Calculating rent per month is a fundamental skill for both tenants and landlords, ensuring clarity and fairness in rental agreements. To determine the monthly rent, start by identifying the total annual rent or the rent for a different period, such as quarterly or biannually. Divide this amount by the number of months in the given period to find the monthly cost. For example, if the annual rent is $12,000, dividing it by 12 months yields a monthly rent of $1,000. Additionally, consider any prorated amounts for partial months or adjustments for utilities, maintenance, or other shared expenses. Understanding this calculation helps tenants budget effectively and ensures landlords receive consistent payments, fostering a transparent and mutually beneficial rental relationship.

| Characteristics | Values |

|---|---|

| Annual Rent Calculation | Multiply the weekly rent by 52 (weeks in a year). |

| Monthly Rent Calculation | Divide the annual rent by 12 (months in a year). |

| Weekly to Monthly Conversion | Multiply the weekly rent by 4.33 (average weeks in a month). |

| Daily Rent Calculation | Divide the weekly rent by 7 (days in a week). |

| Rent per Square Foot | Divide the monthly rent by the total square footage of the property. |

| Rent-to-Income Ratio | Ensure monthly rent does not exceed 30% of gross monthly income. |

| Market Rent Comparison | Research local rental prices for similar properties to ensure fairness. |

| Additional Costs | Include utilities, maintenance fees, or other charges in total rent. |

| Lease Agreement Terms | Specify rent amount, payment due date, and late fees in the contract. |

| Rent Increase Considerations | Check local laws for allowable rent increase percentages and frequency. |

| Tax Implications | Landlords may deduct expenses like repairs and mortgage interest. |

| Online Rent Calculators | Use tools like Zillow or Rentometer for quick rent estimation. |

Explore related products

What You'll Learn

- Calculate Annual Rent: Multiply monthly rent by 12 to find yearly cost

- Divide by Pay Periods: Split monthly rent into weekly or biweekly payments

- Include Utilities: Add estimated utility costs to base rent for total monthly expense

- Use Rent-to-Income Ratio: Ensure rent is 30% or less of monthly income

- Factor in Fees: Include parking, pet fees, or maintenance costs in total rent

![]()

Calculate Annual Rent: Multiply monthly rent by 12 to find yearly cost

Understanding your annual rent commitment is a cornerstone of financial planning for tenants. While monthly rent is the figure most commonly discussed, the yearly cost provides a broader perspective on your housing expenses. To calculate annual rent, simply multiply your monthly rent by 12. This straightforward method offers a clear view of your long-term financial obligation, helping you budget more effectively and plan for the future.

For instance, if your monthly rent is $1,200, multiplying this by 12 yields an annual rent of $14,400. This calculation is particularly useful when comparing housing costs to your annual income or when considering long-term financial goals. It also highlights the cumulative impact of rent increases over time, making it easier to assess whether a particular rental property aligns with your financial plans.

However, this method assumes a fixed monthly rent throughout the year, which may not always be the case. Some leases include provisions for rent increases mid-term, or utilities and other costs might fluctuate. In such scenarios, multiplying the initial monthly rent by 12 provides a baseline estimate, but you should account for potential variations to ensure accuracy. For example, if your rent increases by 3% after six months, calculate the new monthly rate and adjust your annual estimate accordingly.

A practical tip for tenants is to use this calculation as a starting point for broader financial planning. Pair it with an analysis of your monthly income, savings goals, and other expenses to determine if your rent is sustainable long-term. Tools like budgeting apps or spreadsheets can help visualize how annual rent fits into your overall financial picture. Additionally, consider negotiating lease terms that align with your financial goals, such as longer lease agreements that may offer rent stability.

In conclusion, multiplying your monthly rent by 12 is a simple yet powerful way to understand your annual housing commitment. While it’s a foundational calculation, it’s essential to factor in potential changes to rent or associated costs for a more accurate assessment. By mastering this method, you gain valuable insight into your financial obligations, enabling smarter decisions about where and how you live.

Is a California Lease Agreement Essential for Renting Property?

You may want to see also

Explore related products

![]()

Divide by Pay Periods: Split monthly rent into weekly or biweekly payments

For tenants paid weekly or biweekly, aligning rent payments with their pay schedule can ease budgeting. To calculate weekly rent from a monthly total, divide the monthly amount by 4.33 (the average number of weeks in a month). For example, a $1,200 monthly rent becomes approximately $277 per week ($1,200 ÷ 4.33). For biweekly payments, divide the monthly rent by 2.17 (since there are roughly 2.17 pay periods in a month), yielding about $553 biweekly for the same $1,200 rent ($1,200 ÷ 2.17).

This method offers predictability for tenants whose income arrives in regular intervals. For instance, a retail worker earning $600 biweekly can allocate exactly half their paycheck to rent if it’s structured as a $553 biweekly payment. However, landlords must ensure the total collected over the year matches the annual rent obligation. For a $1,200 monthly rent, weekly payments of $277 sum to $14,404 annually (52 weeks × $277), while biweekly payments of $553 total $14,366 (26 pay periods × $553)—both slightly exceeding $14,400 due to rounding, requiring minor adjustments.

A cautionary note: this approach assumes consistent pay periods. If a tenant’s income fluctuates or pay dates shift, misalignment may occur. For example, a month with five Fridays instead of four would require an extra weekly payment, potentially straining the tenant’s budget. Landlords can mitigate this by including a clause in the lease specifying how additional payments are handled, such as applying them to the next month’s rent.

To implement this system effectively, both parties should agree on a clear payment calendar. A shared spreadsheet or app like Splitwise can track payments and due dates. Tenants benefit from smoother cash flow management, while landlords gain consistent income. For instance, a landlord with multiple units could stagger biweekly payments across tenants to ensure a steady cash flow throughout the month, rather than relying on lump-sum monthly payments.

Ultimately, dividing rent by pay periods transforms a large monthly expense into manageable chunks, fostering financial stability for tenants and reliability for landlords. By using precise calculations and proactive communication, this method turns potential budgeting headaches into a win-win arrangement.

Essential Requirements for Renting a U-Haul: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Include Utilities: Add estimated utility costs to base rent for total monthly expense

Utility costs can significantly impact your monthly budget, yet they’re often overlooked when calculating rent. Including utilities in your rent calculation provides a more accurate picture of your total housing expense. Start by identifying which utilities are typically excluded from base rent—electricity, gas, water, internet, and trash removal are common examples. Research average monthly costs for these services in your area, either through local utility providers or rental market reports. For instance, electricity might average $100–$200 per month for a one-bedroom apartment, while internet could range from $50–$80. Adding these estimates to your base rent gives you a realistic total monthly expense.

To streamline this process, consider using online tools or rental platforms that provide utility cost estimates for specific neighborhoods. Some landlords or property managers may also offer bundled utility packages, where certain utilities are included in the rent for a fixed fee. If this is the case, compare the bundled cost to the average market rate to ensure you’re getting a fair deal. For example, if a landlord charges $150 extra for utilities, verify whether this aligns with typical costs for the area. This step prevents unexpected financial strain and helps you budget effectively.

A practical approach is to track your utility usage over time if you’re already renting. Monitor monthly bills for electricity, water, and other services to identify patterns and average costs. This data becomes a valuable reference when evaluating future rentals. For instance, if your current electricity bill averages $120 per month, use this figure as a benchmark when estimating utility costs for a new place. Keep in mind that factors like apartment size, energy efficiency, and personal usage habits can influence these costs, so adjust your estimates accordingly.

Including utilities in your rent calculation isn’t just about avoiding surprises—it’s about making informed decisions. For example, a lower base rent might seem appealing, but if utility costs are exorbitant, the total expense could outweigh the savings. Conversely, a slightly higher rent with utilities included might offer better value and predictability. Prioritize transparency by asking landlords for historical utility data or requesting separate meter readings if utilities are shared. This proactive approach ensures your monthly budget remains stable and manageable.

Finally, consider negotiating utility terms as part of your lease agreement. Some landlords may be open to including utilities in the base rent or capping utility costs to a certain amount. If you’re moving into a shared space, clarify how utilities will be divided among tenants to avoid disputes. By treating utilities as an integral part of your rent calculation, you gain a comprehensive understanding of your housing costs and can make choices that align with your financial goals.

Effective Strategies for Collecting Late Rent in Pennsylvania

You may want to see also

Explore related products

![]()

Use Rent-to-Income Ratio: Ensure rent is 30% or less of monthly income

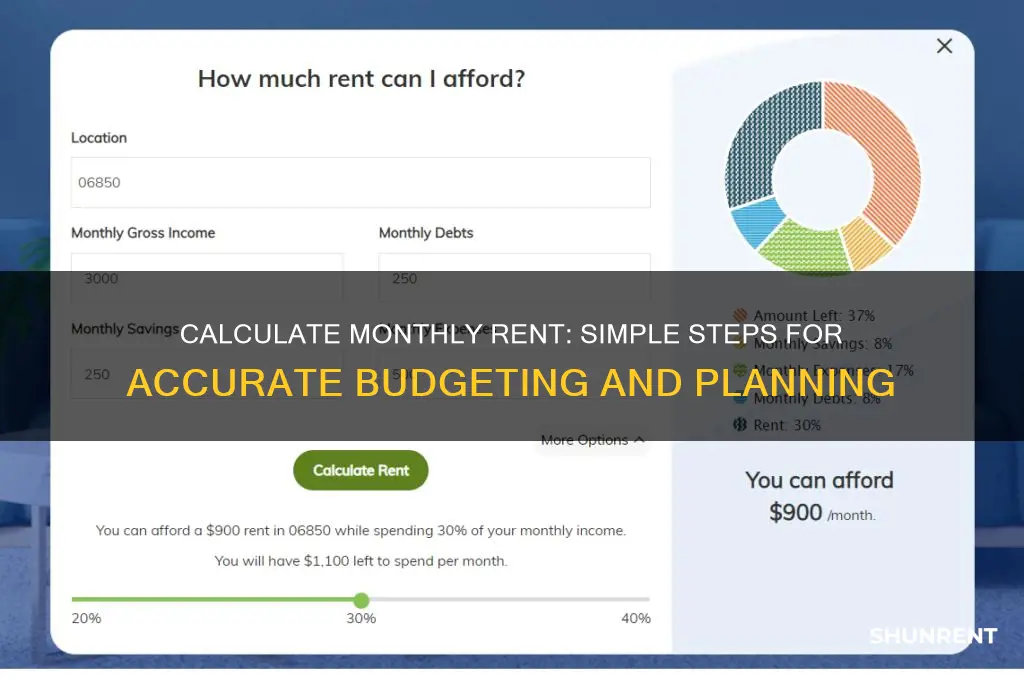

A common rule of thumb in personal finance is the 30% rent-to-income ratio, which suggests that your monthly rent should not exceed 30% of your gross monthly income. This guideline helps ensure that you have enough money left over for other essential expenses, savings, and discretionary spending. For instance, if your monthly income is $4,000, your rent should ideally be $1,200 or less. This simple calculation provides a quick benchmark to assess whether a rental property is within your budget.

To apply this ratio effectively, start by calculating your gross monthly income, which includes all pre-tax earnings from salaries, wages, or other sources. Next, multiply this figure by 0.30 to determine the maximum rent you should consider. For example, if you and your partner have a combined monthly income of $6,000, your rent threshold would be $1,800. This method is particularly useful when comparing multiple rental options, as it provides a clear financial boundary to guide your decision-making.

However, the 30% rule is not one-size-fits-all. Factors such as high cost-of-living areas, significant debt, or irregular income may require adjustments. In expensive cities like New York or San Francisco, renters often exceed this threshold due to limited affordable housing. If you find yourself in this situation, consider strategies like finding a roommate, negotiating rent, or exploring government housing assistance programs. Conversely, if you’re in a lower-cost area or have minimal financial obligations, you might aim for an even lower rent-to-income ratio to accelerate savings or investments.

Critics of the 30% rule argue that it doesn’t account for individual financial circumstances, such as childcare costs, student loans, or medical expenses. To address this, supplement the ratio with a detailed budget that includes all monthly expenses. For example, if your rent is 30% of your income but you also have $500 in student loan payments, you may need to find a less expensive rental to maintain financial stability. Tools like budgeting apps or spreadsheets can help you visualize how rent fits into your overall financial picture.

Ultimately, the 30% rent-to-income ratio serves as a starting point, not a rigid rule. It’s a practical tool to prevent overspending on housing while balancing other financial priorities. By combining this guideline with a personalized budget and an awareness of your unique circumstances, you can make informed decisions about how much rent you can comfortably afford. Remember, the goal is not just to find a place to live, but to secure one that supports your long-term financial health.

Average Rent in Charleston, SC: What to Expect in 2023

You may want to see also

Explore related products

![]()

Factor in Fees: Include parking, pet fees, or maintenance costs in total rent

Rent calculations often stop at the base amount, but savvy tenants know that additional fees can significantly impact monthly expenses. Parking, pet ownership, and maintenance are common add-ons that, when overlooked, lead to budget shortfalls. For instance, a downtown apartment might advertise $1,200 per month but include a $150 parking fee and a $50 pet fee, pushing the total to $1,400. This example underscores the importance of factoring in these costs from the outset.

Analyzing these fees reveals their variability based on location and property type. In urban areas, parking fees can range from $100 to $300 monthly, while suburban complexes might offer free parking. Pet fees also differ widely: some landlords charge a one-time deposit of $200–$500, while others impose monthly fees of $25–$75 per pet. Maintenance costs, often hidden in utilities or bundled into rent, can surface as separate line items in newer or luxury buildings. Understanding these regional and property-specific trends is crucial for accurate budgeting.

To incorporate these fees effectively, start by requesting a detailed breakdown from the landlord or property manager. Ask specifically about parking availability and costs, pet policies, and any maintenance or amenity fees. For example, if a building charges $50 monthly for gym access, decide whether this is a necessary expense or an optional add-on. Next, categorize these fees as fixed (e.g., parking) or variable (e.g., pet fees that depend on the number of pets). Finally, add these totals to the base rent to determine the actual monthly cost.

A persuasive argument for this approach lies in its ability to prevent financial surprises. Tenants who ignore these fees often face cash flow issues, especially when moving into a new place with higher-than-expected costs. By treating the total rent—base amount plus fees—as a single figure, renters can make informed decisions about affordability. For instance, a $1,500 rent with $200 in fees might be more manageable than a $1,600 rent with no fees, depending on the included services.

In conclusion, factoring in fees like parking, pet charges, and maintenance is essential for a realistic rent calculation. This practice requires diligence in gathering information, analyzing regional trends, and categorizing expenses. By adopting this comprehensive approach, tenants can avoid hidden costs and ensure their monthly budget aligns with their financial goals. After all, the true cost of renting extends far beyond the base rent advertised.

Understanding Florida Lot Rents: A Comprehensive Guide for Mobile Homeowners

You may want to see also

Frequently asked questions

Divide the annual rent by 12 to get the monthly rent. For example, if the annual rent is $12,000, the monthly rent is $1,000.

Multiply the weekly rent by 4.33 (the average number of weeks in a month). For example, if the weekly rent is $250, the monthly rent is $1,082.50.

It depends on the agreement. If utilities are included in the rent, factor their estimated cost into the total rent amount. If they’re separate, calculate rent and utilities as distinct expenses.

Multiply the monthly rent by the number of days you’ll occupy the property, then divide by the total days in the month. For example, if the monthly rent is $1,200 and you move in on the 15th of a 30-day month, the prorated rent is $600.

Yes, online rent calculators can help you determine monthly rent based on annual, weekly, or prorated amounts. They’re a quick and accurate tool for rent calculations.

![Rent [Blu-ray]](https://m.media-amazon.com/images/I/61-pbYukUxL._AC_UY218_.jpg)