Collecting rent money tax-free involves understanding and leveraging specific legal strategies and structures to minimize tax liabilities. One common approach is utilizing a 1031 exchange, which allows landlords to defer capital gains taxes by reinvesting rental income into like-kind properties. Another method is establishing a self-directed IRA or a real estate investment trust (REIT), which can provide tax advantages through deductions, deferrals, or exemptions. Additionally, properly categorizing expenses, such as maintenance, repairs, and property management fees, can reduce taxable rental income. Consulting with a tax professional or financial advisor is essential to ensure compliance with IRS regulations and to tailor strategies to individual circumstances.

Explore related products

$17.97 $17.97

What You'll Learn

![]()

Utilize 1031 Exchange for Rental Properties

A 1031 exchange, named after Section 1031 of the U.S. Internal Revenue Code, allows real estate investors to defer capital gains taxes when selling an investment property by reinvesting the proceeds into a similar property. This strategy can be particularly advantageous for rental property owners looking to collect rent money tax-free, as it effectively postpones tax liabilities, allowing for greater cash flow and investment growth. By leveraging a 1031 exchange, landlords can sell a rental property, reinvest the proceeds into a new property, and continue generating rental income without immediately facing a tax burden on the capital gains from the sale.

To execute a 1031 exchange for rental properties, follow these steps: First, identify a replacement property within 45 days of selling the original property. This identification must be in writing and submitted to a qualified intermediary, who facilitates the exchange. Next, complete the purchase of the replacement property within 180 days of the sale. The replacement property must be of "like-kind," meaning it should be similar in nature or character to the original property, though it does not need to be identical. For example, exchanging a residential rental property for a commercial rental property qualifies, as both are held for investment purposes.

One critical aspect of a 1031 exchange is the role of the qualified intermediary. This neutral third party holds the proceeds from the sale of the original property and ensures compliance with IRS rules. The intermediary cannot be a disqualified person, such as a family member or business partner, and must be designated before the sale of the original property is completed. Working with an experienced intermediary is essential to avoid common pitfalls, such as missing deadlines or mishandling funds, which can disqualify the exchange and trigger immediate tax liabilities.

While a 1031 exchange offers significant tax advantages, it is not without limitations. For instance, the exchange must be for investment or business use properties, not personal residences. Additionally, the full amount of the sale proceeds must be reinvested into the replacement property to defer all capital gains taxes. If only a portion is reinvested, the remaining amount, known as "boot," will be subject to taxation. Investors should also consider the long-term implications, as deferring taxes means they will eventually be due if the property is sold outside of another 1031 exchange.

In conclusion, utilizing a 1031 exchange for rental properties is a powerful strategy for collecting rent money tax-free by deferring capital gains taxes. By carefully following IRS guidelines, working with a qualified intermediary, and reinvesting the full proceeds into a like-kind property, investors can maximize cash flow and grow their real estate portfolios more efficiently. While the process requires meticulous planning and adherence to strict timelines, the tax benefits make it a valuable tool for savvy rental property owners.

Rent Relief: A Step-by-Step Guide to Securing a Rental Loan

You may want to see also

Explore related products

![]()

Depreciate Property Value to Offset Income

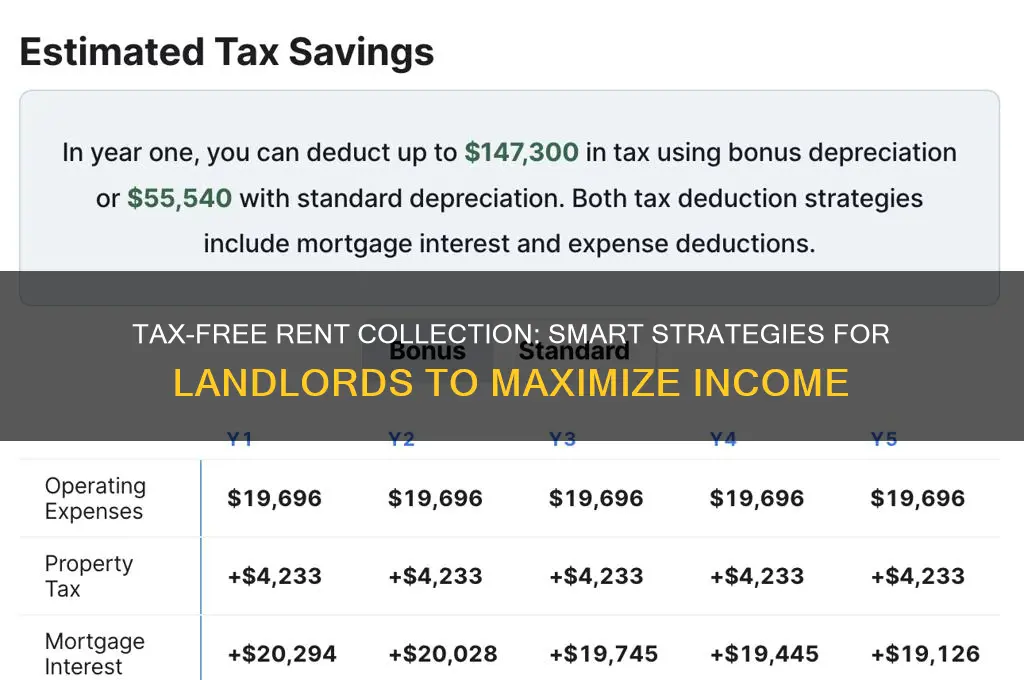

Real estate investors often overlook a powerful tool for reducing taxable rental income: depreciation. The IRS allows you to deduct the cost of purchasing residential rental property over 27.5 years, effectively lowering your taxable income each year. This isn’t a cash expense—it’s a paper deduction that reflects the property’s theoretical wear and tear. For example, if you buy a $300,000 rental property (excluding land value), you can deduct approximately $10,909 annually ($300,000 / 27.5). This reduces your taxable rental income by that amount, potentially saving thousands in taxes annually.

To maximize this strategy, separate the land value from the building value when claiming depreciation. Land doesn’t depreciate, so only the building’s cost qualifies. If you’re unsure how to allocate these values, consult a property tax assessment or hire an appraiser. Additionally, use the straight-line depreciation method, which spreads the deduction evenly over 27.5 years. While other methods like MACRS (Modified Accelerated Cost Recovery System) exist, they’re more complex and typically used for commercial properties. Stick to simplicity unless advised otherwise by a tax professional.

One common mistake is failing to recapture depreciation when selling the property. The IRS requires you to pay a 25% tax on all depreciation claimed during ownership, known as depreciation recapture. However, you can defer this tax by reinvesting the proceeds into another rental property through a 1031 exchange. This allows you to continue deferring taxes while scaling your real estate portfolio. Proper planning ensures you benefit from depreciation now without a hefty tax bill later.

Depreciation isn’t just for high-value properties—it’s equally effective for smaller investments. For instance, if you own a $150,000 duplex, your annual depreciation deduction would be around $5,455. Even modest rental properties can generate significant tax savings over time. Keep detailed records of all improvements, as certain upgrades (e.g., new HVAC systems or roof replacements) can be depreciated separately over 15 years, further reducing taxable income.

In practice, combining depreciation with other tax strategies amplifies its impact. For example, pair it with expense deductions like maintenance, property management fees, and mortgage interest to minimize taxable rental income. If your property operates at a paper loss due to these deductions, you may offset up to $25,000 of other passive income annually (subject to income limits). This makes depreciation a cornerstone of tax-efficient rental property management, turning a theoretical expense into tangible savings.

Rent Payments: Cash Flow Statement Impact

You may want to see also

Explore related products

![]()

Set Up a Self-Directed IRA for Rentals

A self-directed IRA allows you to invest in alternative assets like rental properties, offering a tax-advantaged way to collect rent. Unlike traditional IRAs limited to stocks and bonds, self-directed IRAs give you control over investment choices, including real estate. This strategy can shield your rental income from immediate taxation, letting it grow tax-deferred or tax-free, depending on whether you have a traditional or Roth IRA.

Setting up a self-directed IRA for rentals involves several steps. First, choose a custodian specializing in self-directed IRAs, as not all custodians handle real estate investments. Next, fund your IRA through contributions, transfers, or rollovers from existing retirement accounts. Once funded, identify a rental property that aligns with your investment goals. The IRA, not you personally, must purchase the property, so all transactions—from the down payment to maintenance costs—must come from the IRA funds.

One critical rule to remember is the prohibition on self-dealing. You cannot personally benefit from the property while it’s owned by the IRA. This means no vacationing at your rental property or doing repairs yourself for free. All income, including rent, must go directly into the IRA, and expenses must be paid from IRA funds. Violating these rules can result in penalties and disqualification of the IRA’s tax benefits.

Despite the restrictions, the tax advantages are significant. In a traditional self-directed IRA, rental income grows tax-deferred until withdrawal in retirement, potentially at a lower tax rate. With a Roth IRA, income grows tax-free, and qualified distributions are tax-free in retirement. Additionally, property appreciation within the IRA is shielded from capital gains taxes, maximizing long-term growth.

Before diving in, consider the complexities and costs. Self-directed IRAs require careful management, and custodians often charge higher fees than traditional IRA providers. Maintenance, repairs, and property management must align with IRS rules, adding administrative burdens. However, for those willing to navigate these challenges, a self-directed IRA for rentals can be a powerful tool to collect rent money tax-free while building wealth for retirement.

Adding Bots to Your Rented Server: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Leverage Tax Deductions for Rental Expenses

Rental property owners often overlook the myriad of tax deductions available to them, effectively leaving money on the table. By strategically leveraging these deductions, landlords can significantly reduce their taxable rental income, thereby keeping more of their hard-earned rent money. The key lies in understanding which expenses qualify and how to properly document them. From mortgage interest and property taxes to maintenance costs and depreciation, each deduction plays a crucial role in maximizing tax efficiency.

Consider the depreciation deduction, a powerful yet underutilized tool. Unlike other expenses, depreciation allows landlords to recover the cost of their property over time, even as it appreciates in value. For residential properties, the IRS allows a depreciation period of 27.5 years, while commercial properties are depreciated over 39 years. For instance, if you own a rental property valued at $200,000 (excluding land value), you could claim a yearly depreciation deduction of approximately $7,273 ($200,000 / 27.5). This reduces your taxable rental income without requiring an actual cash outlay, making it a highly effective strategy for tax minimization.

Another often-overlooked area is the deduction for repairs and maintenance. While improvements (e.g., adding a new room) must be capitalized and depreciated over time, repairs (e.g., fixing a leaky roof) can be deducted in full the year they are incurred. Keep detailed records of all maintenance activities, including receipts and invoices, to substantiate these claims. For example, if you spend $2,500 on plumbing repairs in a year, this amount directly reduces your taxable rental income, providing immediate tax relief.

To maximize these deductions, landlords should adopt a proactive approach to expense tracking. Use accounting software tailored for rental properties to categorize expenses accurately and generate year-end reports. Additionally, consult a tax professional to ensure compliance with IRS regulations and identify deductions you might have missed. By staying organized and informed, you can transform rental expenses into valuable tax savings, effectively collecting more of your rent money tax-free.

Discover Top Boat Rental Spots in Ruan's Trails of Sky

You may want to see also

![]()

Use a Real Estate Professional Tax Status

Real estate investors often overlook the Real Estate Professional (REP) tax status, a powerful tool for minimizing taxes on rental income. To qualify, you must spend more than 50% of your working hours and at least 750 hours annually on real estate activities, such as property management, leasing, or maintenance. This status allows you to deduct rental losses against ordinary income, bypassing the passive activity loss rules that typically limit deductions. For example, if you manage three rental properties and spend 25 hours per week on related tasks, you could meet the hourly requirement while potentially saving thousands in taxes.

Qualifying for REP status isn’t just about logging hours—it’s about strategic documentation. Keep detailed records of your time spent on real estate activities, including dates, tasks, and durations. Tools like time-tracking apps or spreadsheets can streamline this process. Additionally, ensure your activities are material and ongoing; sporadic repairs or infrequent tenant check-ins won’t suffice. For instance, if you handle tenant screening, lease negotiations, and property inspections regularly, these tasks count toward your hours. However, passive investments like owning REITs or holding land do not qualify.

One common misconception is that REP status requires a real estate license. This is false—anyone can qualify as long as they meet the time requirements. However, this status isn’t a one-size-fits-all solution. If your rental income is minimal or your non-real estate income is high, the benefits may be limited. For example, a high-earning doctor who spends 750 hours on rentals might still face limitations on deducting losses due to adjusted gross income thresholds. Always consult a tax professional to assess whether pursuing REP status aligns with your financial goals.

A key advantage of REP status is its ability to transform rental losses into active deductions, reducing your overall tax liability. For instance, if your rental properties generate a $20,000 loss and you qualify as an REP, you can offset this against other income, such as wages or business profits. Without this status, the loss would be suspended and carried forward indefinitely. To maximize this benefit, consider bundling multiple properties under one LLC and actively managing them to meet the hourly requirements. This approach not only streamlines operations but also strengthens your case for REP classification.

Finally, beware of pitfalls when pursuing REP status. The IRS scrutinizes claims closely, so ensure your records are accurate and consistent. Spouses can combine hours if filing jointly, but each must individually meet the 750-hour threshold. For example, if one spouse spends 500 hours and the other spends 300, neither qualifies unless their roles are clearly defined and documented. Additionally, if you fail to meet the requirements in a given year, you’ll lose the ability to deduct losses retroactively. Proactive planning and meticulous record-keeping are essential to maintaining this tax-saving status.

Essential NYC Lease Discussions: Key Topics Before Signing Your Rental Agreement

You may want to see also

Frequently asked questions

No, rent collected from a personal residence is generally taxable income unless it qualifies for specific exemptions, such as the rent-a-room scheme in some countries, which allows a limited tax-free income from renting out a room.

Reinvesting rent money into property maintenance or improvements does not make the rent tax-free. However, these expenses can be deducted from your taxable rental income, reducing your overall tax liability.

Transferring property to a family member does not automatically make rent tax-free. The recipient may still be liable for taxes on the rental income, and the transfer itself could trigger capital gains tax or gift tax, depending on local laws.

While trusts or LLCs can help manage rental properties, they do not inherently make rent tax-free. The structure may offer tax benefits, such as pass-through taxation or deductions, but the rent itself remains taxable income unless it falls under specific tax exemptions or incentives.