Claiming rent paid in your income tax return can be a valuable way to reduce your taxable income, especially if you are living in a rented property and meet certain eligibility criteria. In many countries, taxpayers are allowed to claim a deduction for the rent they pay under specific sections of the tax laws, such as Section 80GG in India, which is applicable if you are not receiving House Rent Allowance (HRA) from your employer. To claim this deduction, you typically need to provide details of your rent payments, including the amount paid, the landlord’s PAN (Permanent Account Number) or Aadhaar details, and the rent agreement. It’s important to ensure that you do not own any residential property in the location where you are working and that you are not claiming HRA elsewhere. Proper documentation and adherence to the tax regulations are crucial to successfully claiming this deduction and maximizing your tax savings.

| Characteristics | Values |

|---|---|

| Eligibility | Available for individuals who are salaried or self-employed and pay rent. |

| Section of the IT Act | Section 80GG (for non-HRA recipients) or Section 10(13A) (for HRA exemption). |

| Maximum Deduction (Section 80GG) | Least of: (a) Rent paid minus 10% of total income, (b) Rs. 5,000/month, (c) 25% of adjusted total income. |

| Conditions for Section 80GG | Taxpayer, spouse, or minor child should not own residential property in the place of employment/business. |

| HRA Exemption Calculation | Least of: (a) Actual HRA received, (b) Actual rent paid minus 10% of basic salary, (c) 50% of basic salary (metro cities) or 40% (non-metro). |

| Documents Required | Rent receipts, rent agreement, landlord’s PAN (if rent > Rs. 1 lakh/year). |

| Filing Requirement | Must file ITR to claim the deduction/exemption. |

| Applicability | Only for rented accommodations in India. |

| Non-Applicability | Not available if taxpayer owns a house at the workplace. |

| Tax Benefit Type | Deduction (Section 80GG) or Exemption (HRA). |

| Latest FY Applicability | FY 2023-24 (AY 2024-25). |

| Form for Reporting | ITR-1, ITR-2, or ITR-3, depending on income sources. |

| Carry Forward | Not applicable for HRA or Section 80GG. |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand who can claim rent paid as a deduction under income tax laws

- Documentation Required: Gather rent receipts, lease agreements, and payment proofs for filing

- Section 80GG: Claim deduction if HRA is not part of your salary

- Calculation Method: Learn how to compute deductible rent amount accurately

- Filing Process: Step-by-step guide to claim rent paid in ITR forms

![]()

Eligibility Criteria: Understand who can claim rent paid as a deduction under income tax laws

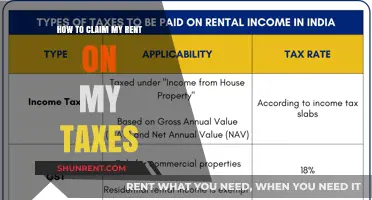

To claim rent paid as a deduction under income tax laws, it is essential to understand the eligibility criteria set forth by tax authorities. Primarily, this deduction is available to individuals who are salaried employees and are residing in rented accommodations. The provision falls under Section 80GG of the Income Tax Act in many jurisdictions, including India, which allows taxpayers to claim deductions on rent paid under certain conditions. It’s important to note that this benefit is applicable only if the taxpayer is not receiving House Rent Allowance (HRA) from their employer and does not own any residential property in the location where they are working and residing.

Another critical eligibility criterion is that the taxpayer must be paying rent for the accommodation. This means that the property should be leased or rented, and the taxpayer must be able to provide proof of the rent paid, such as rent receipts or lease agreements. Additionally, the rented property must be the taxpayer’s primary residence, and the rent paid should exceed 10% of their total income. This ensures that the deduction is claimed for genuine living expenses and not for secondary or vacation properties.

Taxpayers who own a residential property in any other place, whether it is self-occupied or let out, are not eligible to claim this deduction. This rule is in place to prevent individuals from claiming benefits for rent while simultaneously benefiting from ownership of another property. However, if the taxpayer owns a property in a different city from where they are employed and are living on rent in the city of employment, they can still claim the deduction under Section 80GG.

Furthermore, non-salaried individuals, such as freelancers or business owners, are also eligible to claim this deduction if they meet the specified conditions. They must not be in receipt of any HRA and should not own any residential property in the city where they reside. This ensures that the benefit is extended to a broader group of taxpayers who incur genuine rent expenses but do not fall under the salaried employee category.

Lastly, the quantum of deduction is subject to certain limits. The deduction is the least of the following: the rent paid minus 10% of the total income, 25% of the total income (for those residing in metropolitan cities), or Rs. 5,000 per month (in many jurisdictions). Taxpayers must calculate their eligibility based on these parameters to ensure compliance with tax laws. Understanding these eligibility criteria is crucial for accurately claiming rent paid as a deduction and maximizing tax savings.

Unlock Passive Income: Investing in Federal Rent Checks Explained

You may want to see also

Explore related products

![]()

Documentation Required: Gather rent receipts, lease agreements, and payment proofs for filing

When preparing to claim rent paid in your income tax return, gathering the right documentation is crucial. Start by collecting all rent receipts issued by your landlord for the financial year. These receipts should clearly mention the payment date, amount paid, and the period for which the rent is being paid. Ensure that the landlord’s name, address, and PAN (Permanent Account Number) are included, as this information is mandatory for claiming the deduction under Section 80GG of the Income Tax Act, if applicable. If your landlord does not provide receipts, request them formally, as they are essential for verification by tax authorities.

In addition to rent receipts, lease agreements play a vital role in substantiating your claim. The lease or rental agreement should clearly outline the terms of the tenancy, including the duration of the lease, monthly rent amount, and the property details. This document serves as proof of your tenancy and the legitimacy of the rent payments. If you have renewed your lease during the financial year, ensure you have copies of all relevant agreements to cover the entire period for which you are claiming the deduction.

Payment proofs are equally important to establish that the rent was actually paid. These can include bank statements showing rent transfers, canceled checks, or online payment receipts. If you pay rent in cash, ensure that the rent receipts are duly signed by the landlord and clearly indicate the mode of payment. For digital transactions, screenshots or transaction IDs can serve as additional proof. Cross-verify these payment proofs with the rent receipts to ensure consistency in dates and amounts.

Organize all these documents in a systematic manner to avoid discrepancies during filing. Keep both physical and digital copies for easy access and backup. If you are claiming House Rent Allowance (HRA) exemption, ensure that the rent receipts and lease agreement are submitted to your employer as well, as they may require these documents to process your HRA claim. For those claiming under Section 80GG, these documents will be needed when filing your tax return directly.

Lastly, double-check that all documents are legible, complete, and accurate. Incomplete or incorrect information can lead to delays or rejections in your tax filing process. By meticulously gathering and organizing rent receipts, lease agreements, and payment proofs, you ensure a smooth and hassle-free experience when claiming rent paid in your income tax return.

Village Walk of Bonita: Rental Population Insights and Trends

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Section 80GG: Claim deduction if HRA is not part of your salary

Section 80GG of the Income Tax Act is a crucial provision for individuals who do not receive House Rent Allowance (HRA) as part of their salary but still pay rent for their accommodation. This section allows taxpayers to claim a deduction for the rent paid, thereby reducing their taxable income. To avail this benefit, the taxpayer must fulfill certain conditions. Firstly, the taxpayer, their spouse, or minor child should not own any residential property at the place of employment or business. Additionally, the taxpayer must be residing in a rented property and paying rent for the same. This deduction is particularly beneficial for self-employed individuals, freelancers, and salaried employees whose salary structure does not include HRA.

The calculation of the deduction under Section 80GG is based on a specific formula, which is the least of three amounts. The first is the rent paid minus 10% of the taxpayer's total income. The second is Rs. 5,000 per month (Rs. 60,000 annually), and the third is 25% of the total income. For instance, if a taxpayer pays Rs. 15,000 per month as rent and has an annual income of Rs. 6 lakh, the deduction would be calculated as follows: Rent paid minus 10% of total income (Rs. 15,000 - Rs. 6,000 = Rs. 9,000), Rs. 5,000 per month, or 25% of Rs. 6 lakh (Rs. 1.5 lakh). The least of these amounts, which is Rs. 5,000 per month, would be the eligible deduction.

To claim the deduction under Section 80GG, taxpayers must file Form 10BA along with their income tax return. This form requires details such as the rent paid, the period of rent payment, and the address of the rented property. It is essential to maintain proper documentation, including rent receipts, rental agreements, and bank statements showing rent payments, as these may be required for verification by the tax authorities. Failure to provide accurate information or supporting documents could lead to the disallowance of the claim.

It is important to note that Section 80GG cannot be claimed if the taxpayer or their spouse receives HRA from any employer. Moreover, if the taxpayer owns a residential property at any other place, they are not eligible for this deduction. This provision ensures that only those who genuinely incur rent expenses without any other housing benefits can avail of this tax relief. Taxpayers should carefully assess their eligibility and compute the deduction accurately to maximize their tax savings while remaining compliant with the law.

In summary, Section 80GG is a valuable tool for individuals who pay rent but do not receive HRA. By understanding the eligibility criteria, calculation method, and documentation requirements, taxpayers can effectively claim this deduction and reduce their tax liability. It is advisable to consult a tax professional or refer to the latest guidelines from the Income Tax Department to ensure accurate and hassle-free filing.

Original Rent Cast's Historic Run: How Long Did They Perform?

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Calculation Method: Learn how to compute deductible rent amount accurately

To accurately compute the deductible rent amount for your income tax return, it's essential to understand the specific rules and limits set by tax authorities. The deductible rent amount is generally the portion of rent paid that can be claimed as a deduction against your taxable income, often applicable in scenarios like self-employment or when the rented property is used for business purposes. Here’s a step-by-step guide to calculating this amount accurately.

Step 1: Determine Eligibility

Before proceeding with calculations, confirm your eligibility to claim rent as a deduction. Typically, rent paid for a property used exclusively or partially for business or professional purposes qualifies. For instance, if you work from home, a portion of the rent corresponding to the workspace area may be deductible. Ensure you maintain proper documentation, such as rental agreements and utility bills, to substantiate your claim.

Step 2: Calculate the Proportionate Rent

If the rented property is used both for personal and business purposes, only the business portion of the rent is deductible. Measure the total area of the property and the area exclusively used for business. Divide the business area by the total area to find the proportionate percentage. Multiply this percentage by the total annual rent paid to determine the deductible amount. For example, if 20% of a 1,000 sq. ft. apartment is used for business, and the annual rent is ₹1,20,000, the deductible rent would be ₹24,000 (₹1,20,000 * 20%).

Step 3: Apply Statutory Limits

Tax laws often impose limits on the amount of rent that can be claimed as a deduction. For instance, in some jurisdictions, the deductible rent is capped at a certain percentage of the taxpayer’s income or a fixed amount. Refer to the latest tax regulations to ensure your calculation complies with these limits. Exceeding these caps may result in disallowed deductions.

Step 4: Maintain Proper Records

Accurate record-keeping is crucial for claiming rent deductions. Maintain receipts of rent payments, rental agreements, and any other relevant documents. If the property is shared, ensure clear segregation of expenses between personal and business use. In case of an audit, these records will serve as evidence to support your claim.

Step 5: Report Correctly in the Tax Return

Once the deductible rent amount is calculated, report it in the appropriate section of your income tax return. For self-employed individuals, this is typically under business or professional income. Ensure the amount is accurately entered to avoid discrepancies. Double-check the calculations and supporting documents before filing to ensure compliance with tax laws.

By following these steps, you can compute the deductible rent amount accurately and maximize your tax benefits while staying compliant with legal requirements. Always consult a tax professional if you’re unsure about any aspect of the calculation or eligibility criteria.

How Many Americans Rent Self-Storage Units Today?

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Filing Process: Step-by-step guide to claim rent paid in ITR forms

Step 1: Gather Required Documents and Information

Before starting the filing process, ensure you have all necessary documents and details. This includes rent receipts from your landlord, which must include their name, address, PAN (if rent exceeds ₹1 lakh annually), and the rent amount paid. Additionally, collect your Form 16 (if salaried), bank statements, and any other income-related documents. If you are claiming House Rent Allowance (HRA), ensure your employer has provided the HRA component in your salary structure. Verify the rent agreement and payment records to ensure accuracy, as discrepancies can lead to scrutiny.

Step 2: Calculate the Eligible Deduction

The deduction for rent paid is governed by Section 80GG of the Income Tax Act (for non-salaried individuals) or HRA exemption rules (for salaried individuals). For HRA, the exemption is the lowest of: (a) actual HRA received, (b) actual rent paid minus 10% of basic salary, or (c) 50% of basic salary (for metro cities) or 40% (for non-metro cities). For Section 80GG, the deduction is the lowest of: (a) rent paid minus 10% of total income, (b) ₹5,000 per month, or (c) 25% of total income. Use these formulas to calculate the eligible amount before proceeding to the ITR form.

Step 3: Fill the Relevant Sections in ITR Forms

Open the ITR form applicable to your income (e.g., ITR-1 for salaried individuals). Navigate to the "Income Details" section and locate the field for "House Property Income" or "HRA" under salaries. If claiming HRA, enter the exempt amount calculated in Step 2 under the HRA section. For Section 80GG, go to the "Deductions" section and fill the details under Section 80GG, providing the rent paid, landlord’s PAN (if applicable), and other required information. Ensure all fields are accurately filled to avoid errors.

Step 4: Validate and Submit the ITR

After filling the necessary details, review the form for accuracy. Cross-check the rent paid, deductions claimed, and other income details. Use the ITR utility’s validation feature to ensure there are no errors. Once verified, submit the ITR electronically. If claiming HRA, ensure your employer has considered it while deducting TDS. For Section 80GG, attach the rent receipts and Form 10BA (declaration form) if required. After submission, e-verify the return using Aadhaar OTP, net banking, or other available methods to complete the process.

Step 5: Retain Records for Future Reference

After filing, keep all rent receipts, rent agreements, bank statements, and ITR acknowledgment safely for at least six years. These documents may be required in case of an income tax assessment or scrutiny. Maintaining organized records ensures a hassle-free process if the tax department seeks verification of your claims. Regularly update your rent payment records to streamline future filings.

The Cost of Renting a Plane: What to Expect

You may want to see also

Frequently asked questions

Yes, you can claim rent paid as a deduction under Section 80GG of the Income Tax Act, but only if you are a salaried individual, a self-employed person, or a business owner who does not receive House Rent Allowance (HRA) and does not own a residential property in the city where you reside.

To claim rent paid, you need to provide the rent agreement, rent receipts from the landlord, and the landlord’s PAN (if rent exceeds ₹1 lakh annually). Additionally, proof of residence and payment (like bank statements) may be required.

Yes, the deduction under Section 80GG is subject to certain limits: the least of (a) rent paid minus 10% of your total income, (b) ₹5,000 per month, or (c) 25% of your total income.

No, you cannot claim rent paid to parents under Section 80GG, as the Income Tax Department does not consider such transactions as valid rent payments for deduction purposes.

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)