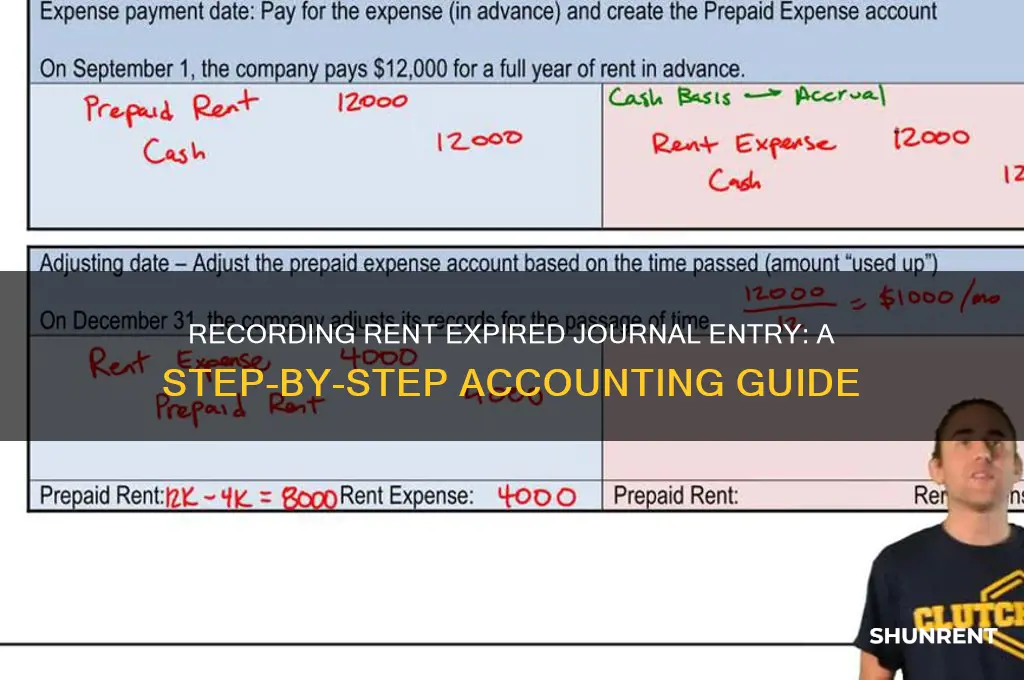

Recording a rent expired journal entry is a critical accounting task that ensures accurate financial reporting by recognizing the portion of prepaid rent that has been consumed over time. This entry is typically made at the end of an accounting period to allocate the prepaid rent expense to the appropriate period, reflecting the principle of matching expenses with revenues. To record this entry, the accountant debits the rent expense account, which increases the expenses on the income statement, and credits the prepaid rent account, reducing the asset on the balance sheet. Proper documentation and consistency in recording these entries are essential to maintain compliance with accounting standards and provide a clear financial picture of the organization's obligations and expenditures.

| Characteristics | Values |

|---|---|

| Journal Entry Type | Adjusting Entry |

| Purpose | To recognize prepaid rent that has been fully consumed (expired) over time |

| Debit Account | Rent Expense (Income Statement Account) |

| Credit Account | Prepaid Rent (Balance Sheet Account) |

| Timing | Recorded at the end of an accounting period |

| Effect on Financial Statements | Increases Rent Expense on the Income Statement; Decreases Prepaid Rent on the Balance Sheet |

| Example Entry | Debit: Rent Expense $X; Credit: Prepaid Rent $X |

| Frequency | Monthly or at the end of each accounting period |

| Documentation Required | Lease agreement, payment receipts, and amortization schedule |

| Compliance | Follows GAAP (Generally Accepted Accounting Principles) or IFRS |

| Impact on Cash Flow | No direct impact on cash flow; reflects the allocation of prepaid rent |

Explore related products

What You'll Learn

- Identify expired leases and related assets for proper journal entry recording

- Determine the correct accounts to debit and credit for rent expiration

- Calculate the amortization of prepaid rent up to expiration date

- Record the reversal of accrued rent liabilities post expiration

- Ensure compliance with accounting standards (e.g., GAAP/IFRS) for accuracy

![]()

Identify expired leases and related assets for proper journal entry recording

Expired leases often linger in accounting records, distorting financial statements and leading to inaccurate reporting. Identifying these dormant agreements is the critical first step in recording proper journal entries to rectify the situation. Begin by systematically reviewing your lease portfolio, cross-referencing lease expiration dates with current occupancy status. Flag any leases that have surpassed their contractual end date without renewal or termination documentation. This process requires meticulous attention to detail, as leases may involve complex terms, extensions, or holdover clauses that affect their expiration status.

Once expired leases are identified, pinpoint the associated assets still recorded on the balance sheet. These typically include leasehold improvements, prepaid rent, or security deposits. For instance, if a tenant vacated a property six months ago but a $5,000 security deposit remains on the books, this asset is no longer valid and must be addressed. Similarly, leasehold improvements amortized over the lease term should be fully expensed once the lease expires, unless the improvements revert to the landlord’s ownership. Failing to adjust these assets results in overstated balance sheets and misrepresented financial health.

The next step involves recording the appropriate journal entries to remove expired leases and related assets from the books. For example, if a prepaid rent balance of $12,000 remains for an expired lease, debit "Rent Expense" for $12,000 and credit "Prepaid Rent" for the same amount. This entry recognizes the unrecoverable expense and eliminates the prepaid asset. Similarly, if a security deposit is no longer refundable, debit "Loss on Lease Expiration" and credit "Security Deposit Payable" to reflect the financial impact. Each entry should be supported by clear documentation, such as lease agreements, termination notices, or correspondence with tenants.

Caution must be exercised when dealing with holdover tenants or leases with automatic renewal clauses. In such cases, determine whether the continued occupancy constitutes a new lease agreement or an extension of the original terms. If treated as a new lease, reclassify the assets accordingly; if considered an extension, adjust the amortization schedules and expiration dates. Misclassifying these scenarios can lead to compliance issues with accounting standards like ASC 842 or IFRS 16, which require precise treatment of lease modifications and extensions.

In conclusion, identifying expired leases and their related assets is a nuanced task requiring diligence, precision, and adherence to accounting principles. By systematically reviewing lease portfolios, adjusting associated assets, and recording accurate journal entries, organizations can maintain clean financial records and avoid misrepresentations. Regular audits of lease agreements and proactive monitoring of expiration dates can further mitigate risks and ensure compliance. This process not only enhances financial accuracy but also strengthens internal controls, fostering trust among stakeholders.

When Does the Star Rental Become Available: Your Guide

You may want to see also

Explore related products

![]()

Determine the correct accounts to debit and credit for rent expiration

Recording a rent expired journal entry requires precision in identifying the correct accounts to debit and credit. The core principle is to recognize that prepaid rent, an asset, decreases as the rental period expires, while rent expense, an income statement account, increases. This reflects the consumption of the prepaid asset over time.

Step-by-Step Account Identification:

- Debit Rent Expense: This account captures the portion of rent attributable to the current period. For example, if a $12,000 annual rent payment is made in advance and one month expires, debit Rent Expense for $1,000 ($12,000 ÷ 12 months).

- Credit Prepaid Rent: This account is reduced by the same amount as the rent expense. Continuing the example, credit Prepaid Rent for $1,000 to reflect the decrease in the prepaid asset.

Cautions and Considerations:

Avoid debiting Cash or crediting Rent Payable, as these accounts are unrelated to the expiration of prepaid rent. Cash is impacted only when the initial payment is made, and Rent Payable applies to unpaid rent, not prepaid amounts. Additionally, ensure the journal entry aligns with the accrual accounting principle, matching expenses to the period in which they are incurred.

Practical Tip:

Use a rent schedule to track prepaid rent balances and expiration dates. This tool simplifies monthly journal entries and ensures accuracy. For instance, a schedule for a $6,000 six-month prepaid rent would show a $1,000 monthly expiration, guiding consistent debits to Rent Expense and credits to Prepaid Rent.

Mastering the correct accounts for rent expiration journal entries hinges on understanding the relationship between prepaid rent and rent expense. By systematically debiting Rent Expense and crediting Prepaid Rent, businesses accurately reflect the consumption of prepaid assets and adhere to accounting principles. This precision ensures financial statements provide a true and fair view of financial performance.

Rent vs. Tick, Tick... Boom: Which Musical Came First?

You may want to see also

Explore related products

![]()

Calculate the amortization of prepaid rent up to expiration date

Prepaid rent represents a unique accounting challenge, as it requires allocating the expense over the period it benefits the business. When the lease expires, any remaining prepaid rent must be recognized as an expense, ensuring the financial statements accurately reflect the business’s obligations. Calculating the amortization of prepaid rent up to the expiration date is a critical step in this process, as it determines how much of the prepaid amount should be expensed and how much remains as an asset.

To begin, identify the total prepaid rent amount and the lease term. For example, if a business pays $12,000 annually for rent and the lease expires in 10 months, the prepaid rent for the remaining period must be calculated. Divide the total prepaid rent by the number of months in the lease term to determine the monthly rent expense. In this case, $12,000 ÷ 12 months = $1,000 per month. Multiply this monthly expense by the number of months remaining in the lease to find the amount to be expensed. For 10 months, the calculation would be $1,000 × 10 = $10,000. This $10,000 represents the prepaid rent that has expired and should be recorded as a rent expense.

A journal entry is then required to reflect this amortization. Debit the rent expense account for $10,000, recognizing the expired portion of the prepaid rent as an expense. Simultaneously, credit the prepaid rent account for the same amount, reducing the asset by the value that has been utilized. This entry ensures the balance sheet and income statement accurately represent the business’s financial position and performance. For instance, the journal entry would appear as: *Debit Rent Expense $10,000, Credit Prepaid Rent $10,000*.

It’s essential to review the lease agreement for any irregularities, such as escalating rent payments or free rent periods, which may affect the amortization calculation. Additionally, ensure compliance with accounting standards like GAAP or IFRS, which may dictate specific treatment for prepaid expenses. By meticulously calculating and recording the amortization of prepaid rent, businesses maintain transparency and accuracy in their financial reporting, fostering trust among stakeholders and ensuring compliance with regulatory requirements.

¿Está Nuestro Alquiler Actualizado? Entendiendo 'Up to Date' en Español

You may want to see also

Explore related products

![]()

Record the reversal of accrued rent liabilities post expiration

Accrued rent liabilities represent obligations for rent expenses incurred but not yet paid. When the rental period expires, these liabilities must be reversed to accurately reflect the financial position of the business. This process ensures compliance with accounting principles like the matching principle, which requires expenses to be recognized in the period they are incurred. Failure to reverse accrued rent liabilities can lead to overstated liabilities and understated equity on the balance sheet.

To record the reversal of accrued rent liabilities post-expiration, follow these steps: First, identify the accrued rent liability account on your books. This account typically resides under current liabilities. Second, debit the accrued rent liability account to reduce its balance. Simultaneously, credit the rent expense account to offset the previously recognized expense. For example, if a company had accrued $5,000 in rent for December but the lease expired on December 31, the journal entry would debit Accrued Rent Liabilities for $5,000 and credit Rent Expense for $5,000. This entry effectively removes the liability and adjusts the expense to reflect the actual rental period.

While the process seems straightforward, caution is necessary to avoid errors. Ensure the accrued amount corresponds precisely to the expired period. Over-reversal or under-reversal can distort financial statements. For instance, if only a portion of the accrued rent pertains to the expired period, reverse only that amount. Additionally, verify that the lease agreement does not include any post-expiration obligations, such as maintenance fees, which might require separate treatment. Cross-referencing the lease agreement with the accrued amount minimizes the risk of inaccuracies.

The reversal of accrued rent liabilities post-expiration is not merely a technical adjustment but a critical step in maintaining financial integrity. It aligns the company’s books with the economic reality of the transaction. For businesses with multiple leases or complex rental agreements, implementing a systematic review process at the end of each reporting period can streamline this task. Software tools with automated accrual reversal features can further enhance accuracy and efficiency, particularly for larger organizations. By mastering this process, businesses ensure their financial statements accurately reflect their obligations and expenses, fostering trust among stakeholders.

Post-Eviction Rent Collection: Legal or Unlawful Practice?

You may want to see also

Explore related products

![]()

Ensure compliance with accounting standards (e.g., GAAP/IFRS) for accuracy

Recording a rent expired journal entry demands precision, especially when aligning with accounting standards like GAAP or IFRS. These frameworks mandate that expenses be recognized in the period they are incurred, not when paid. For rent, this means allocating the expense over the lease term, even if payment is upfront. Under GAAP, ASC 842 requires lessees to recognize a lease liability and right-of-use asset, with rent expense amortized over the lease period. IFRS 16 mirrors this approach, emphasizing the importance of matching expenses to the periods benefiting from the leased asset. Failure to comply can distort financial statements, mislead stakeholders, and trigger regulatory penalties.

To ensure compliance, start by identifying the lease term and payment structure. For instance, if a $12,000 annual rent is paid in advance for a 12-month lease, record the initial payment as a prepaid asset. Each month, adjust the entry by debiting rent expense ($1,000) and crediting the prepaid rent account. This method aligns with the matching principle, a cornerstone of both GAAP and IFRS. Use accounting software with lease accounting modules to automate calculations and reduce errors, particularly for complex leases with escalation clauses or variable payments.

A common pitfall is treating prepaid rent as an expense in the payment month, violating accrual accounting principles. To avoid this, maintain a clear distinction between prepaid assets and expenses. Regularly review lease agreements for changes in terms or extensions, updating journal entries accordingly. For example, if a lease is renewed mid-year, recalculate the monthly expense based on the new term and adjust the prepaid rent balance. Documentation is critical—retain lease agreements, payment receipts, and journal entry details for audit trails.

Compliance also extends to disclosures. Both GAAP and IFRS require lessees to disclose lease terms, payment schedules, and the impact on financial statements. Include these details in footnotes to ensure transparency. For instance, disclose the total lease liability, right-of-use asset, and future minimum lease payments. This not only satisfies regulatory requirements but also provides stakeholders with a clearer understanding of financial obligations.

Finally, stay updated on standard revisions. GAAP and IFRS periodically issue amendments, such as IFRS 16’s recent clarifications on lease modifications. Subscribe to accounting newsletters or consult with professionals to ensure ongoing compliance. By adhering to these standards, businesses not only maintain accuracy in rent expired journal entries but also uphold the integrity of their financial reporting, fostering trust among investors and regulators alike.

Renting Land for Medical Marijuana Cultivation: A Comprehensive Guide

You may want to see also

Frequently asked questions

A rent expired journal entry is a financial transaction recorded in the books of a business to recognize the portion of prepaid rent that has been used up or expired during a specific accounting period.

A rent expired journal entry should be recorded at the end of each accounting period, typically monthly or annually, to allocate the prepaid rent expense over the lease term and accurately reflect the business's financial position.

To calculate the rent expired amount, divide the total prepaid rent by the number of periods in the lease term, then multiply by the number of periods that have passed. The formula is: (Total Prepaid Rent / Lease Term in Periods) x Number of Periods Expired.

The journal entry for recording rent expired typically debits the rent expense account and credits the prepaid rent account. For example: Debit Rent Expense (Income Statement) and Credit Prepaid Rent (Balance Sheet) for the calculated expired amount.