculations. For example, if a lease agreement spans 10 years, the time horizon should also be set to 10 years to capture all relevant cash flows over the entire lease term. This alignment ensures that the NPV calculation reflects the full financial impact of the lease or investment.

The choice of time horizon directly influences the discounting of future cash flows to their present value. A longer time horizon includes more future cash flows, which can significantly affect the NPV result, especially when using a discount rate to account for the time value of money. For instance, a 20-year lease will have a higher cumulative present value of rental income compared to a 5-year lease, assuming all other factors remain constant. Therefore, the time horizon must be carefully selected to match the specific duration of the lease or investment, avoiding underestimation or overestimation of the NPV.

In practice, the time horizon should also consider the expected holding period of the investment. If an investor plans to hold a property for 15 years, the time horizon should reflect this period, even if the lease duration is shorter. This approach ensures that the NPV calculation accounts for potential future leasing scenarios or property resale value after the initial lease expires. However, if the analysis is strictly focused on the lease term, the time horizon should be limited to that period to avoid introducing irrelevant variables.

For leases with renewal options or escalation clauses, the time horizon may need to be extended to capture these future cash flows. For example, if a 5-year lease includes a 5-year renewal option with rent increases, the time horizon should be set to 10 years to account for both the initial term and the renewal period. This comprehensive approach ensures that the NPV calculation reflects the full potential income stream from the lease, providing a more accurate basis for setting rent.

Finally, consistency in the time horizon is essential when comparing multiple investment or leasing options. If analyzing different lease durations or investment scenarios, using a uniform time horizon allows for a fair comparison of NPVs. For instance, when evaluating a 7-year lease versus a 10-year lease, extending the time horizon to 10 years for both scenarios ensures that the comparison is based on the same temporal framework. This consistency helps in making informed decisions by accurately reflecting the long-term financial implications of each option.

Renting: How to Navigate Income Requirements

You may want to see also

Explore related products

![]()

Terminal Value Calculation: Assess property value at the end of the analysis period

When assessing the terminal value of a property at the end of an analysis period, the goal is to estimate the property's value at a future date, typically beyond the explicit forecast period. This value is crucial for determining the overall net present value (NPV) of the investment, which in turn can inform rent-setting strategies. The terminal value calculation is often the most significant component of a property’s NPV, especially for long-term investments. To begin, select an appropriate method for terminal value calculation, such as the perpetuity growth model or the exit multiple approach. The perpetuity growth model assumes that cash flows will grow at a constant rate indefinitely, while the exit multiple approach uses a market multiple (e.g., cap rate or price-to-earnings ratio) to estimate value based on comparable sales or industry standards.

In the perpetuity growth model, the terminal value is calculated as the final year’s net operating income (NOI) divided by the discount rate minus the growth rate. For example, if the NOI in the final year of the analysis period is $200,000, the discount rate is 8%, and the growth rate is 2%, the terminal value would be $200,000 / (8% - 2%) = $200,000 / 6% = $3,333,333. This method is straightforward but relies heavily on stable growth assumptions. When using this approach to base rent, ensure that the growth rate aligns with expected rental income increases over the long term. For instance, if historical rental growth has been 2% annually, this rate can be applied to project future rents and, consequently, the terminal value.

The exit multiple approach, on the other hand, is more market-driven and involves multiplying a metric (e.g., NOI) by a cap rate or other multiple observed in the market. For example, if comparable properties are trading at a 6% cap rate and the final year’s NOI is $200,000, the terminal value would be $200,000 / 6% = $3,333,333. This method is particularly useful when market data is robust and reliable. When basing rent off NPV, this approach allows investors to align rental rates with market expectations of property value at the end of the analysis period. For instance, if the terminal value suggests a higher property value, rents can be adjusted upward to maximize returns.

Regardless of the method chosen, it’s essential to discount the terminal value back to the present using the appropriate discount rate to incorporate it into the overall NPV calculation. The discount rate should reflect the risk associated with the investment and the time value of money. For example, if the terminal value is $3,333,333 and the analysis period is 10 years with an 8% discount rate, the present value of the terminal value would be $3,333,333 / (1 + 8%)^10 = $1,948,565. This present value is then added to the sum of the discounted cash flows during the explicit forecast period to determine the total NPV of the property.

Finally, when using the NPV to base rent, consider how the terminal value impacts the overall investment return. If the terminal value represents a significant portion of the NPV, it may justify higher rents during the holding period to achieve the desired yield. Conversely, a lower terminal value might necessitate more conservative rent-setting to ensure cash flows remain attractive. Regularly review market conditions and update terminal value assumptions to ensure rent levels remain competitive and aligned with long-term property value projections. By integrating terminal value calculations into rent-setting strategies, investors can optimize both current income and future property value.

Evicting a Renter: Understanding the Required Notice Period for Landlords

You may want to see also

Explore related products

![]()

Sensitivity Analysis: Test NPV under varying assumptions to ensure rent pricing robustness

Sensitivity analysis is a critical step in ensuring the robustness of rent pricing when basing it on Net Present Value (NPV). By testing the NPV under varying assumptions, landlords and property managers can assess how changes in key variables impact the overall financial viability of the rental strategy. This process helps identify potential risks and ensures that the rent pricing remains resilient under different scenarios. For instance, variables such as discount rates, rental growth rates, vacancy rates, and operating expenses can significantly influence the NPV calculation. By systematically adjusting these inputs, one can gauge the sensitivity of the NPV to each factor and make informed decisions.

To begin the sensitivity analysis, start by identifying the most influential variables in the NPV calculation. For rental properties, these typically include the discount rate, which reflects the cost of capital or required return, and the rental growth rate, which accounts for potential increases in rent over time. Additionally, vacancy rates and operating expenses are crucial, as they directly affect cash flows. Once these variables are identified, create a range of plausible values for each, considering both optimistic and pessimistic scenarios. For example, discount rates might vary from 5% to 10%, while vacancy rates could range from 2% to 8%, depending on market conditions.

Next, perform the sensitivity analysis by recalculating the NPV for each combination of variable values. This can be done using spreadsheet models or financial software, where inputs are adjusted, and the NPV is automatically recomputed. The goal is to observe how sensitive the NPV is to changes in each variable. For instance, if a small increase in the discount rate significantly reduces the NPV, it indicates that the rent pricing strategy is highly sensitive to the cost of capital. Similarly, if higher vacancy rates drastically lower the NPV, it highlights the importance of maintaining low vacancy levels. Visual aids like tornado diagrams or sensitivity charts can help illustrate the impact of each variable graphically.

Interpreting the results of the sensitivity analysis is key to refining the rent pricing strategy. If the NPV remains stable across a wide range of assumptions, the rent pricing is robust and less likely to be affected by market fluctuations. However, if the NPV is highly sensitive to certain variables, it may be necessary to adjust the rent or implement risk mitigation strategies. For example, if operating expenses are a significant concern, landlords might consider long-term maintenance contracts to stabilize costs. Alternatively, if vacancy rates pose a risk, offering lease incentives or improving property marketing could help maintain occupancy levels.

Finally, incorporate the insights from the sensitivity analysis into the rent pricing decision. This might involve setting a base rent that aligns with the most likely scenario while building in buffers to account for adverse conditions. For instance, if the analysis shows that a 6% vacancy rate reduces the NPV to an unacceptable level, the rent could be adjusted to ensure profitability even at a 7% vacancy rate. Additionally, regularly updating the sensitivity analysis as market conditions evolve ensures that the rent pricing remains aligned with the property’s financial objectives. By systematically testing the NPV under varying assumptions, landlords can establish a rent pricing strategy that is both robust and adaptable to changing circumstances.

Mastering Renting: A Step-by-Step Guide to Budgeting for Bills

You may want to see also

Frequently asked questions

Net Present Value (NPV) is the sum of the present values of all future cash flows from an investment, discounted at a specific rate. When setting rent based on NPV, you calculate the present value of all future rental income and expenses to determine a rent amount that aligns with the property's long-term financial value.

To calculate NPV, list all future cash flows (rental income, maintenance costs, etc.), discount them to their present value using a discount rate (e.g., market interest rate), and sum them up. Subtract the initial investment (property cost) to get the NPV. Rent should be set to maximize positive NPV over the property’s lifecycle.

The discount rate should reflect the risk and return expectations of the investment. Common rates range from 5% to 12%, depending on market conditions, property type, and investor risk tolerance. A higher rate accounts for greater risk or opportunity cost.

Traditional methods often rely on comparable market rents or a percentage of property value. Basing rent off NPV is more forward-looking, considering all future cash flows and their present value, ensuring the rent aligns with the property’s long-term financial goals and risk profile.

Yes, NPV can be applied to both residential and commercial properties. However, the cash flow patterns and discount rates may differ. Commercial properties often have longer lease terms and higher maintenance costs, which should be factored into the NPV calculation when setting rent.