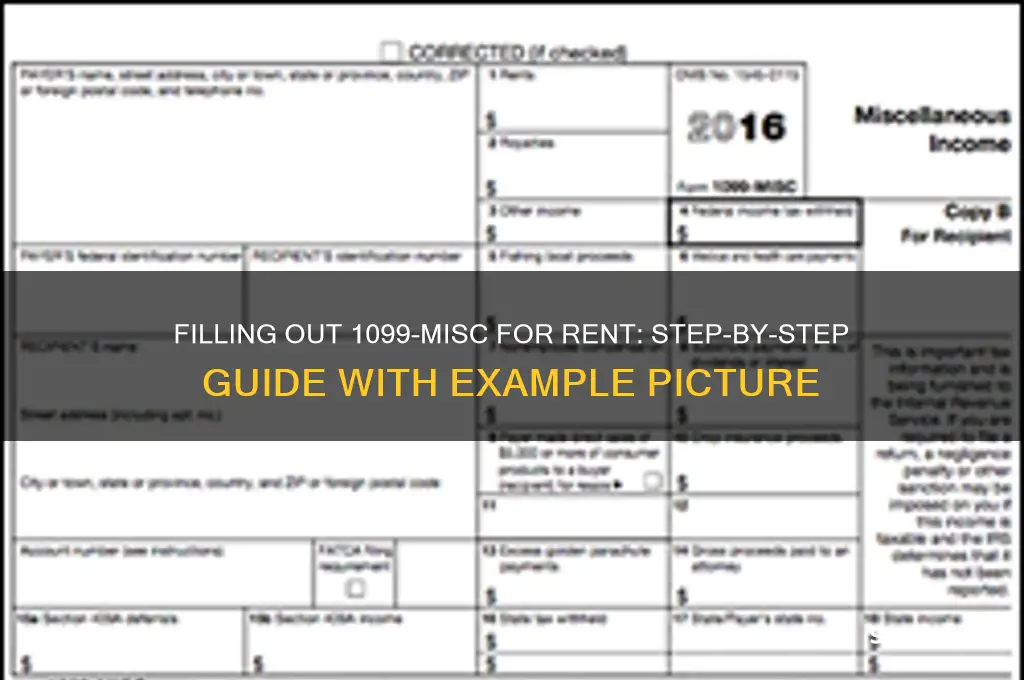

Filling out a 1099-MISC form for rent payments can be a straightforward process, but it requires attention to detail to ensure compliance with IRS regulations. For instance, if you’re a landlord who paid a property manager or contractor $600 or more during the tax year for services related to your rental property, you’ll need to report this on a 1099-MISC. An example picture of a completed form can serve as a helpful guide, showing where to enter the recipient’s name, address, and Taxpayer Identification Number (TIN), as well as the total amount paid in Box 1 (Rents). It’s crucial to double-check all information for accuracy and ensure the form is filed by the IRS deadline, typically January 31st for the recipient and February 28th (or March 31st if filing electronically) for the IRS. This ensures both parties meet their tax obligations and avoid potential penalties.

Explore related products

What You'll Learn

- Landlord/Tenant Information: Include names, addresses, and TINs for both parties on the 1099-MISC form

- Rent Payment Details: Report total rent paid during the tax year in Box 1 (Rents)

- Box 2-7 Instructions: Leave these boxes blank unless other payments apply (e.g., royalties)

- Copy Distribution: Provide Copy B to tenant, Copy C to state, and keep Copy A

- Filing Deadlines: Submit to IRS by January 31 and tenant by the same date

![]()

Landlord/Tenant Information: Include names, addresses, and TINs for both parties on the 1099-MISC form

When filling out the 1099-MISC form for rent, the Landlord/Tenant Information section is critical as it identifies both parties involved in the rental transaction. Start by clearly entering the landlord’s name in the "Payer's name" field. This should match the legal name used for tax purposes. Directly below, input the landlord’s address, including the street, city, state, and ZIP code. Ensure accuracy, as this information is used by the IRS to verify the payer’s identity. If the landlord operates under a business name, include it here as well, but the primary focus should be on the individual or entity responsible for issuing the 1099-MISC.

Next, move to the tenant’s information, which is entered in the "Recipient's name" field. The tenant’s full legal name must be included, as it appears on their tax documents. Below the name, provide the tenant’s address, ensuring it is complete and accurate. This address is essential for the IRS to match the form with the recipient’s tax return. If the tenant uses a different mailing address, include it in the appropriate field to ensure the form reaches them correctly.

Both the landlord and tenant must provide their Taxpayer Identification Numbers (TINs) on the 1099-MISC form. For the landlord, this is typically their Social Security Number (SSN) or Employer Identification Number (EIN), depending on whether they operate as an individual or a business. For the tenant, their TIN is usually their SSN. Double-check these numbers for accuracy, as errors can result in processing delays or penalties. The TINs are located in specific fields on the form, so ensure they are entered in the correct boxes.

It’s important to note that the landlord is responsible for obtaining the tenant’s TIN before filling out the 1099-MISC. If the tenant fails to provide this information, the landlord may be subject to backup withholding. To avoid this, request the tenant’s TIN in advance, typically when the lease agreement is signed. Keep a record of this information for future reference and to ensure compliance with IRS regulations.

Finally, review the Landlord/Tenant Information section carefully before submitting the 1099-MISC form. Errors in names, addresses, or TINs can lead to complications for both parties. Once verified, provide a copy of the form to the tenant by January 31st and file it with the IRS by the specified deadline. Accurate and complete information in this section is essential for proper tax reporting and to avoid potential issues with the IRS.

Balancing Harvard Tuition and Rent: Smart Strategies for Affordability

You may want to see also

Explore related products

![]()

Rent Payment Details: Report total rent paid during the tax year in Box 1 (Rents)

When filling out Form 1099-MISC for rent payments, the primary focus is on accurately reporting the total rent paid during the tax year in Box 1 (Rents). This box is specifically designated for rent income received by the property owner or landlord. As a payer (typically the tenant or property manager), your responsibility is to ensure the amount reported here reflects the exact total of all rent payments made to the landlord or property owner during the calendar year. Start by gathering all rent payment records, including receipts, lease agreements, or bank statements, to verify the total amount paid.

To report the rent payment details, sum up every rent payment made to the landlord or property owner throughout the year. This includes monthly rent payments, as well as any additional rent-related payments such as lease renewal fees or rent increases, provided they are explicitly for rent. Exclude any payments for services (e.g., maintenance or utilities) unless they are part of a rent agreement and not separately itemized. Once you have the total, enter this amount in Box 1 (Rents) of the 1099-MISC form. Ensure the figure is accurate, as errors can lead to complications for both the payer and the recipient.

It’s important to note that only rent payments should be reported in Box 1. If you’ve paid other types of income to the recipient, such as royalties or prizes, those amounts should be reported in their respective boxes on the 1099-MISC form. For example, if you paid both rent and a prize for a contest, the rent goes in Box 1, and the prize goes in Box 3 (Other Income). Keeping these categories separate ensures compliance with IRS guidelines and avoids confusion during tax filing.

When completing Box 1, double-check that the recipient’s information, such as their name, address, and taxpayer identification number (TIN), is correct. This information must match the IRS records to avoid processing delays or penalties. If the recipient is an individual, use their Social Security Number (SSN); for businesses, use their Employer Identification Number (EIN). Accurate recipient information, combined with the correct rent total in Box 1, ensures the 1099-MISC is filed correctly.

Finally, after filling out Box 1 (Rents), review the entire form for accuracy before submitting it to the IRS and providing a copy to the recipient. The deadline for filing 1099-MISC forms is typically January 31st of the following year. Late or incorrect filings can result in penalties, so it’s crucial to stay organized and meet deadlines. By carefully reporting the total rent paid in Box 1, you fulfill your tax obligations and help the recipient accurately report their income.

Hot Dog Cart Rentals: Do You Need a License?

You may want to see also

Explore related products

![]()

Box 2-7 Instructions: Leave these boxes blank unless other payments apply (e.g., royalties)

When filling out Form 1099-MISC for rent payments, Box 2 through Box 7 are typically not applicable to rental income scenarios. These boxes are reserved for specific types of payments that differ from rent, such as royalties, commissions, or other miscellaneous income. Box 2-7 Instructions explicitly state: *"Leave these boxes blank unless other payments apply (e.g., royalties)."* This means if you are reporting rent payments, you should focus on Box 1 (Rents) and disregard these boxes unless the recipient received additional income types covered by Box 2-7. For example, if the tenant paid rent and also received royalties from a separate agreement, only the royalties would be reported in the appropriate box, not the rent.

Box 2 (Royalties) is used to report royalty payments made to the recipient. Royalties are typically associated with intellectual property, such as copyrights, patents, or natural resources. If you are reporting rent, this box does not apply. For instance, if a landlord owns a property and also licenses a patent to a tenant, the patent royalties would go in Box 2, while the rent remains in Box 1. Always ensure the payment type aligns with the correct box to avoid errors.

Box 3 (Other Income), Box 4 (Federal Income Tax Withheld), Box 5 (Fishing Boat Proceeds), Box 6 (Medical and Health Care Payments), and Box 7 (Crop Insurance Proceeds) are similarly unrelated to rent payments. These boxes are for specialized income categories, such as payments to independent contractors (Box 3), fishing industry proceeds (Box 5), or health care reimbursements (Box 6). If the recipient received rent and, for example, crop insurance proceeds, only the latter would be reported in Box 7. Rent payments should never be entered in these boxes.

To ensure accuracy, carefully review the nature of the payments being reported. If you are solely reporting rent, leave Box 2-7 blank. Double-check that all income types are correctly categorized to comply with IRS guidelines. Misreporting rent in these boxes could lead to penalties or delays in processing the form. If you are unsure whether a payment qualifies for Box 2-7, consult IRS instructions or a tax professional for clarification.

In summary, when filling out Form 1099-MISC for rent, Box 2-7 should remain blank unless the recipient received additional income types like royalties or other specified payments. Focus on reporting rent in Box 1 and ensure all other boxes align with their designated purposes. This approach ensures compliance and avoids confusion during tax filing. Always refer to the IRS instructions for specific examples and guidance tailored to your situation.

Extended Stay Rental Costs: Budgeting for Long-Term Accommodation Expenses

You may want to see also

Explore related products

![]()

Copy Distribution: Provide Copy B to tenant, Copy C to state, and keep Copy A

When filling out a 1099-MISC form for rent, understanding the proper distribution of copies is crucial to ensure compliance with IRS regulations. The 1099-MISC form consists of multiple copies, each designated for a specific recipient. Copy B is intended for the tenant or recipient of the income. As the landlord or payer, you must provide Copy B to the tenant by January 31st of the year following the payment. This copy is essential for the tenant to report the income on their tax return. It’s important to ensure that Copy B is legible and includes all necessary details, such as the tenant’s name, address, and the amount paid during the tax year. You can deliver Copy B via mail, in-person, or electronically if the tenant consents to receive it digitally.

Copy C of the 1099-MISC form is designated for the state tax department. This copy must be submitted to the appropriate state agency, as required by state tax laws. Not all states require Copy C, so it’s essential to verify your state’s specific requirements. If your state does require it, ensure that Copy C is filed accurately and on time, typically alongside Copy 1 (which is sent to the IRS). Failure to submit Copy C to the state when required can result in penalties, so double-check the state’s filing instructions and deadlines.

Copy A is the most critical copy, as it is filed with the IRS. This copy must be submitted to the IRS by the annual deadline, which is typically the last day of February if filing by paper, or March 31st if filing electronically. Copy A includes all the same information as Copies B and C but is specifically formatted for IRS processing. When filing Copy A, ensure that it is accompanied by Form 1096, the transmittal form that summarizes all 1099 forms being submitted. Properly completing and filing Copy A is essential to avoid IRS penalties for non-compliance.

To summarize the distribution process, start by providing Copy B to the tenant, ensuring they receive it by January 31st. Next, determine if your state requires Copy C and file it accordingly with the state tax department. Finally, retain Copy A for IRS submission, ensuring it is filed by the deadline along with Form 1096. Keeping accurate records of all copies distributed and filed is vital for your records and to demonstrate compliance if audited.

For landlords or payers new to this process, it’s helpful to use IRS instructions or consult a tax professional to ensure accuracy. Additionally, consider using tax software or IRS-approved e-filing services to streamline the distribution and filing of 1099-MISC forms. Properly managing Copy B, Copy C, and Copy A not only ensures compliance but also helps maintain a smooth tax reporting process for both you and your tenants.

Crafting a Comprehensive Event Rental Contract: Essential Steps and Tips

You may want to see also

Explore related products

![]()

Filing Deadlines: Submit to IRS by January 31 and tenant by the same date

When it comes to filing a 1099-MISC form for rent, understanding the deadlines is crucial to avoid penalties and ensure compliance with IRS regulations. The primary deadline to remember is January 31, which applies to both submitting the form to the IRS and providing a copy to your tenant. This date is non-negotiable and applies to the tax year immediately preceding the filing year. For example, if you are reporting rent income for 2023, both the IRS and your tenant must receive their respective copies by January 31, 2024. Marking this date on your calendar is essential, as missing it can result in fines ranging from $50 to $270 per form, depending on how late the submission is.

Submitting the 1099-MISC to the IRS by January 31 requires careful planning. If you are filing electronically, ensure your IRS-approved software or platform is ready well in advance. For paper filings, the form must be mailed to the IRS by the deadline, so account for postal delivery times. The IRS requires that Copy A of the 1099-MISC be submitted to them, along with Form 1096, which summarizes the information on all 1099 forms filed for the year. Double-check that all fields are accurately filled out, including the tenant’s Taxpayer Identification Number (TIN) and the total rent paid during the tax year, as errors can delay processing or trigger IRS inquiries.

Simultaneously, you must provide Copy B of the 1099-MISC to your tenant by January 31. This can be done via mail, email, or in person, depending on the tenant’s preference and your agreement. Ensure the tenant receives the form on time, as they need it to accurately report their rental income on their tax return. Failure to provide the form to the tenant by the deadline can lead to complaints and potential legal issues, even if the IRS submission is on time. Keep proof of delivery, such as a certified mail receipt or email confirmation, to verify compliance.

It’s important to note that if January 31 falls on a weekend or federal holiday, the deadline is extended to the next business day. However, this extension applies only to the tenant copy; the IRS submission must still be postmarked or transmitted electronically by January 31. To avoid last-minute stress, aim to complete the 1099-MISC form and gather all necessary information well before the deadline. This includes confirming the tenant’s TIN and ensuring the total rent amount is accurate, as discrepancies can require filing corrections later.

Finally, while the January 31 deadline is the most critical, it’s also beneficial to start the 1099-MISC preparation process early in January. This allows time to address any issues, such as incorrect tenant information or miscalculated rent totals. Early preparation also ensures you have enough time to order forms or troubleshoot electronic filing issues. By staying organized and adhering to the January 31 deadline for both the IRS and your tenant, you’ll streamline the filing process and maintain compliance with tax regulations.

Step-by-Step Guide to Creating a Rent Account on QB

You may want to see also

Frequently asked questions

You’ll need the recipient’s name, address, taxpayer identification number (TIN or SSN), and the total amount of rent paid during the tax year. Ensure the information is accurate to avoid filing corrections.

Yes, if you paid $600 or more in rent to an individual or unincorporated business during the year, you must issue a 1099-MISC. Payments below $600 do not require a 1099-MISC.

Rent payments should be reported in Box 1 (Rents) of the 1099-MISC form. Ensure the amount is accurate and matches your records.

Yes, you must file Copy A of the 1099-MISC with the IRS and provide Copy B to the recipient by January 31. Keep Copy C for your records.