Billing for rent in QuickBooks is a straightforward process that streamlines property management tasks for landlords and property managers. To begin, ensure you have set up your tenants as customers within QuickBooks, allowing you to track their rental payments efficiently. Next, create a service item specifically for rent, which can be customized to include details such as the property address and rental amount. When it’s time to bill, generate an invoice for each tenant, selecting the appropriate rent item and adjusting the amount as needed for any additional charges or credits. QuickBooks also allows you to automate recurring invoices, ensuring rent bills are sent out consistently each month. Finally, track payments and reconcile them against the invoices to maintain accurate financial records, making rent collection and accounting seamless and organized.

Explore related products

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UL320_.jpg)

What You'll Learn

- Setting up rental properties in QuickBooks for accurate tenant billing and tracking

- Creating recurring invoices for rent to automate monthly billing processes efficiently

- Applying late fees and tracking overdue rent payments within QuickBooks easily

- Recording rent payments and reconciling accounts to maintain accurate financial records

- Generating rent-related reports for insights into income, expenses, and tenant balances

![]()

Setting up rental properties in QuickBooks for accurate tenant billing and tracking

Managing rental properties requires precision in billing and tracking to ensure financial accuracy and tenant satisfaction. QuickBooks offers robust tools to streamline this process, but setting up your properties correctly is crucial. Begin by creating a separate QuickBooks file or class for each rental property to maintain clear financial boundaries. This segregation allows you to track income and expenses per property, simplifying tax reporting and performance analysis. For instance, if you own three properties, label them as "Property A," "Property B," and "Property C" within QuickBooks, ensuring each has its own income and expense accounts.

Next, establish customer profiles for each tenant within QuickBooks. Assign each tenant to their respective property by linking their profile to the corresponding class or property account. This step ensures that rent payments are accurately recorded against the correct property. For example, if John Doe rents Property A, his customer profile should be tagged under the "Property A" class. Additionally, customize invoices to include property-specific details, such as unit number, lease terms, and payment due dates, to avoid confusion and enhance professionalism.

To automate billing, set up recurring invoices for each tenant based on their lease agreements. QuickBooks allows you to schedule rent invoices to be sent automatically on specific dates, reducing manual effort and minimizing late payments. Include late fees as a line item on the invoice template, with clear terms outlined in the payment section. For instance, a $50 late fee applied after the 5th of the month can be pre-configured, ensuring consistency and compliance with lease agreements.

Tracking expenses is equally vital for maintaining profitability. Create dedicated expense accounts for each property, categorizing costs like maintenance, repairs, and utilities. Use the "Split Transaction" feature to allocate shared expenses proportionally across properties. For example, if a landscaping bill covers multiple units, divide the cost based on square footage or number of tenants. Regularly reconcile these accounts to identify discrepancies and ensure financial health.

Finally, leverage QuickBooks reports to monitor property performance. Run Profit & Loss statements by class to assess each property’s profitability. Use the Accounts Receivable Aging Summary to track outstanding rent payments and identify tenants at risk of default. Customizing these reports to include key metrics, such as occupancy rates or maintenance costs per unit, provides actionable insights for informed decision-making. By meticulously setting up rental properties in QuickBooks, landlords can achieve accurate billing, efficient tracking, and enhanced financial oversight.

Rent Your Book on Amazon: A Step-by-Step Guide

You may want to see also

Explore related products

![Quick-Book Desktop Pro 2024 | LIFETIME Version | USB | Only for PC [software_key_card]](https://m.media-amazon.com/images/I/61UVBdvXIeL._AC_UL320_.jpg)

![]()

Creating recurring invoices for rent to automate monthly billing processes efficiently

Automating monthly rent billing in QuickBooks saves time and reduces errors, ensuring tenants receive consistent, timely invoices. To set up recurring invoices, start by navigating to the "Create" menu and selecting "Invoice." Fill in the tenant’s details, including their name, address, and rental amount. Save this invoice as a template by clicking "Save as Template" and naming it clearly, such as "Monthly Rent Invoice – [Tenant Name]." This template becomes the foundation for automation.

Next, access the "Recurring Transactions" feature under the "Lists" menu. Choose "Invoice" as the transaction type and select the template you created. Specify the frequency as "Monthly" and set the start and end dates for the billing cycle. QuickBooks allows you to customize further by adding reminders or attaching rental agreements as PDFs. Once configured, the system automatically generates and sends invoices on the scheduled date, eliminating manual intervention.

While automation streamlines the process, it’s crucial to review recurring invoices periodically. Tenant details, such as contact information or rental amounts, may change. QuickBooks doesn’t update these fields automatically, so manual checks every quarter ensure accuracy. Additionally, consider setting up payment links within the invoice to encourage prompt payments. This feature integrates seamlessly with QuickBooks Payments, allowing tenants to pay online directly from the invoice.

A practical tip for landlords managing multiple properties is to use class tracking in QuickBooks. Assign each property a class and apply it to the recurring invoice. This enables easy reporting on rental income by property, providing clarity during tax season or financial reviews. By combining recurring invoices with class tracking, landlords can maintain organized, efficient billing processes while gaining valuable insights into their rental portfolio.

Unlock Your J7: Removing Rent-A-Center Phone Lock Easily

You may want to see also

Explore related products

![Quick Books Desktop Pro Plus 2024 | LIFETIME Version | USB | Only for Mac [software_key_card]](https://m.media-amazon.com/images/I/41xG2aOWLLL._AC_UL320_.jpg)

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)

![]()

Applying late fees and tracking overdue rent payments within QuickBooks easily

Late fees are a necessary tool for landlords to encourage timely rent payments, but applying them manually can be tedious and error-prone. QuickBooks simplifies this process by automating late fee calculations and tracking overdue payments, ensuring accuracy and saving you valuable time.

Setting Up Late Fees in QuickBooks

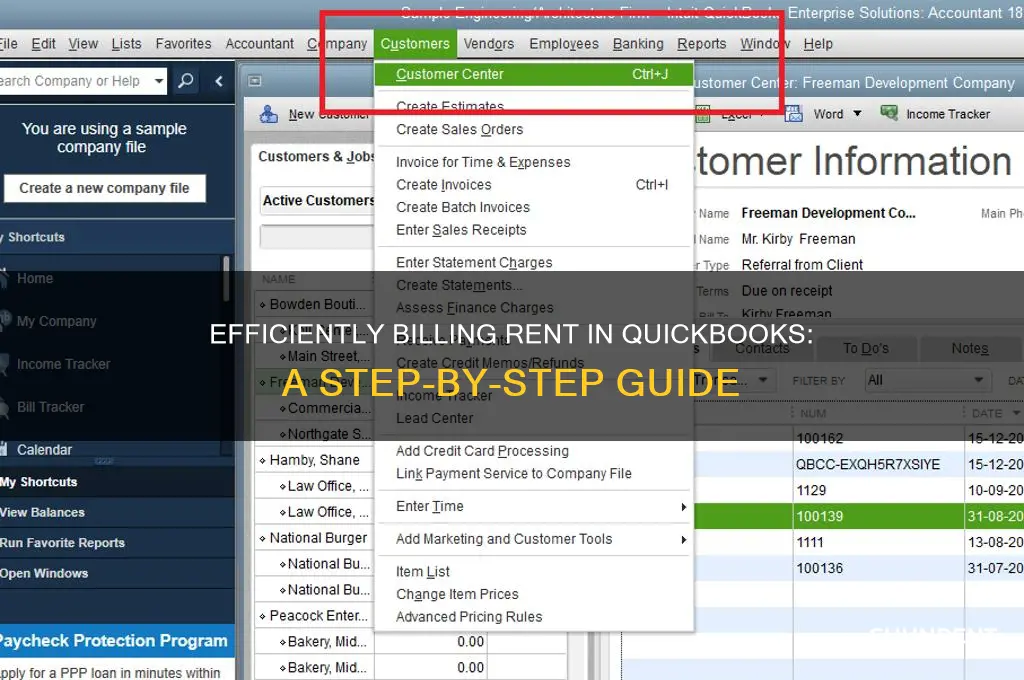

Begin by defining your late fee policy within QuickBooks. Navigate to the "Customers" menu, select "Customer Center," and choose the tenant's profile. Under the "Payment Settings" tab, you'll find the "Finance Charges" section. Here, you can specify the grace period (the number of days after the due date before a late fee is applied), the late fee percentage or fixed amount, and the frequency of late fee assessments (e.g., monthly).

QuickBooks will automatically calculate and add late fees to overdue invoices based on these settings, eliminating the need for manual intervention.

Tracking Overdue Rent Payments

QuickBooks provides robust reporting tools to monitor overdue rent payments. The "A/R Aging Summary" report offers a snapshot of outstanding balances, categorizing them by aging periods (e.g., 0-30 days, 31-60 days). This report allows you to quickly identify tenants with overdue payments and prioritize follow-up actions. Additionally, the "Open Invoices" report provides a detailed list of all unpaid invoices, including due dates and outstanding amounts, enabling you to track individual tenant payment histories.

Automating Payment Reminders

To further streamline the process, QuickBooks allows you to set up automated payment reminders. These reminders can be sent via email or text message, notifying tenants of upcoming due dates and overdue payments. You can customize the reminder templates to include personalized messages, payment instructions, and late fee information. By automating reminders, you can proactively encourage timely payments and reduce the need for manual follow-ups.

Best Practices for Late Fee Application

When applying late fees, it's essential to maintain transparency and consistency. Clearly communicate your late fee policy to tenants in the lease agreement and on each invoice. Ensure that late fees are reasonable and comply with local regulations. Regularly review your late fee settings in QuickBooks to ensure they align with your policy and make adjustments as needed. By leveraging QuickBooks' automation capabilities and reporting tools, you can efficiently manage late fees and overdue rent payments, fostering a more organized and professional rental management process.

Does Rent-A-Center Offer Lazy Boy Recliners for Rent or Sale?

You may want to see also

Explore related products

![]()

Recording rent payments and reconciling accounts to maintain accurate financial records

Accurate financial record-keeping hinges on meticulous recording of rent payments and diligent account reconciliation. In QuickBooks, this process begins with setting up a dedicated rental income account and linking it to tenant records. Each rent payment received should be recorded as a deposit into this account, ensuring clarity in tracking rental income. For instance, if a tenant pays $1,200 monthly, log this transaction under the rental income account, categorizing it as "Rent Received." This foundational step prevents commingling of funds and provides a clear audit trail.

Reconciliation is the linchpin of maintaining accuracy. Monthly, compare the recorded rent payments in QuickBooks against bank statements to identify discrepancies. QuickBooks’ reconciliation tool allows you to match transactions, flagging any unmatched entries. For example, if a $1,200 payment appears in the bank statement but not in QuickBooks, investigate whether it was misrecorded or omitted. Addressing such discrepancies promptly ensures that financial statements reflect the true financial position of the rental business.

Automating recurring rent payments in QuickBooks can streamline this process. Set up memorized transactions for tenants with consistent payment amounts and due dates. This reduces manual entry errors and ensures timely recording. However, automation requires periodic review to account for rent increases, late fees, or prorated payments. For instance, if a tenant’s rent increases from $1,200 to $1,300 mid-lease, update the memorized transaction to reflect this change, avoiding underreporting of income.

A critical yet often overlooked aspect is handling partial payments and late fees. When a tenant pays $600 instead of $1,200, record the partial payment and create an invoice for the outstanding balance. Late fees should be tracked separately under a "Late Fees" income account to distinguish them from rent. This granular approach provides insights into tenant payment behavior and ensures compliance with lease agreements.

Finally, leverage QuickBooks reports to monitor rental income trends and account health. Run the "Profit and Loss by Customer" report to analyze income per tenant, or use the "Account QuickReport" to scrutinize the rental income account. These reports not only aid in financial analysis but also highlight anomalies that may require further investigation. By integrating these practices, landlords can maintain accurate, transparent, and reliable financial records in QuickBooks.

Renting in Belize: A Step-by-Step Guide to Finding Your Perfect Place

You may want to see also

Explore related products

![Quicken Classic Deluxe for New Subscribers| 1 Year [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61ypcFpjCuL._AC_UL320_.jpg)

![]()

Generating rent-related reports for insights into income, expenses, and tenant balances

Effective rent management in QuickBooks hinges on the ability to generate detailed reports that provide actionable insights into income, expenses, and tenant balances. By leveraging QuickBooks’ reporting features, landlords and property managers can track financial performance, identify trends, and ensure compliance with lease agreements. Start by customizing the Profit & Loss Detail Report to filter income and expenses specific to rental properties. This report can be tailored to show monthly or annual summaries, helping you understand net income after accounting for maintenance, repairs, and property taxes. Pair this with the Accounts Receivable Aging Report to monitor tenant balances, highlighting overdue payments and enabling timely follow-ups.

To dive deeper into tenant-specific data, utilize the Customer Balance Detail Report. This tool breaks down each tenant’s payment history, outstanding balances, and recent transactions, providing a clear snapshot of their financial standing. For properties with multiple units, create Class Tracking Reports to categorize income and expenses by property or unit. This allows for a granular analysis of which properties are most profitable or require attention. For example, if one property consistently shows higher maintenance costs, you can investigate the root cause and allocate resources more efficiently.

Another critical report is the Transaction Detail Report, which lists all rent-related transactions, including payments, late fees, and refunds. This report is invaluable for reconciling accounts and ensuring accuracy in financial records. Combine it with the Budget vs. Actual Report to compare projected rental income against actual receipts, identifying variances that may require adjustments in budgeting or rent pricing strategies. For instance, if actual income falls short of projections, you might consider raising rents or reducing expenses.

When generating these reports, ensure data accuracy by consistently categorizing transactions under specific income and expense accounts. Use Memorized Transactions for recurring rent charges to streamline billing and reduce errors. Additionally, set up Custom Fields for tenant-specific details, such as lease start dates or security deposit amounts, to enrich your reports with contextual information. Regularly review these reports—monthly or quarterly—to maintain financial health and make data-driven decisions.

Finally, export these reports into Excel or PDF formats for further analysis or sharing with stakeholders. QuickBooks’ reporting tools not only simplify rent management but also empower property managers to optimize operations, improve tenant relationships, and maximize profitability. By mastering these reports, you transform raw data into strategic insights, ensuring your rental business thrives in a competitive market.

Balancing Restaurant Rent Costs: Ideal Revenue Percentage for Sustainability

You may want to see also

Frequently asked questions

To set up a rental property in QuickBooks, go to the "Customers" menu, select "Customer Center," and add a new customer for the tenant. Then, create a new item under "Items & Services" for the rent, specifying it as a "Service" or "Other Charge." Assign the appropriate income account for tracking rent revenue.

To create recurring invoices for rent, go to the "Customers" menu, select "Create Recurring Invoices," and choose "Invoice" as the transaction type. Enter the tenant’s details, add the rent item, and set the frequency (e.g., monthly). Save the template, and QuickBooks will automatically generate invoices on the specified schedule.

To track late fees, create a separate item under "Items & Services" labeled as a "Late Fee" and assign it to a specific income account. When a tenant incurs a late fee, add this item to their invoice. You can also set up a reminder in QuickBooks to notify tenants of overdue payments before applying the fee.

![Quickbooks Online For Beginners [10 In 1]: The Complete Visual Guide to Mastering QuickBooks Fast. Automate Your Finances, Stay Tax-Ready, and Take Control of Your Business in 30 Days or Less.](https://m.media-amazon.com/images/I/718cpZEH4-L._AC_UL320_.jpg)

![QuickBooks Premier Retail Edition 2008 [OLD VERSION]](https://m.media-amazon.com/images/I/51YBYVJpvLL._AC_UL320_.jpg)