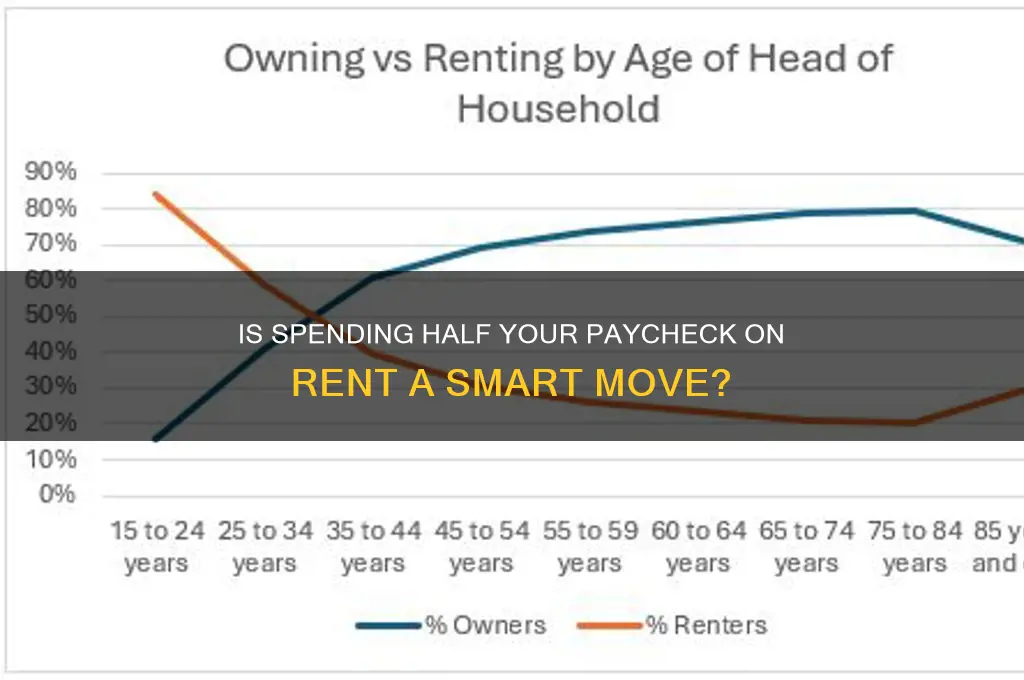

Many individuals, especially those living in high-cost urban areas, often find themselves questioning whether allocating half of their paycheck to rent is financially sustainable. This dilemma arises from the rising cost of housing, stagnant wages, and the need to balance other essential expenses like groceries, utilities, and savings. While some financial experts suggest that rent should not exceed 30% of one's income, the reality for many is that this threshold is increasingly difficult to meet. As a result, renters are forced to weigh the trade-offs between living in a desirable location, maintaining a decent standard of living, and securing their long-term financial stability. This raises important questions about budgeting, prioritizing expenses, and the broader implications of housing affordability on personal and economic well-being.

| Characteristics | Values |

|---|---|

| General Rule | Spending more than 30% of income on rent is considered financially risky. |

| 50% Rule | Spending half your paycheck on rent leaves limited funds for other essentials and savings. |

| Financial Strain | High rent-to-income ratio increases risk of debt, inability to save, and financial instability. |

| Location Impact | In high-cost areas (e.g., NYC, SF), 50% may be common but still risky. |

| Budgeting Challenges | Leaves ~20-25% for necessities (food, utilities, transportation) and minimal savings. |

| Expert Advice | Financial advisors recommend reducing rent burden by finding cheaper housing, increasing income, or relocating. |

| Emergency Risk | Little to no buffer for unexpected expenses (e.g., medical bills, car repairs). |

| Long-Term Goals | Hinders ability to save for retirement, emergencies, or major purchases (e.g., home, education). |

| Psychological Impact | Chronic stress and anxiety from financial instability. |

| Alternative Solutions | Roommates, subsidized housing, or relocating to lower-cost areas can reduce rent burden. |

Explore related products

What You'll Learn

- Affordable Rent Standards: Guidelines on ideal rent-to-income ratios for financial stability

- Budgeting Tips: Strategies to manage expenses when rent consumes half your income

- Alternatives to High Rent: Exploring shared housing, suburbs, or negotiation options

- Long-Term Financial Impact: How high rent affects savings, debt, and future goals

- When to Move: Signs it’s time to find cheaper housing for better finances?

![]()

Affordable Rent Standards: Guidelines on ideal rent-to-income ratios for financial stability

Spending half your paycheck on rent is a red flag for financial stability. This ratio leaves little room for essentials like groceries, utilities, transportation, and savings, let alone discretionary spending. Financial experts widely agree that allocating more than 30% of your gross income to housing is risky. This 30% rule, established by the U.S. Department of Housing and Urban Development (HUD), serves as a benchmark for affordability. Exceeding this threshold increases the likelihood of financial strain, making it difficult to cover unexpected expenses or build wealth over time.

To illustrate, consider a single individual earning $4,000 monthly. Allocating 30% to rent ($1,200) leaves $2,800 for other expenses. In contrast, spending 50% ($2,000) on rent reduces the remaining budget to $2,000, significantly limiting flexibility. For households with multiple earners or dependents, the impact is even more pronounced. A family of four earning $6,000 monthly, spending half on rent ($3,000), would struggle to meet basic needs, let alone save for emergencies or long-term goals like education or retirement.

However, the 30% rule isn’t one-size-fits-all. Factors like location, income level, and personal circumstances play a role. In high-cost cities like San Francisco or New York, where median rents exceed $3,000, adhering to this guideline may be unrealistic. In such cases, a 40-45% ratio might be more feasible, but only if accompanied by strict budgeting in other areas. For instance, reducing dining out, subscription services, or non-essential purchases can offset higher rent costs. Additionally, individuals with high incomes may comfortably allocate more to housing without compromising financial stability, provided they maintain substantial savings and investments.

To determine your ideal rent-to-income ratio, follow these steps: 1. Calculate your monthly gross income. 2. Multiply this figure by 30% to establish a baseline affordable rent. 3. Assess your total monthly expenses, including debt payments, utilities, groceries, and savings goals. 4. Adjust the rent allocation if necessary, ensuring it doesn’t exceed 40% in high-cost areas. 5. Build an emergency fund equivalent to 3-6 months’ expenses to buffer against unforeseen circumstances. For example, if your monthly income is $3,500, aim for rent under $1,050 (30%), but if you live in an expensive city, consider up to $1,400 (40%), while cutting discretionary spending to maintain balance.

Ultimately, while spending half your paycheck on rent may be unavoidable in certain situations, it’s unsustainable for long-term financial health. Prioritize finding housing that aligns with the 30% rule, or take proactive steps to increase income or reduce expenses. Tools like budgeting apps, roommate arrangements, or relocating to more affordable areas can help. Remember, affordable rent isn’t just about the number—it’s about creating a foundation for financial stability and future prosperity.

Renting a Workbench in Crossout Xbox One: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Budgeting Tips: Strategies to manage expenses when rent consumes half your income

Spending half your income on rent leaves little room for other essentials, let alone savings or leisure. This scenario forces a reevaluation of spending habits and a strategic approach to budgeting. The 50/30/20 rule, a popular budgeting framework, suggests allocating 50% of income to needs, 30% to wants, and 20% to savings. However, when rent alone consumes half your paycheck, this rule becomes impractical. Instead, a more tailored approach is necessary to ensure financial stability and avoid debt.

Prioritize Needs Over Wants: A Practical Shift

Begin by distinguishing between needs and wants. Needs include utilities, groceries, transportation, and insurance—essentials for daily living. Wants, such as dining out, subscriptions, or entertainment, should be minimized or eliminated temporarily. For instance, cutting back on $5 daily coffee runs saves $150 monthly, which could cover a utility bill. Use a budgeting app like Mint or YNAB to track expenses and identify areas for reduction. This shift requires discipline but ensures that limited funds are allocated to what truly matters.

Negotiate and Optimize Fixed Expenses: Small Changes, Big Impact

Fixed expenses, like rent, are often non-negotiable, but other fixed costs can be optimized. For example, shop around for cheaper car insurance, switch to a lower-cost phone plan, or negotiate bills like cable or internet. Many providers offer discounts for loyal customers or those willing to bundle services. Additionally, consider downsizing to a more affordable living situation if possible, even if it means sharing space or moving to a less expensive neighborhood. These adjustments free up funds for other necessities or savings.

Build an Emergency Fund: A Safety Net for Uncertainty

Living paycheck to paycheck with half your income going to rent leaves no buffer for unexpected expenses. Start building an emergency fund, even if it’s just $20 a month. Aim for $500 initially, then gradually increase to cover 3–6 months of essential expenses. This fund prevents reliance on high-interest credit cards or loans during emergencies. Automate savings by setting up a direct deposit into a separate account, making it easier to save consistently without feeling the pinch.

Increase Income: A Long-Term Solution

While cutting expenses is crucial, increasing income provides more financial flexibility. Explore side gigs like freelancing, tutoring, or driving for ride-share services. For example, dedicating 10 hours weekly to a side job earning $20/hour adds $800 monthly, significantly easing financial strain. Alternatively, seek opportunities for overtime or a raise at your current job. Even a modest income boost can reduce the proportion of your paycheck going to rent and create room for savings or leisure.

Managing expenses when rent consumes half your income requires a combination of frugality, creativity, and proactive planning. By prioritizing needs, optimizing fixed costs, building an emergency fund, and increasing income, you can regain control over your finances and work toward a more stable future.

For Sale vs. For Rent: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Alternatives to High Rent: Exploring shared housing, suburbs, or negotiation options

Spending half your paycheck on rent is a recipe for financial stress. It leaves little room for savings, emergencies, or simply enjoying life. But before resigning yourself to this reality, consider these alternatives: shared housing, suburban living, and strategic negotiation. Each option offers a path to reclaiming control over your budget.

Sharing your living space isn't just for college students. Platforms like Craigslist, Facebook Marketplace, and specialized co-living websites connect you with potential roommates. Think beyond the traditional roommate setup – consider intergenerational housing, where younger renters share space with older homeowners, offering companionship and reduced costs for both parties. When vetting roommates, prioritize compatibility in lifestyle, cleanliness, and financial responsibility. Draft a clear roommate agreement outlining rent, utilities, guest policies, and conflict resolution procedures.

Suburban living often conjures images of sprawling lawns and long commutes. However, many suburbs now offer vibrant communities, excellent schools, and surprisingly affordable housing. Research areas with good public transportation access to minimize commuting costs. Consider the trade-off between a larger living space and potentially higher transportation expenses. Look for suburbs with thriving local economies, offering job opportunities closer to home. Don't underestimate the value of a shorter commute – it can significantly improve your work-life balance and overall well-being.

Before resigning yourself to a high rent, negotiate. Research comparable rentals in the area to understand the market rate. Highlight your strengths as a tenant – timely rent payments, a stable income, and a clean rental history. Propose a longer lease term in exchange for a lower monthly rent. Offer to take care of minor maintenance tasks yourself, reducing the landlord's burden. Be prepared to walk away if the landlord is unwilling to budge. Remember, negotiation is a dialogue, not a confrontation. Approach it with confidence and a willingness to compromise.

Renting a One-Man Auger in Galesburg, Illinois: Top Locations

You may want to see also

Explore related products

![]()

Long-Term Financial Impact: How high rent affects savings, debt, and future goals

Spending half your paycheck on rent isn’t just a monthly strain—it’s a long-term financial anchor. When 50% of your income goes to housing, your ability to save diminishes drastically. For instance, if you earn $4,000 monthly and pay $2,000 in rent, you’re left with $2,000 for all other expenses. Assuming $1,200 goes to essentials like groceries, transportation, and utilities, you’re left with $800. Now, factor in unexpected costs like medical bills or car repairs, and your savings potential shrinks further. Over a decade, this pattern could mean missing out on $96,000 in potential savings—enough for a down payment on a house or a substantial retirement fund. The takeaway? High rent doesn’t just eat your present income; it devours your future financial security.

Let’s talk debt. When rent consumes half your paycheck, you’re more likely to rely on credit cards or loans to cover gaps. Say you need $300 for a car repair but only have $100 left in your budget. That $200 charged to a credit card at 18% APR becomes $236 if paid off over a year. Multiply these scenarios over time, and high rent becomes a catalyst for mounting debt. A study by the Urban Institute found that renters spending over 30% of their income on housing are twice as likely to carry credit card debt. Worse, this debt can lower your credit score, making it harder to secure favorable loans for future goals like buying a home or starting a business. High rent isn’t just a housing issue—it’s a debt accelerator.

Now, consider future goals. If you’re 25 and spending half your paycheck on rent, you’re delaying critical milestones. For example, saving for a 20% down payment on a $300,000 home requires $60,000. At $800 monthly savings, it would take you 6.25 years to reach that goal. But if you could reduce rent to 30% of your income, freeing up an extra $600 monthly, you’d hit $60,000 in just 2.7 years. High rent doesn’t just postpone homeownership; it delays retirement savings, education funds, and entrepreneurial ventures. Every dollar spent on rent above 30% of your income is a dollar not invested in your future self.

Here’s a practical strategy to mitigate the damage: the 50/30/20 rule adapted for high-rent scenarios. Allocate 50% of your income to needs (including rent), but aim to reduce housing costs to 30% within 12 months. Redirect the freed-up funds to savings (20%) and wants (30%). For example, if you’re paying $2,000 in rent on a $4,000 income, find a $1,200 rental instead. The extra $800 monthly could go toward an emergency fund, retirement account, or debt repayment. Additionally, negotiate rent reductions, consider roommates, or move to a more affordable area. High rent isn’t irreversible—it’s a challenge to strategize against.

Finally, let’s compare outcomes. Imagine two individuals earning $50,000 annually. Person A spends $25,000 on rent, while Person B spends $15,000. Over 10 years, Person A saves $50,000 (assuming $5,000 annual savings), while Person B saves $170,000. Person B not only builds a larger safety net but also gains financial flexibility to pursue opportunities like investing in stocks or real estate. High rent isn’t just a monthly expense—it’s a fork in the road between financial struggle and prosperity. The choice is clear: prioritize reducing rent to reclaim your financial future.

Peak Rental Seasons: When Most Places Are Up for Lease

You may want to see also

Explore related products

![]()

When to Move: Signs it’s time to find cheaper housing for better finances

Spending half your paycheck on rent is a red flag, not a badge of honor. It's a clear sign your housing costs are devouring your financial stability. The 30% rule, a widely accepted guideline, suggests rent should consume no more than 30% of your gross income. Exceeding this threshold leaves little room for essentials like food, transportation, and savings, let alone building wealth or handling emergencies.

If you're constantly juggling bills, dipping into savings, or relying on credit cards to make ends meet, it's time to seriously consider a move.

Let's break down the warning signs. First, examine your budget. Are you consistently overspending in other areas to compensate for high rent? Do you have minimal savings or struggle to contribute to retirement accounts? Second, assess your lifestyle. Are you sacrificing experiences, hobbies, or basic comforts due to rent burden? Finally, consider your future goals. Is your current housing situation hindering your ability to save for a down payment, invest, or achieve financial independence? If you answered yes to any of these, it's a strong indicator that cheaper housing is a necessary step towards financial health.

Remember, downsizing or relocating doesn't equate to failure. It's a strategic decision to prioritize long-term financial well-being over short-term comfort.

The process of finding cheaper housing requires a multi-pronged approach. Start by evaluating your needs versus wants. Can you live with a smaller space, a less trendy neighborhood, or fewer amenities? Research affordable areas, considering factors like commute time, access to public transportation, and local amenities. Explore options like roommates, co-living spaces, or rent-controlled units. Negotiate rent with your current landlord, highlighting your reliability as a tenant. Finally, consider a temporary living situation, like staying with family or friends, while you save for a more permanent solution.

Moving to cheaper housing isn't just about cutting costs; it's about reclaiming control over your finances. It allows you to build a safety net, invest in your future, and pursue your goals without the constant weight of rent anxiety. Remember, financial freedom is a journey, and sometimes, the first step is finding a more affordable place to call home.

Understanding Standard Garnish Amounts for Back Rent: A Comprehensive Guide

You may want to see also

Frequently asked questions

It depends on your overall budget and financial goals. Generally, spending more than 30% of your income on rent is considered high, so 50% may leave little room for other expenses and savings.

Calculate your monthly income and expenses. If after rent, you can comfortably cover essentials like groceries, utilities, transportation, and savings, it might be manageable. Otherwise, it’s likely unsustainable.

Yes, allocating 50% of your income to rent increases the risk of financial strain, especially in emergencies. It may also limit your ability to save for retirement, build an emergency fund, or pay off debt.

Consider finding a more affordable place, getting a roommate to split costs, or increasing your income through a side job or raise. Budgeting tools can also help optimize your spending.

Directly, no—rent payments typically don’t impact your credit score unless reported to credit bureaus. However, high rent can lead to missed payments on other bills, which can negatively affect your credit.