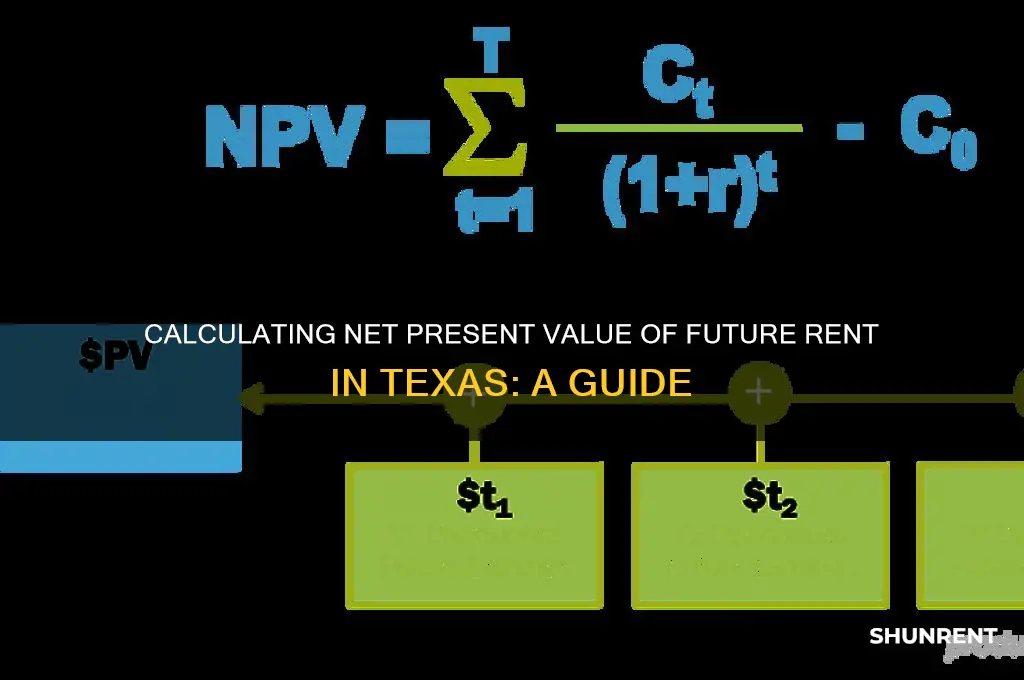

Calculating the Net Present Value (NPV) of future rent in Texas is a critical financial analysis tool for real estate investors and property owners, as it helps determine the current value of anticipated rental income over a specific period. This process involves discounting future cash flows—in this case, rental payments—back to their present value using a predetermined discount rate, which accounts for factors like inflation, risk, and opportunity cost. In Texas, where the real estate market can vary significantly by region, understanding how to accurately compute NPV allows stakeholders to make informed decisions about property investments, lease agreements, or potential developments. Key considerations include local rental trends, property appreciation rates, and the unique economic landscape of Texas, ensuring the calculation reflects both the property’s potential and the broader market dynamics.

| Characteristics | Values |

|---|---|

| Discount Rate | Typically 5-10% (varies based on risk and market conditions) |

| Future Rent Growth Rate | 2-4% annually (based on Texas rental market trends) |

| Property Taxes | 2-3% of property value annually (varies by county in Texas) |

| Maintenance Costs | 1-4% of property value annually (depends on property age and condition) |

| Vacancy Rate | 5-8% (average for Texas rental market) |

| Lease Duration | Typically 12 months (standard in Texas) |

| Inflation Rate | ~2-3% annually (U.S. average, used for long-term projections) |

| Property Appreciation Rate | 3-5% annually (based on Texas real estate trends) |

| Formula for NPV | NPV = ∑ [ (Future Rent - Operating Costs) / (1 + Discount Rate)^t ] |

| Time Period (t) | Number of years in the projection (e.g., 5, 10, or 20 years) |

| Operating Costs | Includes property taxes, maintenance, vacancy, and other expenses |

| Texas-Specific Considerations | No state income tax, but higher property taxes in some areas |

| Data Sources | Texas Real Estate Center, U.S. Bureau of Labor Statistics, Local County Appraisal Districts |

| Software Tools | Excel, Google Sheets, or specialized real estate investment calculators |

| Legal Considerations | Texas Property Code governs landlord-tenant relationships |

| Market Volatility | Moderate; influenced by oil prices, population growth, and economic conditions |

Explore related products

What You'll Learn

![]()

Discount Rate Selection for Texas Real Estate Investments

When determining the Discount Rate Selection for Texas Real Estate Investments, it is crucial to understand that the discount rate is a key component in calculating the Net Present Value (NPV) of future rental income. The discount rate reflects the investor’s required rate of return, accounting for risk, inflation, and opportunity cost. In Texas, where real estate markets vary significantly across cities like Houston, Dallas, Austin, and San Antonio, selecting an appropriate discount rate requires careful analysis of local market conditions, property type, and investment horizon. A higher discount rate reduces the present value of future cash flows, making it essential to balance conservatism with realism.

To select a discount rate, start by benchmarking against the risk-free rate, typically the yield on U.S. Treasury bonds of a similar term. For Texas real estate, add a risk premium to account for market volatility, tenant risk, and property-specific factors. For example, multifamily properties in high-demand areas like Austin may warrant a lower risk premium compared to commercial properties in less stable markets. Additionally, consider the capitalization rate (cap rate), which is widely used in real estate valuation. While the cap rate reflects current market conditions, the discount rate should incorporate future expectations, including potential rent growth or economic downturns.

Another factor to consider is the Weighted Average Cost of Capital (WACC), especially for leveraged investments. In Texas, where financing options and interest rates vary, the WACC can provide a more comprehensive view of the cost of capital. However, for simplicity, many investors use a fixed discount rate based on historical returns or industry standards. For instance, a discount rate of 8-12% is commonly applied to Texas real estate investments, but this range should be adjusted based on property type, location, and market outlook.

Local economic indicators also play a significant role in discount rate selection. Texas’s robust economy, driven by energy, technology, and manufacturing sectors, can influence rental demand and property values. However, regional disparities exist; for example, Houston’s economy is closely tied to oil prices, while Austin benefits from tech industry growth. Incorporating these macroeconomic factors ensures the discount rate aligns with the specific risks and opportunities of the investment.

Finally, sensitivity analysis is a valuable tool for testing the robustness of your discount rate. By varying the discount rate within a reasonable range, investors can assess how changes impact the NPV of future rents. This approach helps identify a threshold where the investment remains viable, providing a buffer against unforeseen market shifts. In Texas, where real estate dynamics can change rapidly, such analysis is particularly important for long-term investments.

In summary, Discount Rate Selection for Texas Real Estate Investments requires a nuanced approach, blending market benchmarks, risk assessment, and local economic insights. By carefully choosing a discount rate, investors can accurately calculate the NPV of future rents and make informed decisions in Texas’s diverse and dynamic real estate market.

Rent Overpayment: Lease Terms and Tenant Rights

You may want to see also

Explore related products

![]()

Estimating Future Rental Income Growth Trends in Texas

Next, consider population trends, including migration patterns and demographic shifts. Texas has consistently been one of the fastest-growing states in the U.S., attracting residents from other states due to its affordability, job opportunities, and low tax environment. Urban centers like Austin, Dallas, and Houston are experiencing rapid population growth, which typically correlates with increased rental demand. However, it’s important to differentiate between markets, as smaller cities or rural areas may have different growth dynamics. Utilize data from the U.S. Census Bureau, Texas Demographic Center, and local real estate reports to project population-driven rental income growth.

Historical rental income data is another key component in estimating future trends. Analyze past rental growth rates in specific Texas markets to identify patterns and potential future trajectories. Tools like the Consumer Price Index (CPI) and local rent indices can provide benchmarks for inflation-adjusted growth. Additionally, consider supply-side factors, such as new construction rates and vacancy levels, which can impact rental prices. If new apartment complexes or single-family homes are being built at a rapid pace, this could temper rental growth, while limited supply in high-demand areas may drive rents upward.

To refine your estimates, incorporate qualitative factors such as local regulations, zoning laws, and government policies that could affect rental markets. For example, rent control measures or incentives for affordable housing development can influence future rental income potential. Similarly, infrastructure projects, such as public transportation expansions or new commercial developments, can enhance the desirability of certain neighborhoods, driving rental growth. Stay informed about Texas-specific legislative changes and urban planning initiatives that may impact the rental landscape.

Finally, use discounted cash flow (DCF) analysis to calculate the NPV of future rental income based on your growth estimates. Apply an appropriate discount rate that reflects the risk associated with Texas rental markets and the time value of money. Software tools or financial models can help automate these calculations, ensuring accuracy and consistency. By combining quantitative data with qualitative insights, you can develop a well-informed projection of future rental income growth in Texas, which is essential for making sound investment decisions and calculating the NPV of future rent streams.

Sue a Tenant for Unpaid Rent: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Tax Implications on Rental Property NPV in Texas

When calculating the Net Present Value (NPV) of future rental income for a property in Texas, it’s crucial to consider the tax implications, as they directly impact the cash flows used in the NPV calculation. Texas does not impose a state income tax, which simplifies the tax considerations compared to other states. However, federal income taxes still apply to rental income, and understanding these obligations is essential for an accurate NPV analysis. Rental income is taxed as ordinary income at the federal level, and deductible expenses such as mortgage interest, property taxes, maintenance, and depreciation can reduce the taxable income from the property.

Depreciation is a significant tax benefit for rental property owners in Texas, as it allows for a non-cash deduction that reduces taxable rental income. The IRS allows residential rental properties to be depreciated over 27.5 years using the straight-line method. This deduction reduces the tax liability associated with rental income, effectively increasing the after-tax cash flow used in the NPV calculation. For example, if a property is valued at $200,000 (excluding land value), the annual depreciation expense would be approximately $7,273 ($200,000 / 27.5 years). This amount is subtracted from rental income before calculating federal taxes.

Another tax consideration is the treatment of property taxes in Texas. Property taxes in Texas are among the highest in the U.S., and they are fully deductible as an expense against rental income. This deduction reduces the taxable rental income, thereby lowering the federal tax liability. For instance, if annual property taxes are $5,000, this amount is subtracted from the rental income before calculating the tax owed. When calculating NPV, it’s important to account for these deductions to accurately reflect the after-tax cash flows.

Capital gains tax is another critical factor when evaluating the NPV of a rental property in Texas. If the property is sold for a profit, the gain is subject to federal capital gains tax. However, if the property has been held for more than one year, the gain is taxed at a lower long-term capital gains rate. Additionally, rental property owners can defer capital gains taxes through a 1031 exchange, which allows reinvestment of proceeds into another like-kind property. This tax deferral strategy can significantly impact the NPV calculation by delaying tax liabilities and potentially increasing future cash flows.

Finally, it’s important to consider the impact of passive activity loss rules on the NPV calculation. The IRS limits the ability to deduct passive losses (such as rental property losses) against non-passive income unless the taxpayer is considered a real estate professional. However, unused passive losses can be carried forward to offset future passive income or gains. When calculating NPV, these rules must be factored in to ensure that the projected cash flows accurately reflect the tax treatment of rental income and expenses. By carefully accounting for these tax implications, investors can derive a more precise NPV for future rental income in Texas.

How Much Money Do You Need to Rent?

You may want to see also

Explore related products

![]()

Inflation Adjustments for Long-Term Rental Cash Flows

When calculating the Net Present Value (NPV) of future rental income in Texas, or any long-term investment, accounting for inflation is crucial. Inflation erodes the purchasing power of money over time, meaning that future cash flows will be worth less in real terms than they are today. To accurately assess the value of future rental income, you must adjust these cash flows for inflation. This involves estimating the future rental income in nominal terms (including inflation) and then discounting it back to present value using a real discount rate, or adjusting the cash flows to real terms first and then discounting them using a nominal discount rate.

The first step in making inflation adjustments is to forecast future rental income in nominal terms. This requires an understanding of historical rental growth rates in Texas and expectations for future inflation. For instance, if the current rental income is $1,000 per month and you expect rents to increase by 3% annually due to inflation and market conditions, you would project next year’s rent as $1,030. This process is repeated for each year of the investment horizon. However, simply projecting nominal cash flows is not enough; you must also ensure that the discount rate used in the NPV calculation aligns with these nominal cash flows.

To properly account for inflation, you can use either a nominal discount rate or a real discount rate. A nominal discount rate includes both the real rate of return and the expected inflation rate, whereas a real discount rate excludes inflation. If using a nominal discount rate, you would discount the nominal cash flows directly. For example, if the nominal discount rate is 7% (assuming 4% real return and 3% inflation), you would apply this rate to the nominal rental income projections. Alternatively, if using a real discount rate, you would first adjust the nominal cash flows to real terms by removing the inflation component and then discount them using the real rate.

Another approach is to use the Fisher equation, which relates nominal and real interest rates. The equation is: Nominal Rate = Real Rate + Inflation Rate + (Real Rate * Inflation Rate). This helps in breaking down the components of the discount rate and ensuring consistency between cash flow projections and the discount rate. For long-term rental cash flows in Texas, where inflation and rental growth rates may vary, this method provides a more precise way to align projections with economic realities.

Finally, sensitivity analysis is essential when adjusting for inflation, as both inflation rates and rental growth rates are uncertain. By testing different inflation scenarios—such as higher or lower inflation—you can assess how sensitive the NPV of future rents is to changes in inflation. This helps in making a more robust investment decision. For Texas-specific investments, consider regional economic trends, local inflation rates, and historical rental market data to refine your inflation adjustments and improve the accuracy of your NPV calculations.

Timing Your Rental Search: How Early Should You Start Looking?

You may want to see also

Explore related products

![Valuation Case Law 103: Lease Agreement Rent Reviews - A Study Guide to understanding Mahoney v RC Dimock Ltd - [1990] 3 NZLR 114](https://m.media-amazon.com/images/I/81eOPZIILVL._AC_UY218_.jpg)

![]()

Risk Assessment in Texas Rental Market NPV Calculations

When conducting Risk Assessment in Texas Rental Market NPV Calculations, it is essential to account for the inherent uncertainties that can impact the future cash flows of rental properties. Net Present Value (NPV) calculations rely on accurate projections of future rental income, expenses, and discount rates, all of which are subject to market fluctuations. In Texas, factors such as local economic conditions, employment rates, and population growth trends directly influence rental demand and property values. For instance, cities like Austin and Dallas have experienced rapid growth, but this also introduces risks such as oversupply or sudden economic downturns. To mitigate these risks, investors should incorporate sensitivity analyses into their NPV models, testing how changes in rental rates, vacancy rates, or operating expenses affect the overall investment viability.

Another critical aspect of Risk Assessment in Texas Rental Market NPV Calculations is the consideration of regulatory and legal risks. Texas has landlord-friendly laws, but changes in local ordinances, zoning regulations, or tenant protection measures can impact rental income and property management costs. For example, rent control policies, though rare in Texas, could emerge in high-demand areas, reducing potential revenue streams. Additionally, property taxes in Texas are relatively high compared to other states, and fluctuations in tax rates can significantly affect cash flows. Investors should factor these potential regulatory changes into their NPV calculations by assigning probability weights to different scenarios and adjusting discount rates accordingly.

Market volatility and interest rate risks also play a significant role in Risk Assessment in Texas Rental Market NPV Calculations. The discount rate used in NPV calculations is often tied to prevailing interest rates, which can fluctuate based on Federal Reserve policies and broader economic conditions. In a rising interest rate environment, the cost of financing rental properties increases, reducing the present value of future cash flows. Conversely, lower interest rates can make investments more attractive but may also signal economic uncertainty. To address this, investors should use a range of discount rates in their models, reflecting both optimistic and pessimistic interest rate scenarios, to ensure a robust risk assessment.

Physical and environmental risks are additional considerations in Risk Assessment in Texas Rental Market NPV Calculations. Texas is prone to natural disasters such as hurricanes, floods, and tornadoes, which can cause property damage and disrupt rental income. Insurance premiums for these risks can be high, and coverage may not fully offset potential losses. Climate change is also increasing the frequency and severity of these events, adding long-term uncertainty. Investors should include contingency reserves in their cash flow projections and consider the potential impact of environmental risks on property values and rental demand. Incorporating these factors into NPV calculations ensures a more comprehensive and realistic assessment of investment risk.

Finally, tenant-related risks, such as defaults and turnover, must be factored into Risk Assessment in Texas Rental Market NPV Calculations. While Texas has a strong rental market, economic downturns or shifts in local employment can lead to higher vacancy rates or late payments. Historical data on tenant turnover and default rates can be used to estimate these risks, but investors should also consider the quality of their tenant screening processes and lease agreements. By incorporating vacancy rates, collection losses, and leasing costs into cash flow projections, investors can create a more accurate NPV model that reflects the true risk profile of their rental property investments in Texas.

Renter's Insurance: Fish Tank Leaks Covered?

You may want to see also

Frequently asked questions

Net Present Value (NPV) is a financial metric used to determine the current value of future cash flows, discounted at a specific rate. For future rent in Texas, NPV calculates the present value of expected rental income over a period, accounting for factors like inflation, discount rates, and property-specific risks. It helps investors assess the profitability of rental properties.

The discount rate for NPV calculations typically reflects the opportunity cost of capital and the risk associated with the investment. For Texas rental properties, consider factors like local market volatility, inflation, and your required rate of return. A common approach is to use the risk-free rate (e.g., U.S. Treasury bond yield) plus a risk premium based on the property’s specifics.

Cash flow projections for NPV should include all expected income (rent) and expenses (maintenance, taxes, insurance, vacancies, etc.). For Texas, account for local property taxes, potential rent growth rates, and regional economic trends. Ensure projections are realistic and span the investment horizon, typically 5–10 years or more.