Paid rent is typically recorded as an expense on a balance sheet rather than being directly calculated on it, as the balance sheet reflects a company’s financial position at a specific point in time, while rent payments are part of the income statement, which tracks revenues and expenses over a period. However, prepaid rent—rent paid in advance for future periods—is recorded as a current asset on the balance sheet until the rental period is utilized. To calculate prepaid rent, the total amount paid in advance is initially recorded as an asset, and then it is gradually expensed over the rental period, reducing the asset balance accordingly. For example, if a company pays $12,000 annually in advance for rent, $1,000 would be expensed each month, with the prepaid rent asset decreasing by the same amount monthly. This ensures accurate representation of both the expense and the asset on the financial statements.

| Characteristics | Values |

|---|---|

| Classification | Rent paid is typically classified as an operating expense, not directly reflected on the balance sheet. |

| Balance Sheet Impact | Rent payments reduce the cash balance (asset) on the balance sheet. |

| Prepaid Rent | If rent is paid in advance, it is recorded as a prepaid expense (current asset) on the balance sheet until the rental period is consumed. |

| Accrued Rent | If rent is owed but not yet paid, it is recorded as an accrued expense (current liability) on the balance sheet. |

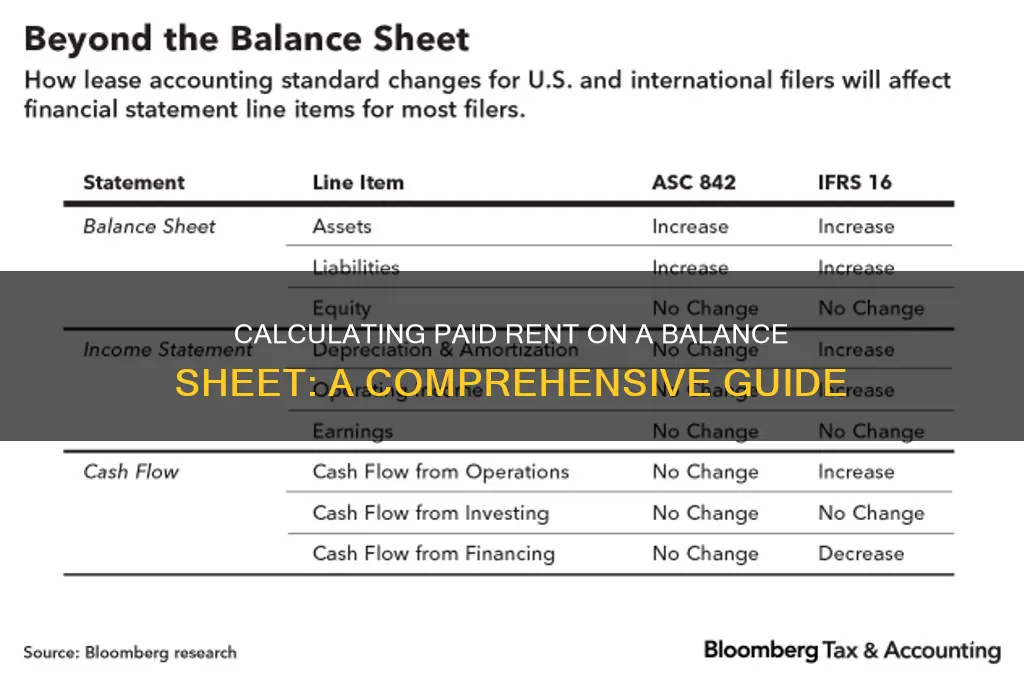

| Lease Accounting (ASC 842/IFRS 16) | For leases, the right-of-use asset and lease liability are recognized on the balance sheet, with rent payments affecting both over time. |

| Expense Recognition | Rent expense is recognized in the income statement in the period it is incurred, regardless of payment timing. |

| Cash Flow Statement | Rent payments are reflected in the operating activities section of the cash flow statement. |

| Tax Treatment | Rent paid is generally tax-deductible as a business expense, reducing taxable income. |

| Disclosure Requirements | Material lease commitments, including future rent payments, must be disclosed in the notes to the financial statements. |

| Frequency of Payment | Rent is typically paid monthly, quarterly, or annually, depending on the lease agreement. |

Explore related products

What You'll Learn

- Rent Accounting Methods: Straight-line vs. accrual basis for recognizing rental expenses over the lease term

- Prepaid Rent Calculation: Unexpired portion of rent paid in advance, recorded as a current asset

- Accrued Rent Expense: Rent incurred but not yet paid, recorded as a current liability

- Lease Classification: Operating vs. finance leases and their impact on rent expense recognition

- Amortization of Rent: Spreading rent expense evenly over the lease period for financial reporting

![]()

Rent Accounting Methods: Straight-line vs. accrual basis for recognizing rental expenses over the lease term

When it comes to recognizing rental expenses over the lease term, businesses have two primary accounting methods to choose from: the straight-line method and the accrual basis method. Each approach has its own advantages and implications for financial reporting, particularly in terms of how paid rent is calculated and presented on a balance sheet. The straight-line method is a straightforward approach that recognizes rental expenses evenly over the lease term, regardless of the actual payment schedule. Under this method, the total rent expense for the lease period is calculated by multiplying the total lease payments by the lease term, then dividing by the number of periods. This results in a consistent rent expense each period, which simplifies budgeting and financial forecasting. For example, if a company signs a 5-year lease with total payments of $500,000, the annual rent expense would be $100,000 ($500,000 / 5 years).

In contrast, the accrual basis method recognizes rental expenses as they are incurred, based on the actual payment schedule outlined in the lease agreement. This approach takes into account any rent escalations, free rent periods, or other variations in the payment schedule. As a result, the rent expense may fluctuate from period to period, reflecting the true cash outflow. For instance, if a lease agreement includes a rent-free period in the first month, followed by escalating payments, the accrual basis method would recognize no rent expense in the first month, followed by increasing expenses in subsequent months. On a balance sheet, the treatment of prepaid or deferred rent differs between the two methods. Under the straight-line method, prepaid rent is recorded as an asset and amortized over the lease term, with a corresponding rent expense recognized each period. The balance sheet would show a prepaid rent asset that decreases over time, while the income statement reflects a consistent rent expense.

The accrual basis method, on the other hand, records rent payments as they are made, with no separate prepaid rent asset. Instead, the rent expense is recognized in the period in which the payment is due, and any prepaid rent is treated as a current asset until the payment is made. This approach provides a more accurate representation of the company's short-term liquidity and cash flow. It's essential to note that the choice between straight-line and accrual basis methods can impact key financial metrics, such as net income, operating cash flow, and return on assets. The straight-line method may result in smoother earnings and more predictable cash flow, while the accrual basis method provides a more accurate picture of the company's financial performance and obligations.

When deciding between the two methods, companies should consider the specific terms of their lease agreements, as well as the requirements of applicable accounting frameworks (e.g., GAAP or IFRS). For example, under ASC 842 (the new lease accounting standard), companies are required to recognize a right-of-use asset and a lease liability on their balance sheets, which may influence the choice of rent accounting method. In practice, some companies may use a combination of both methods, applying the straight-line approach for financial reporting purposes while using the accrual basis method for internal management reporting and cash flow forecasting. Ultimately, the goal is to provide a clear and accurate representation of the company's rental obligations and expenses, enabling stakeholders to make informed decisions.

To illustrate the differences between the two methods, consider a company that signs a 10-year lease with monthly payments of $10,000 for the first 5 years, increasing to $12,000 for the remaining 5 years. Under the straight-line method, the company would recognize a monthly rent expense of $11,000 ($1,200,000 total rent / 120 months), resulting in a consistent expense each period. In contrast, the accrual basis method would recognize $10,000 in rent expense for the first 60 months, followed by $12,000 for the remaining 60 months. The balance sheet treatment would also differ, with the straight-line method showing a prepaid rent asset that decreases over time, while the accrual basis method would reflect the actual cash payments made. By understanding the nuances of each method, companies can make informed decisions about how to recognize and report rental expenses, ensuring compliance with accounting standards and providing a clear picture of their financial health.

Perfect Wedding Photo Booth Rental Duration: Tips for Timing

You may want to see also

Explore related products

![]()

Prepaid Rent Calculation: Unexpired portion of rent paid in advance, recorded as a current asset

Prepaid rent is a common scenario in business accounting where a company pays rent for a property in advance, covering a period that extends beyond the current accounting period. The unexpired portion of this prepaid rent is recorded as a current asset on the balance sheet because it represents a benefit that will be realized within the next 12 months. To calculate prepaid rent, the first step is to determine the total amount of rent paid in advance and identify the portion of that payment that applies to future periods. For example, if a company pays $12,000 for a year’s rent in January, but the accounting period ends in March, $9,000 of that payment ($12,000 - $3,000 for the first three months) is considered prepaid rent and should be recorded as a current asset.

The calculation of prepaid rent involves a straightforward allocation based on time. Divide the total rent payment by the number of months it covers to find the monthly rent amount. Then, multiply this monthly amount by the number of months that fall outside the current accounting period. For instance, if a company pays $6,000 for six months of rent starting in November, and the accounting year ends in December, the prepaid rent would be $5,000 ($1,000 per month × 5 months remaining). This amount is recorded in the prepaid rent account on the balance sheet, while the portion of rent applicable to the current period is expensed.

Recording prepaid rent as a current asset is essential for accurate financial reporting because it reflects the company’s right to use the rented property in the future. When the prepaid rent is initially recorded, the journal entry involves debiting the prepaid rent account (an asset) and crediting cash (or the payment method used). As each month passes, the company adjusts its books by debiting rent expense and crediting prepaid rent for the amount corresponding to that month. This process ensures that expenses are recognized in the period they are incurred, adhering to the matching principle of accounting.

To illustrate, suppose a business pays $18,000 for nine months of rent starting in April, and the fiscal year ends in June. The prepaid rent calculation would be $12,000 ($2,000 per month × 6 months remaining from July to December). The journal entry at the time of payment would be: Debit Prepaid Rent $18,000, Credit Cash $18,000. By June, $6,000 would have been expensed ($2,000 × 3 months), leaving $12,000 as prepaid rent on the balance sheet. This method ensures that the financial statements accurately represent the company’s financial position and the timing of its expenses.

Finally, it’s important to regularly review and adjust prepaid rent accounts to reflect the correct balance. As time progresses and the prepaid rent is consumed, the asset account is reduced, and the corresponding expense is recognized. This ongoing adjustment is typically done through monthly or periodic accounting entries. Proper management of prepaid rent not only ensures compliance with accounting standards but also provides a clear picture of a company’s liquidity and short-term assets. By accurately calculating and recording prepaid rent, businesses can maintain transparency and reliability in their financial reporting.

Renting? Here’s How to Transfer Utilities Bills to Your Name Easily

You may want to see also

Explore related products

![]()

Accrued Rent Expense: Rent incurred but not yet paid, recorded as a current liability

Accrued rent expense is a critical concept in accounting, representing rent that a business has incurred but has not yet paid. This obligation is recorded as a current liability on the balance sheet, reflecting the company’s responsibility to settle the amount in the near term, typically within the next 12 months. The purpose of accruing rent expense is to align the recognition of expenses with the period in which they are incurred, adhering to the accrual accounting principle. This ensures that financial statements accurately reflect the company’s financial position and performance, even if the payment has not yet been made.

To calculate and record accrued rent expense, the business must first determine the amount of rent incurred during the accounting period but not yet paid. For example, if a company’s rent is due on the 1st of each month but the accounting period ends on the 31st, the rent for the days from the 1st to the 31st must be accrued. The formula to calculate accrued rent is straightforward: *Accrued Rent Expense = Daily Rent Rate × Number of Days Incurred*. The daily rent rate is derived by dividing the monthly rent by the number of days in the month. Once calculated, this amount is recorded as a debit to "Rent Expense" on the income statement and a credit to "Accrued Rent" under current liabilities on the balance sheet.

Recording accrued rent expense involves a journal entry that impacts both the income statement and the balance sheet. For instance, if a company’s monthly rent is $5,000 and the accounting period ends 5 days before the rent is due, the accrued rent expense would be calculated as ($5,000 ÷ 30) × 5 = $833.33. The journal entry would debit "Rent Expense" for $833.33 and credit "Accrued Rent" for the same amount. This entry ensures that the expense is recognized in the correct period and that the liability is reflected on the balance sheet until the payment is made.

When the rent is eventually paid, the accrued rent liability is reversed. The payment is recorded by debiting "Accrued Rent" and crediting "Cash," reducing the liability and the cash balance. For example, when the $5,000 rent is paid, the entry would debit "Accrued Rent" for $833.33 (the previously accrued amount) and credit "Cash" for $5,000, with the remaining $4,166.67 ($5,000 - $833.33) debited to "Rent Expense" if the payment covers the next period. This process ensures that the financial statements remain accurate and that expenses are matched with the periods in which they are incurred.

Properly managing accrued rent expense is essential for maintaining the integrity of financial statements and complying with accounting standards. It ensures that liabilities are not understated and that expenses are recognized in the appropriate period, providing a true and fair view of the company’s financial health. By following these steps, businesses can accurately calculate, record, and reverse accrued rent expenses, thereby enhancing the reliability of their financial reporting.

Renting a Food Truck for Your Party: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Lease Classification: Operating vs. finance leases and their impact on rent expense recognition

Lease classification is a critical aspect of financial reporting, particularly under accounting standards like ASC 842 in the United States and IFRS 16 internationally. The classification of a lease as either operating or finance (also known as a capital lease) significantly impacts how rent expense is recognized on a balance sheet and income statement. Understanding these classifications is essential for accurate financial reporting and analysis.

Operating Leases: Under an operating lease, the lessee (tenant) does not recognize the leased asset on their balance sheet. Instead, rent payments are expensed directly on the income statement over the lease term. This treatment reflects that the lessee does not have ownership or control over the asset. For example, if a company pays $1,000 per month for office space under an operating lease, this amount is recorded as a rent expense each month. On the balance sheet, prepaid rent (if any) may be recorded as a current asset, but the leased asset itself is not capitalized. Operating leases are common for short-term or non-essential assets, as they provide flexibility and do not impact the company’s debt-to-equity ratio.

Finance Leases (Capital Leases): In contrast, a finance lease is treated more like a purchase. The lessee recognizes both a right-of-use (ROU) asset and a lease liability on the balance sheet. The ROU asset represents the lessee’s right to use the leased asset, while the lease liability reflects the obligation to make future lease payments. Rent expense is allocated between interest expense (based on the lease liability) and amortization of the ROU asset. For instance, if a company enters a finance lease for equipment with a present value of $50,000, it records an ROU asset and lease liability for $50,000. Each month, a portion of the lease payment reduces the liability (interest expense) and depreciates the ROU asset (amortization expense). This approach aligns with the economic reality of the lease, as the lessee effectively controls the asset.

Impact on Rent Expense Recognition: The classification of a lease directly affects the timing and presentation of rent expense. Operating leases result in a straight-line rent expense, while finance leases separate the expense into interest and amortization components. This distinction is crucial for financial analysis, as it influences metrics like operating income, EBITDA, and leverage ratios. For example, a finance lease increases both assets and liabilities, potentially affecting a company’s financial health indicators, whereas an operating lease has no such impact on the balance sheet.

Determining Lease Classification: Leases are classified based on specific criteria, such as the lease term, the present value of lease payments, and ownership transfer. If a lease meets any of the following conditions, it is classified as a finance lease: the lease term covers a major part of the asset’s economic life, the present value of lease payments is substantially all of the asset’s fair value, the asset is expected to transfer ownership, or the lessee has the option to purchase the asset at a bargain price. If none of these conditions are met, the lease is classified as operating.

In summary, lease classification as operating or finance determines how rent payments are calculated and presented on a balance sheet. Operating leases result in straightforward rent expense recognition, while finance leases involve capitalization of the leased asset and separation of rent expense into interest and amortization. Proper classification ensures compliance with accounting standards and provides a clear picture of a company’s financial obligations and asset usage.

Discovering Your Perfect Honolulu Rental: Tips for Finding Apartments

You may want to see also

Explore related products

![]()

Amortization of Rent: Spreading rent expense evenly over the lease period for financial reporting

Amortization of rent is a critical accounting practice that ensures rent expenses are recognized evenly over the lease period, providing a more accurate representation of a company’s financial health. When rent is paid, it is not immediately expensed in full; instead, it is spread out over the duration of the lease. This approach aligns with the matching principle in accounting, which requires expenses to be recognized in the same period as the revenues they help generate. For example, if a company pays $12,000 annually for a 12-month lease, the rent expense would be recognized as $1,000 per month on the income statement, rather than $12,000 in a single month.

On the balance sheet, prepaid rent is initially recorded as a current asset when the payment is made. This reflects the fact that the company has paid for a benefit that will be consumed over time. As each month passes, a portion of the prepaid rent is transferred to the rent expense account, reducing the asset balance. This process continues until the prepaid rent is fully amortized. For instance, if a company prepays $6,000 for a six-month lease, $1,000 would be expensed each month, and the prepaid rent asset would decrease by the same amount monthly.

The amortization of rent also impacts the income statement and cash flow statement. On the income statement, the rent expense is reported under operating expenses, reflecting the cost of using the leased property. On the cash flow statement, the initial rent payment is recorded as a cash outflow under operating activities, but the subsequent amortization does not affect cash flows since it is a non-cash expense. This distinction ensures that the cash flow statement accurately reflects the movement of cash, while the income statement provides a clear picture of periodic expenses.

To calculate amortized rent, accountants use a straightforward method. The total rent paid is divided by the number of periods (usually months) in the lease term. For example, if a company pays $18,000 for a 12-month lease, the monthly rent expense would be $1,500. This calculation ensures consistency and fairness in financial reporting, as it avoids distorting the company’s profitability in any single period. Proper amortization is essential for compliance with accounting standards like GAAP or IFRS, which require leases to be treated in this manner.

Finally, amortization of rent is particularly important for long-term leases, where prepaying rent upfront is common. Without amortization, a company’s financial statements could misleadingly show a significant expense in one period and none in others. By spreading the expense evenly, amortization provides stakeholders with a more accurate and reliable view of the company’s financial performance and obligations. This practice is fundamental to maintaining transparency and integrity in financial reporting.

Renting Show Series on Dish: A Step-by-Step Guide for Subscribers

You may want to see also

Frequently asked questions

Paid rent is typically recorded as a prepaid expense on the balance sheet if it covers a future period. If the rent payment is for the current period, it is expensed on the income statement and does not appear on the balance sheet.

Prepaid rent is recorded under the "Prepaid Expenses" or "Current Assets" section of the balance sheet, as it represents a future benefit that will be used within one year.

The amount of prepaid rent is calculated by determining the portion of the rent payment that applies to future periods. For example, if a year’s rent is paid in advance, the unused portion is prorated and recorded as prepaid rent.

No, if the rent payment is for the current period, it is recognized as an expense on the income statement and does not impact the balance sheet. Only prepaid rent for future periods is recorded on the balance sheet.

Prepaid rent is adjusted monthly or periodically to reflect the portion of the prepaid amount that has been used. This is done through an adjusting entry, reducing the prepaid rent asset and increasing the rent expense.

![Adams Residential Lease, Forms and Instructions [Print and Downloadable] (LF310)](https://m.media-amazon.com/images/I/81uP3OCk9qL._AC_UL320_.jpg)