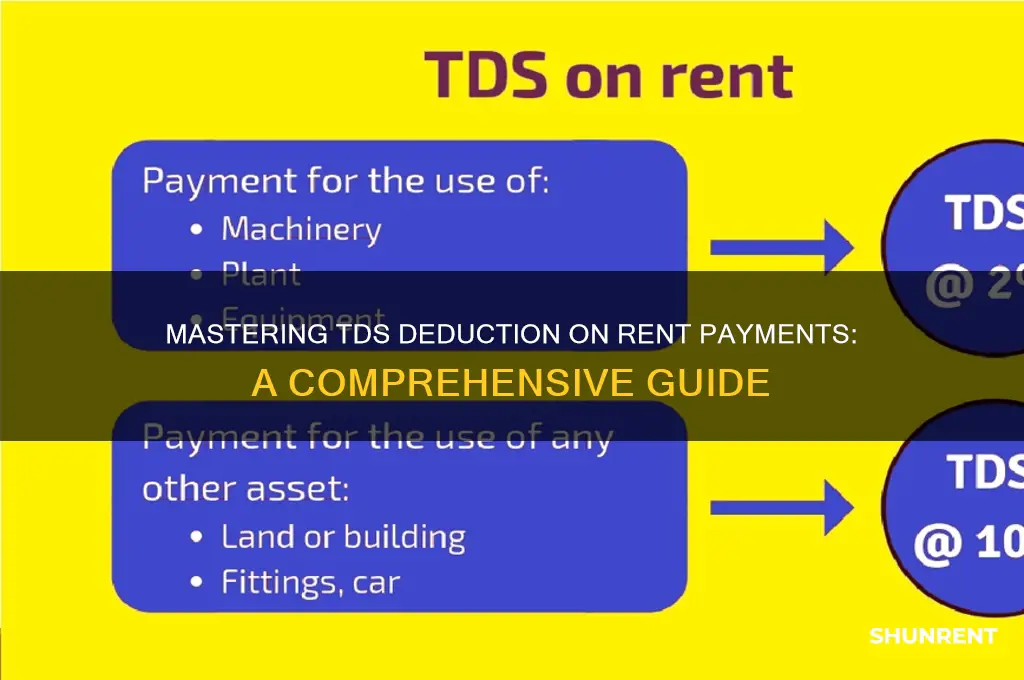

Deducting Tax Deducted at Source (TDS) on rent payments is a crucial compliance requirement under the Indian Income Tax Act, 1961, applicable when the monthly rent exceeds ₹50,000. As per Section 194-I, the tenant or payer is obligated to deduct TDS at a rate of 10% (or applicable rates as per the tenant’s status) before making the payment to the landlord. This deduction must be made irrespective of whether the landlord provides a PAN, though the rate increases to 20% if PAN is not furnished. The tenant is required to obtain a TAN (Tax Deduction Account Number) to remit the TDS and file quarterly returns in Form 26Q. Failure to comply may result in penalties, interest, and legal consequences. Understanding the process, including proper documentation, timely deposits, and issuance of Form 16A to the landlord, is essential for both parties to ensure adherence to tax regulations.

| Characteristics | Values |

|---|---|

| Applicable Section | Section 194-I of the Income Tax Act, 1961 |

| Threshold Limit | TDS is applicable if rent paid exceeds ₹2,40,000 in a financial year |

| TDS Rate | 10% of the rent amount (excluding tax, if any) |

| PAN Requirement | Mandatory to obtain PAN of the landlord; else, TDS rate increases to 20% |

| Deductor Responsibility | Tenant (individual or HUF) if rent exceeds ₹50,000 per month |

| Due Date for Deposit | 7th of the following month in which TDS is deducted |

| Due Date for Return Filing | Quarterly (Form 26Q): On or before 30th April, 30th June, 30th Sept, 31st Dec |

| Certificate Issuance | Form 16C to be issued by the tenant to the landlord |

| Penalty for Non-Deduction | Equal to the amount of TDS not deducted or deposited |

| Interest on Late Deposit | 1% per month or part thereof under Section 201(1A) |

| Applicability to NRI Landlords | TDS rate is 30% (or as per DTAA) unless lower withholding certificate is obtained |

| Exemptions | No TDS if rent is paid for agricultural land or by non-taxable entities |

| Form for Challan | Challan ITNS 281 to deposit TDS with the government |

| TAN Requirement | Tenant must obtain TAN if liable to deduct TDS |

| Revision in TDS | Can be revised if incorrect TDS is deducted (subject to conditions) |

| Refund Process | Landlord can claim refund by filing ITR if excess TDS is deducted |

| Latest Update (AY 2024-25) | No changes in TDS rate or threshold limit as per recent budget |

Explore related products

What You'll Learn

- Understanding TDS Rates: Different rates apply based on tenant type and rent amount

- Form 16: Issuing Form 16 to tenants after TDS deduction is mandatory

- Due Dates: TDS must be deposited by the 7th of the next month

- PAN Requirement: Tenant’s PAN is compulsory for TDS deduction and reporting

- Exemptions: No TDS if rent is below ₹2.4 lakh annually or tenant is HUF

![]()

Understanding TDS Rates: Different rates apply based on tenant type and rent amount

Tax Deducted at Source (TDS) on rent payments in India is not a one-size-fits-all scenario. The rate you apply hinges on two critical factors: the type of tenant and the annual rent amount. Understanding these nuances is crucial for landlords to ensure compliance and avoid penalties.

Let’s break it down.

For individual and Hindu Undivided Family (HUF) tenants, the TDS rate is 10% if the annual rent exceeds ₹2,40,000. For instance, if a tenant pays ₹20,000 per month, the annual rent totals ₹2,40,000, and no TDS is applicable. However, if the rent increases to ₹25,000 monthly, the annual amount becomes ₹3,00,000, triggering a TDS deduction of ₹6,000 (10% of ₹60,000 exceeding the threshold). This calculation requires landlords to monitor rent thresholds closely and adjust TDS deductions accordingly.

Corporate tenants face a different rule. Regardless of the rent amount, TDS is deducted at 10%. This flat rate simplifies the process for landlords dealing with businesses, as they don’t need to track annual rent thresholds. For example, a corporate tenant paying ₹1,50,000 annually would still attract a TDS of ₹15,000. This uniformity, however, underscores the importance of correctly identifying the tenant type to apply the right rate.

Non-resident Indian (NRI) tenants are subject to a higher TDS rate of 30% on rent payments, unless they provide a Tax Deduction Account Number (TAN) and comply with specific conditions. This rate can be reduced under the provisions of a Double Taxation Avoidance Agreement (DTAA) between India and the tenant’s country of residence. Landlords must verify the tenant’s status and applicable treaties to ensure accurate TDS deductions, as errors can lead to legal complications.

Practical tips for landlords include maintaining detailed rent records, obtaining PAN details from tenants, and filing TDS returns quarterly. Using accounting software can streamline these tasks, ensuring timely and accurate deductions. Additionally, landlords should educate themselves on recent amendments to TDS rules, as rates and thresholds are subject to change. By staying informed and organized, landlords can navigate the complexities of TDS on rent payments with confidence.

Gary Coleman's Age in 'Different Strokes': A Surprising Revelation

You may want to see also

Explore related products

$18.4

![]()

Form 16: Issuing Form 16 to tenants after TDS deduction is mandatory

Landlords often overlook a critical step after deducting TDS on rent: issuing Form 16 to their tenants. This document, mandated by the Income Tax Act, serves as proof of tax deducted at source and is essential for tenants to claim credit while filing their returns. Failure to provide it can lead to penalties for the landlord and complications for the tenant.

The process begins with accurate TDS deduction. For rent exceeding ₹50,000 per month, landlords must deduct 10% TDS under Section 194-I. This requires obtaining the tenant’s PAN details and depositing the deducted amount with the government using Form 26QC. Once the payment is made, the landlord receives a certificate, which forms the basis for generating Form 16.

Issuing Form 16 is not just a formality; it’s a legal obligation. This document details the rent paid, TDS deducted, and the tenant’s PAN, enabling them to adjust their tax liability. Landlords can generate Form 16 through the income tax portal using their login credentials. It’s advisable to issue it annually, preferably by May 31 following the financial year in which TDS was deducted.

Tenants should verify the accuracy of Form 16, ensuring the TDS amount matches their records. Any discrepancies must be rectified promptly by the landlord. For landlords, maintaining proper documentation, including rent agreements and TDS payment receipts, is crucial to avoid disputes.

In summary, issuing Form 16 after TDS deduction is a non-negotiable responsibility for landlords. It not only ensures compliance with tax laws but also fosters transparency and trust in the landlord-tenant relationship. Ignoring this step can have far-reaching consequences, making it imperative to prioritize this process.

Returning Rented Books on Amazon: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Due Dates: TDS must be deposited by the 7th of the next month

The 7th of the next month is a critical deadline for landlords and tenants alike when it comes to TDS (Tax Deducted at Source) on rent payments. Missing this due date can result in penalties, interest charges, and unnecessary complications with tax authorities. Understanding this timeline is essential for compliance and financial planning.

From a procedural standpoint, the process begins with the deduction of TDS at the time of rent payment. For instance, if rent is paid on the 25th of March, the TDS must be deducted immediately. However, the deposit deadline isn’t tied to the payment date but rather to the month in which the payment is made. In this example, the TDS must be deposited by the 7th of April. This distinction is crucial, as it allows for a consistent and predictable schedule, regardless of when rent is paid during the month.

A common mistake is assuming that the 7th-day rule applies only to the month in which the TDS is deducted. This misunderstanding can lead to delays and penalties. For example, if TDS is deducted in March but deposited after the 7th of April, the taxpayer is liable for interest at 1.5% per month or part of a month until the payment is made. To avoid this, set reminders or automate payments through online tax portals, ensuring the deposit is made within the stipulated timeframe.

Comparatively, other tax deadlines, such as income tax returns, often allow for extensions or grace periods. The TDS deposit deadline, however, is rigid. This strictness underscores its importance in the tax collection system, as it ensures a steady flow of revenue for the government. For landlords, especially those managing multiple properties, maintaining a calendar specifically for TDS deposits can prevent oversights. Tenants, on the other hand, should verify that their landlords are compliant, as the responsibility for TDS deduction and deposit ultimately lies with the payer.

In practice, here’s a step-by-step approach to ensure timely TDS deposit: first, calculate the TDS amount (10% of rent exceeding ₹50,000 per month for individuals and HUFs under Section 194-I). Second, deduct the TDS at the time of rent payment. Third, use Form 26QC to furnish details of the TDS deduction online. Finally, deposit the TDS by the 7th of the next month using the challan generated. By following these steps, both parties can ensure compliance and avoid unnecessary financial strain.

Churches Renting Schools: A Guide to Shared Space Partnerships

You may want to see also

Explore related products

![]()

PAN Requirement: Tenant’s PAN is compulsory for TDS deduction and reporting

In the realm of rent payments, the Permanent Account Number (PAN) is a critical piece of information that landlords must obtain from their tenants to comply with tax regulations. The Income Tax Department in India mandates that landlords deduct Tax Deducted at Source (TDS) on rent payments exceeding ₹50,000 per month, and this requires the tenant's PAN. Failure to provide the PAN can result in the landlord being liable to deduct TDS at a higher rate of 20% instead of the usual 10%, as per Section 206AA of the Income Tax Act. This underscores the importance of tenants furnishing their PAN details to avoid unnecessary financial burden on both parties.

From a procedural standpoint, the process of obtaining and using the tenant's PAN is straightforward yet crucial. Landlords should request the PAN at the time of finalizing the rental agreement. Once obtained, the PAN must be quoted in the TDS return (Form 26QC) that the landlord files quarterly. This form details the rent paid, TDS deducted, and the tenant's PAN, ensuring transparency and compliance. It’s essential to verify the PAN’s authenticity through the Income Tax Department’s portal to avoid errors or potential penalties. Tenants should be informed that their PAN is not just a formality but a legal requirement for accurate tax reporting.

A comparative analysis reveals that the PAN requirement serves dual purposes: it ensures tenants’ income from rent is correctly reported to the tax authorities, while also protecting landlords from higher TDS rates. For instance, if a tenant pays ₹60,000 per month and fails to provide their PAN, the landlord must deduct ₹12,000 (20%) as TDS instead of ₹6,000 (10%). This discrepancy highlights the financial implications of non-compliance. In contrast, when the PAN is provided, the process is seamless, and both parties benefit from adhering to the legal framework.

Practically, tenants should keep their PAN details handy and share them promptly when requested. Landlords, on the other hand, should integrate PAN collection into their rental agreement process and maintain accurate records. A useful tip is to include a clause in the rental agreement explicitly stating the tenant’s obligation to provide their PAN. Additionally, landlords can use digital tools or accounting software to automate TDS calculations and filings, reducing the risk of errors. By treating the PAN requirement as a non-negotiable aspect of rent transactions, both parties can ensure smooth financial operations and avoid legal complications.

Rent-A-Center Arbitration: Process, Rights, and What Tenants Should Know

You may want to see also

![]()

Exemptions: No TDS if rent is below ₹2.4 lakh annually or tenant is HUF

Under the Indian Income Tax Act, not all rent payments require TDS (Tax Deducted at Source) deductions. Understanding the exemptions can save both landlords and tenants from unnecessary tax complications. One key exemption is that no TDS is required if the annual rent paid is below ₹2.4 lakh. This threshold is crucial because it simplifies tax compliance for smaller-scale rentals, such as single-room accommodations or modest properties. For instance, if a tenant pays ₹20,000 per month, the annual rent totals ₹2.4 lakh, which falls exactly on the threshold. However, if the rent is ₹19,999 monthly, the annual amount is ₹2.39988 lakh, making it exempt from TDS. This exemption is particularly beneficial for students, young professionals, or low-income tenants who rent affordable properties.

Another exemption applies when the tenant is a Hindu Undivided Family (HUF). In such cases, TDS on rent is not applicable, regardless of the rent amount. This rule stems from the HUF’s unique legal status as a separate taxable entity. For example, if a HUF rents a commercial property for ₹5 lakh per month, the landlord is not obligated to deduct TDS. However, it’s essential for landlords to verify the tenant’s HUF status through proper documentation, such as the HUF’s PAN card or a declaration from the Karta (head of the HUF). Misidentifying a tenant as a HUF without valid proof can lead to tax penalties for the landlord.

Landlords must exercise caution when applying these exemptions. For the ₹2.4 lakh threshold, ensure the rent calculation includes all components, such as advance payments or maintenance charges treated as rent. For instance, if a tenant pays ₹1 lakh as a refundable security deposit and ₹1.5 lakh annually as rent, the total does not exceed ₹2.4 lakh, making it exempt. However, if the security deposit is non-refundable and treated as rent, the total might cross the threshold, triggering TDS obligations. Similarly, when dealing with HUF tenants, landlords should avoid assumptions and request formal proof of the HUF’s existence to avoid compliance issues.

Practical tips for landlords include maintaining detailed rent records, including monthly receipts and annual summaries, to easily verify eligibility for exemptions. Tenants, especially those paying below ₹2.4 lakh annually, should remind landlords of the exemption to avoid unnecessary TDS deductions. For HUF tenants, providing the necessary documentation upfront can streamline the rental process. Both parties should stay updated on tax regulations, as thresholds and rules may change periodically. By leveraging these exemptions correctly, landlords and tenants can reduce administrative burdens and ensure compliance with tax laws.

San Diego vs. New York: Which City Has Higher Rent?

You may want to see also

Frequently asked questions

The threshold limit for deducting TDS on rent payment is ₹2,40,000 per annum for individuals and HUFs. If the rent paid exceeds this limit, TDS must be deducted at the rate of 10%.

The person making the rent payment, whether an individual, HUF, or entity, is responsible for deducting TDS if the rent exceeds the threshold limit of ₹2,40,000 per annum.

The rate of TDS on rent payment under Section 194-I is 10% for both individuals and non-individuals, provided the rent exceeds the threshold limit of ₹2,40,000 per annum.

No, TDS on rent payment need not be deducted if the tenant is an individual or HUF and the rent paid is below the threshold limit of ₹2,40,000 per annum. TDS is only applicable when the rent exceeds this limit.