Managing your finances effectively is crucial for maintaining financial stability, and one of the most significant aspects of this is budgeting for rent and bills. These fixed expenses often represent a substantial portion of your monthly income, making it essential to plan and allocate funds wisely. By creating a detailed budget, you can ensure that you cover these necessities while still having money left for savings, emergencies, and discretionary spending. Start by listing all your monthly income sources and then itemize your essential expenses, such as rent, utilities, internet, and insurance. Prioritize these payments to avoid late fees or disruptions in services, and consider setting up automatic payments to streamline the process. Additionally, track your spending to identify areas where you can cut back if needed, and regularly review your budget to adjust for any changes in income or expenses. With a well-structured plan, you can achieve financial peace of mind and work toward your long-term goals.

Explore related products

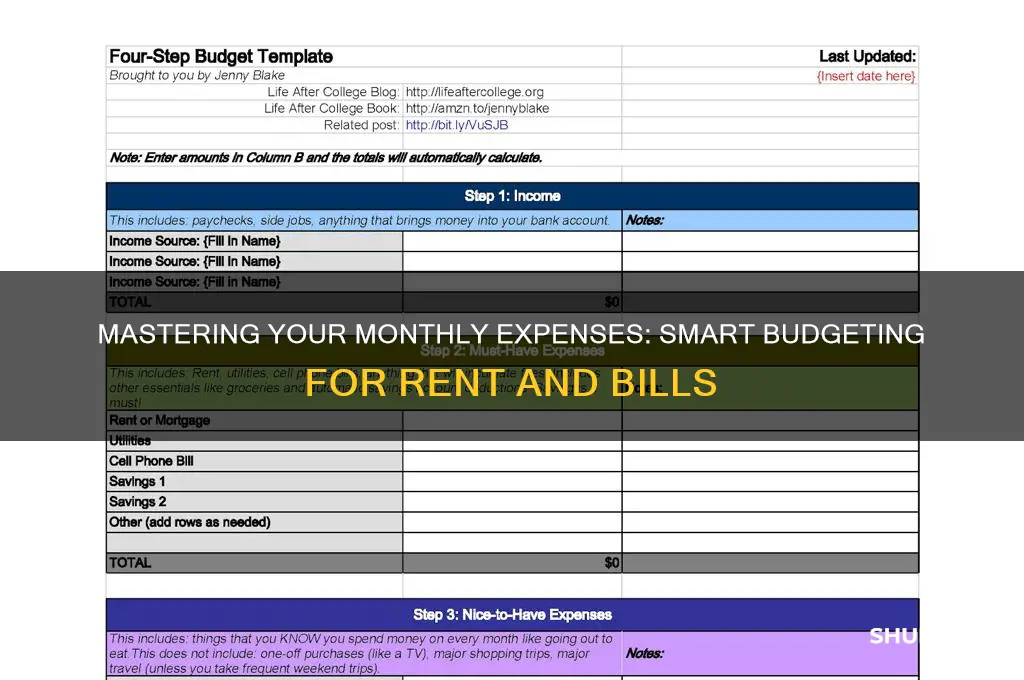

What You'll Learn

![]()

Track Income & Expenses

Understanding your financial flow is the cornerstone of effective budgeting. Tracking income and expenses isn’t just about recording numbers; it’s about gaining clarity on where your money comes from and where it goes. Start by listing all sources of income—salary, freelance earnings, or side hustles—and categorizing them for a clear picture of your total monthly inflow. This step is critical because it sets the foundation for allocating funds to rent, bills, and other necessities. Without this awareness, even the most well-intentioned budget can falter.

Next, monitor your expenses with precision. Break them into fixed (rent, utilities) and variable (groceries, entertainment) categories. Use digital tools like budgeting apps or spreadsheets to log every transaction, no matter how small. For instance, apps like Mint or YNAB sync with your bank accounts to automatically categorize spending, saving you time and reducing errors. If you prefer a hands-on approach, dedicate a notebook to daily entries or use a simple Excel template. The goal is consistency—make tracking a habit, even if it’s just 10 minutes daily.

A common pitfall is underestimating irregular expenses, such as quarterly bills or annual subscriptions. To avoid this, review past bank statements to identify patterns and set aside a small amount monthly for these costs. For example, if your car insurance is $600 annually, allocate $50 each month to a dedicated savings account. This prevents scrambling when the bill arrives and ensures your rent and essential bills remain unaffected.

Comparing your tracked income and expenses reveals areas for adjustment. If your rent and bills consume more than 50% of your income, it’s a red flag. Use this data to negotiate lower rates, find cheaper alternatives, or increase income through overtime or side gigs. For instance, switching to a cheaper internet plan or taking on a weekend job can free up funds. The key is to act on insights rather than letting numbers sit idly.

Finally, tracking isn’t a one-time task—it’s an ongoing process. Review your records monthly to identify trends, such as overspending on dining out or underutilized subscriptions. Adjust your budget accordingly, ensuring it remains realistic and aligned with your goals. Over time, this practice builds financial discipline and empowers you to make informed decisions about rent, bills, and beyond. Remember, the goal isn’t perfection but progress toward financial stability.

Late Rent Payments: Impact on Your Rental History Explained

You may want to see also

Explore related products

![]()

Set Rent Affordability Limit

Determining how much rent you can afford is a critical step in budgeting for your living expenses. A widely accepted rule of thumb is the 30% rule, which suggests that you should spend no more than 30% of your gross monthly income on rent. For example, if your monthly income is $4,000, your rent should ideally not exceed $1,200. This guideline helps prevent financial strain and ensures you have enough left over for other essential expenses like utilities, groceries, and savings.

However, the 30% rule isn’t one-size-fits-all. Factors like your location, income stability, and financial goals can influence this limit. In high-cost-of-living cities like New York or San Francisco, you might need to allocate closer to 40% of your income to rent, but only if it doesn’t compromise your ability to save or cover other bills. Conversely, if you’re in a lower-cost area or have significant debt, aiming for 25% might be more prudent. Analyze your unique circumstances before committing to a percentage.

To set a realistic rent affordability limit, start by calculating your monthly take-home pay after taxes and deductions. Subtract fixed expenses like student loans, car payments, and insurance. The remaining amount is your discretionary income, from which you’ll allocate funds for rent, utilities, and variable expenses. For instance, if your take-home pay is $3,500 and fixed expenses total $800, you’re left with $2,700. Applying the 30% rule to your gross income ($4,000 * 0.30 = $1,200) might be feasible here, but ensure it aligns with your remaining budget for other necessities.

A practical tip is to test your rent limit before signing a lease. Live on your proposed budget for a month or two to see if it’s sustainable. Track your spending to identify areas where you might need to cut back or adjust. For instance, if allocating 30% to rent leaves you struggling to pay bills, consider finding a cheaper place or increasing your income through side gigs. This trial run can prevent long-term financial stress and help you make an informed decision.

Finally, don’t forget to factor in additional housing costs like utilities, internet, and maintenance. These can add 10–20% to your rent, so ensure your budget accounts for them. For example, if your rent is $1,200, plan for an extra $120–$240 monthly for utilities. Setting a rent affordability limit isn’t just about the number on the lease—it’s about creating a holistic budget that supports your financial well-being.

Renters' Guide: Securing Loan Approval Without Homeownership

You may want to see also

Explore related products

![]()

Prioritize Essential Bills

Essential bills are the non-negotiables—housing, utilities, and food—that form the bedrock of your budget. Without these, daily life becomes unsustainable. Start by listing these expenses and their due dates. Housing (rent or mortgage) typically consumes 25-30% of your income, according to the 50/30/20 rule. Utilities like electricity, water, and internet average $200-$400 monthly, depending on location and usage. Groceries, another essential, should align with dietary needs and household size, averaging $300-$600 for individuals and $800-$1,200 for families. Prioritize these first to avoid late fees, service disruptions, or eviction.

Analyzing your essential bills reveals opportunities for optimization. For instance, compare utility providers to find better rates or switch to energy-efficient appliances to reduce consumption. Rent negotiations or roommate arrangements can lower housing costs. Meal planning and bulk buying cut grocery expenses. Tools like bill-tracking apps or spreadsheets help monitor due dates and payments. By scrutinizing these areas, you reclaim control over your finances, ensuring essentials are covered without overspending.

A persuasive argument for prioritizing essentials lies in their long-term impact. Paying rent on time builds credit and housing stability. Consistent utility payments prevent service cuts, which are costly to reinstate. Adequate food spending supports health, reducing medical expenses. Conversely, neglecting these bills leads to compounding problems: eviction, debt, or health issues. Think of essentials as investments in your present and future well-being, not mere obligations.

Comparing essential bills to discretionary spending highlights their urgency. While dining out or streaming services offer immediate gratification, they pale in importance to keeping a roof over your head or lights on. Use the "needs vs. wants" framework to allocate funds. For example, if faced with a tight month, pause subscription services before skipping a utility payment. This mindset shift ensures essentials remain the focal point of your budget, fostering financial resilience.

In practice, prioritizing essentials requires discipline and planning. Automate payments where possible to avoid forgetfulness. Set aside funds for essentials immediately upon receiving income, treating them as non-negotiable deductions. Keep a buffer for unexpected increases, like seasonal utility spikes. For instance, allocate $50 extra monthly for winter heating. By embedding these habits, you safeguard your financial foundation, freeing mental space for other goals.

Rent Loan Approval: Applying Without a Guarantor Made Easy

You may want to see also

Explore related products

![]()

Create an Emergency Fund

Life is unpredictable, and unexpected expenses can derail even the most carefully planned budget. That's why building an emergency fund is a cornerstone of financial resilience. Think of it as your safety net, a dedicated pool of money readily available to cover unforeseen costs like car repairs, medical bills, or a sudden loss of income.

Without it, you might be forced to rely on high-interest credit cards or loans, digging yourself into a deeper financial hole.

Aim to save enough to cover three to six months' worth of essential living expenses. This includes rent, utilities, groceries, transportation, and minimum debt payments. Start small – even $500 can provide a buffer against minor emergencies. Automate your savings by setting up regular transfers from your checking account to a dedicated emergency fund. Consider this a non-negotiable expense, just like rent or bills. High-yield savings accounts offer better interest rates than traditional savings accounts, helping your emergency fund grow faster.

Keep your emergency fund in a readily accessible account, but not so easily accessible that you're tempted to dip into it for non-emergencies.

Building an emergency fund requires discipline and sacrifice. It might mean cutting back on discretionary spending, like dining out or entertainment. Think of it as an investment in your future peace of mind. Remember, the goal is not to deprive yourself, but to create a financial cushion that allows you to weather life's unexpected storms.

Discover the Average Rent in Omaha, Nebraska: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Use Budgeting Tools/Apps

Budgeting for rent and bills doesn’t have to be a manual, error-prone process. Enter budgeting tools and apps—digital solutions designed to automate tracking, categorize expenses, and provide real-time insights. These platforms sync with bank accounts, credit cards, and even investment accounts, offering a holistic view of your finances. For instance, apps like Mint and YNAB (You Need A Budget) allow you to set specific allocations for rent, utilities, and other recurring expenses, ensuring you stay within your limits without constant spreadsheet updates.

Analytically speaking, the strength of budgeting apps lies in their ability to identify spending patterns you might overlook. For example, a tool like PocketGuard analyzes your income and expenses to highlight areas where you’re overspending, such as dining out, which could otherwise eat into your rent budget. By leveraging algorithms, these apps provide personalized recommendations—like suggesting cheaper alternatives for utilities or reminding you of upcoming bill payments. This data-driven approach transforms budgeting from guesswork into a strategic practice.

However, not all budgeting tools are created equal. Some, like EveryDollar, follow a zero-based budgeting philosophy, requiring every dollar to be assigned a purpose. Others, like Honeydue, focus on shared finances, ideal for couples splitting rent and bills. When choosing an app, consider your specific needs: Do you want a hands-on approach, or do you prefer automation? Are you budgeting solo or with a partner? For instance, if you’re prone to forgetting bill due dates, apps with built-in reminders, such as Prism, could be a game-changer.

A cautionary note: While budgeting apps streamline financial management, they require discipline and accuracy. Inputting incorrect data or ignoring alerts defeats their purpose. Additionally, some apps offer premium features at a cost—YNAB, for example, charges $99 annually after a 34-day free trial. Evaluate whether the benefits justify the expense, especially if you’re already tight on funds. Free alternatives like Goodbudget or manual methods like the envelope system might suffice for simpler needs.

In conclusion, budgeting tools and apps are powerful allies in managing rent and bills, but their effectiveness depends on how you use them. Start by syncing all relevant accounts for a comprehensive overview. Set clear goals within the app—allocate 30% of your income to rent, 15% to utilities, and so on. Regularly review the insights provided, adjusting your habits as needed. With the right tool and consistent effort, you’ll not only stay on top of your expenses but also build a sustainable financial foundation.

Understanding Your Rights as a Renter in Pennsylvania: A Comprehensive Guide

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This ensures you have enough left for other expenses like bills, savings, and leisure.

Track your average monthly utility costs over the past year and set aside that amount each month. For seasonal fluctuations, consider saving extra during low-cost months to cover higher bills in peak seasons.

Prioritize rent and essential bills (like electricity and water) first, as they are non-negotiable. Use the 50/30/20 rule: 50% for needs (rent, bills), 30% for wants, and 20% for savings and debt repayment.

Consider downsizing to a smaller rental, splitting rent with a roommate, or negotiating lower rent with your landlord. For bills, reduce energy usage, switch to cheaper providers, or cut non-essential services like subscriptions.

![[Undated] Monthly Budget Planner with 12 Bill Pockets for Income, Debt, Saving, Expense and Bill Tracker Organizer, Pink, Floral Design](https://m.media-amazon.com/images/I/71McwNBYKCL._AC_UL320_.jpg)