Determining what percentage of your income should go toward rent is a critical aspect of financial planning and stability. As a general rule of thumb, financial experts often recommend allocating no more than 30% of your gross monthly income to housing costs, including rent. This guideline, known as the 30% rule, helps ensure that you have enough funds left for other essential expenses like utilities, groceries, transportation, and savings. However, this percentage can vary based on individual circumstances, such as location, income level, and personal financial goals. For instance, in high-cost-of-living areas, renters might need to exceed this threshold, while those with lower incomes may aim for a smaller percentage to avoid financial strain. Understanding this balance is key to maintaining a healthy budget and avoiding the pitfalls of overspending on housing.

| Characteristics | Values |

|---|---|

| Recommended Rent-to-Income Ratio | 30% or less |

| Source of Recommendation | U.S. Department of Housing and Urban Development (HUD) |

| Reason for 30% Rule | Ensures affordability and prevents financial strain |

| Average Rent-to-Income Ratio in the U.S. (2023) | ~32-35% (varies by city and income level) |

| Factors Influencing Ratio | Location, income level, lifestyle, and financial goals |

| High-Cost Urban Areas (e.g., NYC, SF) | Rent often exceeds 30%, sometimes reaching 50%+ |

| Low-Cost Rural Areas | Rent typically below 30% of income |

| Adjustments for Financial Goals | Lower ratio (e.g., 25%) if saving for a home or investments |

| Impact of Debt (e.g., student loans) | May require a lower rent-to-income ratio |

| Alternative Budgeting Methods | 50/30/20 rule (50% needs, 30% wants, 20% savings) |

| Importance of Personalization | Tailor ratio based on individual financial situation |

| Tools for Calculation | Online rent affordability calculators, budgeting apps |

Explore related products

What You'll Learn

- Budgeting Basics: Understanding income allocation for rent and other expenses effectively

- /30/20 Rule: Applying this rule to balance rent within your financial plan

- Local Cost Variations: Adjusting rent percentage based on regional living expenses

- Emergency Funds: Ensuring rent fits without compromising savings for unexpected costs

- Debt Considerations: Balancing rent payments with existing financial obligations wisely

![]()

Budgeting Basics: Understanding income allocation for rent and other expenses effectively

Effective budgeting is a cornerstone of financial stability, and understanding how to allocate your income wisely is crucial. One of the most significant expenses for many individuals and families is rent, which can easily consume a large portion of your earnings if not managed properly. A widely accepted rule of thumb is the 30% rule, which suggests that you should aim to spend no more than 30% of your gross monthly income on rent. This guideline helps ensure that you have enough funds left for other essential expenses, savings, and discretionary spending. However, this percentage may need to be adjusted based on your location, income level, and overall financial goals.

When determining the appropriate percentage of your income to allocate to rent, it’s essential to consider your broader financial situation. For instance, if you live in a high-cost-of-living area, you might find it challenging to stay within the 30% threshold. In such cases, it may be necessary to prioritize housing while cutting back on other discretionary expenses or finding ways to increase your income. Conversely, if you live in a more affordable area, you might allocate less than 30% to rent, allowing you to save more or invest in other financial goals like retirement or emergency funds.

Beyond rent, effective budgeting requires a holistic approach to income allocation. The 50/30/20 rule is another popular framework that can guide your spending habits. According to this rule, 50% of your income should cover necessities (including rent, utilities, groceries, and transportation), 30% should go toward discretionary spending (such as entertainment, dining out, and hobbies), and 20% should be allocated to savings and debt repayment. This rule ensures a balanced approach to managing your finances while still allowing flexibility for personal enjoyment.

To implement these principles, start by calculating your monthly income and fixed expenses. Track your spending for a few months to identify areas where you might be overspending. Use budgeting tools or apps to categorize your expenses and monitor your progress. If your rent exceeds 30% of your income, consider downsizing, finding a roommate, or negotiating your rent with your landlord. Additionally, look for ways to reduce other fixed expenses, such as refinancing loans or cutting unnecessary subscriptions.

Finally, remember that budgeting is a dynamic process that requires regular review and adjustment. Life circumstances change, and so should your budget. Periodically reassess your income, expenses, and financial goals to ensure your budget remains aligned with your priorities. By mastering the basics of income allocation, particularly for rent, you can build a solid foundation for financial health and achieve long-term stability.

Late Rent: How It Impacts Your Rental History

You may want to see also

Explore related products

![]()

50/30/20 Rule: Applying this rule to balance rent within your financial plan

The 50/30/20 Rule is a widely recognized budgeting framework that divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. When applying this rule to determine what percentage of your income should go toward rent, it’s crucial to categorize rent as a need, since housing is essential. This means rent should fall within the 50% allocation for needs, which includes other essentials like groceries, utilities, transportation, and insurance. To maintain financial balance, rent alone should ideally not exceed 30% of your take-home pay, as this leaves room for other necessities within the 50% category.

For example, if your monthly after-tax income is $4,000, the 50/30/20 Rule suggests allocating $2,000 to needs. To adhere to the common guideline that rent should be no more than 30% of your income, your rent should be around $1,200 or less. This ensures you have $800 remaining in the "needs" category for other essential expenses. Exceeding this threshold can strain your budget, leaving insufficient funds for other necessities or forcing you to dip into the "wants" or "savings" categories, which undermines the rule’s purpose.

Applying the 50/30/20 Rule to rent requires careful planning and prioritization. If you live in a high-cost area where rent exceeds 30% of your income, consider adjusting other expenses within the "needs" category or exploring more affordable housing options. For instance, you might reduce transportation costs by using public transit or cut back on utilities by conserving energy. Alternatively, if your rent is well below 30%, you can allocate the surplus to savings, investments, or paying off debt, aligning with the 20% savings goal of the rule.

It’s also important to periodically reassess your budget as your income or expenses change. For instance, if you receive a raise, aim to keep your rent percentage stable or reduce it rather than upgrading to a more expensive place. This ensures you maintain financial stability and continue to meet your savings and debt repayment goals. The 50/30/20 Rule is flexible but requires discipline to ensure rent and other needs don’t overshadow your long-term financial health.

Finally, while the 50/30/20 Rule provides a solid framework, it’s not one-size-fits-all. Individual circumstances, such as high student loan payments or childcare costs, may require adjustments. However, keeping rent within the 30% guideline remains a cornerstone of balanced budgeting. By adhering to this principle, you can ensure that your housing costs support, rather than hinder, your overall financial plan.

Surviving the City: How Community College Professors Afford Rent

You may want to see also

Explore related products

![]()

Local Cost Variations: Adjusting rent percentage based on regional living expenses

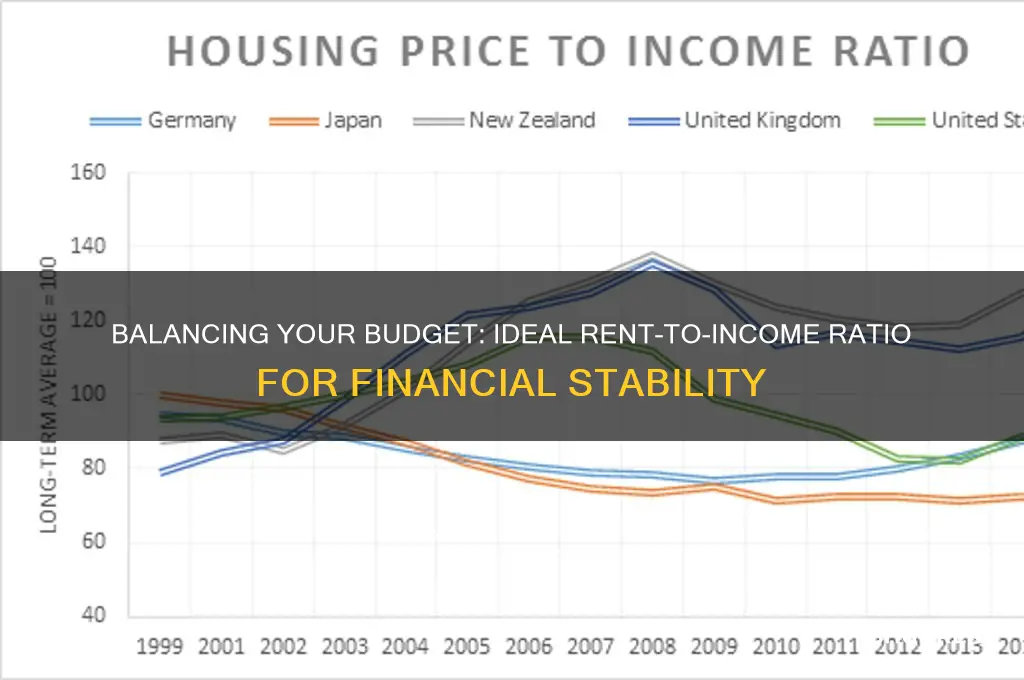

When determining what percentage of your income should go toward rent, it's essential to consider local cost variations, as living expenses differ significantly across regions. The commonly recommended 30% rule—spending no more than 30% of your income on housing—may not be feasible or realistic in high-cost areas like New York City, San Francisco, or London. In these cities, rent often consumes 40% to 50% of income due to skyrocketing housing prices and limited availability. Conversely, in more affordable regions like the Midwest or rural areas, allocating only 20% to 25% of income to rent is often sufficient, allowing for greater financial flexibility in other areas.

Regional economic factors play a critical role in adjusting rent percentages. In cities with robust job markets and high wages, residents may be able to allocate a larger portion of their income to rent without compromising their financial stability. For example, in tech hubs like Seattle or Silicon Valley, higher salaries can justify spending closer to 35% or 40% on housing. However, in areas with lower average incomes, such as parts of the Southern U.S. or smaller towns, adhering strictly to the 30% rule is more practical to ensure affordability and avoid financial strain.

Another factor to consider is the cost of living index for a specific region, which measures expenses like groceries, transportation, and healthcare relative to the national average. In cities with a high cost of living, such as Los Angeles or Miami, rent is just one of several elevated expenses. Here, it may be necessary to adjust the rent percentage upward to reflect the overall financial burden. Conversely, in regions with a lower cost of living, reducing the rent percentage allows individuals to save more or allocate funds to other priorities like debt repayment or investments.

Local housing market dynamics also influence rent affordability. In areas with a housing shortage, such as many urban centers, competition drives up prices, forcing renters to spend a larger share of their income on housing. In contrast, regions with abundant housing supply, such as suburban or rural areas, offer more affordable options, enabling renters to stay within or below the 30% threshold. Understanding these market conditions is crucial for setting realistic rent budgets.

Finally, personal financial goals and circumstances should guide adjustments to the rent percentage. For instance, someone prioritizing saving for a home or retirement in a high-cost city might aim to keep rent closer to 30% by choosing a smaller or shared living space. Conversely, individuals in low-cost areas with stable incomes may opt to spend slightly more on rent for added comfort or convenience. Tailoring the rent percentage to both regional expenses and individual priorities ensures a balanced and sustainable budget.

How to Delete Boards on Rent the Runway: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Emergency Funds: Ensuring rent fits without compromising savings for unexpected costs

When determining what percentage of your income should go toward rent, it’s crucial to consider not only your monthly budget but also your emergency fund. Financial experts often recommend the 30% rule, which suggests that rent should not exceed 30% of your gross monthly income. However, this rule alone can be misleading if it doesn’t account for your ability to save for unexpected expenses. Emergency funds are essential to cover sudden costs like medical bills, car repairs, or job loss, and they should not be compromised to meet rent obligations. To ensure rent fits comfortably within your budget while maintaining savings, start by evaluating your total monthly income and fixed expenses. Subtract essentials like utilities, groceries, and transportation, and then allocate a portion to your emergency fund before determining how much you can afford for rent.

Building and maintaining an emergency fund is a cornerstone of financial stability. Aim to save at least three to six months’ worth of living expenses in a readily accessible account. If your rent consumes too much of your income, it becomes difficult to contribute to this fund consistently. For example, if 40% or more of your income goes toward rent, you may struggle to save for emergencies, leaving you vulnerable to financial stress during unforeseen circumstances. To avoid this, adjust your rent budget downward if necessary, even if it means finding a more affordable living situation. Prioritizing emergency savings ensures that you can handle unexpected costs without derailing your financial goals or relying on high-interest debt.

To strike a balance between rent and emergency savings, consider the 50/30/20 rule as a complementary guideline. This rule suggests allocating 50% of your income to needs (including rent), 30% to wants, and 20% to savings and debt repayment. Within the 20% savings category, prioritize your emergency fund. If rent is pushing your needs above 50%, reevaluate your housing options or explore ways to increase your income. For instance, downsizing to a smaller apartment or moving to a more affordable neighborhood can free up funds for savings. Additionally, tracking your expenses and cutting non-essential costs can create more room in your budget for both rent and emergency savings.

Another strategy is to treat your emergency fund contribution as a non-negotiable monthly expense, just like rent or utilities. Automate transfers to your savings account to ensure consistency. If you’re already paying a high percentage of your income in rent, focus on gradually reducing housing costs while simultaneously building your emergency fund, even if it’s in small increments. Remember, the goal is to create a financial buffer that allows you to cover rent and other essentials during emergencies without going into debt. By keeping your rent within a reasonable percentage of your income and prioritizing savings, you can achieve a more secure and balanced financial life.

Finally, regularly review your budget to ensure that your rent and emergency savings remain aligned with your financial goals. Life circumstances, such as a job change or increase in income, may allow you to adjust your housing situation or save more. Conversely, unexpected expenses or a reduction in income may require you to temporarily reduce rent or slow emergency fund contributions. Staying proactive and flexible in managing your budget will help you maintain a healthy balance between rent and savings, ensuring that you’re prepared for whatever financial challenges come your way.

Maximize Your Venue's Appeal: Proven Strategies to Attract Renters

You may want to see also

Explore related products

![]()

Debt Considerations: Balancing rent payments with existing financial obligations wisely

When determining what percentage of your income should go toward rent, it’s crucial to consider your existing financial obligations, especially debt. The widely recommended guideline is that rent should not exceed 30% of your gross monthly income. However, this rule must be adjusted based on your overall financial situation, particularly if you’re managing student loans, credit card debt, car payments, or other liabilities. High debt payments can significantly reduce your disposable income, making it essential to allocate rent within a lower percentage of your budget to avoid financial strain.

Start by assessing your total monthly debt obligations. Add up payments for student loans, credit cards, personal loans, and any other recurring debts. If these payments consume a large portion of your income, consider reducing your rent budget below the 30% threshold. For example, if 25% of your income goes toward debt repayment, limiting rent to 20-25% of your income may be more sustainable. This ensures you have enough funds to cover essentials and avoid accumulating additional debt.

Prioritizing high-interest debt is another critical aspect of balancing rent with financial obligations. If you’re paying off credit cards or other high-interest loans, it may be wise to allocate more of your income to debt repayment rather than rent. While housing is essential, paying down high-interest debt faster can save you money in the long run and free up more of your income for other expenses. Consider negotiating a slightly lower rent or choosing a more affordable living situation to accelerate debt repayment.

Creating a detailed budget is essential for managing rent and debt effectively. List all monthly expenses, including rent, debt payments, utilities, groceries, and discretionary spending. This will help you identify areas where you can cut back to accommodate both rent and debt obligations. For instance, reducing dining out or subscription services can free up funds to meet your financial commitments without overextending yourself. A clear budget also highlights whether the 30% rent rule is feasible or if adjustments are necessary.

Finally, build an emergency fund to provide a buffer for unexpected expenses. When a significant portion of your income is allocated to rent and debt, unexpected costs can derail your financial stability. Aim to save at least three to six months’ worth of living expenses in an emergency fund. This not only protects you from unforeseen events but also reduces the likelihood of relying on high-interest debt to cover emergencies. Balancing rent payments with existing financial obligations requires careful planning, prioritization, and a proactive approach to managing debt.

Rent Tripling: $3600 a Month?

You may want to see also

Frequently asked questions

A common rule of thumb is to spend no more than 30% of your gross monthly income on rent. This guideline helps ensure you have enough money left for other expenses, savings, and emergencies.

Not necessarily. The 30% rule is a general guideline, but individual circumstances vary. Factors like high cost of living, debt, or financial goals may require adjusting this percentage downward to maintain a balanced budget.

If rent exceeds 30% of your income, consider options like finding a roommate, moving to a more affordable area, or increasing your income through side jobs or promotions.

Yes, it’s best to include all housing-related expenses, such as utilities, renters insurance, and maintenance, in your calculation to get a more accurate picture of your total housing costs.